Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- CH13 Trial Balance 12.31.26Document1 pageCH13 Trial Balance 12.31.26Crystal TelaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 5325702-Strategic-Management-Assignment-1758476635-1307697674 - 1894915866 .EdiDocument24 pages5325702-Strategic-Management-Assignment-1758476635-1307697674 - 1894915866 .EdiSparsh Sharma100% (1)

- Income and Changes in Retained Earnings: - Chapter 12Document49 pagesIncome and Changes in Retained Earnings: - Chapter 12Moqadus SeharNo ratings yet

- ASSIGNMENTDocument5 pagesASSIGNMENTTushar GuptaNo ratings yet

- Financcial LiteracyDocument3 pagesFinanccial LiteracyTushar GuptaNo ratings yet

- 3525 25113 Textbooksolution PDFDocument40 pages3525 25113 Textbooksolution PDFTushar Gupta100% (1)

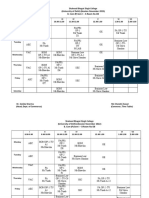

- Revised B. Com (PGM) Sem-I Time Table 2022 24.12.2022Document4 pagesRevised B. Com (PGM) Sem-I Time Table 2022 24.12.2022Tushar GuptaNo ratings yet

- Faq 1203Document11 pagesFaq 1203Tushar GuptaNo ratings yet

- Functional Areas of ManagementDocument74 pagesFunctional Areas of ManagementTushar GuptaNo ratings yet

- Bcom I Fa 103 MCQSDocument11 pagesBcom I Fa 103 MCQSTushar GuptaNo ratings yet

- BCOM Preference List For DUDocument1 pageBCOM Preference List For DUTushar GuptaNo ratings yet

- List of Ug Programmes 2022 23 With EligibilityDocument6 pagesList of Ug Programmes 2022 23 With EligibilityTushar GuptaNo ratings yet

- Case Studies On ODDocument3 pagesCase Studies On ODAnonymous KK3PrbNo ratings yet

- Share CapitalDocument67 pagesShare Capitalayushmaharaj68No ratings yet

- Value Creation: It Solves The Massive Problem of Employees Having ToDocument2 pagesValue Creation: It Solves The Massive Problem of Employees Having Toindukana PaulNo ratings yet

- Neugene Marketing vs. CADocument1 pageNeugene Marketing vs. CAGlen MaullonNo ratings yet

- 8ed TB SampleDocument18 pages8ed TB SampleEdenA.MataNo ratings yet

- The Analytics Stack GuidebookDocument187 pagesThe Analytics Stack GuidebookVFisa67% (3)

- Derivados Avanzados-Francisco DelgadoDocument486 pagesDerivados Avanzados-Francisco DelgadoPablo Cosar100% (1)

- Solution Manual For Operations and Supply Chain Management 2nd Edition David Alan Collier James R Evans Full DownloadDocument37 pagesSolution Manual For Operations and Supply Chain Management 2nd Edition David Alan Collier James R Evans Full Downloaddavidrothanpyjtmfkw100% (44)

- Ethics in Information Technology, Fourth Edition: Ethics of IT OrganizationsDocument65 pagesEthics in Information Technology, Fourth Edition: Ethics of IT Organizationshassan tariqNo ratings yet

- Unit 2 Project ManagementDocument98 pagesUnit 2 Project ManagementSita RamNo ratings yet

- Folleto de Las Características Del Programa de FormaciónDocument2 pagesFolleto de Las Características Del Programa de FormaciónacilegnaNo ratings yet

- CA 2 Assignment BBA 601 - Project ManagementDocument7 pagesCA 2 Assignment BBA 601 - Project ManagementSonali ChoudharyNo ratings yet

- Lab1-5 YourBank CRM SRS v1.0.1 PDFDocument86 pagesLab1-5 YourBank CRM SRS v1.0.1 PDFNhân NguyễnNo ratings yet

- Khan Sanction LetterDocument7 pagesKhan Sanction LetterArman KhanNo ratings yet

- CFO Dashboards and Business IntelligenceDocument8 pagesCFO Dashboards and Business IntelligenceCasino Marketeer100% (1)

- Flow Chart of Export of PulpDocument8 pagesFlow Chart of Export of Pulpsoniachawla9No ratings yet

- Brochure TeraVialDocument2 pagesBrochure TeraVialwlukumanNo ratings yet

- Business Analytics 2nd Edition Evans Test BankDocument15 pagesBusiness Analytics 2nd Edition Evans Test BankMrNicolasGuerraJrnsadz100% (64)

- TX NotesDocument157 pagesTX Notessahalacca123No ratings yet

- Business Marketing Management-WDDocument81 pagesBusiness Marketing Management-WDMaruko ChanNo ratings yet

- Urban Ladder Vs Pepperfry 2Document10 pagesUrban Ladder Vs Pepperfry 2Sabhay ChoudharyNo ratings yet

- DownloadDocument91 pagesDownloadVijayendran PNo ratings yet

- Performance Analysis - NBFCS - IndiaDocument55 pagesPerformance Analysis - NBFCS - IndiaRajeev RsNo ratings yet

- Prisma Deal Making Guidelines: For Private Sector PartnersDocument32 pagesPrisma Deal Making Guidelines: For Private Sector PartnersFarai MandisodzaNo ratings yet

- Himanshu Aggarwal: Mobile: 8882345013Document5 pagesHimanshu Aggarwal: Mobile: 8882345013himanshu chritianNo ratings yet

- Augustus Softwares Company ProfileDocument5 pagesAugustus Softwares Company ProfileKanishk SinghNo ratings yet

- Strategic Management : Gregory G. Dess and G. T. LumpkinDocument19 pagesStrategic Management : Gregory G. Dess and G. T. LumpkinJeramz QuijanoNo ratings yet