Download as pdf or txt

You might also like

- Apparel Liquidation Companies PDFDocument12 pagesApparel Liquidation Companies PDFtarekZADNo ratings yet

- Audit Procedure On Expenses - PDFDocument14 pagesAudit Procedure On Expenses - PDF黄勇添No ratings yet

- Chapter 4 - Present Worth AnalysisDocument8 pagesChapter 4 - Present Worth AnalysisSandipNo ratings yet

- DPA50163 Sesi 2 2021 - 2022Document26 pagesDPA50163 Sesi 2 2021 - 2022黄勇添No ratings yet

- 01 Quiz 1Document2 pages01 Quiz 1anna mae orcioNo ratings yet

- Appendix F: Accounting For PartnershipsDocument17 pagesAppendix F: Accounting For PartnershipsDerian Wijaya100% (1)

- Fin22 Cash Flow and LevarageDocument3 pagesFin22 Cash Flow and LevarageJoeNo ratings yet

- Group Assignment - China US Trade WarDocument27 pagesGroup Assignment - China US Trade WarEileen OngNo ratings yet

- Financial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Document12 pagesFinancial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Joel Christian MascariñaNo ratings yet

- 57 International Financial Reporting Standards May 2022Document8 pages57 International Financial Reporting Standards May 2022premium info2222No ratings yet

- FAR-2 Mock September 2021 FinalDocument8 pagesFAR-2 Mock September 2021 FinalMuhammad RahimNo ratings yet

- Mba 4 Sem Fa Project Planning Appraisal and Control K 580 Oct 2020Document2 pagesMba 4 Sem Fa Project Planning Appraisal and Control K 580 Oct 2020Vampire KNo ratings yet

- Bangalore University Previous Year Question Paper AFM 2020Document3 pagesBangalore University Previous Year Question Paper AFM 2020Ramakrishna NagarajaNo ratings yet

- f9 2018 Marjun QDocument6 pagesf9 2018 Marjun QDilawar HayatNo ratings yet

- 01 Quiz 1 11Document2 pages01 Quiz 1 11claudia smithNo ratings yet

- CHRIST (Deemed To Be University), Bengaluru - 560 029: BIF431 - Page 1 of 9Document9 pagesCHRIST (Deemed To Be University), Bengaluru - 560 029: BIF431 - Page 1 of 9Arpit SharmaNo ratings yet

- Cib GH 04-23 Financial Reporting, Planning & Analysis Level Iii Page 1Document8 pagesCib GH 04-23 Financial Reporting, Planning & Analysis Level Iii Page 1lilliananne5051No ratings yet

- Paper20A Set2Document8 pagesPaper20A Set2Ramanpreet KaurNo ratings yet

- ACC030 Comprehensive Project April2018 (Q)Document5 pagesACC030 Comprehensive Project April2018 (Q)Fatin AkmalNo ratings yet

- Far670 - Sept 2020Q - SuppDocument4 pagesFar670 - Sept 2020Q - SuppnurulsyafiqahNo ratings yet

- FAR ND-2023 QuestionDocument4 pagesFAR ND-2023 QuestionMd HasanNo ratings yet

- Accountancy Sample Question PaperDocument8 pagesAccountancy Sample Question PaperSoNam ZaNgmoNo ratings yet

- Question 1288284Document11 pagesQuestion 1288284groverpankaj04No ratings yet

- CPAR MAS Preweek - May 2005 EditionDocument47 pagesCPAR MAS Preweek - May 2005 EditionIvhy Cruz Estrella100% (5)

- Final (Question) BTM 4103 Financial Accounting IDocument3 pagesFinal (Question) BTM 4103 Financial Accounting ITasfia MeherNo ratings yet

- R2.TAXM - .L Question CMA June 2021 Exam.Document7 pagesR2.TAXM - .L Question CMA June 2021 Exam.Pavel DhakaNo ratings yet

- Financial Management 2016Document2 pagesFinancial Management 2016Riya AgrawalNo ratings yet

- Paper 4 Taxation May 12Document12 pagesPaper 4 Taxation May 12raviNo ratings yet

- Group I Nov.2010Document111 pagesGroup I Nov.2010anand003No ratings yet

- Question Paper Unsolved - Special Study in FinanceDocument18 pagesQuestion Paper Unsolved - Special Study in FinanceAbhijeet KulshreshthaNo ratings yet

- Final Exam, s2, 2019-FINALDocument13 pagesFinal Exam, s2, 2019-FINALReenalNo ratings yet

- 5302 Facgdse02t L 4Document4 pages5302 Facgdse02t L 4piyousshil13No ratings yet

- Advanced Accounting 2eDocument3 pagesAdvanced Accounting 2eHarusiNo ratings yet

- Time: 3 Hours Total Marks: 100: Printed Pages:03 Sub Code: KMB 204/KMT 204 Paper Id: 270244 Roll NoDocument3 pagesTime: 3 Hours Total Marks: 100: Printed Pages:03 Sub Code: KMB 204/KMT 204 Paper Id: 270244 Roll NoHimanshuNo ratings yet

- Chapter 1 To 8 Practice Problem SolutionsDocument120 pagesChapter 1 To 8 Practice Problem SolutionsHardeep Kaur100% (1)

- Quiz 2 Lesson 3Document5 pagesQuiz 2 Lesson 3Andreau Granada0% (1)

- May 2013 Advanced TaxationDocument4 pagesMay 2013 Advanced TaxationTIMOREGHNo ratings yet

- She Bsa 4-2Document7 pagesShe Bsa 4-2Justine GuilingNo ratings yet

- PGDM D - Corp ValDocument2 pagesPGDM D - Corp Valsanket patilNo ratings yet

- Model Questions BBS 3rd Year Fundamental of Financial Management PDFDocument9 pagesModel Questions BBS 3rd Year Fundamental of Financial Management PDFShah SujitNo ratings yet

- ITL&P - Assignment 2Document3 pagesITL&P - Assignment 2Yashika JainNo ratings yet

- PGDT Assignment QP TEE Jun18Document10 pagesPGDT Assignment QP TEE Jun18abhishekchavda20No ratings yet

- Statement of Comprehensive Income Test BankDocument4 pagesStatement of Comprehensive Income Test BankJhazz0% (1)

- LiabilitiesDocument2 pagesLiabilitiesFrederick AbellaNo ratings yet

- Management Accounting For Financial ServicesDocument2 pagesManagement Accounting For Financial ServicesJAVEDNo ratings yet

- II PUC ACC REVISED POQs FOR 2022-23Document3 pagesII PUC ACC REVISED POQs FOR 2022-23Shree Lakshmi vNo ratings yet

- Acco 1115Document9 pagesAcco 1115Sarah RanduNo ratings yet

- CO3CRT07 - Corporate Accounting I (T)Document5 pagesCO3CRT07 - Corporate Accounting I (T)shemymuhammad289No ratings yet

- Eco 02Document6 pagesEco 02rykaNo ratings yet

- This Test Is Only For Students of MS Consultancy ManagementDocument2 pagesThis Test Is Only For Students of MS Consultancy ManagementrudypatilNo ratings yet

- Eqps - Structured QuestionsDocument5 pagesEqps - Structured QuestionsamirahNo ratings yet

- Tayo RollsDocument7 pagesTayo RollsAkhil ChaudharyNo ratings yet

- ACCT6003 Assessment 2 T1 2020 Brief PDFDocument7 pagesACCT6003 Assessment 2 T1 2020 Brief PDFbhavikaNo ratings yet

- Accounting NSC P1 Memo Nov 2022 EngDocument12 pagesAccounting NSC P1 Memo Nov 2022 EngItumeleng MogoleNo ratings yet

- Pathfinder Pei Nov2010Document118 pagesPathfinder Pei Nov2010Idogun Olufemi Ezekiel100% (1)

- 2022 FIA132 Term Test 1 FinalDocument9 pages2022 FIA132 Term Test 1 FinalkaityNo ratings yet

- Salary StructureDocument1 pageSalary Structureomer farooqNo ratings yet

- P5 Adv Ac Ans Nov 23 Exam @CAInterLegendsDocument31 pagesP5 Adv Ac Ans Nov 23 Exam @CAInterLegendsramjeshyadav107No ratings yet

- Uts MK Mei 2021 PascaDocument2 pagesUts MK Mei 2021 PascaDwiayu WidyastutiNo ratings yet

- Sample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To InstallDocument45 pagesSample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To Installumangsingh054No ratings yet

- Chapter 1 QuizDocument6 pagesChapter 1 Quizhantu hantuNo ratings yet

- MMPC-004 Dec 2021-June 2023Document16 pagesMMPC-004 Dec 2021-June 2023sydatharNo ratings yet

- Week1 Assignment1Document8 pagesWeek1 Assignment1kireeti415No ratings yet

- Acc Gr11 March 2022 QP and MemoDocument20 pagesAcc Gr11 March 2022 QP and Memonxumalothandolwethu1No ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Topic 5 - Code of Ethics For AuditorsDocument39 pagesTopic 5 - Code of Ethics For Auditors黄勇添No ratings yet

- Slide Impact It On Audit Process - LatestDocument48 pagesSlide Impact It On Audit Process - Latest黄勇添No ratings yet

- Chapter 4 Information Technology ItDocument63 pagesChapter 4 Information Technology It黄勇添No ratings yet

- Slide Audit ReportDocument37 pagesSlide Audit Report黄勇添No ratings yet

- Chapter 3 Audit Report Isa 700 and Isa 705 Dpa50153Document48 pagesChapter 3 Audit Report Isa 700 and Isa 705 Dpa50153黄勇添No ratings yet

- Chapter 1 (Updated) - Audit On Financial StatementDocument100 pagesChapter 1 (Updated) - Audit On Financial Statement黄勇添No ratings yet

- Chapter 3 - Sesi 1 2022 2023Document42 pagesChapter 3 - Sesi 1 2022 2023黄勇添No ratings yet

- Audit On RevenueDocument27 pagesAudit On Revenue黄勇添No ratings yet

- Slide Audit ProcessDocument15 pagesSlide Audit Process黄勇添No ratings yet

- Slide Audit On Revenue - Latest - 1Document22 pagesSlide Audit On Revenue - Latest - 1黄勇添No ratings yet

- Sesi Jun 2018Document16 pagesSesi Jun 2018黄勇添No ratings yet

- Dpa5033 - Malaysian Taxation 2 Dis 2018Document22 pagesDpa5033 - Malaysian Taxation 2 Dis 2018黄勇添No ratings yet

- Prototype Courier ChargesDocument16 pagesPrototype Courier ChargesDeepak BhanjiNo ratings yet

- Cost Accounting OMDocument26 pagesCost Accounting OMJohn CenaNo ratings yet

- ABDUL BASHIR - ASEAN-FTA Impact On Rubber and Crude Palm Oil Export An Empirical Evidence From IMT Countries - EPDocument15 pagesABDUL BASHIR - ASEAN-FTA Impact On Rubber and Crude Palm Oil Export An Empirical Evidence From IMT Countries - EPABDUL BASHIRNo ratings yet

- Africans' Contribution To Science: A Culture of ExcellenceDocument10 pagesAfricans' Contribution To Science: A Culture of ExcellenceheheNo ratings yet

- Oliva Customer Registration FormDocument10 pagesOliva Customer Registration FormRama UmbaraNo ratings yet

- Group 1: Aditya Waghela 25 Sanika Raut 62 Mehul Bari 81Document8 pagesGroup 1: Aditya Waghela 25 Sanika Raut 62 Mehul Bari 81mehul bariNo ratings yet

- Solved Problems in Engineering Economy 2016 - CompressDocument61 pagesSolved Problems in Engineering Economy 2016 - CompressCol. Jerome Carlo Magmanlac, ACP100% (1)

- Group 1 Market Integration HandoutDocument28 pagesGroup 1 Market Integration HandoutTIMOTHY MELCHOR BALTAZAR. GASPARNo ratings yet

- InvoiceDocument1 pageInvoiceTejinder Singh Lakhwani (P20MS008)No ratings yet

- Level 3 ABC 2021Document54 pagesLevel 3 ABC 2021Ami KayNo ratings yet

- Biswajit Nag and Pratiksha ChaturvediDocument18 pagesBiswajit Nag and Pratiksha ChaturvediPARUL SINGH MBA 2019-21 (Delhi)No ratings yet

- Tax Invoice Aditya Birla Fashion and Retail Limited Fred PerryDocument2 pagesTax Invoice Aditya Birla Fashion and Retail Limited Fred PerrybidikajyotiNo ratings yet

- TC AR Form 1 APPLICATION FOR ADVANCE RULING PDFDocument6 pagesTC AR Form 1 APPLICATION FOR ADVANCE RULING PDFHarrenNo ratings yet

- International BusinessDocument14 pagesInternational Businesssaloni singhNo ratings yet

- 04 - Claims For Excise Tax Refund InquiryDocument6 pages04 - Claims For Excise Tax Refund InquiryAhyz DyNo ratings yet

- MBA R02 Retail Mangement & Franchising - Layout 1 - CompressedDocument106 pagesMBA R02 Retail Mangement & Franchising - Layout 1 - CompressedRajni BharadwazNo ratings yet

- International Finance SyllabusDocument5 pagesInternational Finance Syllabussarathbabu_zeeNo ratings yet

- Estatement20221213 000475984Document10 pagesEstatement20221213 000475984AHMAD HAFIZUDDIN BIN HASHIM STUDENTNo ratings yet

- Case Study Mis and Implementation - Rustan's - ShopwiseDocument3 pagesCase Study Mis and Implementation - Rustan's - ShopwiseMaikeru SanNo ratings yet

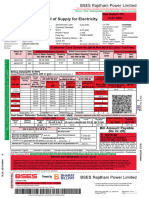

- Bill of Supply For Electricity: BSES Rajdhani Power LimitedDocument3 pagesBill of Supply For Electricity: BSES Rajdhani Power LimitedKishan GuptaNo ratings yet

- Impacts of The Islamic Financial Services Act 2013 On Investment Account Products Offered by Islamic Banks in MalaysiaDocument11 pagesImpacts of The Islamic Financial Services Act 2013 On Investment Account Products Offered by Islamic Banks in MalaysiaMuhammad SyamailNo ratings yet

- Katarmal Divyaben BlackbookDocument77 pagesKatarmal Divyaben Blackbookritzzzz1309No ratings yet

- SP0837-M008.00-3W11-001 - Tower Crane - CA Rev00 SignedDocument3 pagesSP0837-M008.00-3W11-001 - Tower Crane - CA Rev00 SignedBUDI HARIANTONo ratings yet

- A.1. Financial Statements Part 2Document53 pagesA.1. Financial Statements Part 2Kondreddi SakuNo ratings yet

- Invoice 7477Document1 pageInvoice 7477Biswajit PatraNo ratings yet

- U8 The First Silk Roads 16pages 2012Document8 pagesU8 The First Silk Roads 16pages 2012Jakob RodrichsonNo ratings yet

- The Poor Demand Conditions Due To Low Per Capita Income, High Unemployment RateDocument3 pagesThe Poor Demand Conditions Due To Low Per Capita Income, High Unemployment RateGakiya SultanaNo ratings yet