Download as docx, pdf, or txt

You might also like

- A Study On Customer Satisfaction Towards Online ShoppingDocument71 pagesA Study On Customer Satisfaction Towards Online ShoppingSumit Gupta75% (64)

- Accounting For PpeDocument37 pagesAccounting For PpeJohn Francis Idanan50% (6)

- Investment in Debt SecuritiesDocument31 pagesInvestment in Debt SecuritiesJohn Francis Idanan100% (1)

- Chapter 1 - Introduction To Marketing ResearchDocument11 pagesChapter 1 - Introduction To Marketing Researchdredoogie200167% (3)

- Depreciated Separately.: Property, Plant and EquipmentDocument5 pagesDepreciated Separately.: Property, Plant and EquipmentEmma Mariz GarciaNo ratings yet

- Chapter 10 (Class 2)Document9 pagesChapter 10 (Class 2)Daniela SawaNo ratings yet

- CHAPTER 16 PPE (PART 2) - For Distribution PDFDocument21 pagesCHAPTER 16 PPE (PART 2) - For Distribution PDFemman neriNo ratings yet

- Note Buổi 6Document5 pagesNote Buổi 6Long Chế Vũ BảoNo ratings yet

- DEPRECIATIONDocument4 pagesDEPRECIATIONAlexander DimaliposNo ratings yet

- AE 121 - C28 To C30 - Depreciation and DepletionDocument66 pagesAE 121 - C28 To C30 - Depreciation and DepletionKendall JennerNo ratings yet

- Depreciation: AR1 SY 2016-17 Pol D. MedinaDocument52 pagesDepreciation: AR1 SY 2016-17 Pol D. MedinaShieldon Vic PinoonNo ratings yet

- ACC 1100 Days 14&15 Long-Lived Assets PDFDocument25 pagesACC 1100 Days 14&15 Long-Lived Assets PDFYevhenii VdovenkoNo ratings yet

- E - Learning Content DepreciationDocument14 pagesE - Learning Content DepreciationNikhil JadhavNo ratings yet

- Depreciation and AmortisationDocument25 pagesDepreciation and AmortisationNikhil RamalingamNo ratings yet

- Student Notes Chap 11Document6 pagesStudent Notes Chap 11TINAIDANo ratings yet

- Depreciation, DepletionDocument2 pagesDepreciation, DepletionHassan AdamNo ratings yet

- Financial Accounting CIA - IIIDocument26 pagesFinancial Accounting CIA - IIIMEHAK L BAGRECHA 2010330No ratings yet

- Depreciation and DepletionDocument5 pagesDepreciation and DepletionMohammad Salim HossainNo ratings yet

- Module 7.3Document10 pagesModule 7.3Althea mary kate MorenoNo ratings yet

- Depreciation in AccountingDocument13 pagesDepreciation in AccountingNirmal PrasadNo ratings yet

- Subsequent Measurement of PropertyDocument28 pagesSubsequent Measurement of PropertyMa. Izabelle Andre LasquiteNo ratings yet

- Briefly Explain Different Method of Providing Depreciation?Document6 pagesBriefly Explain Different Method of Providing Depreciation?ajayghangareNo ratings yet

- Depreciation. PART 1 (Straight Line Variable Method) - 021728Document60 pagesDepreciation. PART 1 (Straight Line Variable Method) - 021728UnoNo ratings yet

- Depreciation PresentationDocument34 pagesDepreciation PresentationMahalakshmi Arumugam0% (1)

- Chapter 11Document24 pagesChapter 11eilsel_ljNo ratings yet

- Chapter 30Document2 pagesChapter 30Ney GascNo ratings yet

- DepreciationDocument6 pagesDepreciationSYOUSUF45No ratings yet

- CFAS Reviewer (Not Yet Done)Document34 pagesCFAS Reviewer (Not Yet Done)Kassandra AlbertoNo ratings yet

- Concept and Accounting of DepreciationDocument14 pagesConcept and Accounting of DepreciationSanzida Rahman AshaNo ratings yet

- Depreciation: Part - A: Theory SectionDocument19 pagesDepreciation: Part - A: Theory SectionDivya Punjabi0% (1)

- PPE Part 2 ModuleDocument13 pagesPPE Part 2 ModuleNatalie SerranoNo ratings yet

- Module 4 (Topic 5) - Depreciation (Straight Line and Variable Method)Document9 pagesModule 4 (Topic 5) - Depreciation (Straight Line and Variable Method)Ann BergonioNo ratings yet

- Reviewer Depreciation and Depletion Expires PDFDocument64 pagesReviewer Depreciation and Depletion Expires PDFGab Ignacio0% (1)

- Depreciation Methods and Accounting For Changes in Useful Life and MethodsDocument17 pagesDepreciation Methods and Accounting For Changes in Useful Life and MethodskyramaeNo ratings yet

- Far Rev FinalsDocument90 pagesFar Rev FinalsmickaNo ratings yet

- Depreciation of Non Current AssetsDocument27 pagesDepreciation of Non Current Assetskimuli FreddieNo ratings yet

- Subsequent Measurement Accounting Property Plant and EquipmentDocument60 pagesSubsequent Measurement Accounting Property Plant and EquipmentNatalie SerranoNo ratings yet

- Intacc ReportDocument4 pagesIntacc ReportChristen HerceNo ratings yet

- Chapter 7 DepreciationDocument50 pagesChapter 7 Depreciationpriyam.200409No ratings yet

- EEC Unit5-DepreciationDocument4 pagesEEC Unit5-DepreciationSankara nathNo ratings yet

- A7 Accounting For Depreciation and Disposal of Fixed Assets 2Document17 pagesA7 Accounting For Depreciation and Disposal of Fixed Assets 2diggywilldoitNo ratings yet

- Accounting For Non-Current AssetsDocument8 pagesAccounting For Non-Current AssetsvladsteinarminNo ratings yet

- DepreciationDocument19 pagesDepreciationamit palNo ratings yet

- CH 09 In-Class Problems - Fall 2013Document4 pagesCH 09 In-Class Problems - Fall 2013StephNo ratings yet

- Fixed Assests As-10Document25 pagesFixed Assests As-10meghaNo ratings yet

- Depreciation: Aromal S A Roll No. 5 Govt. College NedumangadDocument24 pagesDepreciation: Aromal S A Roll No. 5 Govt. College NedumangadAromalNo ratings yet

- Week 10 - 03 - Module 24 - Property, Plant & Equipment (Part 3)Document8 pagesWeek 10 - 03 - Module 24 - Property, Plant & Equipment (Part 3)지마리No ratings yet

- DepreciationDocument16 pagesDepreciationYashi GuptaNo ratings yet

- Property, Plant Equipment-IAS 16Document21 pagesProperty, Plant Equipment-IAS 16Shoaib SakhiNo ratings yet

- TOA 011 - Depreciation, Revaluation and Impairment With AnsDocument5 pagesTOA 011 - Depreciation, Revaluation and Impairment With AnsSyril SarientasNo ratings yet

- DepreciationDocument2 pagesDepreciationCharles Reginald K. HwangNo ratings yet

- TA07b - Current AssetsDocument11 pagesTA07b - Current AssetsMarsha Sabrina LillahNo ratings yet

- Methods of DepreciationDocument12 pagesMethods of Depreciationamun din100% (1)

- Property, Plant and Equipment - DepreciationDocument34 pagesProperty, Plant and Equipment - DepreciationSharmaineMiranda50% (2)

- Lesson 4Document23 pagesLesson 4shadowlord468No ratings yet

- ENG'G 151-Module-IIIDocument16 pagesENG'G 151-Module-IIISHERWIN MOSOMOSNo ratings yet

- DepreciationDocument7 pagesDepreciationSoumendra RoyNo ratings yet

- Fair Value Matching PrincipleDocument5 pagesFair Value Matching PrincipleGracie Kiarie100% (1)

- Property Plant and EquipmentDocument13 pagesProperty Plant and EquipmentWilsonNo ratings yet

- DEPRECIATION AND DEPLETION Supplementary Review MaterialDocument5 pagesDEPRECIATION AND DEPLETION Supplementary Review MaterialCaseylyn RonquilloNo ratings yet

- IAS 16 Property Plant and EquipmentDocument12 pagesIAS 16 Property Plant and Equipmentwaseefahmad89No ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- Accounting For Service BusinessDocument2 pagesAccounting For Service BusinessJohn Francis IdananNo ratings yet

- 8-Capital BudgetingDocument89 pages8-Capital BudgetingJohn Francis IdananNo ratings yet

- Time Value of MoneyDocument5 pagesTime Value of MoneyJohn Francis IdananNo ratings yet

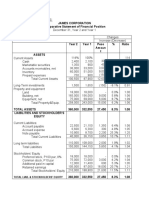

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionDocument7 pagesHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananNo ratings yet

- Substantive Test of LiabilitiesDocument4 pagesSubstantive Test of LiabilitiesJohn Francis IdananNo ratings yet

- Accounting For InvestmentsDocument42 pagesAccounting For InvestmentsJohn Francis Idanan100% (4)

- International Financial Reporting StandardsDocument3 pagesInternational Financial Reporting Standardsmarkobare2019No ratings yet

- Chapter 6 Practical Aspects of Investment Appraisal (Student)Document10 pagesChapter 6 Practical Aspects of Investment Appraisal (Student)Nguyễn Thái Minh ThưNo ratings yet

- Case Study - COSO Components PrinciplesDocument6 pagesCase Study - COSO Components PrinciplesGalinaNo ratings yet

- Accounting Fundamentals: The Accounting Equation and The Double-Entry SystemDocument70 pagesAccounting Fundamentals: The Accounting Equation and The Double-Entry SystemAllana Mier100% (1)

- 13 Dela Cruz - Chapters 5 and 6 Summaries PDFDocument12 pages13 Dela Cruz - Chapters 5 and 6 Summaries PDFMau Dela CruzNo ratings yet

- Case Study ZaraDocument6 pagesCase Study ZaraAizuddeen100% (5)

- 11.dealing With The CompetitionDocument48 pages11.dealing With The CompetitionAvinash SinghNo ratings yet

- Lonni Auditors Report 2020Document6 pagesLonni Auditors Report 2020Zenita CardinesNo ratings yet

- Marymount Academy of Paranaque Inc.: Abm 5 Fundamentals of Accounting andDocument9 pagesMarymount Academy of Paranaque Inc.: Abm 5 Fundamentals of Accounting andAlexidaniel LabasbasNo ratings yet

- Asyad Financial AnalysisDocument9 pagesAsyad Financial AnalysisshawktNo ratings yet

- Name: Milan Patel Roll No: 39 College: SEMCOM: Logistics ManagementDocument10 pagesName: Milan Patel Roll No: 39 College: SEMCOM: Logistics ManagementYogesh PatelNo ratings yet

- ACCA AA TuitionEx2021-22 CBE As JG21Jan crw1502 gf0203 crw0403 SPi12MarDocument22 pagesACCA AA TuitionEx2021-22 CBE As JG21Jan crw1502 gf0203 crw0403 SPi12MarAbid AliNo ratings yet

- Intermediate Accounting 1Document22 pagesIntermediate Accounting 1Nemalai VitalNo ratings yet

- PrevDocument68 pagesPrevSamuelNo ratings yet

- Chapter 1: Company Profile 1.1. Introduction CompanyDocument7 pagesChapter 1: Company Profile 1.1. Introduction Companypink pinkNo ratings yet

- TME 100 - Promotional ToolsDocument4 pagesTME 100 - Promotional ToolsDelmae ToledoNo ratings yet

- Inven Manajemen OperasionalDocument45 pagesInven Manajemen OperasionalCristopher ReynaldiNo ratings yet

- Auditor's Report Adverse EDocument3 pagesAuditor's Report Adverse EGerome Echano50% (2)

- CPA Exam Prep:Bus Envr & Cncpt-Q2Document7 pagesCPA Exam Prep:Bus Envr & Cncpt-Q2DominickdadNo ratings yet

- Allen and Hanbury LTDDocument19 pagesAllen and Hanbury LTDsharaf fahimNo ratings yet

- T 4Document3 pagesT 4Muntasir AhmmedNo ratings yet

- Ias 2 Test Bank PDFDocument11 pagesIas 2 Test Bank PDFAB Cloyd100% (1)

- Marketing CDocument20 pagesMarketing CReefat Arefin KhanNo ratings yet

- P and G Marketing Strategy-1Document19 pagesP and G Marketing Strategy-1Daniel CerneiNo ratings yet

- Budget ReportsDocument65 pagesBudget ReportsKrishnaNo ratings yet

- Kiran Pawar: Sales & Marketing / Business DevelopmentDocument3 pagesKiran Pawar: Sales & Marketing / Business DevelopmentAnonymous QRZK8VPRNo ratings yet

- Cornerstones of Cost Management 2nd Edition Hansen Test BankDocument26 pagesCornerstones of Cost Management 2nd Edition Hansen Test BankChristopherKnightagem100% (57)