Download as pdf or txt

You might also like

- WorldExplorationTrends2023 ReportDocument16 pagesWorldExplorationTrends2023 ReportKrash King100% (1)

- Spanning The GlobeDocument3 pagesSpanning The GlobeAli Fasl69% (13)

- EE On Ikea and Its Marketing StrategiesDocument16 pagesEE On Ikea and Its Marketing StrategiesWilmore JulioNo ratings yet

- 01 PDFDocument2 pages01 PDFsamirarabello0% (2)

- Nirmal Bang Berger Paints Q3FY22 Result Update 11 February 2022Document11 pagesNirmal Bang Berger Paints Q3FY22 Result Update 11 February 2022Shinde Chaitanya Sharad C-DOT 5688No ratings yet

- Pcomp Up On Gov't Stimulus Programs: Week in ReviewDocument2 pagesPcomp Up On Gov't Stimulus Programs: Week in ReviewJervie GacutanNo ratings yet

- Presales Recovery Expected in 2H, Earnings To Follow: Sector BriefDocument8 pagesPresales Recovery Expected in 2H, Earnings To Follow: Sector BrieftataxpNo ratings yet

- AbacusShortTakes 08312022Document7 pagesAbacusShortTakes 08312022ignaciomannyNo ratings yet

- Top Story:: WED 11 JAN 2023Document9 pagesTop Story:: WED 11 JAN 2023Elcano MirandaNo ratings yet

- AbacusShortTakes 08232022Document7 pagesAbacusShortTakes 08232022ignaciomannyNo ratings yet

- Half-Year Construction Market View - FinalDocument19 pagesHalf-Year Construction Market View - FinalAdam DawsonNo ratings yet

- India Strategy Report - 28th Feb 2024Document20 pagesIndia Strategy Report - 28th Feb 2024MalolanRNo ratings yet

- Ey Pe VC Trend BookDocument80 pagesEy Pe VC Trend BookRama KumarNo ratings yet

- EquityInvestmentStrategy May2022Document85 pagesEquityInvestmentStrategy May2022varanasidineshNo ratings yet

- Infosys 140422 MotiDocument10 pagesInfosys 140422 MotiGrace StylesNo ratings yet

- Axis Securities Equity Investment Strategy September 2022Document87 pagesAxis Securities Equity Investment Strategy September 2022Shriramkumar SinghNo ratings yet

- Colliers - Logistics - Report Q1 2023Document8 pagesColliers - Logistics - Report Q1 2023ANUSUA DASNo ratings yet

- Ciptadana Company Update MYOR 7 Mar 2024 Reiterate Buy Lower TPDocument7 pagesCiptadana Company Update MYOR 7 Mar 2024 Reiterate Buy Lower TPprima.brpNo ratings yet

- ORR BOSS Global Report WEBDocument2 pagesORR BOSS Global Report WEBasim.agueroNo ratings yet

- 2021 08 13 Dial - M - For - MarketDocument11 pages2021 08 13 Dial - M - For - MarketXavier StraussNo ratings yet

- AbacusShortTakes 09082022Document7 pagesAbacusShortTakes 09082022ignaciomannyNo ratings yet

- Consumer: Commodity Cost Inflation Inflicts Earnings CutsDocument6 pagesConsumer: Commodity Cost Inflation Inflicts Earnings CutsktyNo ratings yet

- Consumer Durables: B2C and Small Ticket Items Lead RecoveryDocument5 pagesConsumer Durables: B2C and Small Ticket Items Lead RecoveryAnupam JainNo ratings yet

- Canada Cap Rate Report Q2 2023Document20 pagesCanada Cap Rate Report Q2 2023abahomed12No ratings yet

- Ki Unvr 20240212Document9 pagesKi Unvr 20240212muh.asad.amNo ratings yet

- Housing & Construction Review 2021Document17 pagesHousing & Construction Review 2021gutosaabNo ratings yet

- ComoDocument12 pagesComoLEKH021No ratings yet

- 2024 Market Outlook Sam 14 Des 2023 240116 124609Document26 pages2024 Market Outlook Sam 14 Des 2023 240116 124609marcellusdarrenNo ratings yet

- 7204 - D&O - PUBLIC BANK - 2023-08-24 - BUY - 4.37 - DOGreenTechnologiesExpectingaVShapeRecovery - 1840691060Document5 pages7204 - D&O - PUBLIC BANK - 2023-08-24 - BUY - 4.37 - DOGreenTechnologiesExpectingaVShapeRecovery - 1840691060Nicholas ChehNo ratings yet

- Through The Looking Glass Chinas 2023 GDP and The Year AheadDocument11 pagesThrough The Looking Glass Chinas 2023 GDP and The Year Aheadt8enedNo ratings yet

- Ey Ivca Monthly Pe VC Roundup December 2022Document77 pagesEy Ivca Monthly Pe VC Roundup December 2022Mehul GargNo ratings yet

- Flash - HM. Sampoerna: 2Q20 Volume and Key Forward-Looking StatementDocument3 pagesFlash - HM. Sampoerna: 2Q20 Volume and Key Forward-Looking Statementjnn sNo ratings yet

- 2QFY24 Results Recap - Good, Bad, Ugly - 231117Document58 pages2QFY24 Results Recap - Good, Bad, Ugly - 231117krishna_buntyNo ratings yet

- Asian Paints 18012024 MotiDocument12 pagesAsian Paints 18012024 Motigaurav24021990No ratings yet

- 2hcy22 Outlook Midf 010722Document56 pages2hcy22 Outlook Midf 010722jcw288No ratings yet

- FINAL - Capstone Headwaters Capital Markets Update Q2 2020Document30 pagesFINAL - Capstone Headwaters Capital Markets Update Q2 2020Ray CarpenterNo ratings yet

- Colliers Manila Q3 2022 Residential v2Document4 pagesColliers Manila Q3 2022 Residential v2bhandari_raviNo ratings yet

- Colliers Manila Q2 2022 Residential JB 07282022 BO Edits 2Document5 pagesColliers Manila Q2 2022 Residential JB 07282022 BO Edits 2Geodel CuarteroNo ratings yet

- 4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedDocument5 pages4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedbradburywillsNo ratings yet

- Still Challenging, Yet Promising Outlook: Quarterly - Office - Jakarta - 6 October 2021Document37 pagesStill Challenging, Yet Promising Outlook: Quarterly - Office - Jakarta - 6 October 2021Arko A.100% (1)

- Asian-Paints Broker ReportDocument7 pagesAsian-Paints Broker Reportsj singhNo ratings yet

- Kuwait Quarterly Brief 20230228 EDocument6 pagesKuwait Quarterly Brief 20230228 ERaven BlingNo ratings yet

- GroupM-DEC 2022Document34 pagesGroupM-DEC 2022nicholas.tan2810No ratings yet

- Pakistan Strategy 2020.Document60 pagesPakistan Strategy 2020.muddasir1980No ratings yet

- Morning Market Report 06-APR-2023Document2 pagesMorning Market Report 06-APR-2023Amit MittalNo ratings yet

- Can Fin Homes Ltd-4QFY23 Result UpdateDocument5 pagesCan Fin Homes Ltd-4QFY23 Result UpdateUjwal KumarNo ratings yet

- Nio - JesseDocument9 pagesNio - JessejayRNo ratings yet

- Insights Dim Light at The End of TunnelDocument37 pagesInsights Dim Light at The End of TunnelKelvin Narada GunawanNo ratings yet

- O/W: "You Only Sell The Dresses You Have ": City Chic Collective (CCX)Document5 pagesO/W: "You Only Sell The Dresses You Have ": City Chic Collective (CCX)Muhammad ImranNo ratings yet

- Nirmal Bang Voltas Management Meet Update 13 June 2022Document6 pagesNirmal Bang Voltas Management Meet Update 13 June 2022Anku YadavNo ratings yet

- GS Sales Trading - Good Morning Mail 27.03.2024Document6 pagesGS Sales Trading - Good Morning Mail 27.03.2024Franco CaraballoNo ratings yet

- Real Estate Outlook Global Edition March 2023Document6 pagesReal Estate Outlook Global Edition March 2023Saif MonajedNo ratings yet

- JLL - Singapore Property Market Monitor 1Q 2022Document2 pagesJLL - Singapore Property Market Monitor 1Q 2022WNo ratings yet

- Ashok Leyland Q3FY19 Result UpdateDocument4 pagesAshok Leyland Q3FY19 Result Updatekapil bahetiNo ratings yet

- JLL Global Real Estate Perspective November 2020Document7 pagesJLL Global Real Estate Perspective November 2020Trần Não EmailNo ratings yet

- CIMB Strategy Note 2 Aug 2023 2Q23, Mixed Results, Large Banks AheadDocument10 pagesCIMB Strategy Note 2 Aug 2023 2Q23, Mixed Results, Large Banks Aheadbotoy26No ratings yet

- Horizons Q3 Issue v4Document68 pagesHorizons Q3 Issue v4wyowhokojzsvvyrbvaNo ratings yet

- 15134-The Nigerian Financial Market 2021 Review and 2022 Outlook - A Mix of Boom and Gloom-ProshareDocument29 pages15134-The Nigerian Financial Market 2021 Review and 2022 Outlook - A Mix of Boom and Gloom-ProshareOladipo OlanyiNo ratings yet

- Pidilite Industries Limited: Eyeing Strong Post-Pandemic RecoveryDocument7 pagesPidilite Industries Limited: Eyeing Strong Post-Pandemic RecoveryIS group 7No ratings yet

- WilliamBlair - PCA 2024 Secondary Market Survey Report Mar 2024Document9 pagesWilliamBlair - PCA 2024 Secondary Market Survey Report Mar 2024Alexandre Da costaNo ratings yet

- Indian Mortgage Finance Market PDFDocument61 pagesIndian Mortgage Finance Market PDFmikecoreleonNo ratings yet

- Id 23062020 PDFDocument11 pagesId 23062020 PDFbala gamerNo ratings yet

- Annual Report of The Keepers Holdings. Inc. For Cy 2021Document201 pagesAnnual Report of The Keepers Holdings. Inc. For Cy 2021ignaciomannyNo ratings yet

- LRWC-SEC 17C - Financial Highlights of Q1 2022Document4 pagesLRWC-SEC 17C - Financial Highlights of Q1 2022ignaciomannyNo ratings yet

- First Quarterly Report of The Keepers Holdings, Inc. Cy 2022Document73 pagesFirst Quarterly Report of The Keepers Holdings, Inc. Cy 2022ignaciomannyNo ratings yet

- Response To PSE Query 07 September 2022Document1 pageResponse To PSE Query 07 September 2022ignaciomannyNo ratings yet

- AbacusShortTakes 09092022Document6 pagesAbacusShortTakes 09092022ignaciomannyNo ratings yet

- AbacusShortTakes 08232022Document7 pagesAbacusShortTakes 08232022ignaciomannyNo ratings yet

- Disclosure 2022-09-09 PSE Approval of AREIT Shares Lodgement (SEC-PSE)Document3 pagesDisclosure 2022-09-09 PSE Approval of AREIT Shares Lodgement (SEC-PSE)ignaciomannyNo ratings yet

- AbacusShortTakes 08312022Document7 pagesAbacusShortTakes 08312022ignaciomannyNo ratings yet

- AbacusShortTakes 09212022Document5 pagesAbacusShortTakes 09212022ignaciomannyNo ratings yet

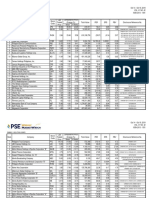

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Document3 pagesWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)ignaciomannyNo ratings yet

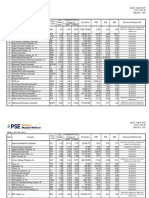

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- AbacusShortTakes 09082022Document7 pagesAbacusShortTakes 09082022ignaciomannyNo ratings yet

- AbacusShortTakes 10252022Document6 pagesAbacusShortTakes 10252022ignaciomannyNo ratings yet

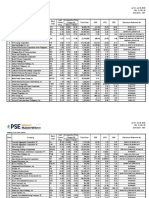

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

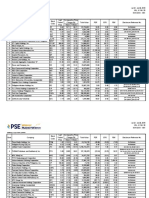

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument5 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument4 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Document3 pagesWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)ignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Document3 pagesWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)ignaciomannyNo ratings yet

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Document3 pagesWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)ignaciomannyNo ratings yet

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocument3 pagesWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVignaciomannyNo ratings yet

- 22 Dec 16 GNLMDocument16 pages22 Dec 16 GNLMmoe aungNo ratings yet

- Kevin Werbach - Chinas Social Credit SystemDocument57 pagesKevin Werbach - Chinas Social Credit SystemHellenNo ratings yet

- Strategic Management Case Study Group ReportDocument21 pagesStrategic Management Case Study Group ReportDevi Savira AlyshiaNo ratings yet

- 2012 International Arbitration Report Issue 1Document36 pages2012 International Arbitration Report Issue 1Khaled ChilwanNo ratings yet

- China's Ghost CitiesDocument46 pagesChina's Ghost CitiesasiafinancenewsNo ratings yet

- The Analects of ConfuciusDocument7 pagesThe Analects of ConfuciusAnonymous w5cOOIHNo ratings yet

- Drama 1105Document17 pagesDrama 1105EmpressMay ThetNo ratings yet

- On His Innovative Thought From The Book of Sangetsuki by Nakajima AtsushiDocument4 pagesOn His Innovative Thought From The Book of Sangetsuki by Nakajima AtsushiPseudo FiintaNo ratings yet

- China On Plastic WastesDocument3 pagesChina On Plastic WastesNica TemajoNo ratings yet

- XuetongDocument6 pagesXuetongVasil V. HristovNo ratings yet

- Boxer ProtocolDocument7 pagesBoxer ProtocolKeon Woo OhNo ratings yet

- China Facts For Kids China For Kids Cool Kid FactsDocument10 pagesChina Facts For Kids China For Kids Cool Kid Factsexfireex1No ratings yet

- Pak and Its Ties With CARsDocument12 pagesPak and Its Ties With CARsSaffiNo ratings yet

- Letter of Complaint (English)Document5 pagesLetter of Complaint (English)anyseeNo ratings yet

- RS Global Hotel Investment OutlookDocument17 pagesRS Global Hotel Investment OutlookGanesh LadNo ratings yet

- Tangram InstructionsDocument2 pagesTangram InstructionsJune SabatinNo ratings yet

- Dimensions of Cyber-Attacks: Cultural, Social, Economic, and PoliticalDocument11 pagesDimensions of Cyber-Attacks: Cultural, Social, Economic, and Politicalndaru_No ratings yet

- Unit 4 Writing AssignmentDocument6 pagesUnit 4 Writing AssignmentDan100% (2)

- Chapter 5 Global Customers: Global Marketing Management, 8e (Keegan)Document11 pagesChapter 5 Global Customers: Global Marketing Management, 8e (Keegan)prateek707199No ratings yet

- Feng Shui m2Document6 pagesFeng Shui m2Unicornio Azul0% (3)

- National Transport & Logistics Public Information Platform (MOT CHINA)Document36 pagesNational Transport & Logistics Public Information Platform (MOT CHINA)Lau MungNo ratings yet

- China Going Global: Between Ambition and CapacityDocument12 pagesChina Going Global: Between Ambition and CapacityOmar David Ramos VásquezNo ratings yet

- Zhang - Wang and Wang China 2012Document36 pagesZhang - Wang and Wang China 2012Karla VenegasNo ratings yet

- Jay Abraham The CEO Who Sees Around CornersDocument304 pagesJay Abraham The CEO Who Sees Around Cornersmichael3laterzaNo ratings yet

- Primary Source and Reading Guide - Rapid Development in China and IndiaDocument2 pagesPrimary Source and Reading Guide - Rapid Development in China and Indiajahran9194No ratings yet

- China Water Purifier Production: 4.2.2 by SegmentDocument3 pagesChina Water Purifier Production: 4.2.2 by SegmentWendell MerrillNo ratings yet

- China-Kyrgyzstan-Uzbekistan Railway - Opportunities and Challenges For ChinaDocument3 pagesChina-Kyrgyzstan-Uzbekistan Railway - Opportunities and Challenges For ChinaYunis ŞerifliNo ratings yet