Download as pdf or txt

You might also like

- Request For Reconsideration and ReinvestigationDocument2 pagesRequest For Reconsideration and Reinvestigationalmira halasanNo ratings yet

- BIR Releases Rules On Appealing Disputed Tax AssessmentsDocument13 pagesBIR Releases Rules On Appealing Disputed Tax AssessmentsDana100% (1)

- TaxationBarQ26A TaxRemediesDocument32 pagesTaxationBarQ26A TaxRemediesCire Gee100% (2)

- Chavez v. CA Case DigestDocument3 pagesChavez v. CA Case DigestElaine BercenioNo ratings yet

- Family Law Moot MemorialDocument22 pagesFamily Law Moot MemorialAakanksha KochharNo ratings yet

- Appealing BIR Assessment at The CTADocument1 pageAppealing BIR Assessment at The CTAhenzencameroNo ratings yet

- Taxation Law CasesDocument28 pagesTaxation Law CasesLou Corina LacambraNo ratings yet

- Taxpayers Remedies For FDDADocument2 pagesTaxpayers Remedies For FDDAalmira halasanNo ratings yet

- Tax Refunds Setting Matters StraightDocument3 pagesTax Refunds Setting Matters StraightSiobhan RobinNo ratings yet

- Tax Remedies Digest 62 70Document12 pagesTax Remedies Digest 62 70Christine Angelus MosquedaNo ratings yet

- Supreme Court: Factual AntecedentsDocument33 pagesSupreme Court: Factual AntecedentsCarmelie CumigadNo ratings yet

- CIR Vs PAL - ConstructionDocument8 pagesCIR Vs PAL - ConstructionEvan NervezaNo ratings yet

- Protesting A Tax AssessmentDocument3 pagesProtesting A Tax AssessmenterinemilyNo ratings yet

- Taxpayer's RemediesDocument5 pagesTaxpayer's RemediesCel TanNo ratings yet

- Supreme Court: Factual AntecedentsDocument9 pagesSupreme Court: Factual Antecedentspoloy6200No ratings yet

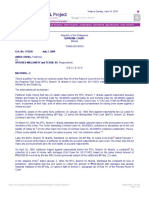

- G.R. No. 175097 Allied Banking Corporation, Petitioner, vs. Commissioner of Internal Revenue, Respondent. Del Castillo, J.Document2 pagesG.R. No. 175097 Allied Banking Corporation, Petitioner, vs. Commissioner of Internal Revenue, Respondent. Del Castillo, J.thelionleo1No ratings yet

- Allied Banking Corp Vs CIRDocument15 pagesAllied Banking Corp Vs CIRLeslie LernerNo ratings yet

- Republic of The Philippines: Supreme CourtDocument12 pagesRepublic of The Philippines: Supreme Courtlen_dy010487No ratings yet

- BIR AssessmentDocument2 pagesBIR AssessmentambonulanNo ratings yet

- Commissioner of Internal Revenue Vs First Express PawnshopDocument3 pagesCommissioner of Internal Revenue Vs First Express PawnshopJennilyn Gulfan Yase100% (1)

- Remedies of The TaxpayerDocument4 pagesRemedies of The TaxpayerAngelyn Sanjorjo50% (2)

- Allied Bank v. CIR Case DigestDocument4 pagesAllied Bank v. CIR Case DigestCareenNo ratings yet

- Due Process in The Issuance of Internal Revenue Tax AssessmentsDocument11 pagesDue Process in The Issuance of Internal Revenue Tax AssessmentsKing AlduezaNo ratings yet

- AJJJJJJJJJJJJJJJDocument2 pagesAJJJJJJJJJJJJJJJanthony paduaNo ratings yet

- Allied Banking Corporation v. CIR, G.R. No. 175097, 2010Document3 pagesAllied Banking Corporation v. CIR, G.R. No. 175097, 2010Michael TampengcoNo ratings yet

- Tax RemediesDocument8 pagesTax RemediesJade BelenNo ratings yet

- Required Before The BIR May Audit The Records of The Taxpayer? Letter of Authority (LOA)Document6 pagesRequired Before The BIR May Audit The Records of The Taxpayer? Letter of Authority (LOA)Jade CoritanaNo ratings yet

- Lascona Land Co. Inc. v. Commissioner of Internal Revenue, G.R. No. 171251, 05 March 2012Document10 pagesLascona Land Co. Inc. v. Commissioner of Internal Revenue, G.R. No. 171251, 05 March 2012Bernadette Luces BeldadNo ratings yet

- Bir Process On Tax AssessmentDocument8 pagesBir Process On Tax AssessmentAnonymous qjsSkwF50% (2)

- TaxationBarQ26A TaxRemediesDocument32 pagesTaxationBarQ26A TaxRemediesjuneson agustinNo ratings yet

- PDR Tax Forum 2016 Recent Court Decisions On Tax - FinalDocument144 pagesPDR Tax Forum 2016 Recent Court Decisions On Tax - FinalFender Boyang100% (1)

- REmedies Procedure Lecture 1Document5 pagesREmedies Procedure Lecture 1Susannie AcainNo ratings yet

- Tax AssignmentDocument6 pagesTax AssignmentShubh DixitNo ratings yet

- Howey Test) : (1) A Contract, Transaction, or Scheme (2) An Investment ofDocument3 pagesHowey Test) : (1) A Contract, Transaction, or Scheme (2) An Investment ofJeffrey A PobladorNo ratings yet

- Facts:: G.R. No. 175723, February 4, 2014 The City of Manila vs. Hon. Caridad H. Grecia-CuerdoDocument5 pagesFacts:: G.R. No. 175723, February 4, 2014 The City of Manila vs. Hon. Caridad H. Grecia-CuerdoShielden B. MoradaNo ratings yet

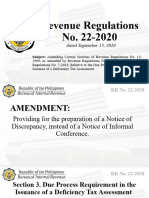

- RR No. 18-2013 (Digest)Document3 pagesRR No. 18-2013 (Digest)Alisa FitzpatrickNo ratings yet

- TAXREVDocument3 pagesTAXREVasdfghjkatt0% (1)

- Harte-Hanks Phils vs. CIRDocument2 pagesHarte-Hanks Phils vs. CIRCaroline A. Legaspino50% (2)

- Notes in Taxation Law (2014) : Jason R. BarlisDocument12 pagesNotes in Taxation Law (2014) : Jason R. BarlismarkbulloNo ratings yet

- Tax Remedies of The Taxpayer PDFDocument4 pagesTax Remedies of The Taxpayer PDFJester LimNo ratings yet

- Doctrines in Tax Remedies CasesDocument7 pagesDoctrines in Tax Remedies CasesMa Gabriellen Quijada-TabuñagNo ratings yet

- Week 10Document8 pagesWeek 10Victor LimNo ratings yet

- 8 - Global Fresh Products, Inc. v. CIRDocument13 pages8 - Global Fresh Products, Inc. v. CIRCarlota VillaromanNo ratings yet

- Examination Proper:: Tax Law Review Mid-Term ExaminationDocument9 pagesExamination Proper:: Tax Law Review Mid-Term ExaminationGRACENo ratings yet

- TopicsDocument40 pagesTopicsDa Yani ChristeeneNo ratings yet

- Case DigestsDocument21 pagesCase DigestsRose Ann VeloriaNo ratings yet

- Pbcom V CirDocument9 pagesPbcom V CirAbby ParwaniNo ratings yet

- Bureau of Internal Revenue: Deficiency Tax AssessmentDocument9 pagesBureau of Internal Revenue: Deficiency Tax AssessmentXavier Cajimat UrbanNo ratings yet

- Protesting The Deficiency Tax AssessmentDocument2 pagesProtesting The Deficiency Tax AssessmentbutowskiNo ratings yet

- CasesDocument79 pagesCasesJoel MendozaNo ratings yet

- Tax AssessmentsDocument3 pagesTax AssessmentsKing AlduezaNo ratings yet

- Procedures On Issuance of Deficiency Tax AssessmentDocument15 pagesProcedures On Issuance of Deficiency Tax AssessmentmirabelvidalNo ratings yet

- PBCOM Vs CommissionerDocument2 pagesPBCOM Vs Commissioner上原クリスNo ratings yet

- Dispute of Assessment - WongDocument5 pagesDispute of Assessment - WongAnne Fatima PilayreNo ratings yet

- Tax DiscussionDocument4 pagesTax DiscussionRawr rawrNo ratings yet

- COMMISSIONER OF INTERNAL REVENUE. vs. TRANSITIONS PHILIPPINES, OPTICAL INC. & Samar-I Electric Cooperative (SIEC) vs. CIRDocument4 pagesCOMMISSIONER OF INTERNAL REVENUE. vs. TRANSITIONS PHILIPPINES, OPTICAL INC. & Samar-I Electric Cooperative (SIEC) vs. CIRRica CorderoNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Facts and AssumptionsDocument4 pagesFacts and AssumptionsJbNo ratings yet

- GRABICATION FS 10mosDocument37 pagesGRABICATION FS 10mosJbNo ratings yet

- Grab Bication Final PaperDocument61 pagesGrab Bication Final PaperJbNo ratings yet

- H&H Reimbursement FormDocument3 pagesH&H Reimbursement FormJbNo ratings yet

- Release NotesDocument13 pagesRelease NotesJbNo ratings yet

- Anticipatory Bail: Submitted To Dr. Asad MalikDocument37 pagesAnticipatory Bail: Submitted To Dr. Asad Malikmohit kumarNo ratings yet

- Carolino V SengaDocument7 pagesCarolino V Sengacertiorari19No ratings yet

- American President Lines V ClaveDocument1 pageAmerican President Lines V ClaveZoe VelascoNo ratings yet

- Gulf County Sheriff's Office Law Enforcement Summary May 18, 2020 - May 24, 2020Document3 pagesGulf County Sheriff's Office Law Enforcement Summary May 18, 2020 - May 24, 2020Michael AllenNo ratings yet

- Revised Content Family Law July 2017Document7 pagesRevised Content Family Law July 2017Dhevasenaa RajendhirakumaarNo ratings yet

- 7E Kruysel V AbionDocument3 pages7E Kruysel V AbionGerald DacilloNo ratings yet

- Chan - v. - Carrera PDFDocument6 pagesChan - v. - Carrera PDFJulius ReyesNo ratings yet

- Board of Medicine vs. OtaDocument2 pagesBoard of Medicine vs. OtaKel Magtira0% (1)

- Canons 14 - 22Document71 pagesCanons 14 - 22Louem GarceniegoNo ratings yet

- Governance and Fiscal Management: The Philippine ContextDocument20 pagesGovernance and Fiscal Management: The Philippine ContextConnie LopicoNo ratings yet

- Lito Corpuz Vs People of The Philippines CASE DIGESTDocument4 pagesLito Corpuz Vs People of The Philippines CASE DIGESTCJ PonceNo ratings yet

- Supreme Court of Pakistan Judgment About Coruption in Pakistan Steel Mills CorpDocument57 pagesSupreme Court of Pakistan Judgment About Coruption in Pakistan Steel Mills CorpMYOB420No ratings yet

- Annexure Whistle Blower Policy / Vigil Mechanism of Telecommunications Consultants India Limited 1. PrefaceDocument12 pagesAnnexure Whistle Blower Policy / Vigil Mechanism of Telecommunications Consultants India Limited 1. PrefaceDrishti TiwariNo ratings yet

- Noel M. Manrique v. Delta Earthmoving, Inc., Ed Anyayahan and Ian HansenDocument1 pageNoel M. Manrique v. Delta Earthmoving, Inc., Ed Anyayahan and Ian HansenMark Anthony ReyesNo ratings yet

- Sarguja Rail Corridor Private Limited: Earnings Amount Deductions Amount Perks/Other income/Exempton/RebatesDocument1 pageSarguja Rail Corridor Private Limited: Earnings Amount Deductions Amount Perks/Other income/Exempton/RebatesDeeptimayee SahooNo ratings yet

- Kilosbayan v. ErmitaDocument2 pagesKilosbayan v. ErmitaMarius SumiraNo ratings yet

- Tanner Advertising Group v. City of Brookhaven, GADocument16 pagesTanner Advertising Group v. City of Brookhaven, GABrookhaven Post100% (1)

- Azuhoto A0400042 PDFDocument11 pagesAzuhoto A0400042 PDFAbemo kikonNo ratings yet

- Humboldt County 2003-04 Grand Jury, Final Report, 2004.Document60 pagesHumboldt County 2003-04 Grand Jury, Final Report, 2004.Rick ThomaNo ratings yet

- Orientation On DTP ME With DMOs - November 4 2022Document28 pagesOrientation On DTP ME With DMOs - November 4 2022Arlo Winston De GuzmanNo ratings yet

- Whatis DemocracyWhy DemocracyDocument29 pagesWhatis DemocracyWhy DemocracyAsad IbrarNo ratings yet

- Criminal Justice & HR RUDocument55 pagesCriminal Justice & HR RUkunal mehtoNo ratings yet

- A.C. No. 6484Document3 pagesA.C. No. 6484Rose Ann VeloriaNo ratings yet

- Data Classification TemplateDocument4 pagesData Classification TemplateMansoor AhmedNo ratings yet

- SALE DEED - Plot No. 262-8 IMT MANESAR PRINTEDDocument8 pagesSALE DEED - Plot No. 262-8 IMT MANESAR PRINTEDGirish SharmaNo ratings yet

- Jaipur National University Seedling School of Law & GovernanceDocument15 pagesJaipur National University Seedling School of Law & GovernancePrashant MahawarNo ratings yet

- Del Rosario v. People, 3 SCRA 650Document2 pagesDel Rosario v. People, 3 SCRA 650PRINCESS MAGPATOCNo ratings yet

- Petitioner's Affidavit of Fact, Evidence, and Information: Exhibit ADocument8 pagesPetitioner's Affidavit of Fact, Evidence, and Information: Exhibit ABeyNo ratings yet