Download as docx, pdf, or txt

You might also like

- Porter's Diamond Analysis On Philippine Business IndustryDocument3 pagesPorter's Diamond Analysis On Philippine Business IndustryDaceler MaxionNo ratings yet

- Galaxy Chocolate - Final ReportDocument17 pagesGalaxy Chocolate - Final Reportasiregar_marzuqi0% (3)

- Rewe Group in Retailing (World) PDFDocument37 pagesRewe Group in Retailing (World) PDFYuriy Kot100% (1)

- Argumentative EssayDocument2 pagesArgumentative EssayMaria Angelica FontiverosNo ratings yet

- Rflib Chapter 4,5,6 - 1Document22 pagesRflib Chapter 4,5,6 - 1CJ Tin100% (1)

- Precision WorldwideDocument9 pagesPrecision WorldwidePedro José ZapataNo ratings yet

- 10 Facts About Emerging MarketsDocument4 pages10 Facts About Emerging MarketsBasavaraj MithareNo ratings yet

- Perez Socsci Research RevisedDocument17 pagesPerez Socsci Research RevisedJoan PerezNo ratings yet

- The Rise of BPO Industry and Its Effects To The 2021 Philippine EconomyDocument8 pagesThe Rise of BPO Industry and Its Effects To The 2021 Philippine EconomyLean Dale IgosNo ratings yet

- PLDT Company Portfolio AnalysisDocument13 pagesPLDT Company Portfolio AnalysisMary Bernadette VillaluzNo ratings yet

- GlobaleconomyDocument5 pagesGlobaleconomyCarmelo TarigaNo ratings yet

- How The Covid-19 Pandemic Has Affected The Philippine Digital Economy - Perez ResearchDocument13 pagesHow The Covid-19 Pandemic Has Affected The Philippine Digital Economy - Perez ResearchJoan PerezNo ratings yet

- Group 1 and 3Document4 pagesGroup 1 and 3Thricia Lou OpialaNo ratings yet

- Brosas, Cabug-Os & Cayaco - RRL (Final Draft)Document8 pagesBrosas, Cabug-Os & Cayaco - RRL (Final Draft)Adrheyni Kyle Cabug-osNo ratings yet

- 220 - PSU - Supporting MSMEs Digitalization Amid COVID-19Document9 pages220 - PSU - Supporting MSMEs Digitalization Amid COVID-19Francis Loie RepuelaNo ratings yet

- QUESTION 1: Read The Above Article and Explain What Are The Global Conflicting Trade Signals?Document7 pagesQUESTION 1: Read The Above Article and Explain What Are The Global Conflicting Trade Signals?mzhouryNo ratings yet

- EcoDev FinalsDocument4 pagesEcoDev FinalsChristian De GuzmanNo ratings yet

- GA.ibi Tham KhảoDocument13 pagesGA.ibi Tham KhảoHoàng TriềuNo ratings yet

- Marketing ResearchDocument33 pagesMarketing ResearchAuto TeaserNo ratings yet

- Covid 19 Effect On Energy CommoditiesDocument5 pagesCovid 19 Effect On Energy CommoditiesShazedul Haque RadhitNo ratings yet

- All PPT and QuizDocument29 pagesAll PPT and QuizKylie Luigi Leynes BagonNo ratings yet

- Systematic Country Diagnostic of The Philippines - Realizing The Filipino Dream For 2040Document8 pagesSystematic Country Diagnostic of The Philippines - Realizing The Filipino Dream For 2040Chelsea ArzadonNo ratings yet

- ITA Module 5Document63 pagesITA Module 5Dan DiNo ratings yet

- Viet Nam EconomyDocument8 pagesViet Nam Economynguyenthilena297No ratings yet

- 19bce0696 VL2021220701671 Ast04Document9 pages19bce0696 VL2021220701671 Ast04Parijat NiyogyNo ratings yet

- The Strategic Importance of The Philippine Manufacturing SectorDocument6 pagesThe Strategic Importance of The Philippine Manufacturing SectorchialunNo ratings yet

- SOC - PeTa 2Document18 pagesSOC - PeTa 2jeq9eNo ratings yet

- PWC Philippines M&A Challenge Preliminary Round: November 06, 2020Document22 pagesPWC Philippines M&A Challenge Preliminary Round: November 06, 2020Mary Anne JamisolaNo ratings yet

- Keynote Speech of Secretary Ramon M. Lopez, Security Bank's 2021 Economic ForumDocument10 pagesKeynote Speech of Secretary Ramon M. Lopez, Security Bank's 2021 Economic ForumJasmin MacabacyaoNo ratings yet

- Pest VietnamDocument4 pagesPest VietnamMelisa SureNo ratings yet

- The Philippine IT Plan: Prospects and Problems: Claro V. ParladeDocument10 pagesThe Philippine IT Plan: Prospects and Problems: Claro V. ParladeLGS A RO12-05No ratings yet

- Cruz, D Longexam Bsma2-1Document4 pagesCruz, D Longexam Bsma2-1Dianne Mae Saballa CruzNo ratings yet

- Philippines Economic Update October 2019Document8 pagesPhilippines Economic Update October 2019Shalin Srikant Ruadap PrabhakerNo ratings yet

- Impact Covid 19 To Malaysia EconomyDocument10 pagesImpact Covid 19 To Malaysia EconomyMasidayu MehatNo ratings yet

- Impact of Covid-19 On Firms' PerformanceDocument2 pagesImpact of Covid-19 On Firms' PerformanceNguyễn Thuỳ LinhNo ratings yet

- DocumentDocument1 pageDocumentCarmelo TarigaNo ratings yet

- Chapter 1 Draft-Brosas, Cabug-Os, CayacoDocument20 pagesChapter 1 Draft-Brosas, Cabug-Os, CayacoAdrheyni Kyle Cabug-osNo ratings yet

- Dela Cruz Pestel Cbet 25 102pDocument9 pagesDela Cruz Pestel Cbet 25 102pALTHEA MAE DELA CRUZNo ratings yet

- Presentation EcoDocument13 pagesPresentation EcoSumit KashyapNo ratings yet

- Impact of Pandemic On Job Creation in IndiaDocument9 pagesImpact of Pandemic On Job Creation in IndiaAnindita PrustyNo ratings yet

- IntroductionDocument6 pagesIntroductionArnab SenNo ratings yet

- Seminar Report: I: Subject: Business Environment Mba Sy Sem IiiDocument5 pagesSeminar Report: I: Subject: Business Environment Mba Sy Sem IiipankajkapseNo ratings yet

- BE SeminarDocument5 pagesBE SeminarpankajkapseNo ratings yet

- Describe An Industry That Is Active in Vietnam, Mentioning The Size, The Employees and Its Economic Impact On Vietnam.Document3 pagesDescribe An Industry That Is Active in Vietnam, Mentioning The Size, The Employees and Its Economic Impact On Vietnam.buihoahaiyena1.c3hn2020No ratings yet

- Eco205 Industry TienDocument7 pagesEco205 Industry TienLê Hoàn Minh ĐăngNo ratings yet

- Impact of COVID-19 On Indian EconomyDocument13 pagesImpact of COVID-19 On Indian EconomySumit KashyapNo ratings yet

- The Impact of The COVID-19 Pandemic On The Construc On Industry in The PhilippinesDocument44 pagesThe Impact of The COVID-19 Pandemic On The Construc On Industry in The PhilippinesPLM CETSC PRC 22-23No ratings yet

- ASEAN-Korea Digital Partnership in The Post-COVID-19 EraDocument7 pagesASEAN-Korea Digital Partnership in The Post-COVID-19 EraAngelNo ratings yet

- HR Mega Trends - Team 3Document14 pagesHR Mega Trends - Team 3Jakia KhanomNo ratings yet

- T2 - English For Business - Group11-TR. FINALDocument9 pagesT2 - English For Business - Group11-TR. FINALSantiago CalderonNo ratings yet

- The Impact of COVID-19 in The Philippines: An Economic StudyDocument8 pagesThe Impact of COVID-19 in The Philippines: An Economic StudyMary Grace CuevaNo ratings yet

- Aykac FurnitureDocument7 pagesAykac FurnitureIsmail ArshadNo ratings yet

- The Economic Impact of Covid-19 On Different Sectors in IndiaDocument7 pagesThe Economic Impact of Covid-19 On Different Sectors in IndiamanishNo ratings yet

- Christian Faith C. Zebua Mba MM - I PUP - ManilaDocument10 pagesChristian Faith C. Zebua Mba MM - I PUP - ManilaChristian ZebuaNo ratings yet

- IPP 2014 Appendix 1 Sectoral AnalysesDocument63 pagesIPP 2014 Appendix 1 Sectoral AnalysesRose Ann AguilarNo ratings yet

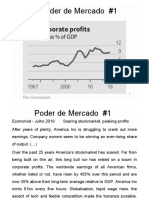

- O I Poder MercadoDocument12 pagesO I Poder MercadoLuisa LourençoNo ratings yet

- At The Beginning of The ReportDocument5 pagesAt The Beginning of The ReportPhan Tú AnhNo ratings yet

- Group 2 - ASIADocument54 pagesGroup 2 - ASIAMichael AquinoNo ratings yet

- Factors That Affect Advertising and MarketingDocument6 pagesFactors That Affect Advertising and MarketingmanishinsightNo ratings yet

- Macroeconomic Overview of The Philippines and The New Industrial PolicyDocument18 pagesMacroeconomic Overview of The Philippines and The New Industrial PolicyGwyneth ValdezNo ratings yet

- SWOT Analysis - Philippine MarketDocument5 pagesSWOT Analysis - Philippine MarketArmando SantosNo ratings yet

- EDIT PNF Sept 26 2014Document14 pagesEDIT PNF Sept 26 2014straywolf0No ratings yet

- Digitalisation in Europe 2021-2022: Evidence from the EIB Investment SurveyFrom EverandDigitalisation in Europe 2021-2022: Evidence from the EIB Investment SurveyNo ratings yet

- Digitalisation in Europe 2022-2023: Evidence from the EIB Investment SurveyFrom EverandDigitalisation in Europe 2022-2023: Evidence from the EIB Investment SurveyNo ratings yet

- Public AdDocument13 pagesPublic AdDONNAVEL ROSALESNo ratings yet

- Reflection Paper #2Document1 pageReflection Paper #2DONNAVEL ROSALESNo ratings yet

- Evolution of Public AdministrationDocument8 pagesEvolution of Public AdministrationDONNAVEL ROSALESNo ratings yet

- Reflection Paper - Infrastructure SectorDocument1 pageReflection Paper - Infrastructure SectorDONNAVEL ROSALESNo ratings yet

- PA 206 MidtermDocument4 pagesPA 206 MidtermDONNAVEL ROSALESNo ratings yet

- Reflection Paper-Development Administration GroupDocument1 pageReflection Paper-Development Administration GroupDONNAVEL ROSALESNo ratings yet

- Recruitment, Screening & SelectionDocument17 pagesRecruitment, Screening & SelectionDONNAVEL ROSALES100% (1)

- Reflection Paper - Social SectorDocument1 pageReflection Paper - Social SectorDONNAVEL ROSALESNo ratings yet

- PA 222 - Economic Development GroupDocument2 pagesPA 222 - Economic Development GroupDONNAVEL ROSALESNo ratings yet

- Internal & External RecruitmentDocument2 pagesInternal & External RecruitmentDONNAVEL ROSALESNo ratings yet

- Success Stories 2022Document1 pageSuccess Stories 2022DONNAVEL ROSALESNo ratings yet

- ZamPen Top 10 Priority PAPs FY 2023Document38 pagesZamPen Top 10 Priority PAPs FY 2023DONNAVEL ROSALESNo ratings yet

- Zamboanga Peninsula Regional Development Investment Program 2017-2022Document544 pagesZamboanga Peninsula Regional Development Investment Program 2017-2022DONNAVEL ROSALESNo ratings yet

- Conservation and Protection of Wildlife ResourcesDocument19 pagesConservation and Protection of Wildlife ResourcesDONNAVEL ROSALESNo ratings yet

- Weekly 3Document1 pageWeekly 3DONNAVEL ROSALESNo ratings yet

- Advantages, Disadvantages, Challenges & Trends in E-GovernanceDocument22 pagesAdvantages, Disadvantages, Challenges & Trends in E-GovernanceDONNAVEL ROSALESNo ratings yet

- 2022 - Philippine National Development Planning Cognate - Karyl Kristal VillejoDocument43 pages2022 - Philippine National Development Planning Cognate - Karyl Kristal VillejoDONNAVEL ROSALESNo ratings yet

- Lettr Req FunrunDocument1 pageLettr Req FunrunDONNAVEL ROSALESNo ratings yet

- Saint Columban College: Corner V. Cerilles Sagun Street, San Francisco District, Pagadian City Certificate of EnrollmentDocument1 pageSaint Columban College: Corner V. Cerilles Sagun Street, San Francisco District, Pagadian City Certificate of EnrollmentDONNAVEL ROSALESNo ratings yet

- Anti-Graft & Corrupt Practices Act R.A. 3019: Sections 8-16Document17 pagesAnti-Graft & Corrupt Practices Act R.A. 3019: Sections 8-16DONNAVEL ROSALESNo ratings yet

- MRK108 Week 1 - CH 1 - JTDocument38 pagesMRK108 Week 1 - CH 1 - JTranulNo ratings yet

- Statement of The ProblemDocument5 pagesStatement of The ProblemAireen Rose Rabino Manguiran0% (1)

- Case ValeoDocument10 pagesCase ValeoDarwicheNo ratings yet

- CC Unit 9, Application LetterDocument28 pagesCC Unit 9, Application Lettermirana261No ratings yet

- Market-To-Cash: Trade Promotion ManagementDocument43 pagesMarket-To-Cash: Trade Promotion ManagementSevNo ratings yet

- Important Tips On The Law On SalesDocument34 pagesImportant Tips On The Law On SalesJanetGraceDalisayFabreroNo ratings yet

- Research Report 2022Document48 pagesResearch Report 2022Jeremiah CharlesNo ratings yet

- Business Model - SoapDocument11 pagesBusiness Model - SoapRupam BiswasNo ratings yet

- Submitted To: MKT337, Section: 10 Summer 2019Document21 pagesSubmitted To: MKT337, Section: 10 Summer 2019Azmaine AdilNo ratings yet

- Customer CentricityDocument12 pagesCustomer CentricityShashank Kapur100% (2)

- The Hospitality Business Plan - FinalDocument144 pagesThe Hospitality Business Plan - Finalkdfohasfowdesh75% (4)

- 1B6 S4hana1909 BPD en UsDocument54 pages1B6 S4hana1909 BPD en UsBiji RoyNo ratings yet

- Chapter 13 Dimensions of Marketing Strategy: ObjectivesDocument23 pagesChapter 13 Dimensions of Marketing Strategy: ObjectivesAhmad ArdiansyahNo ratings yet

- Shopee - Fulfilled by Shopee Info Deck (External)Document33 pagesShopee - Fulfilled by Shopee Info Deck (External)Shaleeena AiharaNo ratings yet

- Communication Styles: A Key To Adaptive Selling Today: Quicktime™ and A Decompressor Are Needed To See This PictureDocument32 pagesCommunication Styles: A Key To Adaptive Selling Today: Quicktime™ and A Decompressor Are Needed To See This PictureVilky ApriliaNo ratings yet

- Abm2020 LeadershipbriefDocument2 pagesAbm2020 Leadershipbriefapi-699139188No ratings yet

- PRJ p856 PDFDocument5 pagesPRJ p856 PDF10 unknown facts priyanka suman KeshriNo ratings yet

- BL-ECON-6110-LEC-1923T INTRODUCTORY TO ECONOMICS Lesson 2 - The Law of Supply and DemandDocument13 pagesBL-ECON-6110-LEC-1923T INTRODUCTORY TO ECONOMICS Lesson 2 - The Law of Supply and DemandDougie ChanNo ratings yet

- Flipkart Labels 01 Dec 2023 12 09Document3 pagesFlipkart Labels 01 Dec 2023 12 09KalashNo ratings yet

- Introduction of Usha MartinDocument20 pagesIntroduction of Usha MartinVishal VermaNo ratings yet

- Kamias LollipopDocument115 pagesKamias LollipopEdselle Abinal AcupiadoNo ratings yet

- United Nations Convention On Contracts For The International Sale of Goods (1980) (Cisg)Document26 pagesUnited Nations Convention On Contracts For The International Sale of Goods (1980) (Cisg)Samira SbcNo ratings yet

- Traditional Approaches in MarketingDocument24 pagesTraditional Approaches in MarketingGina DiwagNo ratings yet

- Negotiation PWDocument13 pagesNegotiation PWbenNo ratings yet

- Freedom From Command and ControlDocument374 pagesFreedom From Command and ControlGargee100% (1)

- Excel Inventory Template 300 V1Document6,052 pagesExcel Inventory Template 300 V1sophia lorreine chattoNo ratings yet