Download as pdf or txt

You might also like

- Account Titles With DefinitionDocument5 pagesAccount Titles With DefinitionAngelo Miranda88% (8)

- Fin 550 Milestone 2Document6 pagesFin 550 Milestone 2writer topNo ratings yet

- Presentation On CRISILDocument14 pagesPresentation On CRISILChanchal Gulati80% (5)

- Users of Accounting InformationDocument4 pagesUsers of Accounting InformationWycliffe OgetiiNo ratings yet

- Unit IDocument8 pagesUnit InamianNo ratings yet

- TallyDocument15 pagesTallySujit PaulNo ratings yet

- Accounting ReviewerDocument6 pagesAccounting ReviewerFictional PlayerNo ratings yet

- Financial AccountingDocument16 pagesFinancial AccountingSNo ratings yet

- Assignment of Financial AccountingDocument9 pagesAssignment of Financial Accountingsavi vermaNo ratings yet

- Chapter 1 Introduction To Accounting - 1.5Document4 pagesChapter 1 Introduction To Accounting - 1.5BHAWNANo ratings yet

- Introduction To Accounting: Chapter - 1Document5 pagesIntroduction To Accounting: Chapter - 1Varshitha ReddyNo ratings yet

- Faa IDocument18 pagesFaa INishtha RathNo ratings yet

- CMBE 2 - Lesson 3 ModuleDocument12 pagesCMBE 2 - Lesson 3 ModuleEunice AmbrocioNo ratings yet

- EpfoDocument6 pagesEpfoSiddharth OjhaNo ratings yet

- Chapter 1 Introduction To Accounting - NotesDocument5 pagesChapter 1 Introduction To Accounting - NotesShaji RarothNo ratings yet

- Introduction To Accounting Introduction To Accounting Introduction To AccountingDocument23 pagesIntroduction To Accounting Introduction To Accounting Introduction To AccountingAsitha AjayanNo ratings yet

- 3.4 Business IbDocument11 pages3.4 Business IbsamaraarrobaNo ratings yet

- Financial ControlDocument9 pagesFinancial Controlima funtanaresNo ratings yet

- Acc PDFDocument61 pagesAcc PDFSmarika BistNo ratings yet

- FABM1-CHAP6-Types of Major AccountsDocument5 pagesFABM1-CHAP6-Types of Major AccountsKyla BallesterosNo ratings yet

- BACNTHIDocument3 pagesBACNTHIFaith CalingoNo ratings yet

- FABM 1 Major AccountsDocument31 pagesFABM 1 Major AccountscatajannicolinNo ratings yet

- Accounting - : Basic Terms in Accounting - 1. TransactionDocument14 pagesAccounting - : Basic Terms in Accounting - 1. TransactionKaran Singh RathoreNo ratings yet

- FinanceDocument48 pagesFinanceMimi Adriatico JaranillaNo ratings yet

- Study Material AccountingDocument62 pagesStudy Material Accountingsagar sheralNo ratings yet

- CBSE 11th Commerce Sample Accountancy IDocument18 pagesCBSE 11th Commerce Sample Accountancy ILakshmi PonduriNo ratings yet

- BOOKKEEPING Module (For Printing)Document73 pagesBOOKKEEPING Module (For Printing)Tesda TesdaNo ratings yet

- Accounting Module E BookDocument43 pagesAccounting Module E BookMahima SheromiNo ratings yet

- AccountingDocument4 pagesAccountingKristine Marie ParalNo ratings yet

- FAI - Introduction To AccountingDocument9 pagesFAI - Introduction To Accountingalanorules001No ratings yet

- Fundamentals OF Accounting 1: FOR Grade 11Document29 pagesFundamentals OF Accounting 1: FOR Grade 11Francois GonzalesNo ratings yet

- Fabm 1Document4 pagesFabm 1hanhermosilla0528No ratings yet

- ACCOUNTING NOTES BcomDocument13 pagesACCOUNTING NOTES Bcomjacksonkimani3617No ratings yet

- Account TitlesDocument9 pagesAccount TitlesFaelynnNo ratings yet

- Types of Major AccountsDocument4 pagesTypes of Major AccountsPortia AbestanoNo ratings yet

- Financial Accounting - 1Document42 pagesFinancial Accounting - 1MajdiNo ratings yet

- Unit-Iv Capital and Capital BudgetingDocument16 pagesUnit-Iv Capital and Capital BudgetingSubhas BeraNo ratings yet

- Text 47FF 9B41 4C 0Document4 pagesText 47FF 9B41 4C 0Toph BeifongNo ratings yet

- MEFA - IV and V UnitsDocument30 pagesMEFA - IV and V UnitsMOHAMMAD AZEEMANo ratings yet

- Anglais s1Document9 pagesAnglais s1JassNo ratings yet

- Fabm 1Document8 pagesFabm 1zachie7770No ratings yet

- ACCA NoteDocument21 pagesACCA NoteTanbir Ahsan RubelNo ratings yet

- Hand Out in Basic AccountingDocument32 pagesHand Out in Basic AccountingJemuell RedNo ratings yet

- Unit 1 External Financial Statements and Revenue RecognitionDocument31 pagesUnit 1 External Financial Statements and Revenue Recognitionestihdaf استهدافNo ratings yet

- Accounting and Financial MangementDocument25 pagesAccounting and Financial MangementSHASHINo ratings yet

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae Sasutil100% (1)

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae SasutilNo ratings yet

- What Is AccountingDocument29 pagesWhat Is Accountingmule mulugetaNo ratings yet

- Lecture in FUNAC 2Document84 pagesLecture in FUNAC 2Shaira Bloom RagonjanNo ratings yet

- Guideline For Financial AccountingDocument65 pagesGuideline For Financial AccountingKhánh PhươngNo ratings yet

- BS Unit 3Document4 pagesBS Unit 3Enea NastriNo ratings yet

- For ACCO 101 - Review of Accounting Concepts and Process (Part 1)Document32 pagesFor ACCO 101 - Review of Accounting Concepts and Process (Part 1)Fionna Rei DeGaliciaNo ratings yet

- Chapter 12 Managing The Finance FunctionDocument16 pagesChapter 12 Managing The Finance Functionedward0% (2)

- Reviewer FinanceDocument9 pagesReviewer FinanceChristine Marie RamirezNo ratings yet

- Chapter 2 HandoutsDocument15 pagesChapter 2 HandoutsBlackpink BtsNo ratings yet

- Business VocabularyDocument2 pagesBusiness VocabularyLiza BazileviciNo ratings yet

- ASSIGMENT ACC - EditedDocument9 pagesASSIGMENT ACC - EditedLuqman SyahbudinNo ratings yet

- Chapter IDocument90 pagesChapter IAdmasu GirmaNo ratings yet

- Parts of The Business Plan EntrepDocument6 pagesParts of The Business Plan EntrepBrev SobremisanaNo ratings yet

- Lesson 1 SFPDocument14 pagesLesson 1 SFPLydia Rivera100% (3)

- Types of Major AccountsDocument30 pagesTypes of Major AccountsEstelle GammadNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Rac 101 - Example of Journal Entries Posting and Extracting Trial BalanceDocument1 pageRac 101 - Example of Journal Entries Posting and Extracting Trial BalanceMiko MananiNo ratings yet

- Rac 101 - Trial Balance - An ExampleDocument1 pageRac 101 - Trial Balance - An ExampleMiko MananiNo ratings yet

- Rac 101 - Adjusting Entries or Year End AjustmentsDocument6 pagesRac 101 - Adjusting Entries or Year End AjustmentsMiko MananiNo ratings yet

- Online and Blended Courses-RCS102-Object Oriented Programming 2022Document2 pagesOnline and Blended Courses-RCS102-Object Oriented Programming 2022Miko MananiNo ratings yet

- Lesson: 39: Give and Take: Collective BargainingDocument32 pagesLesson: 39: Give and Take: Collective Bargainingsarthak1826No ratings yet

- Tugas 2Document14 pagesTugas 2Tri Sunanda FathanahNo ratings yet

- Kesari ToursDocument15 pagesKesari ToursBhumika ShrivastavaNo ratings yet

- NCFM Technical AnalysisDocument18 pagesNCFM Technical AnalysisJagannathasarmaNo ratings yet

- Ismailia Public Free Zone About UsDocument3 pagesIsmailia Public Free Zone About UsAhmed El-AdawyNo ratings yet

- Grade 4 Multiplication: Answer The QuestionsDocument6 pagesGrade 4 Multiplication: Answer The QuestionsEduGainNo ratings yet

- Vertical Integration at Suguna Poultry Farms - A Critical Look at Pro PoorDocument24 pagesVertical Integration at Suguna Poultry Farms - A Critical Look at Pro PoorRamen LewisNo ratings yet

- Executive SummaryDocument2 pagesExecutive SummaryAshlindah KisakuraNo ratings yet

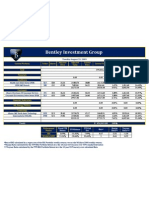

- Bentley Investment Group: Tuesday August 25, 2009Document1 pageBentley Investment Group: Tuesday August 25, 2009bentleyinvestmentgroupNo ratings yet

- Meaning of A Director: " Any Person Occupying The Position of Director, by Whatever Name Called" - Sec. 2Document21 pagesMeaning of A Director: " Any Person Occupying The Position of Director, by Whatever Name Called" - Sec. 2smsmbaNo ratings yet

- C39 - Fraud Awareness and Prevention - 2015 - AddendumDocument3 pagesC39 - Fraud Awareness and Prevention - 2015 - AddendumNidhi KatyalNo ratings yet

- International and Dutch Standards On Business and Human RightsDocument3 pagesInternational and Dutch Standards On Business and Human RightsjosienkapmaNo ratings yet

- AE13 Final ActivityDocument5 pagesAE13 Final ActivityWenjunNo ratings yet

- What Is Indivisible Works ContractDocument1 pageWhat Is Indivisible Works ContractAnonymous Q3J7APoNo ratings yet

- Advanced Corporate Finance 1st Edition Ogden Test BankDocument13 pagesAdvanced Corporate Finance 1st Edition Ogden Test Bankpottpotlacew8mf1t100% (17)

- A STUDY ON Financial Statement Analysis of Axis BankDocument94 pagesA STUDY ON Financial Statement Analysis of Axis BankKeleti Santhosh75% (8)

- When A New Manager Stumbles, Who's at Fault?Document11 pagesWhen A New Manager Stumbles, Who's at Fault?Shivam Khandelwal100% (1)

- SHRM Action PlanDocument3 pagesSHRM Action PlanAvery Jan Magabanua SilosNo ratings yet

- Scope of Health EconomicsDocument33 pagesScope of Health EconomicsSanjeev Chougule100% (2)

- BSIE Cost AccountingDocument5 pagesBSIE Cost AccountingJoovs JoovhoNo ratings yet

- Up SellingDocument3 pagesUp SellingNora GambronNo ratings yet

- Case Study SummaryDocument3 pagesCase Study Summary4 7No ratings yet

- A Literature Review On Social Enterprise: Yuting Zhang & Yong LiDocument6 pagesA Literature Review On Social Enterprise: Yuting Zhang & Yong LiJEFFREY WILLIAMS P M 20221013No ratings yet

- Personal Finance Canadian 7th Edition Kapoor Solutions ManualDocument25 pagesPersonal Finance Canadian 7th Edition Kapoor Solutions ManualDrAnnaHubbardDVMitaj100% (46)

- SPK Akugrosir 2018 (Staff Gudang) in EnglishDocument3 pagesSPK Akugrosir 2018 (Staff Gudang) in EnglishBimo Mahendra PutraNo ratings yet

- Howden Capabilities Oct 2017 ScreenDocument68 pagesHowden Capabilities Oct 2017 ScreenukdealsNo ratings yet

- Support Resistance For Day TradingDocument1,103 pagesSupport Resistance For Day Tradingnbhnbhnnb nhbbnh50% (2)

- Work To Build The Country: Mousumi NetworkDocument55 pagesWork To Build The Country: Mousumi NetworkSelim KhanNo ratings yet