Download as pdf or txt

You might also like

- 2024 Budget Deal - Fact SheetDocument5 pages2024 Budget Deal - Fact SheetRebecca C. LewisNo ratings yet

- Income From Property 1Document18 pagesIncome From Property 1aisha jabeenNo ratings yet

- Income Tax - VK SinghaniaDocument598 pagesIncome Tax - VK SinghaniaKartik67% (3)

- Tax Unit 1-2 - 25Document1 pageTax Unit 1-2 - 25joy BoseNo ratings yet

- Tax Unit 1-2 - 23Document1 pageTax Unit 1-2 - 23joy BoseNo ratings yet

- Income From House PropertyDocument3 pagesIncome From House PropertySneha PotekarNo ratings yet

- Rajasthan ActDocument237 pagesRajasthan Actabhinavanand6No ratings yet

- P P Namavati 019 EasementsDocument7 pagesP P Namavati 019 Easementsprajakta vaidyaNo ratings yet

- (uploadMB - Com) 18 - House PropertyDocument22 pages(uploadMB - Com) 18 - House PropertyhariomnarayanNo ratings yet

- Dogovor Za NaemDocument1 pageDogovor Za NaemKatya IvanovaNo ratings yet

- Tax Unit 1-2 - 18Document1 pageTax Unit 1-2 - 18joy BoseNo ratings yet

- En (1120)Document1 pageEn (1120)reacharunkNo ratings yet

- IFPDocument11 pagesIFPMuhammad JunaidNo ratings yet

- Income From House PropertyDocument9 pagesIncome From House PropertySukritiNo ratings yet

- House PropertyDocument12 pagesHouse Propertydhritipawar4No ratings yet

- Unit - 2: Income From House Property: After Studying This Chapter, You Would Be Able ToDocument47 pagesUnit - 2: Income From House Property: After Studying This Chapter, You Would Be Able Toadityaraj purohitNo ratings yet

- Chapter 10 15Document89 pagesChapter 10 15Aira Mae P. VispoNo ratings yet

- TAX 22-9-2020 Income From House PropertyDocument13 pagesTAX 22-9-2020 Income From House PropertyChitraNo ratings yet

- Distress BdosDocument7 pagesDistress BdosMichelle Webster100% (1)

- HUMTUM15 TH AugDocument2 pagesHUMTUM15 TH AugSushil_Pandey_4297No ratings yet

- 37 Income From House PropertyDocument7 pages37 Income From House Propertytejasgjain100% (1)

- Difference Pledge MortgageDocument6 pagesDifference Pledge MortgageJeffrey Constantino Patacsil100% (1)

- CG 3Document9 pagesCG 3Arnav MishraNo ratings yet

- Tax HandoutDocument6 pagesTax Handoutshekharsuhani5No ratings yet

- LeaseDocument8 pagesLeaseapi-3778039No ratings yet

- Land PowerPoint 4 - LeasesDocument46 pagesLand PowerPoint 4 - LeaseslabouzirouzNo ratings yet

- Apartment Lease Contract: This Is A Binding Document. Read Carefully Before SigningDocument63 pagesApartment Lease Contract: This Is A Binding Document. Read Carefully Before SigningDamien HowardNo ratings yet

- 316 - 340 LunzagaDocument24 pages316 - 340 LunzagaLUNZAGA JESSENo ratings yet

- Estate Tax Summary Tax CodeDocument1 pageEstate Tax Summary Tax CodeAlthea PalmaNo ratings yet

- Royalty AccountsDocument30 pagesRoyalty AccountsKavinraj R S0% (1)

- TAX 25-9-2020 DeductionsDocument3 pagesTAX 25-9-2020 DeductionsChitraNo ratings yet

- 56465bos45796cp4u2 PDFDocument49 pages56465bos45796cp4u2 PDFNarendra VasavanNo ratings yet

- House PropertyDocument18 pagesHouse PropertyNidhi LathNo ratings yet

- Comm Rev Abella NotesDocument65 pagesComm Rev Abella NotesRoger Montero Jr.No ratings yet

- Lease - Accessory Cs - CreditsDocument21 pagesLease - Accessory Cs - CreditsMikeeNo ratings yet

- Income Tax in Real Estate TransactionsDocument2 pagesIncome Tax in Real Estate TransactionsdavewagNo ratings yet

- Ordinary DeductionDocument1 pageOrdinary DeductionXhaNo ratings yet

- Rent May Be Defined As Re: That, Other Factors of Production, Whose Supply Is RelativelyDocument9 pagesRent May Be Defined As Re: That, Other Factors of Production, Whose Supply Is RelativelyStuti SinghNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House PropertyMonisha ParekhNo ratings yet

- The Yale Law Journal Company, Inc. The Yale Law JournalDocument5 pagesThe Yale Law Journal Company, Inc. The Yale Law JournalMUKUL DHIRANNo ratings yet

- CH 8 RPGT - Slides - Group 5Document47 pagesCH 8 RPGT - Slides - Group 5Maxamed YareNo ratings yet

- House Property ReturnDocument6 pagesHouse Property Returnkeshav315No ratings yet

- Chapter 4Document14 pagesChapter 4Ke LopezNo ratings yet

- To The Estate Upon Which The Refection Was Made, and OnlyDocument9 pagesTo The Estate Upon Which The Refection Was Made, and OnlyGracey PelagioNo ratings yet

- tp movableDocument1 pagetp movableABISHEKNo ratings yet

- Pre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFDocument106 pagesPre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFParmeet NainNo ratings yet

- Tax Unit 1-2 - 1-2Document2 pagesTax Unit 1-2 - 1-2joy BoseNo ratings yet

- Income From House Property: Section/Rule Subject MatterDocument29 pagesIncome From House Property: Section/Rule Subject MatterRajesh NangaliaNo ratings yet

- MemorandumsDocument4 pagesMemorandumsMyrna Joy JaposNo ratings yet

- Of Cost of Costing For Such: HouseDocument8 pagesOf Cost of Costing For Such: HousePriya100% (1)

- No. 21 of 1987Document44 pagesNo. 21 of 1987weeklylawimprintsNo ratings yet

- Commercial Law Review Abella PDFDocument71 pagesCommercial Law Review Abella PDFcarlo_tabangcuraNo ratings yet

- Tax Ranjan SirDocument111 pagesTax Ranjan SirMd. Anowar MorshedNo ratings yet

- Chapter 2 RoyaltiesDocument11 pagesChapter 2 Royaltiestawhid0000017No ratings yet

- Heads of Income: Unit - 2: Income From House PropertyDocument40 pagesHeads of Income: Unit - 2: Income From House PropertyMaheswar SethiNo ratings yet

- Project House PropertyDocument35 pagesProject House PropertyishichadhaNo ratings yet

- Income From House PropertDocument6 pagesIncome From House PropertAkshi JainNo ratings yet

- Income From House Property: After Studying This Chapter, You Would Be Able ToDocument35 pagesIncome From House Property: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Tax Unit 1-2 - 23Document1 pageTax Unit 1-2 - 23joy BoseNo ratings yet

- বাহাদুর বিড়াল (1)Document52 pagesবাহাদুর বিড়াল (1)joy BoseNo ratings yet

- Tax Unit 1-2 - 25Document1 pageTax Unit 1-2 - 25joy BoseNo ratings yet

- Tax Unit 1-2 - 16Document1 pageTax Unit 1-2 - 16joy BoseNo ratings yet

- ( )Document65 pages( )joy BoseNo ratings yet

- Tax Unit 1-2 - 24Document1 pageTax Unit 1-2 - 24joy BoseNo ratings yet

- Tax Unit 1-2 - 15Document1 pageTax Unit 1-2 - 15joy BoseNo ratings yet

- Tax Unit 1-2 - 21Document1 pageTax Unit 1-2 - 21joy BoseNo ratings yet

- Tax Unit 1-2 - 14Document1 pageTax Unit 1-2 - 14joy BoseNo ratings yet

- Tax Unit 1-2 - 18Document1 pageTax Unit 1-2 - 18joy BoseNo ratings yet

- Tax Unit 1-2 - 19Document1 pageTax Unit 1-2 - 19joy BoseNo ratings yet

- Tax Unit 1-2 - 22Document1 pageTax Unit 1-2 - 22joy BoseNo ratings yet

- Tax Unit 1-2 - 11Document1 pageTax Unit 1-2 - 11joy BoseNo ratings yet

- Ecom QuesDocument4 pagesEcom Quesjoy BoseNo ratings yet

- Tax Unit 1-2 - 7-8Document2 pagesTax Unit 1-2 - 7-8joy BoseNo ratings yet

- Nonte Fonte DhamakaDocument56 pagesNonte Fonte Dhamakajoy BoseNo ratings yet

- Nonte Fonte La JobabDocument55 pagesNonte Fonte La Jobabjoy BoseNo ratings yet

- Tax Unit 1-2 - 1-2Document2 pagesTax Unit 1-2 - 1-2joy BoseNo ratings yet

- Tax Unit 1-2 - 5-6Document2 pagesTax Unit 1-2 - 5-6joy BoseNo ratings yet

- Tax Unit 1-2 - 12Document1 pageTax Unit 1-2 - 12joy BoseNo ratings yet

- Tax Unit 1-2 - 9-10Document2 pagesTax Unit 1-2 - 9-10joy BoseNo ratings yet

- Tax Unit 1-2 - 3-4Document2 pagesTax Unit 1-2 - 3-4joy BoseNo ratings yet

- Cash and Accrual Basis ProblemsDocument1 pageCash and Accrual Basis ProblemsCAINo ratings yet

- Chakra Bahadur Oli Ward 5Document6 pagesChakra Bahadur Oli Ward 5deeploved2001No ratings yet

- GST (Impact On Common Man)Document2 pagesGST (Impact On Common Man)Kajal kumariNo ratings yet

- Sum of The YearsDocument9 pagesSum of The YearsMary Joy DelgadoNo ratings yet

- BAR Taxation Syllabus: I. General Principles of TaxationDocument12 pagesBAR Taxation Syllabus: I. General Principles of TaxationAnonymous wDganZNo ratings yet

- Direct and Indirect TaxesDocument14 pagesDirect and Indirect Taxeskratika singhNo ratings yet

- Budget 2023 2024Document12 pagesBudget 2023 2024finance bnbmNo ratings yet

- The Following Is A List of Possible Transactions 1 Purchased Inventory PDFDocument2 pagesThe Following Is A List of Possible Transactions 1 Purchased Inventory PDFTaimur TechnologistNo ratings yet

- Pakistan - Enigma of Taxation (Chapter VIII)Document6 pagesPakistan - Enigma of Taxation (Chapter VIII)Zaid NaveedNo ratings yet

- Casanovas V HordDocument11 pagesCasanovas V HordfullpizzaNo ratings yet

- Dashmesh Tractors and Farm EquipmentsDocument2 pagesDashmesh Tractors and Farm EquipmentsdashmeshNo ratings yet

- 7th Term - Legal Frameworks of ConstructionDocument79 pages7th Term - Legal Frameworks of ConstructionShreedharNo ratings yet

- Sarthak Enterprises-Sae14420: GST No: 24Aabca2390M1Zp State Code:24Document6 pagesSarthak Enterprises-Sae14420: GST No: 24Aabca2390M1Zp State Code:24Samir ShaikhNo ratings yet

- 06 Gross IncomeDocument103 pages06 Gross IncomeJSNo ratings yet

- Elements of Corporate TaxationDocument4 pagesElements of Corporate Taxationreggie1010No ratings yet

- Apv PDFDocument9 pagesApv PDFAnkit ThakurNo ratings yet

- Penalty and ProsecutionDocument19 pagesPenalty and Prosecutionmir makarim ahsanNo ratings yet

- Awb 6564652463Document1 pageAwb 6564652463Shahid SaleemNo ratings yet

- Price List 1950sft.Document1 pagePrice List 1950sft.IKONIC GROUPNo ratings yet

- Rate of Contribution To SSSDocument13 pagesRate of Contribution To SSSBiens IIINo ratings yet

- Capital Gains Tax-Chap6Document5 pagesCapital Gains Tax-Chap6Garcia Alizsandra L.No ratings yet

- Agriculture Income SynopsisDocument2 pagesAgriculture Income Synopsisqubrex1No ratings yet

- DocxDocument4 pagesDocxnicole bancoro100% (1)

- 1.permanent Account Number (Pan)Document10 pages1.permanent Account Number (Pan)akashNo ratings yet

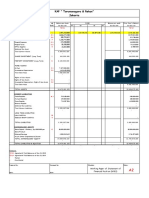

- KAP " Tarumanagara & Rekan" Jakarta: TB'20 TB'19 C E.1 E.2 F G.1 G.2 HDocument2 pagesKAP " Tarumanagara & Rekan" Jakarta: TB'20 TB'19 C E.1 E.2 F G.1 G.2 HAprijanti MalinoNo ratings yet

- CIR Vs CA G.R. No. 108358Document1 pageCIR Vs CA G.R. No. 108358ariel.decastroNo ratings yet

- Eros InvoiceDocument1 pageEros InvoiceRohit JhaNo ratings yet

- Quicknotes Tax MCQS Book 1 - Gen. Principles PDFDocument18 pagesQuicknotes Tax MCQS Book 1 - Gen. Principles PDFMethlyNo ratings yet

- National Income - Definitions - Lovish KakkarDocument2 pagesNational Income - Definitions - Lovish KakkarAjuni ShahNo ratings yet

- Jobseekers Notification - 03 - 05 - 23 PDFDocument4 pagesJobseekers Notification - 03 - 05 - 23 PDFPalombella BellaNo ratings yet