Download as pdf or txt

You might also like

- WMG Business Model SummaryDocument1 pageWMG Business Model SummaryAugustus CignaNo ratings yet

- Data Flow Diagram of Expenditure CycleDocument1 pageData Flow Diagram of Expenditure CycleWaynestonne Driz60% (5)

- Chapter 1Document94 pagesChapter 1Narendran SrinivasanNo ratings yet

- Financial InclusionbookDocument160 pagesFinancial InclusionbookRajendra LamsalNo ratings yet

- E-Banking in India: Services Provided by The Bank ThroughDocument21 pagesE-Banking in India: Services Provided by The Bank ThroughKomal SahuNo ratings yet

- Financial Access and The Finance - Growth Nexus - Evidence From Developing Economies PDFDocument16 pagesFinancial Access and The Finance - Growth Nexus - Evidence From Developing Economies PDFSucatta IDNo ratings yet

- Babu SinghDocument1 pageBabu SinghRohitNo ratings yet

- 5 Chapter Thesis RenaLihayLihay#updatedDocument146 pages5 Chapter Thesis RenaLihayLihay#updatedRena LihaylihayNo ratings yet

- Sakina LotiaDocument22 pagesSakina LotiaEldorado OSNo ratings yet

- Black BookDocument41 pagesBlack BookMoazza QureshiNo ratings yet

- Mutual FundsDocument35 pagesMutual FundsAmrita DasNo ratings yet

- 4.factors Impacting The Usage of E-Wallets in National CapitalDocument12 pages4.factors Impacting The Usage of E-Wallets in National Capitalphamuyen11012003No ratings yet

- Financial Management Practices of Restaurant Employees in Cabanatuan CityDocument4 pagesFinancial Management Practices of Restaurant Employees in Cabanatuan CityPoonam KilaniyaNo ratings yet

- Review of Related Literature and StudiesDocument14 pagesReview of Related Literature and StudiesAtasha MarLi IbbotsonNo ratings yet

- REVIEW OF LITERATURE ofDocument64 pagesREVIEW OF LITERATURE ofYash BangarNo ratings yet

- Ai Finance 1Document10 pagesAi Finance 1Purnachandrarao SudaNo ratings yet

- GST On Service Sector Handbook by ICAIDocument288 pagesGST On Service Sector Handbook by ICAIbasavaraj2772No ratings yet

- Sip Project On Hotel Industry PDFDocument34 pagesSip Project On Hotel Industry PDFDarshan BhanageNo ratings yet

- Manuscript Edited Tingal Et Al 3.editedDocument38 pagesManuscript Edited Tingal Et Al 3.editedDrenology Llamas IINo ratings yet

- Financial Literacy and Personal FinanciaDocument20 pagesFinancial Literacy and Personal FinanciaAby RuNo ratings yet

- Investment Behaviour of The Middle Class People in Chennai CityDocument27 pagesInvestment Behaviour of The Middle Class People in Chennai CityMajjer100% (1)

- Determinants of Non Performing Loans in Commercial Banks: A Study of NBC Bank Dodoma TanzaniaDocument25 pagesDeterminants of Non Performing Loans in Commercial Banks: A Study of NBC Bank Dodoma TanzaniaEdlamu Alemie100% (1)

- Enhancing Financial Inclusion Pakistan PostDocument14 pagesEnhancing Financial Inclusion Pakistan PostHareem AyeshaNo ratings yet

- Fintech and Financial Inclusion, Opportunities and PitfallsDocument26 pagesFintech and Financial Inclusion, Opportunities and PitfallsServing HumanityNo ratings yet

- BAFDocument100 pagesBAFiftikharhayderNo ratings yet

- THE Nalsar MBA 2023-25Document24 pagesTHE Nalsar MBA 2023-25Abhinav KumarNo ratings yet

- Group 3 ProjectDocument27 pagesGroup 3 ProjectAbhishek DhruvNo ratings yet

- Vision India 2025Document9 pagesVision India 2025Srinivas PrabhuNo ratings yet

- ProjectDocument93 pagesProjectDilip BalachandranNo ratings yet

- Universal Banking HDFCDocument62 pagesUniversal Banking HDFCrajesh bathulaNo ratings yet

- Dr. W - Saranya, V - Kausallya 2oba Converted by AbcdpdfDocument7 pagesDr. W - Saranya, V - Kausallya 2oba Converted by AbcdpdfAnkita RanaNo ratings yet

- Research Proposal On Customer SatisfactiDocument16 pagesResearch Proposal On Customer SatisfactiTofael HazariNo ratings yet

- Indian Banks Building Resilient LeadershipDocument88 pagesIndian Banks Building Resilient Leadershiparul.btugNo ratings yet

- Manuscript The Online Payment System PDFDocument158 pagesManuscript The Online Payment System PDFBERNELLIE MAE GUERRA ARANETANo ratings yet

- Mcom Sem 3 ProjectDocument50 pagesMcom Sem 3 Projectshruti janaskarNo ratings yet

- Immersion ProjectDocument62 pagesImmersion Projectraghavan swaminathanNo ratings yet

- Materi PayLaterDocument18 pagesMateri PayLaterJonathan Martin LimbongNo ratings yet

- 19 Kartik D KarkeraDocument73 pages19 Kartik D KarkeraAnkush SuryawanshiNo ratings yet

- 30-07-2022-1659161461-7-IJBGM-2. Reviewed - IJBGM - An Overview - Impact of FinTech in Indian Banking SectorDocument4 pages30-07-2022-1659161461-7-IJBGM-2. Reviewed - IJBGM - An Overview - Impact of FinTech in Indian Banking Sectoriaset123No ratings yet

- Anju Saroj Project WorkDocument101 pagesAnju Saroj Project WorkAnju SarojNo ratings yet

- Capital Mobility in Developing CountriesDocument41 pagesCapital Mobility in Developing CountriesEmir TermeNo ratings yet

- Hierarchical Chart BAPCCUL OKDocument1 pageHierarchical Chart BAPCCUL OKmunjukinzekaNo ratings yet

- Digital IndiaDocument10 pagesDigital IndiaMithil PatelNo ratings yet

- Effect of Investment Appraisal On The Profitability of Quoted Consumer Goods Companies in NigeriaDocument61 pagesEffect of Investment Appraisal On The Profitability of Quoted Consumer Goods Companies in NigeriaPrecious Chioma AgulukaNo ratings yet

- An Introduction To The Banking Sector in IndiaDocument69 pagesAn Introduction To The Banking Sector in Indiaghoshsubhankar1844No ratings yet

- SWETA SAH - SIP On WIPRO & INFOSYS LIMITED 2Document63 pagesSWETA SAH - SIP On WIPRO & INFOSYS LIMITED 2Sweta sahNo ratings yet

- 273 Simranjeet KaurDocument60 pages273 Simranjeet Kaurprathmesh666patilNo ratings yet

- Yes Bank Case Study 2Document10 pagesYes Bank Case Study 2AbhishekNo ratings yet

- Capital Structure, Capitalisation and LeverageDocument53 pagesCapital Structure, Capitalisation and LeverageCollins NyendwaNo ratings yet

- The Insolvency and Bankruptcy CodeDocument4 pagesThe Insolvency and Bankruptcy Codepranoti tardeNo ratings yet

- Summer Internship ProjectDocument75 pagesSummer Internship ProjectPratik ChavhanNo ratings yet

- Desis in UAE, UK and UAEDocument8 pagesDesis in UAE, UK and UAESchallim ReubenNo ratings yet

- Project Report On AdvertisingDocument67 pagesProject Report On AdvertisingKetan RathodNo ratings yet

- The Use of Social Networking Sites For Language Practice and LearningDocument28 pagesThe Use of Social Networking Sites For Language Practice and LearningHendi PratamaNo ratings yet

- Project On Retail Assets of BOB OkDocument76 pagesProject On Retail Assets of BOB OkKanchan100% (1)

- A Study On Online Payment Methods Among College Students With Special Reference To Christ CollegeDocument60 pagesA Study On Online Payment Methods Among College Students With Special Reference To Christ CollegeAnjaliNo ratings yet

- Financial Inclusion: Know All About ItDocument9 pagesFinancial Inclusion: Know All About ItAnjita SrivastavaNo ratings yet

- Big Data Features, Applications, and Analytics in Cardiology-A Systematic Literature ReviewDocument30 pagesBig Data Features, Applications, and Analytics in Cardiology-A Systematic Literature ReviewMuhammad Tanzeel Qaisar DogarNo ratings yet

- A Comparative Study On Financial Literacy Among Arts and Science College Students Ijariie3989Document5 pagesA Comparative Study On Financial Literacy Among Arts and Science College Students Ijariie3989Shobiga V100% (1)

- University of Hargeisa Hargeisa School eDocument22 pagesUniversity of Hargeisa Hargeisa School eamira yonisNo ratings yet

- Regulators Regulations Dec 2021Document44 pagesRegulators Regulations Dec 2021Ravi Shankar VermaNo ratings yet

- A Project Report On Banking 29Document28 pagesA Project Report On Banking 29manojkumaryadav2514No ratings yet

- CSD Chinese Mandarin CvsuDocument17 pagesCSD Chinese Mandarin CvsuKevin MagnoNo ratings yet

- 2badillo Pre Sioson ENCODED ACTUAL Survey ResultsDocument37 pages2badillo Pre Sioson ENCODED ACTUAL Survey ResultsKevin MagnoNo ratings yet

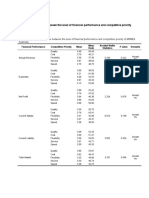

- Analysis of Difference Between The Level of Financial Performance and Competitive Priority of MSMEs BusinessDocument1 pageAnalysis of Difference Between The Level of Financial Performance and Competitive Priority of MSMEs BusinessKevin MagnoNo ratings yet

- Actual Thesis Manuscript - Badillo, Pre, SiosonDocument80 pagesActual Thesis Manuscript - Badillo, Pre, SiosonKevin MagnoNo ratings yet

- Final Exam ORAL PRESENTATIONDocument1 pageFinal Exam ORAL PRESENTATIONKevin MagnoNo ratings yet

- Results Objective 4Document5 pagesResults Objective 4Kevin MagnoNo ratings yet

- Results Objective 5Document2 pagesResults Objective 5Kevin MagnoNo ratings yet

- Heavy Equipment Sales ProposalDocument5 pagesHeavy Equipment Sales Proposalyummy playlist mineNo ratings yet

- Final Media-Plan-Fazaia-Housing-Scheme-Aviation-City-Kamra 10 DecDocument49 pagesFinal Media-Plan-Fazaia-Housing-Scheme-Aviation-City-Kamra 10 DecMuntaha Arbab100% (1)

- Case StudyDocument2 pagesCase StudyXie marquezNo ratings yet

- Bhagwati Steel CentreDocument8 pagesBhagwati Steel CentreMuhammad ArslanNo ratings yet

- Moses ResumeDocument3 pagesMoses ResumehenryNo ratings yet

- b1 Solving Set 3 May 2018 - OnlineDocument4 pagesb1 Solving Set 3 May 2018 - OnlineGadafi FuadNo ratings yet

- Falak Ishrat Bba Mba Integrated ECON153Document20 pagesFalak Ishrat Bba Mba Integrated ECON153sehar Ishrat SiddiquiNo ratings yet

- Career Opportunities in HousekeepingDocument12 pagesCareer Opportunities in HousekeepingRohan HundareNo ratings yet

- ICM (Communication Work)Document6 pagesICM (Communication Work)Rifki Warri ZainNo ratings yet

- Value Creation (Tesla) - 1Document20 pagesValue Creation (Tesla) - 1OpeyemiNo ratings yet

- MARKETING-"Pricing" Present By: Jasmi Noor Bin SahudinDocument8 pagesMARKETING-"Pricing" Present By: Jasmi Noor Bin SahudinMohd Faisal BaharuddinNo ratings yet

- Midterm Exam November2021 SolutionDocument9 pagesMidterm Exam November2021 SolutionLuca VanzNo ratings yet

- Publisher Version (Open Access)Document67 pagesPublisher Version (Open Access)spiconsultantdaNo ratings yet

- Heliyon: Tomy Perdana, Diah Chaerani, Audi Luqmanul Hakim Achmad, Fernianda Rahayu HermiatinDocument22 pagesHeliyon: Tomy Perdana, Diah Chaerani, Audi Luqmanul Hakim Achmad, Fernianda Rahayu HermiatinFernianda RahayuNo ratings yet

- BSBHRM506 Student AssessmentDocument81 pagesBSBHRM506 Student Assessmentklm klmNo ratings yet

- Block Work and PlasteringDocument7 pagesBlock Work and Plasteringmohammed sohail100% (1)

- Fayol - 5 Functions of ManagementDocument1 pageFayol - 5 Functions of ManagementNurun NabiNo ratings yet

- NSTP - Entrepreneurship - Starting and Growing The BusinessDocument23 pagesNSTP - Entrepreneurship - Starting and Growing The BusinessShiela May FeriaNo ratings yet

- Kuratko9eCh07 - Pathways To Entrepreneurial Ventures - ClassDocument27 pagesKuratko9eCh07 - Pathways To Entrepreneurial Ventures - Classbristikhan405No ratings yet

- Korn Ferry RPO EbookDocument30 pagesKorn Ferry RPO EbookHafizNo ratings yet

- NIKE CASE - Alice Roullet de La BouillerieDocument9 pagesNIKE CASE - Alice Roullet de La BouillerieAlice dlbNo ratings yet

- I-03 07problemDocument1 pageI-03 07problemmnrk 1997No ratings yet

- Accounting Fifo LifoDocument7 pagesAccounting Fifo LifoFariha tamannaNo ratings yet

- Lounge Access List World PDFDocument4 pagesLounge Access List World PDFashwin16No ratings yet

- Lesson 2 2Document15 pagesLesson 2 2Angela MagtibayNo ratings yet

- Format Lembar Kerja AkuntansiDocument29 pagesFormat Lembar Kerja AkuntansiBudi SusantoNo ratings yet

- Cost Sheet - PVR ScreenDocument1 pageCost Sheet - PVR ScreensumitNo ratings yet

- Context of BusinessDocument10 pagesContext of BusinessMd. Ariful Haque ChowdhuryNo ratings yet