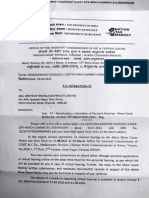

Sunworld Infrastructure PLtdvs Income Tax Officer, Ward 2

Sunworld Infrastructure PLtdvs Income Tax Officer, Ward 2

You might also like

- Almanzar v. KebeDocument8 pagesAlmanzar v. KebeBillboard100% (1)

- Motion For Judicial Notice - Motion To ReconsiderDocument5 pagesMotion For Judicial Notice - Motion To ReconsiderMarc MkKoy100% (3)

- Sales Agency AgreementDocument3 pagesSales Agency AgreementNef Urja ChautariNo ratings yet

- Mumbai Itat On Service of Notice by Affixture Section 282Document15 pagesMumbai Itat On Service of Notice by Affixture Section 282hvdatar8898No ratings yet

- 2024 01 17 2023 157 Taxmann Com 125 Delhi 31 01 2023 Indo Laminates P LTD Vs Assessment UnitDocument3 pages2024 01 17 2023 157 Taxmann Com 125 Delhi 31 01 2023 Indo Laminates P LTD Vs Assessment UnitCA Ujjwal GuptaNo ratings yet

- Asst Order Ankur Gupta AY 2022-23Document2 pagesAsst Order Ankur Gupta AY 2022-23basecandlesNo ratings yet

- 1 Judgment-WPL 11293-21.odtDocument30 pages1 Judgment-WPL 11293-21.odtAlok SinghNo ratings yet

- Indo Office Solutions (P) Ltd. Versus ACIT, Central Circle-17, New DelhiDocument6 pagesIndo Office Solutions (P) Ltd. Versus ACIT, Central Circle-17, New DelhiAshish GoelNo ratings yet

- Rajasthan HC Rampal Samdani - 148 - Change of Opinion - After 4 YearsDocument10 pagesRajasthan HC Rampal Samdani - 148 - Change of Opinion - After 4 YearsSubramanyam SettyNo ratings yet

- Income Tax Department. ... The Process of Examination of The Return by The Income Tax DepartmentDocument36 pagesIncome Tax Department. ... The Process of Examination of The Return by The Income Tax DepartmentjcnakwjecbNo ratings yet

- DocumentDocument2 pagesDocumentSubrata HalderNo ratings yet

- Itr-V Adyps7344c 2023-24 149225400310723Document1 pageItr-V Adyps7344c 2023-24 149225400310723taxindia610No ratings yet

- Alok Bhandari Anr. vs. ACIT ITAT DelhiDocument7 pagesAlok Bhandari Anr. vs. ACIT ITAT DelhivedaNo ratings yet

- Versus: 2023:BHC-OS:12955-DBDocument4 pagesVersus: 2023:BHC-OS:12955-DBkumarhealthcare2000No ratings yet

- Afcan Reply 133Document1 pageAfcan Reply 133rajorajisunnyNo ratings yet

- ITATDocument16 pagesITATKarthikNo ratings yet

- AKTPS1245A - Notice Us 142 (1) - 06032022Document3 pagesAKTPS1245A - Notice Us 142 (1) - 06032022Birdhi ChandNo ratings yet

- Chemetall Rai India LimitedDocument6 pagesChemetall Rai India LimitedvedaNo ratings yet

- Assessment Order1000231549602017Document3 pagesAssessment Order1000231549602017AdvocateNitinsharmaNo ratings yet

- TC Minutes - Maintenance PAGT DischargedDocument14 pagesTC Minutes - Maintenance PAGT Dischargedimhrishi12No ratings yet

- Moot PropositionDocument38 pagesMoot PropositionshantanuNo ratings yet

- FRPPK9574Q - Order Pass Us 148A - 1050920243 (1) - 18032023Document4 pagesFRPPK9574Q - Order Pass Us 148A - 1050920243 (1) - 18032023atishrijiNo ratings yet

- AssessmentProcedure 3rdsepDocument16 pagesAssessmentProcedure 3rdseparshNo ratings yet

- Adjudication Order in Respect of Golden Soya Ltd. (In The Matter of Non Redressal of Investor Grievances and Non Obtaining of SCORES Authentication)Document7 pagesAdjudication Order in Respect of Golden Soya Ltd. (In The Matter of Non Redressal of Investor Grievances and Non Obtaining of SCORES Authentication)Shyam SunderNo ratings yet

- 1684303940-ITA No.1070-D-2022 - Havells India LTDDocument5 pages1684303940-ITA No.1070-D-2022 - Havells India LTDArulnidhi Ramanathan SeshanNo ratings yet

- PDF 334657210280923Document1 pagePDF 334657210280923Manish NirwanNo ratings yet

- Rajeev Ratanlal Tulshyan Vs ITO ITAT MumbaiDocument14 pagesRajeev Ratanlal Tulshyan Vs ITO ITAT Mumbaisolanki.bharatNo ratings yet

- Assessment: Issues in Assessment & Reassessment Under I. T. ActDocument36 pagesAssessment: Issues in Assessment & Reassessment Under I. T. ActSUNILNo ratings yet

- Appral GrievanceDocument24 pagesAppral GrievanceGOKUL NATHNo ratings yet

- Offshore Expenses Incurred Can Be Claimed Using This Form: Travel Self and Family - Sub Total: 1416.00 (INR)Document1 pageOffshore Expenses Incurred Can Be Claimed Using This Form: Travel Self and Family - Sub Total: 1416.00 (INR)chrreddyNo ratings yet

- jgjListFile ZPHUAB9TghjgjDocument219 pagesjgjListFile ZPHUAB9TghjgjA Common Man MahiNo ratings yet

- Indian Income Tax Return Verification FormDocument1 pageIndian Income Tax Return Verification FormRahul BhanNo ratings yet

- Hotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.InDocument2 pagesHotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.Insanjiv kumarNo ratings yet

- 14374752Document2 pages14374752Anshul MehtaNo ratings yet

- Penalty Notice - Dhanush - AY 2016-17Document2 pagesPenalty Notice - Dhanush - AY 2016-17client itNo ratings yet

- 2023 - AST - 7000000066219100 - 87442168 - 2023 - AST - FRPPK9574Q - Order Us 147 - 1063432472 (1) - 27032024Document6 pages2023 - AST - 7000000066219100 - 87442168 - 2023 - AST - FRPPK9574Q - Order Us 147 - 1063432472 (1) - 27032024atishrijiNo ratings yet

- JV IMPEX (Remand Back)Document9 pagesJV IMPEX (Remand Back)mau8684No ratings yet

- L9235515100521Document3 pagesL9235515100521dycmmgncrNo ratings yet

- Assessmnt Order Us 144 & 147 - Dhanush - AY 2016-17Document3 pagesAssessmnt Order Us 144 & 147 - Dhanush - AY 2016-17client itNo ratings yet

- Sanjaybhai Ranchhodbhai Patel (1) - WatermarkDocument4 pagesSanjaybhai Ranchhodbhai Patel (1) - Watermarkbcda66334No ratings yet

- Index - Crew BossDocument1 pageIndex - Crew Bossaditya sharmaNo ratings yet

- AEWPT4779H - Show Cause Notice For Proceedings Us 143 (3) - 1058063019 (1) - 20112023Document2 pagesAEWPT4779H - Show Cause Notice For Proceedings Us 143 (3) - 1058063019 (1) - 20112023Corman LimitedNo ratings yet

- Cit (A)Document8 pagesCit (A)Raaja ThalapathyNo ratings yet

- Audit Report 22-23Document18 pagesAudit Report 22-23info.capifutureNo ratings yet

- 'CL 2021 22 (1) 3Document24 pages'CL 2021 22 (1) 3aakash jainNo ratings yet

- Department Name I&Cad: Transaction Fee DetailsDocument3 pagesDepartment Name I&Cad: Transaction Fee DetailsRoja GuthiReddyNo ratings yet

- 2023transco - MS 9Document1 page2023transco - MS 9Raajesh VinukondaNo ratings yet

- Ilovepdf MergedDocument58 pagesIlovepdf MergedGaurav shuklaNo ratings yet

- Form 16Document22 pagesForm 16Ajay Chowdary Ajay ChowdaryNo ratings yet

- E Newsletter September 2013Document13 pagesE Newsletter September 2013sd naikNo ratings yet

- Adjudication Order in Respect of Datar Switchgear LTD in The Matter of Non Redressal of Investor Complaints.Document7 pagesAdjudication Order in Respect of Datar Switchgear LTD in The Matter of Non Redressal of Investor Complaints.Shyam SunderNo ratings yet

- Aa2401240042705 SCN02012024Document1 pageAa2401240042705 SCN02012024vikenveerNo ratings yet

- Print FileDocument6 pagesPrint FileShahid AminNo ratings yet

- 2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsDocument11 pages2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsAbhishek JainNo ratings yet

- "Noticee"/ "The Company") Had Failed To Redress The Investor Grievances. TheDocument4 pages"Noticee"/ "The Company") Had Failed To Redress The Investor Grievances. TheJairaam PrasadNo ratings yet

- Kusum Gupta v. ITO (Delhi HC)Document6 pagesKusum Gupta v. ITO (Delhi HC)Avar LambaNo ratings yet

- 21 - 30221463102456 NCR JhansiDocument2 pages21 - 30221463102456 NCR JhansiAbhishek DahiyaNo ratings yet

- Withgrawal ApplicationDocument9 pagesWithgrawal ApplicationRavi YadavNo ratings yet

- Page 1/3Document3 pagesPage 1/3Ankur MishraNo ratings yet

- 2022.09.16 CM 1031 of 2022 in CA 110 of 2022 Application For Reference To High Court FinalDocument69 pages2022.09.16 CM 1031 of 2022 in CA 110 of 2022 Application For Reference To High Court FinalSarvadaman OberoiNo ratings yet

- Anil Marda 143 2 NoticeDocument32 pagesAnil Marda 143 2 NoticeLNo ratings yet

- Power Roles and Responsibilities - Offences Booked by Roving Squad OfficersDocument16 pagesPower Roles and Responsibilities - Offences Booked by Roving Squad OfficersAnandd BabunathNo ratings yet

- Swati Malove Divetiavs Income Tax OfficerDocument4 pagesSwati Malove Divetiavs Income Tax OfficerAnandd BabunathNo ratings yet

- GST & Central ExciseDocument2 pagesGST & Central ExciseAnandd BabunathNo ratings yet

- Draft Disclosures of ICDS in Clause 13 (F) of Form 3CD: CA. Pramod JainDocument9 pagesDraft Disclosures of ICDS in Clause 13 (F) of Form 3CD: CA. Pramod JainAnandd BabunathNo ratings yet

- Republic Vs SantosDocument13 pagesRepublic Vs SantosSachuzenNo ratings yet

- Contract Law TutorialDocument3 pagesContract Law TutorialSarah DarkoNo ratings yet

- Zafra vs. CADocument2 pagesZafra vs. CAJean Ben Go SingsonNo ratings yet

- Right To Constitutional Remedies: Article-32Document22 pagesRight To Constitutional Remedies: Article-32Dolphin100% (1)

- Functional Responsibility of International Organisations The European Union and International Economic Law (Emilija Leinarte)Document292 pagesFunctional Responsibility of International Organisations The European Union and International Economic Law (Emilija Leinarte)andremiguelrosa5352No ratings yet

- Endaya vs. CA PDFDocument8 pagesEndaya vs. CA PDFLynne AgapitoNo ratings yet

- Nava History Reflection PaperDocument5 pagesNava History Reflection PaperAnonymous QmnYZ5IXJINo ratings yet

- Abella v. NLRCDocument2 pagesAbella v. NLRCNHYNo ratings yet

- GH00224 - SANRU - Y2 Application - TR - Comments-Recommandations PDFDocument215 pagesGH00224 - SANRU - Y2 Application - TR - Comments-Recommandations PDFDenis MatshifiNo ratings yet

- Dui PDFDocument2 pagesDui PDFbearj7637No ratings yet

- Penalty and ProsecutionDocument19 pagesPenalty and Prosecutionmir makarim ahsanNo ratings yet

- Sakshi Powers ConstiDocument13 pagesSakshi Powers Constishivank kumarNo ratings yet

- Company Exam 2021 ADocument6 pagesCompany Exam 2021 AsrvshNo ratings yet

- CM 3013 2023 REV 1 - enDocument6 pagesCM 3013 2023 REV 1 - enA. KatsarakisNo ratings yet

- People Vs BalotolDocument2 pagesPeople Vs BalotolJules VosotrosNo ratings yet

- Pro Line Sports Center Vs CADocument2 pagesPro Line Sports Center Vs CAJulius ManaloNo ratings yet

- When There Was No Agreement Between The Parties Regarding Essential Terms of The Agreement - No Consensus Ad-Idem As Such No Valid Contract To Be Enforced 1990 SCDocument12 pagesWhen There Was No Agreement Between The Parties Regarding Essential Terms of The Agreement - No Consensus Ad-Idem As Such No Valid Contract To Be Enforced 1990 SCSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್No ratings yet

- Role of International Society in Political ObligatioDocument6 pagesRole of International Society in Political ObligatioVibhutiNo ratings yet

- Points of Land Law - 5Document6 pagesPoints of Land Law - 5Vyankatesh GotalkarNo ratings yet

- Criminal Law: Answers To Bar Examination Questions INDocument169 pagesCriminal Law: Answers To Bar Examination Questions INPam Otic-ReyesNo ratings yet

- Macariola vs. Ascunsion, Adm. Case No. 133-J May 31, 1982Document16 pagesMacariola vs. Ascunsion, Adm. Case No. 133-J May 31, 1982Tin SagmonNo ratings yet

- PSIR Test 9 CASTE, RELIGION ANDDocument11 pagesPSIR Test 9 CASTE, RELIGION ANDtjravi26No ratings yet

- Gashumba V NkudiyeDocument7 pagesGashumba V NkudiyeAshraf KiswiririNo ratings yet

- City of Naga vs. Hon. Elvi John S. AsuncionDocument2 pagesCity of Naga vs. Hon. Elvi John S. AsuncionJillian Asdala100% (1)

- Pondicherry Pawnbrokers Act 1966Document30 pagesPondicherry Pawnbrokers Act 1966Latest Laws TeamNo ratings yet

- United States v. Goldhammer, 4th Cir. (2005)Document2 pagesUnited States v. Goldhammer, 4th Cir. (2005)Scribd Government DocsNo ratings yet

- Georgia Evidence Quick Reference Guide 1707358659Document4 pagesGeorgia Evidence Quick Reference Guide 1707358659kirakimneyNo ratings yet

Download as rtf, pdf, or txt

You might also like

- Almanzar v. KebeDocument8 pagesAlmanzar v. KebeBillboard100% (1)

- Motion For Judicial Notice - Motion To ReconsiderDocument5 pagesMotion For Judicial Notice - Motion To ReconsiderMarc MkKoy100% (3)

- Sales Agency AgreementDocument3 pagesSales Agency AgreementNef Urja ChautariNo ratings yet

- Mumbai Itat On Service of Notice by Affixture Section 282Document15 pagesMumbai Itat On Service of Notice by Affixture Section 282hvdatar8898No ratings yet

- 2024 01 17 2023 157 Taxmann Com 125 Delhi 31 01 2023 Indo Laminates P LTD Vs Assessment UnitDocument3 pages2024 01 17 2023 157 Taxmann Com 125 Delhi 31 01 2023 Indo Laminates P LTD Vs Assessment UnitCA Ujjwal GuptaNo ratings yet

- Asst Order Ankur Gupta AY 2022-23Document2 pagesAsst Order Ankur Gupta AY 2022-23basecandlesNo ratings yet

- 1 Judgment-WPL 11293-21.odtDocument30 pages1 Judgment-WPL 11293-21.odtAlok SinghNo ratings yet

- Indo Office Solutions (P) Ltd. Versus ACIT, Central Circle-17, New DelhiDocument6 pagesIndo Office Solutions (P) Ltd. Versus ACIT, Central Circle-17, New DelhiAshish GoelNo ratings yet

- Rajasthan HC Rampal Samdani - 148 - Change of Opinion - After 4 YearsDocument10 pagesRajasthan HC Rampal Samdani - 148 - Change of Opinion - After 4 YearsSubramanyam SettyNo ratings yet

- Income Tax Department. ... The Process of Examination of The Return by The Income Tax DepartmentDocument36 pagesIncome Tax Department. ... The Process of Examination of The Return by The Income Tax DepartmentjcnakwjecbNo ratings yet

- DocumentDocument2 pagesDocumentSubrata HalderNo ratings yet

- Itr-V Adyps7344c 2023-24 149225400310723Document1 pageItr-V Adyps7344c 2023-24 149225400310723taxindia610No ratings yet

- Alok Bhandari Anr. vs. ACIT ITAT DelhiDocument7 pagesAlok Bhandari Anr. vs. ACIT ITAT DelhivedaNo ratings yet

- Versus: 2023:BHC-OS:12955-DBDocument4 pagesVersus: 2023:BHC-OS:12955-DBkumarhealthcare2000No ratings yet

- Afcan Reply 133Document1 pageAfcan Reply 133rajorajisunnyNo ratings yet

- ITATDocument16 pagesITATKarthikNo ratings yet

- AKTPS1245A - Notice Us 142 (1) - 06032022Document3 pagesAKTPS1245A - Notice Us 142 (1) - 06032022Birdhi ChandNo ratings yet

- Chemetall Rai India LimitedDocument6 pagesChemetall Rai India LimitedvedaNo ratings yet

- Assessment Order1000231549602017Document3 pagesAssessment Order1000231549602017AdvocateNitinsharmaNo ratings yet

- TC Minutes - Maintenance PAGT DischargedDocument14 pagesTC Minutes - Maintenance PAGT Dischargedimhrishi12No ratings yet

- Moot PropositionDocument38 pagesMoot PropositionshantanuNo ratings yet

- FRPPK9574Q - Order Pass Us 148A - 1050920243 (1) - 18032023Document4 pagesFRPPK9574Q - Order Pass Us 148A - 1050920243 (1) - 18032023atishrijiNo ratings yet

- AssessmentProcedure 3rdsepDocument16 pagesAssessmentProcedure 3rdseparshNo ratings yet

- Adjudication Order in Respect of Golden Soya Ltd. (In The Matter of Non Redressal of Investor Grievances and Non Obtaining of SCORES Authentication)Document7 pagesAdjudication Order in Respect of Golden Soya Ltd. (In The Matter of Non Redressal of Investor Grievances and Non Obtaining of SCORES Authentication)Shyam SunderNo ratings yet

- 1684303940-ITA No.1070-D-2022 - Havells India LTDDocument5 pages1684303940-ITA No.1070-D-2022 - Havells India LTDArulnidhi Ramanathan SeshanNo ratings yet

- PDF 334657210280923Document1 pagePDF 334657210280923Manish NirwanNo ratings yet

- Rajeev Ratanlal Tulshyan Vs ITO ITAT MumbaiDocument14 pagesRajeev Ratanlal Tulshyan Vs ITO ITAT Mumbaisolanki.bharatNo ratings yet

- Assessment: Issues in Assessment & Reassessment Under I. T. ActDocument36 pagesAssessment: Issues in Assessment & Reassessment Under I. T. ActSUNILNo ratings yet

- Appral GrievanceDocument24 pagesAppral GrievanceGOKUL NATHNo ratings yet

- Offshore Expenses Incurred Can Be Claimed Using This Form: Travel Self and Family - Sub Total: 1416.00 (INR)Document1 pageOffshore Expenses Incurred Can Be Claimed Using This Form: Travel Self and Family - Sub Total: 1416.00 (INR)chrreddyNo ratings yet

- jgjListFile ZPHUAB9TghjgjDocument219 pagesjgjListFile ZPHUAB9TghjgjA Common Man MahiNo ratings yet

- Indian Income Tax Return Verification FormDocument1 pageIndian Income Tax Return Verification FormRahul BhanNo ratings yet

- Hotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.InDocument2 pagesHotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.Insanjiv kumarNo ratings yet

- 14374752Document2 pages14374752Anshul MehtaNo ratings yet

- Penalty Notice - Dhanush - AY 2016-17Document2 pagesPenalty Notice - Dhanush - AY 2016-17client itNo ratings yet

- 2023 - AST - 7000000066219100 - 87442168 - 2023 - AST - FRPPK9574Q - Order Us 147 - 1063432472 (1) - 27032024Document6 pages2023 - AST - 7000000066219100 - 87442168 - 2023 - AST - FRPPK9574Q - Order Us 147 - 1063432472 (1) - 27032024atishrijiNo ratings yet

- JV IMPEX (Remand Back)Document9 pagesJV IMPEX (Remand Back)mau8684No ratings yet

- L9235515100521Document3 pagesL9235515100521dycmmgncrNo ratings yet

- Assessmnt Order Us 144 & 147 - Dhanush - AY 2016-17Document3 pagesAssessmnt Order Us 144 & 147 - Dhanush - AY 2016-17client itNo ratings yet

- Sanjaybhai Ranchhodbhai Patel (1) - WatermarkDocument4 pagesSanjaybhai Ranchhodbhai Patel (1) - Watermarkbcda66334No ratings yet

- Index - Crew BossDocument1 pageIndex - Crew Bossaditya sharmaNo ratings yet

- AEWPT4779H - Show Cause Notice For Proceedings Us 143 (3) - 1058063019 (1) - 20112023Document2 pagesAEWPT4779H - Show Cause Notice For Proceedings Us 143 (3) - 1058063019 (1) - 20112023Corman LimitedNo ratings yet

- Cit (A)Document8 pagesCit (A)Raaja ThalapathyNo ratings yet

- Audit Report 22-23Document18 pagesAudit Report 22-23info.capifutureNo ratings yet

- 'CL 2021 22 (1) 3Document24 pages'CL 2021 22 (1) 3aakash jainNo ratings yet

- Department Name I&Cad: Transaction Fee DetailsDocument3 pagesDepartment Name I&Cad: Transaction Fee DetailsRoja GuthiReddyNo ratings yet

- 2023transco - MS 9Document1 page2023transco - MS 9Raajesh VinukondaNo ratings yet

- Ilovepdf MergedDocument58 pagesIlovepdf MergedGaurav shuklaNo ratings yet

- Form 16Document22 pagesForm 16Ajay Chowdary Ajay ChowdaryNo ratings yet

- E Newsletter September 2013Document13 pagesE Newsletter September 2013sd naikNo ratings yet

- Adjudication Order in Respect of Datar Switchgear LTD in The Matter of Non Redressal of Investor Complaints.Document7 pagesAdjudication Order in Respect of Datar Switchgear LTD in The Matter of Non Redressal of Investor Complaints.Shyam SunderNo ratings yet

- Aa2401240042705 SCN02012024Document1 pageAa2401240042705 SCN02012024vikenveerNo ratings yet

- Print FileDocument6 pagesPrint FileShahid AminNo ratings yet

- 2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsDocument11 pages2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsAbhishek JainNo ratings yet

- "Noticee"/ "The Company") Had Failed To Redress The Investor Grievances. TheDocument4 pages"Noticee"/ "The Company") Had Failed To Redress The Investor Grievances. TheJairaam PrasadNo ratings yet

- Kusum Gupta v. ITO (Delhi HC)Document6 pagesKusum Gupta v. ITO (Delhi HC)Avar LambaNo ratings yet

- 21 - 30221463102456 NCR JhansiDocument2 pages21 - 30221463102456 NCR JhansiAbhishek DahiyaNo ratings yet

- Withgrawal ApplicationDocument9 pagesWithgrawal ApplicationRavi YadavNo ratings yet

- Page 1/3Document3 pagesPage 1/3Ankur MishraNo ratings yet

- 2022.09.16 CM 1031 of 2022 in CA 110 of 2022 Application For Reference To High Court FinalDocument69 pages2022.09.16 CM 1031 of 2022 in CA 110 of 2022 Application For Reference To High Court FinalSarvadaman OberoiNo ratings yet

- Anil Marda 143 2 NoticeDocument32 pagesAnil Marda 143 2 NoticeLNo ratings yet

- Power Roles and Responsibilities - Offences Booked by Roving Squad OfficersDocument16 pagesPower Roles and Responsibilities - Offences Booked by Roving Squad OfficersAnandd BabunathNo ratings yet

- Swati Malove Divetiavs Income Tax OfficerDocument4 pagesSwati Malove Divetiavs Income Tax OfficerAnandd BabunathNo ratings yet

- GST & Central ExciseDocument2 pagesGST & Central ExciseAnandd BabunathNo ratings yet

- Draft Disclosures of ICDS in Clause 13 (F) of Form 3CD: CA. Pramod JainDocument9 pagesDraft Disclosures of ICDS in Clause 13 (F) of Form 3CD: CA. Pramod JainAnandd BabunathNo ratings yet

- Republic Vs SantosDocument13 pagesRepublic Vs SantosSachuzenNo ratings yet

- Contract Law TutorialDocument3 pagesContract Law TutorialSarah DarkoNo ratings yet

- Zafra vs. CADocument2 pagesZafra vs. CAJean Ben Go SingsonNo ratings yet

- Right To Constitutional Remedies: Article-32Document22 pagesRight To Constitutional Remedies: Article-32Dolphin100% (1)

- Functional Responsibility of International Organisations The European Union and International Economic Law (Emilija Leinarte)Document292 pagesFunctional Responsibility of International Organisations The European Union and International Economic Law (Emilija Leinarte)andremiguelrosa5352No ratings yet

- Endaya vs. CA PDFDocument8 pagesEndaya vs. CA PDFLynne AgapitoNo ratings yet

- Nava History Reflection PaperDocument5 pagesNava History Reflection PaperAnonymous QmnYZ5IXJINo ratings yet

- Abella v. NLRCDocument2 pagesAbella v. NLRCNHYNo ratings yet

- GH00224 - SANRU - Y2 Application - TR - Comments-Recommandations PDFDocument215 pagesGH00224 - SANRU - Y2 Application - TR - Comments-Recommandations PDFDenis MatshifiNo ratings yet

- Dui PDFDocument2 pagesDui PDFbearj7637No ratings yet

- Penalty and ProsecutionDocument19 pagesPenalty and Prosecutionmir makarim ahsanNo ratings yet

- Sakshi Powers ConstiDocument13 pagesSakshi Powers Constishivank kumarNo ratings yet

- Company Exam 2021 ADocument6 pagesCompany Exam 2021 AsrvshNo ratings yet

- CM 3013 2023 REV 1 - enDocument6 pagesCM 3013 2023 REV 1 - enA. KatsarakisNo ratings yet

- People Vs BalotolDocument2 pagesPeople Vs BalotolJules VosotrosNo ratings yet

- Pro Line Sports Center Vs CADocument2 pagesPro Line Sports Center Vs CAJulius ManaloNo ratings yet

- When There Was No Agreement Between The Parties Regarding Essential Terms of The Agreement - No Consensus Ad-Idem As Such No Valid Contract To Be Enforced 1990 SCDocument12 pagesWhen There Was No Agreement Between The Parties Regarding Essential Terms of The Agreement - No Consensus Ad-Idem As Such No Valid Contract To Be Enforced 1990 SCSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್No ratings yet

- Role of International Society in Political ObligatioDocument6 pagesRole of International Society in Political ObligatioVibhutiNo ratings yet

- Points of Land Law - 5Document6 pagesPoints of Land Law - 5Vyankatesh GotalkarNo ratings yet

- Criminal Law: Answers To Bar Examination Questions INDocument169 pagesCriminal Law: Answers To Bar Examination Questions INPam Otic-ReyesNo ratings yet

- Macariola vs. Ascunsion, Adm. Case No. 133-J May 31, 1982Document16 pagesMacariola vs. Ascunsion, Adm. Case No. 133-J May 31, 1982Tin SagmonNo ratings yet

- PSIR Test 9 CASTE, RELIGION ANDDocument11 pagesPSIR Test 9 CASTE, RELIGION ANDtjravi26No ratings yet

- Gashumba V NkudiyeDocument7 pagesGashumba V NkudiyeAshraf KiswiririNo ratings yet

- City of Naga vs. Hon. Elvi John S. AsuncionDocument2 pagesCity of Naga vs. Hon. Elvi John S. AsuncionJillian Asdala100% (1)

- Pondicherry Pawnbrokers Act 1966Document30 pagesPondicherry Pawnbrokers Act 1966Latest Laws TeamNo ratings yet

- United States v. Goldhammer, 4th Cir. (2005)Document2 pagesUnited States v. Goldhammer, 4th Cir. (2005)Scribd Government DocsNo ratings yet

- Georgia Evidence Quick Reference Guide 1707358659Document4 pagesGeorgia Evidence Quick Reference Guide 1707358659kirakimneyNo ratings yet