Download as docx, pdf, or txt

You might also like

- TM 9-1005-347-10 Machine Gun, Caliber .50, M2a1 April 2011Document160 pagesTM 9-1005-347-10 Machine Gun, Caliber .50, M2a1 April 2011GLOCK3588% (8)

- Economics Edexcel A Level: Diagram Practice BookDocument9 pagesEconomics Edexcel A Level: Diagram Practice BookMd Safwat0% (1)

- ZAHAV: A World of Israeli Cooking by Michael Solomonov and Steven CookDocument7 pagesZAHAV: A World of Israeli Cooking by Michael Solomonov and Steven CookHoughton Mifflin Harcourt Cookbooks40% (5)

- Al-Ghazali: The Alchemy of HappinessDocument4 pagesAl-Ghazali: The Alchemy of HappinessZeeshan AhmedNo ratings yet

- Case Digests For FinalsDocument40 pagesCase Digests For FinalsJayson YuzonNo ratings yet

- Economics 1A Unit 2 NotesDocument13 pagesEconomics 1A Unit 2 NotesUrish PreethlallNo ratings yet

- Chp1 Eco1001Document78 pagesChp1 Eco1001Anathi Magwaza100% (1)

- Production Possibility Curve (PPC)Document10 pagesProduction Possibility Curve (PPC)Saanvi LambaNo ratings yet

- Production Possibilities Curve (PPC)Document13 pagesProduction Possibilities Curve (PPC)Dhawal GuptaNo ratings yet

- Effect On PPC Due To Various Government PoliciesDocument3 pagesEffect On PPC Due To Various Government PoliciesGayabux Singh100% (1)

- Adobe Scan 07 Nov 2021Document3 pagesAdobe Scan 07 Nov 2021Gayabux SinghNo ratings yet

- WWW Investopedia Com Terms P Productionpossibilityfrontier ASPDocument14 pagesWWW Investopedia Com Terms P Productionpossibilityfrontier ASPᏗᏕᎥᎷ ᏗᏝᎥNo ratings yet

- Production-Possibility FrontierDocument7 pagesProduction-Possibility FrontierNaveen MettaNo ratings yet

- EconModels PPC&CFOIDocument31 pagesEconModels PPC&CFOITodd FedanNo ratings yet

- IGCSE Economics 1.4 Production Possibility CurvesDocument4 pagesIGCSE Economics 1.4 Production Possibility Curvesyeweiwei0925No ratings yet

- Class 9Document17 pagesClass 9dattananddineeNo ratings yet

- Production Possibilities CurveDocument4 pagesProduction Possibilities CurveHayley JackNo ratings yet

- Production Possibility Frontier Cheat Sheet: by ViaDocument1 pageProduction Possibility Frontier Cheat Sheet: by ViaAnaze_hNo ratings yet

- IG Eco Chapter 4 Production Possibility CurvesDocument11 pagesIG Eco Chapter 4 Production Possibility CurvesHasanNo ratings yet

- Chapter 1: Answers To Questions For ReviewDocument3 pagesChapter 1: Answers To Questions For ReviewlilyNo ratings yet

- IntroductionToMacroeconomics L1&L2Document12 pagesIntroductionToMacroeconomics L1&L2Jai KishoreNo ratings yet

- Economics PPF and ScarcityDocument25 pagesEconomics PPF and Scarcityash_khaanNo ratings yet

- UntitledDocument3 pagesUntitledImranNo ratings yet

- General Competitive Equilibrium: Slides by Pamela L. Hall Western Washington UniversityDocument60 pagesGeneral Competitive Equilibrium: Slides by Pamela L. Hall Western Washington UniversityTeed DwilightNo ratings yet

- The Production Possibility FrontierDocument14 pagesThe Production Possibility FrontierPrashantNo ratings yet

- PPC 讲义Document25 pagesPPC 讲义s-zhangyuchengNo ratings yet

- A Production Possibility FrontierDocument3 pagesA Production Possibility FrontiervikashknNo ratings yet

- Production Possibilities Curve NotesDocument5 pagesProduction Possibilities Curve NotesLeonardo A. Salas100% (1)

- PA 103: Introduction To Microeconomics: Md. Roni Hossain Lecturer Department of Economics Jahangirnagar UniversityDocument33 pagesPA 103: Introduction To Microeconomics: Md. Roni Hossain Lecturer Department of Economics Jahangirnagar Universitymd jowel khanNo ratings yet

- EFE-PPC NotesDocument2 pagesEFE-PPC Notesgursimark.sodhiNo ratings yet

- End of Semester Exams Section BDocument5 pagesEnd of Semester Exams Section BBhoi ChampionNo ratings yet

- Chapter 1 BASIC ECONOMIC CONCEPTDocument19 pagesChapter 1 BASIC ECONOMIC CONCEPTMuhammad FirdausNo ratings yet

- RIngkasan Teori Perdagangan InternasionalDocument5 pagesRIngkasan Teori Perdagangan Internasionall a t h i f a hNo ratings yet

- Chapter # 2: Goods/resourcesDocument3 pagesChapter # 2: Goods/resourcesSyed Noman ShamimNo ratings yet

- Production-Possibility FrontierDocument8 pagesProduction-Possibility FrontierSushmita RamaNo ratings yet

- Lecture 3Document61 pagesLecture 3Nikoli MajorNo ratings yet

- Topic (1) - IntroductionDocument12 pagesTopic (1) - IntroductionWEI SZI LIMNo ratings yet

- AS Eco Chapter 3Document9 pagesAS Eco Chapter 3Noreen Al-MansurNo ratings yet

- (SN) II Principles of MicroeconomicsDocument108 pages(SN) II Principles of MicroeconomicsNarmeen RefaiNo ratings yet

- Production & PricingDocument24 pagesProduction & Pricingpranjal farhanNo ratings yet

- ECO+201+ +Final+Review+FA+2023Document100 pagesECO+201+ +Final+Review+FA+2023n4ctvpjvj7No ratings yet

- Chapter 2 PPC and Economic GrowthDocument16 pagesChapter 2 PPC and Economic GrowthnajlaaNo ratings yet

- AL Economics Notes (Ver 3) by A Karim LakhaniDocument33 pagesAL Economics Notes (Ver 3) by A Karim LakhaniAfnan Tariq100% (1)

- Chapter 1Document23 pagesChapter 1abdullahkhanazeemNo ratings yet

- Ee For Students-1Document301 pagesEe For Students-1Manoj Kumar SNo ratings yet

- PPC ProjectDocument11 pagesPPC ProjectKuber PatidarNo ratings yet

- PPFDocument10 pagesPPFadilnewaz75No ratings yet

- Asm Economics 190101Document30 pagesAsm Economics 190101AnandiniNo ratings yet

- Page 1Document1 pagePage 1Sun NyNo ratings yet

- B) Production Possibility Frontiers (PPFS)Document5 pagesB) Production Possibility Frontiers (PPFS)jaysambakerNo ratings yet

- E) Production Possibility CurvesDocument5 pagesE) Production Possibility CurveskaveriNo ratings yet

- Igcse Economics DiagramsDocument30 pagesIgcse Economics DiagramsVÕ PHANNo ratings yet

- Dwnload Full Economics 11th Edition Michael Parkin Solutions Manual PDFDocument36 pagesDwnload Full Economics 11th Edition Michael Parkin Solutions Manual PDFaminamuckenfuss804uk100% (17)

- Full Download Economics 11th Edition Michael Parkin Solutions ManualDocument36 pagesFull Download Economics 11th Edition Michael Parkin Solutions Manualpaimanmaidsi100% (39)

- Week 5 Lecture Comparative Advantage and Market ForcesDocument5 pagesWeek 5 Lecture Comparative Advantage and Market Forcescbenn0001No ratings yet

- ECO Reviewer 2-3Document6 pagesECO Reviewer 2-3Gwen Ashley Dela PenaNo ratings yet

- Economics Unit 1.4 Revision Notes by MSUDocument3 pagesEconomics Unit 1.4 Revision Notes by MSUMsuBrainBoxNo ratings yet

- International Economics Week4 The Specific Factors Model - With AnswersDocument60 pagesInternational Economics Week4 The Specific Factors Model - With AnswersPeleoneNo ratings yet

- PPF PPT GclassroomDocument21 pagesPPF PPT GclassroomKrishita ThakralNo ratings yet

- 1chapter 1 - Introduction To EconomicsDocument38 pages1chapter 1 - Introduction To EconomicsJen CaremNo ratings yet

- Microeconomics 11th Edition Michael Parkin Solutions ManualDocument35 pagesMicroeconomics 11th Edition Michael Parkin Solutions Manualorangeventradee87j100% (30)

- Macroeconomics Canada in The Global Environment Canadian 9th Edition Parkin Solutions ManualDocument5 pagesMacroeconomics Canada in The Global Environment Canadian 9th Edition Parkin Solutions ManualHollyCamposjfynd100% (46)

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Economics 1 A Notes - Unit 4Document11 pagesEconomics 1 A Notes - Unit 4Kathryn ParadisosNo ratings yet

- Economics 1 A Unit 3 Notes Definition of A MarketDocument5 pagesEconomics 1 A Unit 3 Notes Definition of A MarketKathryn ParadisosNo ratings yet

- PPC Curve and NotesDocument1 pagePPC Curve and NotesKathryn ParadisosNo ratings yet

- Examples of Test QuestionsDocument6 pagesExamples of Test QuestionsKathryn ParadisosNo ratings yet

- RatiosDocument13 pagesRatiosKathryn ParadisosNo ratings yet

- Master Fiancial Statements SP Act 1Document13 pagesMaster Fiancial Statements SP Act 1Kathryn ParadisosNo ratings yet

- CalculationsDocument37 pagesCalculationsKathryn ParadisosNo ratings yet

- Financial Statements For Sole Partnership - KatDocument12 pagesFinancial Statements For Sole Partnership - KatKathryn ParadisosNo ratings yet

- Vlook UpDocument2 pagesVlook UpKathryn ParadisosNo ratings yet

- Circular Progress Chart GraphDocument2 pagesCircular Progress Chart GraphKathryn ParadisosNo ratings yet

- Harvard Style of Referencing NewDocument4 pagesHarvard Style of Referencing NewKathryn ParadisosNo ratings yet

- Banking SWOT Analysis v2Document29 pagesBanking SWOT Analysis v2Chiraroj AngsumaleeNo ratings yet

- MDU Fiber WhitePaperDocument6 pagesMDU Fiber WhitePaperbuicongluyenNo ratings yet

- The Silk Road: ¿What Is It?Document2 pagesThe Silk Road: ¿What Is It?Harold Stiven HERNANDEZ RAYONo ratings yet

- Voucher Tur DubaiDocument2 pagesVoucher Tur Dubaimaria caragopNo ratings yet

- Private International LawDocument16 pagesPrivate International LawMelvin PernezNo ratings yet

- Cadenas Drives USA PDFDocument238 pagesCadenas Drives USA PDFCamilo Araya ArayaNo ratings yet

- Edtpa Lesson PlanDocument4 pagesEdtpa Lesson Planapi-280516383No ratings yet

- Efficient Market HypothesisDocument2 pagesEfficient Market HypothesisSAMEEKSHA SUDHINDRA HOSKOTE 2133361No ratings yet

- Concrete Quality Control PlanDocument5 pagesConcrete Quality Control PlanKripasindhu SamantaNo ratings yet

- Effectiveness of School Heads FinancialDocument9 pagesEffectiveness of School Heads FinancialRonald AlmagroNo ratings yet

- International Ticket SEAYLP 2017Document3 pagesInternational Ticket SEAYLP 2017AngelNo ratings yet

- Adani Under Attack: Q&A With Finance Minister ON BUDGET 2023-24Document104 pagesAdani Under Attack: Q&A With Finance Minister ON BUDGET 2023-24Jorge Antonio PichardoNo ratings yet

- YCMOU Study Center Submission Slip: Application No: Distance EducationDocument4 pagesYCMOU Study Center Submission Slip: Application No: Distance Educationvaibhavpardeshi55No ratings yet

- 2010 CLC 350Document5 pages2010 CLC 350Asif NawazNo ratings yet

- Link Reit Part 2 PDFDocument97 pagesLink Reit Part 2 PDFDnukumNo ratings yet

- Inglés Ix: Dra. Mercy Noelia Páliza ChampiDocument30 pagesInglés Ix: Dra. Mercy Noelia Páliza ChampiEdwin Christian Laurente HuertasNo ratings yet

- Summary (Nido)Document3 pagesSummary (Nido)G21. Villanueva, Camille T.No ratings yet

- bsp2018 PDFDocument97 pagesbsp2018 PDFLyn RNo ratings yet

- BG Construction POW.R1V6Document13 pagesBG Construction POW.R1V6Deepum HalloomanNo ratings yet

- Ancestors: Optional Rules For Legend of The 5 Rings Third EditionDocument5 pagesAncestors: Optional Rules For Legend of The 5 Rings Third EditionGerrit DeikeNo ratings yet

- Airport Markings Flash CardsDocument12 pagesAirport Markings Flash CardsrohokaNo ratings yet

- Survey Questionnaire For PSU CPAs Synthesis 1Document2 pagesSurvey Questionnaire For PSU CPAs Synthesis 1hilarytevesNo ratings yet

- 1 5407Document37 pages1 5407Norman ScheelNo ratings yet

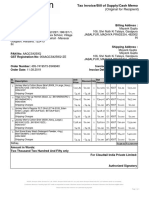

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document2 pagesTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)MAYANK GUPTANo ratings yet

- Focus Group Discussion Questionnaire (24.01.2022)Document4 pagesFocus Group Discussion Questionnaire (24.01.2022)Mohammed EcoNo ratings yet

- Indian Bank - Education Loan Application FormDocument2 pagesIndian Bank - Education Loan Application Formabhishek100% (4)