Download as pdf or txt

You might also like

- Juan Negosyante Blank Worksheets by Chinkee TanDocument9 pagesJuan Negosyante Blank Worksheets by Chinkee TanAbby Balendo100% (4)

- Assessing Survival Strategies For Agro-Dealers in Chipata and Petauke Districts, Eastern ZambiaDocument6 pagesAssessing Survival Strategies For Agro-Dealers in Chipata and Petauke Districts, Eastern ZambiaThe IjbmtNo ratings yet

- Problems: Operations ManagementDocument2 pagesProblems: Operations ManagementHammad Ishfaq0% (1)

- 2V0-21.19 - Professional VMware Vsphere 6.7Document2 pages2V0-21.19 - Professional VMware Vsphere 6.7Carlos Alan Pulido I.100% (1)

- Forecasting Demand For Petroleum Products in Ghana Using Time Series ModelsDocument14 pagesForecasting Demand For Petroleum Products in Ghana Using Time Series Modelsraj1508No ratings yet

- Using Non-Linear Garch Model To Predict Silicon Content in Blast Furnace Hot MetalDocument6 pagesUsing Non-Linear Garch Model To Predict Silicon Content in Blast Furnace Hot MetalFrustrated engineerNo ratings yet

- Using ARIMA-GARCH Model To Analyze Fluctuation Law of Price OilDocument7 pagesUsing ARIMA-GARCH Model To Analyze Fluctuation Law of Price OilMatias VargasNo ratings yet

- 预测铜价格通过应用强大的人工智能技术Document11 pages预测铜价格通过应用强大的人工智能技术赵一霏No ratings yet

- 提出两种预测铜的新型混合智能模型价格基于极限学习机和元启发式算法Document12 pages提出两种预测铜的新型混合智能模型价格基于极限学习机和元启发式算法赵一霏No ratings yet

- Modeling High-Temperature Mechanical Properties of Austenitic Stainlesssteels by Neural NetworksDocument12 pagesModeling High-Temperature Mechanical Properties of Austenitic Stainlesssteels by Neural NetworkssayesteNo ratings yet

- Chen - 2018 - IOP - Conf. - Ser. - Mater. - Sci. - Eng. - 394 - 052024Document8 pagesChen - 2018 - IOP - Conf. - Ser. - Mater. - Sci. - Eng. - 394 - 052024Najiyah SalehNo ratings yet

- Non-Ferrous Metal Price Point and Interval Prediction Based On Variational Mode Decomposition and Optimized LSTM NetworkDocument16 pagesNon-Ferrous Metal Price Point and Interval Prediction Based On Variational Mode Decomposition and Optimized LSTM Network赵一霏No ratings yet

- Timeseries ModifiedDocument12 pagesTimeseries ModifiedsikandarshahNo ratings yet

- Article 4. 41Document14 pagesArticle 4. 41ricardoloureirosoareNo ratings yet

- ID Perbandingan Model Archgarch Model ArimaDocument8 pagesID Perbandingan Model Archgarch Model ArimaauraNo ratings yet

- STAT758: Final ProjectDocument19 pagesSTAT758: Final ProjectYeswanthNo ratings yet

- Zhou - 2021 - J. - Phys. - Conf. - Ser. - 1941 - 012064Document7 pagesZhou - 2021 - J. - Phys. - Conf. - Ser. - 1941 - 012064Cheryl AdaraNo ratings yet

- Prediction of Silicon Content of Alloy in Ferrochrome Smelting Using Data-Driven ModelsDocument8 pagesPrediction of Silicon Content of Alloy in Ferrochrome Smelting Using Data-Driven Modelscesar8319No ratings yet

- PagoluSreenivasaRao HariSankarVanka 48 PDFDocument8 pagesPagoluSreenivasaRao HariSankarVanka 48 PDFRavinder ReddyNo ratings yet

- Application of Operations Research in Steel IndustryDocument7 pagesApplication of Operations Research in Steel IndustryInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- J Measurement 2020 108465Document9 pagesJ Measurement 2020 108465Raheel AdeelNo ratings yet

- Artigo - An Optimization Procedure For Overhead Gantry Crane Exposed To Buckling and Yield Criteria - IRA v.8 I.2 2017 - Ali Ahmid Et Al PDFDocument11 pagesArtigo - An Optimization Procedure For Overhead Gantry Crane Exposed To Buckling and Yield Criteria - IRA v.8 I.2 2017 - Ali Ahmid Et Al PDFKaique CavalcanteNo ratings yet

- Aggarwal 2009Document10 pagesAggarwal 2009Yusuf Ali DanışNo ratings yet

- Parameter Condition of Being Optimized For MIG Welding of Austenitic Stainless Steel & Low Carbon Steel Using Taguchi MethodDocument3 pagesParameter Condition of Being Optimized For MIG Welding of Austenitic Stainless Steel & Low Carbon Steel Using Taguchi MethodIjrtsNo ratings yet

- Forming Limit Diagram Generation of Aluminum Alloy AA2014Document8 pagesForming Limit Diagram Generation of Aluminum Alloy AA2014Andrés MaiguaNo ratings yet

- Weldability Studies and Parameter Optimization of AISI 904L Super Austenitic Stainless Steel Using Friction WeldingDocument18 pagesWeldability Studies and Parameter Optimization of AISI 904L Super Austenitic Stainless Steel Using Friction Weldinggabesh3192No ratings yet

- Punch Strech TestDocument11 pagesPunch Strech Testschool boyvsNo ratings yet

- Steel Structural Design Using Nonlinear Inelastic Analysis: Viet-Hung Truong and Seung-Eock KimDocument9 pagesSteel Structural Design Using Nonlinear Inelastic Analysis: Viet-Hung Truong and Seung-Eock KimIgnacio TabuadaNo ratings yet

- Material Variability Effects On Automotive Part Production ProcessDocument9 pagesMaterial Variability Effects On Automotive Part Production Processkenthbrian.ayingNo ratings yet

- Advances in Modelling and Analysis C: Received: 16 November 2018 Accepted: 22 February 2019Document5 pagesAdvances in Modelling and Analysis C: Received: 16 November 2018 Accepted: 22 February 2019prashanth palaniNo ratings yet

- Comparative Analysis and Design of Box Girder Bridge Sub-Structure With Two DiDocument6 pagesComparative Analysis and Design of Box Girder Bridge Sub-Structure With Two DiNelly BuquironNo ratings yet

- Modeling of The MIG Welding Process Using Statistical ApproachesDocument25 pagesModeling of The MIG Welding Process Using Statistical ApproachesBarnik Saha RoyNo ratings yet

- Analysis of Piston, Connecting Rod and Crank Shaft Assembly: SciencedirectDocument10 pagesAnalysis of Piston, Connecting Rod and Crank Shaft Assembly: Sciencedirectvikek vikumarNo ratings yet

- High Efficient Welding Technology of The Car BodiesDocument8 pagesHigh Efficient Welding Technology of The Car BodiessarikaNo ratings yet

- 1 Analysis of Cold Rolling Process With Different ParametersDocument9 pages1 Analysis of Cold Rolling Process With Different Parametersomid hamidishadNo ratings yet

- Optimization of Micro-Electrical Discharge Machining Parameters of Ti6AL4V Component: A Mapping StudyDocument14 pagesOptimization of Micro-Electrical Discharge Machining Parameters of Ti6AL4V Component: A Mapping StudyNguyễn Hữu PhấnNo ratings yet

- Study On The Correlation of Toughness With ChemicaDocument7 pagesStudy On The Correlation of Toughness With ChemicaarvindNo ratings yet

- Optimization of Mig Welding Parameters On Tensile Strength of Aluminum Alloy by Taguchi ApproachDocument7 pagesOptimization of Mig Welding Parameters On Tensile Strength of Aluminum Alloy by Taguchi ApproachAdarsh KumarNo ratings yet

- Performance of Predictive Models To Determine Weld Bead Shape - 2022 - Marine STDocument13 pagesPerformance of Predictive Models To Determine Weld Bead Shape - 2022 - Marine STAditya KumarNo ratings yet

- Chen 2018 IOP Conf. Ser. Mater. Sci. Eng. 394 052024Document8 pagesChen 2018 IOP Conf. Ser. Mater. Sci. Eng. 394 052024marlonekeilaNo ratings yet

- Emfrm+2022 3104 3111Document8 pagesEmfrm+2022 3104 3111aidynn.enocNo ratings yet

- Ijret20130213011 PDFDocument8 pagesIjret20130213011 PDFAakash KamthaneNo ratings yet

- ANALYSIS of DAILY STOCK TREND Prediction by Usning Time SeriesDocument21 pagesANALYSIS of DAILY STOCK TREND Prediction by Usning Time SeriesGazi Mohammad JamilNo ratings yet

- Optimisation of Wireedm Parameters For H11 Tool Steel Using CorrelationDocument8 pagesOptimisation of Wireedm Parameters For H11 Tool Steel Using CorrelationEditor IJRITCCNo ratings yet

- 01.predicting SET50 Stock Prices Using CARIMADocument4 pages01.predicting SET50 Stock Prices Using CARIMAkamran raiysatNo ratings yet

- Time Series Analysis and Forecasting of Gold Price Using ARIMA and LSTM ModelDocument8 pagesTime Series Analysis and Forecasting of Gold Price Using ARIMA and LSTM ModelIJRASETPublicationsNo ratings yet

- The Prediction of Gold Price Using ARIMA Model: Abstract-Although, 2016 and 2017 Have Risen, The InternationalDocument4 pagesThe Prediction of Gold Price Using ARIMA Model: Abstract-Although, 2016 and 2017 Have Risen, The InternationalpydyNo ratings yet

- Comparison of Multiple Regression and Radial Basis PDFDocument8 pagesComparison of Multiple Regression and Radial Basis PDFM. Sadiq. A. PachapuriNo ratings yet

- A Deformation Theory of PlasticityDocument14 pagesA Deformation Theory of PlasticityRohit KoreNo ratings yet

- 1 s2.0 S2238785418301467 MainDocument22 pages1 s2.0 S2238785418301467 MainBharat VinjamuriNo ratings yet

- J H: A E M C S F M: Umping Edges N Xamination of Ovements in Opper Pot and Utures ArketsDocument21 pagesJ H: A E M C S F M: Umping Edges N Xamination of Ovements in Opper Pot and Utures ArketsKumaran SanthoshNo ratings yet

- Experimental Study of Tribological Behavior of Casted Aluminium-BronzeDocument10 pagesExperimental Study of Tribological Behavior of Casted Aluminium-BronzeLULZNo ratings yet

- Goswami 2020Document5 pagesGoswami 2020Najiyah SalehNo ratings yet

- 1 s2.0 S1568494616305348 MainDocument7 pages1 s2.0 S1568494616305348 MainSiva GuruNo ratings yet

- Equipment Fault Forecasting Based On ARMA ModelDocument5 pagesEquipment Fault Forecasting Based On ARMA ModelClaudio RobertoNo ratings yet

- Materials Selection For Hot Stamped Automotive Body Parts: An Application of The Ashby Approach Based On The Strain Hardening Exponent and Stacking Fault Energy of MaterialsDocument10 pagesMaterials Selection For Hot Stamped Automotive Body Parts: An Application of The Ashby Approach Based On The Strain Hardening Exponent and Stacking Fault Energy of MaterialsJaka Haris MustafaNo ratings yet

- Metals: Numerical Prediction of Forming Car Body Parts With Emphasis On SpringbackDocument15 pagesMetals: Numerical Prediction of Forming Car Body Parts With Emphasis On SpringbackKrishna VamsiNo ratings yet

- Arima-Garch Models in Estimating Market Risk Using Value at Risk For The Wig20 IndexDocument9 pagesArima-Garch Models in Estimating Market Risk Using Value at Risk For The Wig20 IndexFernando HillNo ratings yet

- Energies 05 00355Document16 pagesEnergies 05 00355notat80726No ratings yet

- Optimization of wire-EDM Process of Titanium Alloy-Grade 5 Using Taguchi's Method and Grey Relational AnalysisDocument10 pagesOptimization of wire-EDM Process of Titanium Alloy-Grade 5 Using Taguchi's Method and Grey Relational Analysismustafa sertNo ratings yet

- Reference Values For Railway Sidings Track Geometry: SciencedirectDocument10 pagesReference Values For Railway Sidings Track Geometry: Sciencedirectjavier sotoNo ratings yet

- Simulation and Experimental Studies On Arc Efficiency and Mechanical Characterization For GTA-Welded Ti-6Al-4V SheetsDocument12 pagesSimulation and Experimental Studies On Arc Efficiency and Mechanical Characterization For GTA-Welded Ti-6Al-4V SheetsdvktrichyNo ratings yet

- Handbook of Optimization in the Railway IndustryFrom EverandHandbook of Optimization in the Railway IndustryRalf BorndörferNo ratings yet

- Influence of Devolved Dispute Resolution Mechanisms On Job Satisfaction of Health Care Workers in Nakuru County KenyaDocument13 pagesInfluence of Devolved Dispute Resolution Mechanisms On Job Satisfaction of Health Care Workers in Nakuru County KenyaThe IjbmtNo ratings yet

- Constructing Brand Personality From The TripAdvisor Online ReviewsDocument6 pagesConstructing Brand Personality From The TripAdvisor Online ReviewsThe IjbmtNo ratings yet

- The Resort Brand Personality A Study On Long Term Period Online Reviews 2008 - 2020Document6 pagesThe Resort Brand Personality A Study On Long Term Period Online Reviews 2008 - 2020The IjbmtNo ratings yet

- Evaluation For E-Commerce Using AHP: Designing The ExperimentDocument11 pagesEvaluation For E-Commerce Using AHP: Designing The ExperimentThe IjbmtNo ratings yet

- Internal Control and Corporate Governance Among CooperativesDocument14 pagesInternal Control and Corporate Governance Among CooperativesThe IjbmtNo ratings yet

- Trip Advisor Resort Online Reviews in Bali. Content Analysis Based On Big DataDocument8 pagesTrip Advisor Resort Online Reviews in Bali. Content Analysis Based On Big DataThe IjbmtNo ratings yet

- Resiliency of Microenterprises Amidst Pandemic in Davao Del Sur PhilippinesDocument18 pagesResiliency of Microenterprises Amidst Pandemic in Davao Del Sur PhilippinesThe IjbmtNo ratings yet

- Effect of Market Penetration Strategy On Financial Performance of Tobacco Manufacturing Firms in KenyaDocument10 pagesEffect of Market Penetration Strategy On Financial Performance of Tobacco Manufacturing Firms in KenyaThe IjbmtNo ratings yet

- Effect of Enterprise Risk Management Strategyon Financial Performance of Listed Banks at Nigeria Stock ExchangeDocument11 pagesEffect of Enterprise Risk Management Strategyon Financial Performance of Listed Banks at Nigeria Stock ExchangeThe IjbmtNo ratings yet

- Carbon Accounting Information Disclosure Under The Background of Green DevelopmentDocument7 pagesCarbon Accounting Information Disclosure Under The Background of Green DevelopmentThe IjbmtNo ratings yet

- High Performance Work Practices, Entrepreneurial Orientation and Organisation Excellence in Nigerian HEIs: A Correlational AnalysisDocument12 pagesHigh Performance Work Practices, Entrepreneurial Orientation and Organisation Excellence in Nigerian HEIs: A Correlational AnalysisThe IjbmtNo ratings yet

- Influence of Customer Orientation On The Growth of Manufacturing Firms in Nakuru East and West Sub-Counties KenyaDocument10 pagesInfluence of Customer Orientation On The Growth of Manufacturing Firms in Nakuru East and West Sub-Counties KenyaThe IjbmtNo ratings yet

- Topic:Nexus Between Public Sector Employees and Effectiveness of Trade UnionismDocument8 pagesTopic:Nexus Between Public Sector Employees and Effectiveness of Trade UnionismThe IjbmtNo ratings yet

- Intention and Behavior Towards Bringing Your Own Shopping Bags in Vietnam: An Investigation Using The Theory of Planned BehaviorDocument8 pagesIntention and Behavior Towards Bringing Your Own Shopping Bags in Vietnam: An Investigation Using The Theory of Planned BehaviorThe IjbmtNo ratings yet

- Factors Affecting Employees' Innovative Behavior in Enterprises: The Case of VietnamDocument6 pagesFactors Affecting Employees' Innovative Behavior in Enterprises: The Case of VietnamThe IjbmtNo ratings yet

- Does Human Capital Predict Resources: Evidence From Denominational Institutions in GhanaDocument9 pagesDoes Human Capital Predict Resources: Evidence From Denominational Institutions in GhanaThe IjbmtNo ratings yet

- The Influence of Youtube Advertising Value On Brand Awareness and Purchase Intentions of Vietnamese CustomersDocument9 pagesThe Influence of Youtube Advertising Value On Brand Awareness and Purchase Intentions of Vietnamese CustomersThe IjbmtNo ratings yet

- Strategic Literature Review On Contingency Factors and Bank Performance in ChinaDocument10 pagesStrategic Literature Review On Contingency Factors and Bank Performance in ChinaThe IjbmtNo ratings yet

- Entrepreneurial Intention of The Cotabato City State Polytechnic College (CCSPC) - Bachelor of Science in Business Administration (BSBA) GraduatesDocument10 pagesEntrepreneurial Intention of The Cotabato City State Polytechnic College (CCSPC) - Bachelor of Science in Business Administration (BSBA) GraduatesThe IjbmtNo ratings yet

- Knowledge Mapping of Platform Competition: Literature Review and Research AgendaDocument7 pagesKnowledge Mapping of Platform Competition: Literature Review and Research AgendaThe IjbmtNo ratings yet

- Policy Framework For Cyber Security Concernsand Performance of Small and Medium Enterprises For Global Economic Recovery Amidst Covid-19Document9 pagesPolicy Framework For Cyber Security Concernsand Performance of Small and Medium Enterprises For Global Economic Recovery Amidst Covid-19The IjbmtNo ratings yet

- Effect of Net Profit Margin, Debt To Equity Ratio, Current Ratio and Inflation On Dividend Payout RatioDocument10 pagesEffect of Net Profit Margin, Debt To Equity Ratio, Current Ratio and Inflation On Dividend Payout RatioThe IjbmtNo ratings yet

- Management Innovation and Business Performance of Micro, Small, and Medium Enterprises in Cotabato City During The COVID-19 PandemicDocument9 pagesManagement Innovation and Business Performance of Micro, Small, and Medium Enterprises in Cotabato City During The COVID-19 PandemicThe IjbmtNo ratings yet

- The Determinants of The Sustainability of Microfinance Institutions Through The Control Systems: Case of Cameroon in Context Covid19Document13 pagesThe Determinants of The Sustainability of Microfinance Institutions Through The Control Systems: Case of Cameroon in Context Covid19The IjbmtNo ratings yet

- Assessment of Turkey's Innovation Performance During The European Union Candidacy PeriodDocument17 pagesAssessment of Turkey's Innovation Performance During The European Union Candidacy PeriodThe IjbmtNo ratings yet

- Transformational Leadership and Corporate Entrepreneur The Proposed Strategy To Enhance Ahmad Dahlan University's Business Sustainability: A Literature ReviewDocument4 pagesTransformational Leadership and Corporate Entrepreneur The Proposed Strategy To Enhance Ahmad Dahlan University's Business Sustainability: A Literature ReviewThe IjbmtNo ratings yet

- Influence of Capacity Building in The Management Reform On Service Delivery at Nakuru Water and Sanitation Services Company (NAWASSCO)Document6 pagesInfluence of Capacity Building in The Management Reform On Service Delivery at Nakuru Water and Sanitation Services Company (NAWASSCO)The IjbmtNo ratings yet

- Developing Product Brand Value in Response To Customer Satisfaction Participation in Building and Customer. Experience ManagementDocument6 pagesDeveloping Product Brand Value in Response To Customer Satisfaction Participation in Building and Customer. Experience ManagementThe IjbmtNo ratings yet

- Influence of Job Enrichment On Performance of Academic Staff in Public Universities in KenyaDocument8 pagesInfluence of Job Enrichment On Performance of Academic Staff in Public Universities in KenyaThe IjbmtNo ratings yet

- July 2020 BBF20103 Introduction To Financial Management Assignment 2Document5 pagesJuly 2020 BBF20103 Introduction To Financial Management Assignment 2Muhamad SaifulNo ratings yet

- Solution Manual For Elementary Statistics 9th Edition by Weiss ISBN 0321989392 9780321989390Document36 pagesSolution Manual For Elementary Statistics 9th Edition by Weiss ISBN 0321989392 9780321989390carriescottmbtxnrjfwq100% (24)

- Unit 4Document30 pagesUnit 4AakanshasoniNo ratings yet

- BA+VERSA+Kolben en 102619 2011 05 Rev.ADocument18 pagesBA+VERSA+Kolben en 102619 2011 05 Rev.APappa Mihai RazvanNo ratings yet

- Union of India Vs Solar PesticidesDocument6 pagesUnion of India Vs Solar PesticidesRanvidsNo ratings yet

- Hazel Case StudyDocument17 pagesHazel Case StudyPyae PyaeNo ratings yet

- Motorcycle To Car Ownership The Role of Road Mobility Accessibility and Income InequalityDocument8 pagesMotorcycle To Car Ownership The Role of Road Mobility Accessibility and Income Inequalitymèo blinksNo ratings yet

- Actual HDD 1 ProfileDocument12 pagesActual HDD 1 Profiletang weng wai100% (1)

- Balanced Scorecard Project Templates Menu: Prepared By: Matt H. Evans, CPA, CMA, CFM Date Prepared: April 21, 2001Document41 pagesBalanced Scorecard Project Templates Menu: Prepared By: Matt H. Evans, CPA, CMA, CFM Date Prepared: April 21, 2001aftab_sweet3024No ratings yet

- Ii Bba Production and Materials Management - 416BDocument21 pagesIi Bba Production and Materials Management - 416BponnasaikumarNo ratings yet

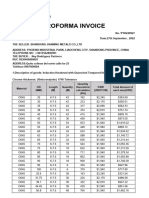

- Update Proforma Invoice YYH220927Document3 pagesUpdate Proforma Invoice YYH220927jesus RodriguezNo ratings yet

- HR Exam Question and Answer Paper For Competitive Exam - Exam ForumDocument5 pagesHR Exam Question and Answer Paper For Competitive Exam - Exam Forumdevarshi_shukla100% (2)

- Sifat Finishing Lantai BambuDocument9 pagesSifat Finishing Lantai BambuFroscka WayNo ratings yet

- Invoice No 20 October 2023Document14 pagesInvoice No 20 October 2023Hiruy GulilatNo ratings yet

- Printed by SYSUSER: A/C No: 7124960000Document1 pagePrinted by SYSUSER: A/C No: 7124960000Mukharram KhanNo ratings yet

- Fitwell IMP Gye Catalouge 2023Document91 pagesFitwell IMP Gye Catalouge 2023Jeremy Courtois RenthleiNo ratings yet

- PRB M3Document4 pagesPRB M3John Alejandro Rangel RetaviscaNo ratings yet

- Roof Deck SpecificationsDocument2 pagesRoof Deck SpecificationsVictor IkeNo ratings yet

- A04 - EcoDev TheoriesofEcoGrowth&DevDocument2 pagesA04 - EcoDev TheoriesofEcoGrowth&DevcamillaNo ratings yet

- Decision Theory Comparison of Payoff Distributions in Terms or Return and RiskDocument16 pagesDecision Theory Comparison of Payoff Distributions in Terms or Return and RiskvaisagarNo ratings yet

- So N Unit 9Document8 pagesSo N Unit 9Lam TrúcNo ratings yet

- PT Kirana - Jawaban QuizDocument2 pagesPT Kirana - Jawaban QuizJesselin VemberainNo ratings yet

- Role of Micro-Financing in Women Empowerment: An Empirical Study of Urban PunjabDocument16 pagesRole of Micro-Financing in Women Empowerment: An Empirical Study of Urban PunjabAnum ZubairNo ratings yet

- Sectional Plan, HFD, Ga Drawing of Bypass Line 1 - 1 of 5 - 11.10.2022Document1 pageSectional Plan, HFD, Ga Drawing of Bypass Line 1 - 1 of 5 - 11.10.2022Anirban MukherjeeNo ratings yet

- RRC Quotation SP Singla Majuli Ew 175Document2 pagesRRC Quotation SP Singla Majuli Ew 175Dolabari to Jamuguri 4 Lane Road ProjectNo ratings yet

- Millar v. Urban Outfitters + Hot Topic - THE PLURAL OF VINYL IS VINYL Trademark Complaint PDFDocument19 pagesMillar v. Urban Outfitters + Hot Topic - THE PLURAL OF VINYL IS VINYL Trademark Complaint PDFMark JaffeNo ratings yet

- 2390USD (EX-WORK) Includes: Optional Parts 120USD 10USD/PCS 10USD/PCS 15USD/PCSDocument6 pages2390USD (EX-WORK) Includes: Optional Parts 120USD 10USD/PCS 10USD/PCS 15USD/PCSMohamed IbrahemNo ratings yet