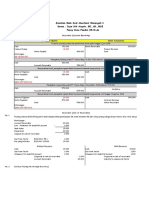

Accounting ГОТОВО

Accounting ГОТОВО

You might also like

- Accounting Terms & DefinitionsDocument6 pagesAccounting Terms & DefinitionsMir Wajid KhanNo ratings yet

- Accounting Term-WPS OfficeDocument9 pagesAccounting Term-WPS OfficeStefhanie Nicole C. GonzagaNo ratings yet

- 2 Accounting Work BookDocument89 pages2 Accounting Work Bookrachel rankuNo ratings yet

- Basics of AccountingDocument16 pagesBasics of Accountingmule mulugetaNo ratings yet

- Unit 1: Balance SheetDocument8 pagesUnit 1: Balance SheetthejeshwarNo ratings yet

- English For Accounting: Module Session 3 - Accounting Terms by Yulia Sulianti Se - Ak, M.IkomDocument3 pagesEnglish For Accounting: Module Session 3 - Accounting Terms by Yulia Sulianti Se - Ak, M.IkomWulan AyuNo ratings yet

- Accounting Equation: Ads by GoogleDocument9 pagesAccounting Equation: Ads by GoogleOliver HarmonNo ratings yet

- CH1 - Accounting in BusinessDocument18 pagesCH1 - Accounting in BusinessMaiaOshakmashviliNo ratings yet

- ACC321Document5 pagesACC321Allysa Del MundoNo ratings yet

- Chapter 10Document4 pagesChapter 10Nguyên BùiNo ratings yet

- Fabm Research ProjectDocument41 pagesFabm Research ProjectMon Kiego MagnoNo ratings yet

- Definition of AccountingDocument3 pagesDefinition of AccountingtpequitNo ratings yet

- Prepare Financial Report IbexDocument13 pagesPrepare Financial Report Ibexfentahun enyewNo ratings yet

- Accounting IntroductionDocument10 pagesAccounting Introductionomer mazharNo ratings yet

- Understand Basic Accounting TermsDocument5 pagesUnderstand Basic Accounting Termsabu taherNo ratings yet

- ACC321Document6 pagesACC321Allysa Del MundoNo ratings yet

- Accounting TermsDocument3 pagesAccounting Termsnada_nastityNo ratings yet

- Fabm 2 and FinanceDocument5 pagesFabm 2 and FinanceLenard TaberdoNo ratings yet

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae SasutilNo ratings yet

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae Sasutil100% (1)

- Chapter 1: Financialapplications Fundamentals of AccountingDocument60 pagesChapter 1: Financialapplications Fundamentals of AccountingSTEVE WAYNE100% (1)

- Accounting 1Document4 pagesAccounting 1Shoaib YousufNo ratings yet

- Receita KIWIFFDocument2 pagesReceita KIWIFFithallothallysdejesuslopesNo ratings yet

- Definition of Terms1Document3 pagesDefinition of Terms1Yusuf ÖzdemirNo ratings yet

- Equation Becomes: Assets A Liabilities L + Stockholders' Equity SEDocument2 pagesEquation Becomes: Assets A Liabilities L + Stockholders' Equity SEJorge L CastelarNo ratings yet

- AccountingDocument44 pagesAccountingPrasith baskyNo ratings yet

- Account Records Date Back To The Ancient CivilizatinsDocument6 pagesAccount Records Date Back To The Ancient Civilizatinsarimaskhassim00No ratings yet

- System of RecordDocument3 pagesSystem of RecordJonalyn MontecalvoNo ratings yet

- FABM Dictionary 1Document32 pagesFABM Dictionary 1Candy TinapayNo ratings yet

- Actg 1 Module 3Document5 pagesActg 1 Module 3Mae BertilloNo ratings yet

- Accounting AssignmentDocument2 pagesAccounting AssignmentMarvel TatingNo ratings yet

- Accounting CycleDocument4 pagesAccounting Cycleddoc.mimiNo ratings yet

- Introduction To AccountingDocument34 pagesIntroduction To AccountingBianca Mhae De LeonNo ratings yet

- What Is The Difference Between Job Costing and Process Costing?Document31 pagesWhat Is The Difference Between Job Costing and Process Costing?Muhammad AsimNo ratings yet

- FINANCIAL ACCOUNTING - AsbDocument9 pagesFINANCIAL ACCOUNTING - AsbMuskaanNo ratings yet

- Financial StatementsDocument8 pagesFinancial StatementsbouhaddihayetNo ratings yet

- Accounting TermsDocument5 pagesAccounting Termsbla csdcdNo ratings yet

- Chap.2 Financial Statements: Accounting Identity: Assets Liabilities + Owners' EquityDocument4 pagesChap.2 Financial Statements: Accounting Identity: Assets Liabilities + Owners' EquityGhassan EidNo ratings yet

- Chapter 2 Fundamentals of Accounting ConceptsDocument27 pagesChapter 2 Fundamentals of Accounting Conceptshaider_shah882267100% (1)

- BasicsDocument11 pagesBasicsMukesh MukiNo ratings yet

- Accounting Principles and Procedures: Indian Quantity Surveyors Association IQSA-APC-MatrixDocument11 pagesAccounting Principles and Procedures: Indian Quantity Surveyors Association IQSA-APC-MatrixKishan SolankimbaccepmpNo ratings yet

- Basic Terminologies of AccountingDocument3 pagesBasic Terminologies of AccountingAditi SoodNo ratings yet

- Financial Accounting - TestDocument9 pagesFinancial Accounting - TestAdriana MassaadNo ratings yet

- Chapter 2 Accounting PDFDocument23 pagesChapter 2 Accounting PDFChan Man SeongNo ratings yet

- Accounting Unit 1Document3 pagesAccounting Unit 1Pramod Kumar RayNo ratings yet

- Lecture - 2: Financial Reporting and AccountingDocument41 pagesLecture - 2: Financial Reporting and AccountingMuhammad Waheed SattiNo ratings yet

- Glossary of Terms For FA2 and MA2 AmendedDocument12 pagesGlossary of Terms For FA2 and MA2 AmendedS RaihanNo ratings yet

- Reviewer On Basic AccountingDocument8 pagesReviewer On Basic AccountingPRINCESS JOY BALAISNo ratings yet

- Glossaryof Business TermsDocument14 pagesGlossaryof Business TermsAmaresh MohapatraNo ratings yet

- Accounting Terminologies FABM 2121Document5 pagesAccounting Terminologies FABM 2121Richard MerkNo ratings yet

- Final Accounts LessonDocument12 pagesFinal Accounts LessonSiham KhayetNo ratings yet

- bd4769edd615cbff9a10b93d43ba3972Document17 pagesbd4769edd615cbff9a10b93d43ba3972Tanish HandaNo ratings yet

- Chapter 2 HandoutsDocument15 pagesChapter 2 HandoutsBlackpink BtsNo ratings yet

- 02 Handout 1Document6 pages02 Handout 1Stacy Anne LucidoNo ratings yet

- A Balance SheetDocument3 pagesA Balance SheetKarthik ThotaNo ratings yet

- Financial AccountingDocument13 pagesFinancial AccountingBogdan MorosanNo ratings yet

- Ans.Q1) Accounting Is The Process of Recording Financial Transactions Pertaining To ADocument8 pagesAns.Q1) Accounting Is The Process of Recording Financial Transactions Pertaining To ALavina AgarwalNo ratings yet

- The Four Financial StatementsDocument9 pagesThe Four Financial Statementssangeethadurjati100% (1)

- Finance and AccountsDocument10 pagesFinance and AccountsvijayNo ratings yet

- Financial CrisisDocument8 pagesFinancial CrisisАнна РиякоNo ratings yet

- Sitdikova Alsu CV66Document2 pagesSitdikova Alsu CV66Анна РиякоNo ratings yet

- Start The Business From ZeroDocument16 pagesStart The Business From ZeroАнна РиякоNo ratings yet

- BookkeepingDocument3 pagesBookkeepingАнна РиякоNo ratings yet

- AlsuDocument2 pagesAlsuАнна РиякоNo ratings yet

- Bogdanova OlgaDocument3 pagesBogdanova OlgaАнна РиякоNo ratings yet

- Bluedart Express: Strategic Investments Continue To Weigh On MarginsDocument9 pagesBluedart Express: Strategic Investments Continue To Weigh On MarginsYash AgarwalNo ratings yet

- Essay Topics For Engineers Professional ExaminationDocument6 pagesEssay Topics For Engineers Professional ExaminationAanper802No ratings yet

- Restaurant Startup Checklist: Countdown To Opening - by CategoryDocument60 pagesRestaurant Startup Checklist: Countdown To Opening - by CategoryMarisa Arizky PutriNo ratings yet

- 06.21.22 Brand Management Course Syllabus Fall 2022Document5 pages06.21.22 Brand Management Course Syllabus Fall 2022TrialNo ratings yet

- Earning Outcomes: LSPU Self-Paced Learning Module (SLM)Document35 pagesEarning Outcomes: LSPU Self-Paced Learning Module (SLM)Arolf John Michael LimboNo ratings yet

- Circle of Profit - 1Document7 pagesCircle of Profit - 1Harik CNo ratings yet

- Syllabus Level 4 AssistantDocument3 pagesSyllabus Level 4 AssistantNisha ThapaNo ratings yet

- Product Proposal For Achieving Your Life Goals Product Proposal For Achieving Your Life GoalsDocument6 pagesProduct Proposal For Achieving Your Life Goals Product Proposal For Achieving Your Life Goalsshikha742642No ratings yet

- Translation Exposure Part 1Document31 pagesTranslation Exposure Part 1Magzoub MohaNo ratings yet

- Enhancing SAP Standard Transactions FBL3N/FBL1N/FBL5N With Extra Fields in The Output List Via BTEDocument13 pagesEnhancing SAP Standard Transactions FBL3N/FBL1N/FBL5N With Extra Fields in The Output List Via BTEAhmed HamadNo ratings yet

- Adani Transmission LTDDocument7 pagesAdani Transmission LTDxia89627No ratings yet

- 2 Frontiers of Risk ManagementDocument29 pages2 Frontiers of Risk ManagementBooNo ratings yet

- SOCIAL SECURITY SYSTEM EMPLOYEES ASSOCIATION Vs CADocument4 pagesSOCIAL SECURITY SYSTEM EMPLOYEES ASSOCIATION Vs CAM Azeneth JJNo ratings yet

- YieldDocument15 pagesYieldcrisNo ratings yet

- Issues and Challenges of Foreign ProfessDocument10 pagesIssues and Challenges of Foreign ProfessVeer SinghNo ratings yet

- S3 - 3 - Alibaba Cainiao Initiatives in Air Cargo Logistics - XI Luhao - Alibaba Cainiao - EN PDFDocument13 pagesS3 - 3 - Alibaba Cainiao Initiatives in Air Cargo Logistics - XI Luhao - Alibaba Cainiao - EN PDFEdiNo ratings yet

- ZM Low Pressure 12p Brochure 2013 0423 LR tcm795-3550460 PDFDocument12 pagesZM Low Pressure 12p Brochure 2013 0423 LR tcm795-3550460 PDFhardik033No ratings yet

- Civil Service Reform in Malaysia - Commitment and ConsistencyDocument12 pagesCivil Service Reform in Malaysia - Commitment and ConsistencyManivannan M.BNo ratings yet

- Mirpuri v. CADocument22 pagesMirpuri v. CAMariaFaithFloresFelisartaNo ratings yet

- Finance (Theory) : MCQ Series Lecture - 5Document24 pagesFinance (Theory) : MCQ Series Lecture - 5devesh chaudharyNo ratings yet

- Shabbir Kamran - 00741946 - 645-TWI Middle East FZ - LLC - IG-1Document14 pagesShabbir Kamran - 00741946 - 645-TWI Middle East FZ - LLC - IG-1Rashid Jamil100% (1)

- Module 2.3 - Loan ReceivableDocument1 pageModule 2.3 - Loan ReceivableEilana CandelariaNo ratings yet

- Assessment Method 2 - Case Study-Part 1: Instructions To StudentsDocument9 pagesAssessment Method 2 - Case Study-Part 1: Instructions To StudentsJyoti Verma0% (3)

- NO HLD 10 TPSH 810008 - Rev00 Electrical Isolation Procedure TotalDocument16 pagesNO HLD 10 TPSH 810008 - Rev00 Electrical Isolation Procedure TotalAUGUSTA WIBI ARDIKTANo ratings yet

- Inflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyDocument34 pagesInflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyRazvan Catalin CostinNo ratings yet

- Claimant's - Statement - For - Death - Claim - (SSG Affinity)Document2 pagesClaimant's - Statement - For - Death - Claim - (SSG Affinity)saika tabbasumNo ratings yet

- Jawaban Soal, Akuntansi Menengah 1Document7 pagesJawaban Soal, Akuntansi Menengah 1Mira OktaviaNo ratings yet

- PT10 Issued RWP 2022 1355 38 232Document2 pagesPT10 Issued RWP 2022 1355 38 232Zeeshan MursleenNo ratings yet

- Funds Flow State Ment Method 2Document1 pageFunds Flow State Ment Method 2Vignesh NarayananNo ratings yet

- Plagiarism Checker X Originality Report: Similarity Found: 4%Document10 pagesPlagiarism Checker X Originality Report: Similarity Found: 4%Bicycle ThiefNo ratings yet

Download as docx, pdf, or txt

You might also like

- Accounting Terms & DefinitionsDocument6 pagesAccounting Terms & DefinitionsMir Wajid KhanNo ratings yet

- Accounting Term-WPS OfficeDocument9 pagesAccounting Term-WPS OfficeStefhanie Nicole C. GonzagaNo ratings yet

- 2 Accounting Work BookDocument89 pages2 Accounting Work Bookrachel rankuNo ratings yet

- Basics of AccountingDocument16 pagesBasics of Accountingmule mulugetaNo ratings yet

- Unit 1: Balance SheetDocument8 pagesUnit 1: Balance SheetthejeshwarNo ratings yet

- English For Accounting: Module Session 3 - Accounting Terms by Yulia Sulianti Se - Ak, M.IkomDocument3 pagesEnglish For Accounting: Module Session 3 - Accounting Terms by Yulia Sulianti Se - Ak, M.IkomWulan AyuNo ratings yet

- Accounting Equation: Ads by GoogleDocument9 pagesAccounting Equation: Ads by GoogleOliver HarmonNo ratings yet

- CH1 - Accounting in BusinessDocument18 pagesCH1 - Accounting in BusinessMaiaOshakmashviliNo ratings yet

- ACC321Document5 pagesACC321Allysa Del MundoNo ratings yet

- Chapter 10Document4 pagesChapter 10Nguyên BùiNo ratings yet

- Fabm Research ProjectDocument41 pagesFabm Research ProjectMon Kiego MagnoNo ratings yet

- Definition of AccountingDocument3 pagesDefinition of AccountingtpequitNo ratings yet

- Prepare Financial Report IbexDocument13 pagesPrepare Financial Report Ibexfentahun enyewNo ratings yet

- Accounting IntroductionDocument10 pagesAccounting Introductionomer mazharNo ratings yet

- Understand Basic Accounting TermsDocument5 pagesUnderstand Basic Accounting Termsabu taherNo ratings yet

- ACC321Document6 pagesACC321Allysa Del MundoNo ratings yet

- Accounting TermsDocument3 pagesAccounting Termsnada_nastityNo ratings yet

- Fabm 2 and FinanceDocument5 pagesFabm 2 and FinanceLenard TaberdoNo ratings yet

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae SasutilNo ratings yet

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae Sasutil100% (1)

- Chapter 1: Financialapplications Fundamentals of AccountingDocument60 pagesChapter 1: Financialapplications Fundamentals of AccountingSTEVE WAYNE100% (1)

- Accounting 1Document4 pagesAccounting 1Shoaib YousufNo ratings yet

- Receita KIWIFFDocument2 pagesReceita KIWIFFithallothallysdejesuslopesNo ratings yet

- Definition of Terms1Document3 pagesDefinition of Terms1Yusuf ÖzdemirNo ratings yet

- Equation Becomes: Assets A Liabilities L + Stockholders' Equity SEDocument2 pagesEquation Becomes: Assets A Liabilities L + Stockholders' Equity SEJorge L CastelarNo ratings yet

- AccountingDocument44 pagesAccountingPrasith baskyNo ratings yet

- Account Records Date Back To The Ancient CivilizatinsDocument6 pagesAccount Records Date Back To The Ancient Civilizatinsarimaskhassim00No ratings yet

- System of RecordDocument3 pagesSystem of RecordJonalyn MontecalvoNo ratings yet

- FABM Dictionary 1Document32 pagesFABM Dictionary 1Candy TinapayNo ratings yet

- Actg 1 Module 3Document5 pagesActg 1 Module 3Mae BertilloNo ratings yet

- Accounting AssignmentDocument2 pagesAccounting AssignmentMarvel TatingNo ratings yet

- Accounting CycleDocument4 pagesAccounting Cycleddoc.mimiNo ratings yet

- Introduction To AccountingDocument34 pagesIntroduction To AccountingBianca Mhae De LeonNo ratings yet

- What Is The Difference Between Job Costing and Process Costing?Document31 pagesWhat Is The Difference Between Job Costing and Process Costing?Muhammad AsimNo ratings yet

- FINANCIAL ACCOUNTING - AsbDocument9 pagesFINANCIAL ACCOUNTING - AsbMuskaanNo ratings yet

- Financial StatementsDocument8 pagesFinancial StatementsbouhaddihayetNo ratings yet

- Accounting TermsDocument5 pagesAccounting Termsbla csdcdNo ratings yet

- Chap.2 Financial Statements: Accounting Identity: Assets Liabilities + Owners' EquityDocument4 pagesChap.2 Financial Statements: Accounting Identity: Assets Liabilities + Owners' EquityGhassan EidNo ratings yet

- Chapter 2 Fundamentals of Accounting ConceptsDocument27 pagesChapter 2 Fundamentals of Accounting Conceptshaider_shah882267100% (1)

- BasicsDocument11 pagesBasicsMukesh MukiNo ratings yet

- Accounting Principles and Procedures: Indian Quantity Surveyors Association IQSA-APC-MatrixDocument11 pagesAccounting Principles and Procedures: Indian Quantity Surveyors Association IQSA-APC-MatrixKishan SolankimbaccepmpNo ratings yet

- Basic Terminologies of AccountingDocument3 pagesBasic Terminologies of AccountingAditi SoodNo ratings yet

- Financial Accounting - TestDocument9 pagesFinancial Accounting - TestAdriana MassaadNo ratings yet

- Chapter 2 Accounting PDFDocument23 pagesChapter 2 Accounting PDFChan Man SeongNo ratings yet

- Accounting Unit 1Document3 pagesAccounting Unit 1Pramod Kumar RayNo ratings yet

- Lecture - 2: Financial Reporting and AccountingDocument41 pagesLecture - 2: Financial Reporting and AccountingMuhammad Waheed SattiNo ratings yet

- Glossary of Terms For FA2 and MA2 AmendedDocument12 pagesGlossary of Terms For FA2 and MA2 AmendedS RaihanNo ratings yet

- Reviewer On Basic AccountingDocument8 pagesReviewer On Basic AccountingPRINCESS JOY BALAISNo ratings yet

- Glossaryof Business TermsDocument14 pagesGlossaryof Business TermsAmaresh MohapatraNo ratings yet

- Accounting Terminologies FABM 2121Document5 pagesAccounting Terminologies FABM 2121Richard MerkNo ratings yet

- Final Accounts LessonDocument12 pagesFinal Accounts LessonSiham KhayetNo ratings yet

- bd4769edd615cbff9a10b93d43ba3972Document17 pagesbd4769edd615cbff9a10b93d43ba3972Tanish HandaNo ratings yet

- Chapter 2 HandoutsDocument15 pagesChapter 2 HandoutsBlackpink BtsNo ratings yet

- 02 Handout 1Document6 pages02 Handout 1Stacy Anne LucidoNo ratings yet

- A Balance SheetDocument3 pagesA Balance SheetKarthik ThotaNo ratings yet

- Financial AccountingDocument13 pagesFinancial AccountingBogdan MorosanNo ratings yet

- Ans.Q1) Accounting Is The Process of Recording Financial Transactions Pertaining To ADocument8 pagesAns.Q1) Accounting Is The Process of Recording Financial Transactions Pertaining To ALavina AgarwalNo ratings yet

- The Four Financial StatementsDocument9 pagesThe Four Financial Statementssangeethadurjati100% (1)

- Finance and AccountsDocument10 pagesFinance and AccountsvijayNo ratings yet

- Financial CrisisDocument8 pagesFinancial CrisisАнна РиякоNo ratings yet

- Sitdikova Alsu CV66Document2 pagesSitdikova Alsu CV66Анна РиякоNo ratings yet

- Start The Business From ZeroDocument16 pagesStart The Business From ZeroАнна РиякоNo ratings yet

- BookkeepingDocument3 pagesBookkeepingАнна РиякоNo ratings yet

- AlsuDocument2 pagesAlsuАнна РиякоNo ratings yet

- Bogdanova OlgaDocument3 pagesBogdanova OlgaАнна РиякоNo ratings yet

- Bluedart Express: Strategic Investments Continue To Weigh On MarginsDocument9 pagesBluedart Express: Strategic Investments Continue To Weigh On MarginsYash AgarwalNo ratings yet

- Essay Topics For Engineers Professional ExaminationDocument6 pagesEssay Topics For Engineers Professional ExaminationAanper802No ratings yet

- Restaurant Startup Checklist: Countdown To Opening - by CategoryDocument60 pagesRestaurant Startup Checklist: Countdown To Opening - by CategoryMarisa Arizky PutriNo ratings yet

- 06.21.22 Brand Management Course Syllabus Fall 2022Document5 pages06.21.22 Brand Management Course Syllabus Fall 2022TrialNo ratings yet

- Earning Outcomes: LSPU Self-Paced Learning Module (SLM)Document35 pagesEarning Outcomes: LSPU Self-Paced Learning Module (SLM)Arolf John Michael LimboNo ratings yet

- Circle of Profit - 1Document7 pagesCircle of Profit - 1Harik CNo ratings yet

- Syllabus Level 4 AssistantDocument3 pagesSyllabus Level 4 AssistantNisha ThapaNo ratings yet

- Product Proposal For Achieving Your Life Goals Product Proposal For Achieving Your Life GoalsDocument6 pagesProduct Proposal For Achieving Your Life Goals Product Proposal For Achieving Your Life Goalsshikha742642No ratings yet

- Translation Exposure Part 1Document31 pagesTranslation Exposure Part 1Magzoub MohaNo ratings yet

- Enhancing SAP Standard Transactions FBL3N/FBL1N/FBL5N With Extra Fields in The Output List Via BTEDocument13 pagesEnhancing SAP Standard Transactions FBL3N/FBL1N/FBL5N With Extra Fields in The Output List Via BTEAhmed HamadNo ratings yet

- Adani Transmission LTDDocument7 pagesAdani Transmission LTDxia89627No ratings yet

- 2 Frontiers of Risk ManagementDocument29 pages2 Frontiers of Risk ManagementBooNo ratings yet

- SOCIAL SECURITY SYSTEM EMPLOYEES ASSOCIATION Vs CADocument4 pagesSOCIAL SECURITY SYSTEM EMPLOYEES ASSOCIATION Vs CAM Azeneth JJNo ratings yet

- YieldDocument15 pagesYieldcrisNo ratings yet

- Issues and Challenges of Foreign ProfessDocument10 pagesIssues and Challenges of Foreign ProfessVeer SinghNo ratings yet

- S3 - 3 - Alibaba Cainiao Initiatives in Air Cargo Logistics - XI Luhao - Alibaba Cainiao - EN PDFDocument13 pagesS3 - 3 - Alibaba Cainiao Initiatives in Air Cargo Logistics - XI Luhao - Alibaba Cainiao - EN PDFEdiNo ratings yet

- ZM Low Pressure 12p Brochure 2013 0423 LR tcm795-3550460 PDFDocument12 pagesZM Low Pressure 12p Brochure 2013 0423 LR tcm795-3550460 PDFhardik033No ratings yet

- Civil Service Reform in Malaysia - Commitment and ConsistencyDocument12 pagesCivil Service Reform in Malaysia - Commitment and ConsistencyManivannan M.BNo ratings yet

- Mirpuri v. CADocument22 pagesMirpuri v. CAMariaFaithFloresFelisartaNo ratings yet

- Finance (Theory) : MCQ Series Lecture - 5Document24 pagesFinance (Theory) : MCQ Series Lecture - 5devesh chaudharyNo ratings yet

- Shabbir Kamran - 00741946 - 645-TWI Middle East FZ - LLC - IG-1Document14 pagesShabbir Kamran - 00741946 - 645-TWI Middle East FZ - LLC - IG-1Rashid Jamil100% (1)

- Module 2.3 - Loan ReceivableDocument1 pageModule 2.3 - Loan ReceivableEilana CandelariaNo ratings yet

- Assessment Method 2 - Case Study-Part 1: Instructions To StudentsDocument9 pagesAssessment Method 2 - Case Study-Part 1: Instructions To StudentsJyoti Verma0% (3)

- NO HLD 10 TPSH 810008 - Rev00 Electrical Isolation Procedure TotalDocument16 pagesNO HLD 10 TPSH 810008 - Rev00 Electrical Isolation Procedure TotalAUGUSTA WIBI ARDIKTANo ratings yet

- Inflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyDocument34 pagesInflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyRazvan Catalin CostinNo ratings yet

- Claimant's - Statement - For - Death - Claim - (SSG Affinity)Document2 pagesClaimant's - Statement - For - Death - Claim - (SSG Affinity)saika tabbasumNo ratings yet

- Jawaban Soal, Akuntansi Menengah 1Document7 pagesJawaban Soal, Akuntansi Menengah 1Mira OktaviaNo ratings yet

- PT10 Issued RWP 2022 1355 38 232Document2 pagesPT10 Issued RWP 2022 1355 38 232Zeeshan MursleenNo ratings yet

- Funds Flow State Ment Method 2Document1 pageFunds Flow State Ment Method 2Vignesh NarayananNo ratings yet

- Plagiarism Checker X Originality Report: Similarity Found: 4%Document10 pagesPlagiarism Checker X Originality Report: Similarity Found: 4%Bicycle ThiefNo ratings yet