Download as pdf or txt

You might also like

- Valucon ReviewerDocument12 pagesValucon ReviewerAnjo Salonga del Rosario100% (4)

- RJR Nabisco - Case QuestionsDocument2 pagesRJR Nabisco - Case QuestionsJorge SmithNo ratings yet

- VCM ReviewerDocument2 pagesVCM ReviewerChristen HerceNo ratings yet

- Valuation 1-3Document8 pagesValuation 1-3HERMENIA PAGUINTONo ratings yet

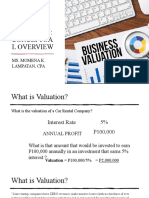

- What Is Valuation?Document14 pagesWhat Is Valuation?aswinvignesh38No ratings yet

- Introduction To Business ValuationDocument9 pagesIntroduction To Business Valuationscholta00No ratings yet

- Valuation ConsultancyDocument6 pagesValuation ConsultancyNishant Shah, GAANo ratings yet

- Business ValuationDocument8 pagesBusiness ValuationKomalNo ratings yet

- Fundamental Analysis: Capital MarketsDocument19 pagesFundamental Analysis: Capital MarketsIT GAMINGNo ratings yet

- Corporate AccountingDocument17 pagesCorporate AccountingShriyaNo ratings yet

- Valuation Notes C2Document10 pagesValuation Notes C2kristine torresNo ratings yet

- F9 Note (Business Valuation 1)Document12 pagesF9 Note (Business Valuation 1)CHIAMAKA EGBUKOLE100% (1)

- VALUATIONDocument7 pagesVALUATIONOllid Kline Jayson JNo ratings yet

- CH 1 P1 PDFDocument16 pagesCH 1 P1 PDFAhmed RedaNo ratings yet

- Legon Stats BSC Actuarial Company ValuationDocument3 pagesLegon Stats BSC Actuarial Company ValuationSamuel EssumanNo ratings yet

- Stock and Stock Valuation Garcia Cheska Kate HDocument4 pagesStock and Stock Valuation Garcia Cheska Kate HJosua PranataNo ratings yet

- Chapter 1 FUNDAMENTALS PRINCIPLES OF VALUATIONDocument52 pagesChapter 1 FUNDAMENTALS PRINCIPLES OF VALUATIONMs. VelNo ratings yet

- Conceptual Overview To ValuationDocument23 pagesConceptual Overview To ValuationHazraphine Linso100% (1)

- Cept of Value and Principles and Techniques of Valuation 1Document5 pagesCept of Value and Principles and Techniques of Valuation 1Kristelle De VeraNo ratings yet

- Module 2 CVR Notes PDFDocument8 pagesModule 2 CVR Notes PDFDr. Shalini H SNo ratings yet

- ValuationDocument7 pagesValuationSiva SankariNo ratings yet

- Valuation 1Document13 pagesValuation 1Shantanu JanaNo ratings yet

- Task 1Document5 pagesTask 1my youtube advisorNo ratings yet

- Lesson 1 - OVERVIEW OF VALUATION CONCEPTS AND METHODSDocument14 pagesLesson 1 - OVERVIEW OF VALUATION CONCEPTS AND METHODSGevilyn M. GomezNo ratings yet

- Valuation: The Valuation Principle: The Foundation of Financial Decision Making ValuationDocument15 pagesValuation: The Valuation Principle: The Foundation of Financial Decision Making ValuationWensky RagpalaNo ratings yet

- Valuation-Ch 01 Part OneDocument16 pagesValuation-Ch 01 Part OneMostafa HossamNo ratings yet

- ECON75 Lecture VI. Valuation Financial AnalysisDocument120 pagesECON75 Lecture VI. Valuation Financial AnalysisJoshua De VeraNo ratings yet

- Lesson 1 OVERVIEW OF VALUATION CONCEPTS AND METHODSDocument4 pagesLesson 1 OVERVIEW OF VALUATION CONCEPTS AND METHODSJessica PaludipanNo ratings yet

- Reflection Paper Valuation FinalDocument7 pagesReflection Paper Valuation FinalMaureen CortezNo ratings yet

- What Is Valuation?: Capital Structure Market Value Fundamental Analysis Capm DDMDocument4 pagesWhat Is Valuation?: Capital Structure Market Value Fundamental Analysis Capm DDMRohit BajpaiNo ratings yet

- Curs 1-5 InvestopediaDocument25 pagesCurs 1-5 InvestopediasdasdfaNo ratings yet

- Sos ReportDocument6 pagesSos ReportTushaar JhamtaniNo ratings yet

- VALUATIONPPTDocument12 pagesVALUATIONPPTdevNo ratings yet

- Equity Research On Ultratech CementDocument17 pagesEquity Research On Ultratech CementViral GalaNo ratings yet

- Equity Vs EVDocument9 pagesEquity Vs EVSudipta ChatterjeeNo ratings yet

- Long Quiz Chap 1Document3 pagesLong Quiz Chap 1Christen HerceNo ratings yet

- PRE 6 Lesson 1Document4 pagesPRE 6 Lesson 1Angeli GarcesNo ratings yet

- ASSIGNMENT 2 FinanceDocument2 pagesASSIGNMENT 2 FinanceAbhishek ChoudharyNo ratings yet

- How To Value A CompanyDocument120 pagesHow To Value A CompanyAbhishek kushawahaNo ratings yet

- GAURAV Valuation Content Edited RevisedDocument17 pagesGAURAV Valuation Content Edited Revisedgauravbansall567No ratings yet

- Fundamentals Principles of ValuationDocument48 pagesFundamentals Principles of Valuationorion.dimaapi14No ratings yet

- Intro To ValuationDocument6 pagesIntro To ValuationDEVERLYN SAQUIDONo ratings yet

- Lecture 1Document3 pagesLecture 1Eric CauilanNo ratings yet

- Valuation Methods Chapter 1Document5 pagesValuation Methods Chapter 1garcesangelidanielle2324No ratings yet

- F3 Chapter 12Document37 pagesF3 Chapter 12Ali ShahnawazNo ratings yet

- Fixed Asset Accounting and ManagementDocument16 pagesFixed Asset Accounting and ManagementOni SegunNo ratings yet

- IPO ValuationDocument3 pagesIPO Valuationansh071102No ratings yet

- Valuation AcquisitionDocument4 pagesValuation AcquisitionKnt Nallasamy GounderNo ratings yet

- Asset Base ValuationDocument27 pagesAsset Base ValuationLinda JNo ratings yet

- Task 3 - Investment AppraisalDocument12 pagesTask 3 - Investment AppraisalYashmi BhanderiNo ratings yet

- VALUATION CHP 1 - Edited Handout (BNW)Document8 pagesVALUATION CHP 1 - Edited Handout (BNW)Jadea RioNo ratings yet

- FIN 404 Final AssessmentDocument16 pagesFIN 404 Final AssessmentHOSSAIN MOHAMMAD YEASINNo ratings yet

- Unit - Iv Valuation of Shares and Goodwill What Is Share Valuation?Document56 pagesUnit - Iv Valuation of Shares and Goodwill What Is Share Valuation?Rizwan AkhtarNo ratings yet

- FNE Security Analysis PRELIMDocument6 pagesFNE Security Analysis PRELIMAldrin John TungolNo ratings yet

- Managerial AnalysisDocument5 pagesManagerial Analysiswriters herbNo ratings yet

- VALCOM d1Document4 pagesVALCOM d1Ivan Jay E. EsminoNo ratings yet

- Key TermsDocument73 pagesKey Termsnmsusarla999No ratings yet

- Valuation Concept and MethodologiesDocument8 pagesValuation Concept and MethodologiesKei YoshidaNo ratings yet

- 11 - Business Valuation: Prof. S. Satya MoorthiDocument13 pages11 - Business Valuation: Prof. S. Satya MoorthiVandana Kuntal ChaharNo ratings yet

- Price-Earnings Ratio (P/E Ratio)Document6 pagesPrice-Earnings Ratio (P/E Ratio)Asif AminNo ratings yet

- Unit 1Document15 pagesUnit 1tayyaba fatimaNo ratings yet

- Introduction in JIT and Lean OperationsDocument4 pagesIntroduction in JIT and Lean OperationsAlexis RiveraNo ratings yet

- BUSINESS MATH - Chapter 5Document5 pagesBUSINESS MATH - Chapter 5Alexis RiveraNo ratings yet

- Introduction To Science, Technology and Society: John Heilbron (2003)Document4 pagesIntroduction To Science, Technology and Society: John Heilbron (2003)Alexis RiveraNo ratings yet

- Sts 1Document4 pagesSts 1Alexis RiveraNo ratings yet

- Mas 02 - CVPDocument24 pagesMas 02 - CVPAlexis RiveraNo ratings yet

- Prelim SeatworkDocument4 pagesPrelim SeatworkAlexis RiveraNo ratings yet

- Stra MaDocument4 pagesStra MaAlexis RiveraNo ratings yet

- Living in The IT Era HandoutsDocument36 pagesLiving in The IT Era HandoutsAlexis RiveraNo ratings yet

- Risk AnalysisDocument2 pagesRisk AnalysisAlexis RiveraNo ratings yet

- Prelim QuizDocument26 pagesPrelim QuizAlexis RiveraNo ratings yet

- Mergers and Acquisitions: Group 5Document18 pagesMergers and Acquisitions: Group 5Pratham TadasareNo ratings yet

- LBO (Leveraged Buyout) Model For Private Equity FirmsDocument2 pagesLBO (Leveraged Buyout) Model For Private Equity FirmsDishant KhanejaNo ratings yet

- CBS Pe KKRDocument2 pagesCBS Pe KKRJames bondNo ratings yet

- LBO Blank TemplateDocument15 pagesLBO Blank TemplateBrian DongNo ratings yet

- LBO Interviews Questions BIWSDocument5 pagesLBO Interviews Questions BIWSartemidualikNo ratings yet

- Dear ChairmanDocument4 pagesDear ChairmanSrishti 2k22No ratings yet

- Jefferies-Global Secondary Market Review-January 2023Document10 pagesJefferies-Global Secondary Market Review-January 2023Chuan JiNo ratings yet

- EDF Will Indeed Buy The Nuclear Activity of GE (Ex-Alstom)Document3 pagesEDF Will Indeed Buy The Nuclear Activity of GE (Ex-Alstom)Ramesh-NairNo ratings yet

- Ia Assignment 3Document3 pagesIa Assignment 3Resty VillaroelNo ratings yet

- Determinants of Mergers: A Case of Specified Purpose Acquisition Companies (Spacs)Document8 pagesDeterminants of Mergers: A Case of Specified Purpose Acquisition Companies (Spacs)payal chaudhariNo ratings yet

- Mergers AND Acquisitions: BY: Piyush Bhardwaj Jaikrit VatsalDocument31 pagesMergers AND Acquisitions: BY: Piyush Bhardwaj Jaikrit Vatsalamaad4mNo ratings yet

- 2025 CFA Level 1 IFT Review Notes (Sample)Document14 pages2025 CFA Level 1 IFT Review Notes (Sample)craigsappletreeNo ratings yet

- Exercise Answers - General ConceptsDocument2 pagesExercise Answers - General ConceptsJohn Philip L Concepcion100% (1)

- TP M&aDocument7 pagesTP M&aKAVVIKANo ratings yet

- Chapter 21Document5 pagesChapter 21John Dale Mondejar0% (1)

- Toys "R" Us Files For Bankruptcy: The Rise of E-Commerce Did For America's Former FavouriteDocument2 pagesToys "R" Us Files For Bankruptcy: The Rise of E-Commerce Did For America's Former FavouritedevikaNo ratings yet

- BP Dividend Valuation FinancingDocument31 pagesBP Dividend Valuation FinancingTowhidul IslamNo ratings yet

- Intermediate AccountingDocument4 pagesIntermediate AccountingMary Ellen LuceñaNo ratings yet

- Advanced Accounting 4th Edition Jeter Test BankDocument20 pagesAdvanced Accounting 4th Edition Jeter Test Bankbryanharrismpqrsfbokn100% (15)

- Mergers and AcquisitionsDocument20 pagesMergers and Acquisitionsfirman prabowoNo ratings yet

- Chapter 13 Financing The DealDocument27 pagesChapter 13 Financing The DealK60 Phạm Thị Phương AnhNo ratings yet

- Ifrs 3 - Business Combination: According To The Nature of BusinessDocument5 pagesIfrs 3 - Business Combination: According To The Nature of BusinessBrian GoNo ratings yet

- The Twitter (Leveraged) Buyout: Is Elon Musk A Madman or A Genius?Document23 pagesThe Twitter (Leveraged) Buyout: Is Elon Musk A Madman or A Genius?merag76668No ratings yet

- Final - Welingkar - Private Equity CompaniesDocument60 pagesFinal - Welingkar - Private Equity Companiessam coolNo ratings yet

- Alternative Investments - Cheat SheetDocument6 pagesAlternative Investments - Cheat SheetUchit MehtaNo ratings yet

- IBIG 03 03 Your Own DealsDocument17 pagesIBIG 03 03 Your Own DealsіфвпаіNo ratings yet

- Chapter 5 - Bonds Payable Other ConceptsDocument28 pagesChapter 5 - Bonds Payable Other ConceptsAngelica Joy ManaoisNo ratings yet

- Private Equity Part 3Document6 pagesPrivate Equity Part 3Paolina NikolovaNo ratings yet