234 Lkwef 132 e 23 LK 428 G 3 Oh 987

234 Lkwef 132 e 23 LK 428 G 3 Oh 987

You might also like

- Pavegen (Final Project)Document18 pagesPavegen (Final Project)K M Tanveer Ahmed0% (1)

- Latin America Gri Real Estate 2023Document22 pagesLatin America Gri Real Estate 2023Tiago Pedroso FonsecaNo ratings yet

- Eq Test Questionnaire PDFDocument5 pagesEq Test Questionnaire PDFAnna May Daray0% (1)

- Suzlon Energy Call TranscriptDocument19 pagesSuzlon Energy Call TranscriptKishor TilokaniNo ratings yet

- Solar Energy Handbook BarcapDocument396 pagesSolar Energy Handbook BarcapClaudio SalinasNo ratings yet

- Q3 09 FinalDocument2 pagesQ3 09 FinalHeng Chong KwangNo ratings yet

- India Solar Handbook 2016 PDFDocument33 pagesIndia Solar Handbook 2016 PDFalkanm750No ratings yet

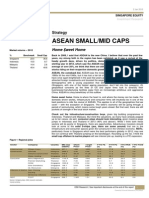

- 2jan13 - ASEAN Small CapsDocument11 pages2jan13 - ASEAN Small Capsqwerty1991srNo ratings yet

- Company Analysis Uge International (UGE - TSXV // UGEIF-PINK)Document27 pagesCompany Analysis Uge International (UGE - TSXV // UGEIF-PINK)tomave1No ratings yet

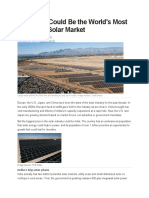

- Why India Could Be The World's Most Important Solar Market: Travis Hoium More Articles CommentsDocument6 pagesWhy India Could Be The World's Most Important Solar Market: Travis Hoium More Articles CommentsShakthi RatnakumaranNo ratings yet

- US Solar Market Insight - 2013 YIR - Executive SummaryDocument22 pagesUS Solar Market Insight - 2013 YIR - Executive SummaryNguyen Doan QuyetNo ratings yet

- Adani Write-UpDocument6 pagesAdani Write-UpadithyaNo ratings yet

- RHB Equity 360° - 19 July 2010 (O&G, Berjaya Retail Technical: Genting, UEM Land) - 19/7/2010Document3 pagesRHB Equity 360° - 19 July 2010 (O&G, Berjaya Retail Technical: Genting, UEM Land) - 19/7/2010Rhb InvestNo ratings yet

- Political EconomicalDocument15 pagesPolitical EconomicalRaymond PascualNo ratings yet

- Top 10 Solar Trends For 2011Document3 pagesTop 10 Solar Trends For 2011hmm14No ratings yet

- Chapter3 - Economic Growth QuestionsDocument6 pagesChapter3 - Economic Growth QuestionsvietzergNo ratings yet

- Below Is The Verbatim Transcript. Also Watch The Accompanying VideoDocument2 pagesBelow Is The Verbatim Transcript. Also Watch The Accompanying VideoJason FernandesNo ratings yet

- Good News Amid The Influx of Bad NewsDocument3 pagesGood News Amid The Influx of Bad Newsjan gatchallanNo ratings yet

- Business Plan of Solar SystemDocument31 pagesBusiness Plan of Solar SystemIsrar AhmadNo ratings yet

- BRIDGE To INDIA India Solar Handbook 2015 Online 1Document28 pagesBRIDGE To INDIA India Solar Handbook 2015 Online 1Nithya Susan VargheseNo ratings yet

- TexttDocument3 pagesTexttjakife8633No ratings yet

- RHB Equity 360° - 13 September 2010 (Emas Kiara, Banks, Mah Sing, SP Setia Technical: TDC, WCT)Document4 pagesRHB Equity 360° - 13 September 2010 (Emas Kiara, Banks, Mah Sing, SP Setia Technical: TDC, WCT)Rhb InvestNo ratings yet

- 1127 Course SharingDocument7 pages1127 Course Sharingshanizam ariffinNo ratings yet

- Byte Case StudyDocument17 pagesByte Case StudyWael_Barakat_3179100% (1)

- Launch Vodafone in Pakistan StrategiesDocument45 pagesLaunch Vodafone in Pakistan StrategiesshNo ratings yet

- 1116 Course SharingDocument8 pages1116 Course Sharingshanizam ariffinNo ratings yet

- Is Malaysia Ready For The Renewable Energy EraDocument7 pagesIs Malaysia Ready For The Renewable Energy EraMr. HNo ratings yet

- Budget 2012-13: Pragmatism Must Dictate: by Abu Yousuf Md. Abdullah, PHDDocument4 pagesBudget 2012-13: Pragmatism Must Dictate: by Abu Yousuf Md. Abdullah, PHDAshfaqul Haq ChowdhuryNo ratings yet

- Entrepreneurship Business PlanDocument35 pagesEntrepreneurship Business PlanUmar FarooqNo ratings yet

- Long Term FinancingDocument15 pagesLong Term FinancingPriyanshu BhattacharyaNo ratings yet

- Improving The Policies of Solar Energy in Pakistan: Current ProgressDocument5 pagesImproving The Policies of Solar Energy in Pakistan: Current ProgressabidNo ratings yet

- ECO720 Global and Regional Economic Development FinalsDocument13 pagesECO720 Global and Regional Economic Development FinalsJohn TanNo ratings yet

- Suzlon - An Investment CaseDocument5 pagesSuzlon - An Investment CaseAbhilasha BansalNo ratings yet

- The India Solar HandbookDocument44 pagesThe India Solar Handbookamasssk22108No ratings yet

- Redwan Afrid Avin - 19104022 - BUS203 - Section 4Document5 pagesRedwan Afrid Avin - 19104022 - BUS203 - Section 4Redwan Afrid AvinNo ratings yet

- 3 A New Singaporean Growth Model Can Energize Emerging AsiaDocument5 pages3 A New Singaporean Growth Model Can Energize Emerging AsiaYudi KhoNo ratings yet

- Solar Energy Au1910330 AasthagalaniDocument15 pagesSolar Energy Au1910330 AasthagalaniAastha GalaniNo ratings yet

- Case of AJL Capital Equities-FinalDocument8 pagesCase of AJL Capital Equities-FinalDavy RoseNo ratings yet

- Singapore Property Weekly Issue 89Document16 pagesSingapore Property Weekly Issue 89Propwise.sgNo ratings yet

- Executive SummaryDocument23 pagesExecutive SummaryZahid Bin IslamNo ratings yet

- Potential Impact of COVID-19 On Indian EconomyDocument7 pagesPotential Impact of COVID-19 On Indian EconomyHarshit Kumar SinghNo ratings yet

- PWC Real Estate 2020Document40 pagesPWC Real Estate 2020jcschiaffino100% (1)

- Next Pot of Gold!Document10 pagesNext Pot of Gold!Aryan SharmaNo ratings yet

- Lu Nam Anh Rough DraftDocument7 pagesLu Nam Anh Rough Draftsvxnv88kynNo ratings yet

- EY Middle East and North Africa Cleantech SurveyDocument24 pagesEY Middle East and North Africa Cleantech SurveylassasaNo ratings yet

- Suzlon AnalysisDocument31 pagesSuzlon AnalysisSushil KumarNo ratings yet

- RHB Equity 360° (Strategy, Market, Plantation, Telecom, Steel, Faber, KPJ, PetGas Technical: DRB-Hicom) - 01/04/2010Document6 pagesRHB Equity 360° (Strategy, Market, Plantation, Telecom, Steel, Faber, KPJ, PetGas Technical: DRB-Hicom) - 01/04/2010Rhb InvestNo ratings yet

- SectoralUpdate 03012014Document13 pagesSectoralUpdate 03012014ashish10mcaNo ratings yet

- Assignment On Telecommunication Industry in BangladeshDocument23 pagesAssignment On Telecommunication Industry in BangladeshMd.Hafizur RahamanNo ratings yet

- Prediction Consensus - News English SpeakingDocument5 pagesPrediction Consensus - News English Speaking노진성No ratings yet

- Market Size: LG PakistanDocument3 pagesMarket Size: LG PakistanAmir AliNo ratings yet

- Business Confidence SaggingDocument7 pagesBusiness Confidence SagginghellonelsonNo ratings yet

- The State of Lagos Housing Market Report TEASER N75000 PERDocument21 pagesThe State of Lagos Housing Market Report TEASER N75000 PEROkewole Olayemi SamuelNo ratings yet

- Solar Facts & Figures - Southeast Asia 2018Document38 pagesSolar Facts & Figures - Southeast Asia 2018TeeBoneNo ratings yet

- Stock MarketDocument7 pagesStock Marketapi-375962513No ratings yet

- Global Wind Report 2010Document72 pagesGlobal Wind Report 2010Uğur ÖzkanNo ratings yet

- China's New Energy Revolution: How the World Super Power is Fostering Economic Development and Sustainable Growth through Thin-Film Solar TechnologyFrom EverandChina's New Energy Revolution: How the World Super Power is Fostering Economic Development and Sustainable Growth through Thin-Film Solar TechnologyNo ratings yet

- Freedom Unleashed: How to Make Malaysia a Tax Free CountryFrom EverandFreedom Unleashed: How to Make Malaysia a Tax Free CountryRating: 5 out of 5 stars5/5 (1)

- Defying the Market (Review and Analysis of the Leebs' Book)From EverandDefying the Market (Review and Analysis of the Leebs' Book)No ratings yet

- Philippines: Energy Sector Assessment, Strategy, and Road MapFrom EverandPhilippines: Energy Sector Assessment, Strategy, and Road MapNo ratings yet

- 234 LK 23 LK 428 G 3 OhDocument3 pages234 LK 23 LK 428 G 3 OhDannyNo ratings yet

- Fae 5 y 4 U 6 J 5 Nrythew 35546Document2 pagesFae 5 y 4 U 6 J 5 Nrythew 35546DannyNo ratings yet

- 234 LK 3 y 53 Het 23 LK 428 G 3 Oh 8759Document4 pages234 LK 3 y 53 Het 23 LK 428 G 3 Oh 8759DannyNo ratings yet

- 234 LK 23 LK 428 G 3 Ohw 2 R 098 y 1 TH 2 GoqDocument3 pages234 LK 23 LK 428 G 3 Ohw 2 R 098 y 1 TH 2 GoqDannyNo ratings yet

- 234 LK 23 LK 428 G 3 Ohi 7 Qef 97Document9 pages234 LK 23 LK 428 G 3 Ohi 7 Qef 97DannyNo ratings yet

- 234 LK 23 LK 428 G 3 Oh 8759Document6 pages234 LK 23 LK 428 G 3 Oh 8759DannyNo ratings yet

- ACG StarterDocument1 pageACG StarterLeo HiterozaNo ratings yet

- Marketing Information SystemDocument3 pagesMarketing Information SystemsanjayNo ratings yet

- Scrap Specifications CircularDocument57 pagesScrap Specifications Circulargiám địnhNo ratings yet

- Devops MCQ PDFDocument6 pagesDevops MCQ PDFSaad Mohamed SaadNo ratings yet

- IBM Power Systems Cloud Security Guide: Protect IT Infrastructure in All LayersDocument220 pagesIBM Power Systems Cloud Security Guide: Protect IT Infrastructure in All Layersbenmagha9904No ratings yet

- Proforma Architect - Owner Agreement: Very Important NotesDocument11 pagesProforma Architect - Owner Agreement: Very Important NotesJean Erika Bermudo BisoñaNo ratings yet

- MKT 005 Module 6 SASDocument5 pagesMKT 005 Module 6 SASconandetic123No ratings yet

- 2014 Elec HD FS CKTruck 100713 ChevroletDocument247 pages2014 Elec HD FS CKTruck 100713 ChevroletREINALDO GONZALEZNo ratings yet

- Emg ManualDocument20 pagesEmg ManualSalih AnwarNo ratings yet

- Aditya Vikram Verma - CVDocument2 pagesAditya Vikram Verma - CVAdityaVikramVermaNo ratings yet

- Fleck SXT Timer: Service ManualDocument24 pagesFleck SXT Timer: Service ManualdracuojiNo ratings yet

- CBME 102 REviewerDocument17 pagesCBME 102 REviewerEilen Joyce BisnarNo ratings yet

- Self-Efficacy Mediated Spiritual Leadership On Citizenship Behavior Towards The Environment of Employees at Harapan Keluarga HospitalDocument7 pagesSelf-Efficacy Mediated Spiritual Leadership On Citizenship Behavior Towards The Environment of Employees at Harapan Keluarga HospitalInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- On Annemarie Mols The Body MultipleDocument4 pagesOn Annemarie Mols The Body MultipleMAGALY GARCIA RINCONNo ratings yet

- Supplemental-Guide GenderQuestWkbkTeensDocument9 pagesSupplemental-Guide GenderQuestWkbkTeensPaula ZuccoloNo ratings yet

- Parametric & Non Parametric TestDocument8 pagesParametric & Non Parametric TestAngelica Alejandro100% (1)

- Competency Enhancing Courses Jan June2023Document2 pagesCompetency Enhancing Courses Jan June2023Yashveer TakooryNo ratings yet

- Visto-Resume 26710306Document1 pageVisto-Resume 26710306api-350663722No ratings yet

- Phenomena of Double RefractionDocument5 pagesPhenomena of Double RefractionMahendra PandaNo ratings yet

- Setting Goals: Throughout This Course You Have Gone Through The Process of Education and Career/Life PlanningDocument4 pagesSetting Goals: Throughout This Course You Have Gone Through The Process of Education and Career/Life PlanningMuhammad AbdullahNo ratings yet

- TRA 02 Lifting of Skid Units During Rig MovesDocument3 pagesTRA 02 Lifting of Skid Units During Rig MovesPirlo PoloNo ratings yet

- Thesis Statement About Business AdministrationDocument4 pagesThesis Statement About Business Administrationokxyghxff100% (2)

- Art Meta-Analyses of Experimental Data in An PDFDocument12 pagesArt Meta-Analyses of Experimental Data in An PDFIonela HoteaNo ratings yet

- Performix™ High Speed Dissolver - Technical DataDocument1 pagePerformix™ High Speed Dissolver - Technical DataNegash JaferNo ratings yet

- Performance TaskDocument6 pagesPerformance TaskPrinces Aliesa Bulanadi100% (1)

- Ashcroft Dial GaugeDocument1 pageAshcroft Dial GaugeReva Astra DiptaNo ratings yet

- Troy-Bilt 019191 PDFDocument34 pagesTroy-Bilt 019191 PDFSteven W. NinichuckNo ratings yet

- Job Shop Scheduling Vs Flow Shop SchedulingDocument11 pagesJob Shop Scheduling Vs Flow Shop SchedulingMatthew MhlongoNo ratings yet

- Docusign: Customer Success Case Study SamplerDocument7 pagesDocusign: Customer Success Case Study Samplerozge100% (1)

Download as txt, pdf, or txt

You might also like

- Pavegen (Final Project)Document18 pagesPavegen (Final Project)K M Tanveer Ahmed0% (1)

- Latin America Gri Real Estate 2023Document22 pagesLatin America Gri Real Estate 2023Tiago Pedroso FonsecaNo ratings yet

- Eq Test Questionnaire PDFDocument5 pagesEq Test Questionnaire PDFAnna May Daray0% (1)

- Suzlon Energy Call TranscriptDocument19 pagesSuzlon Energy Call TranscriptKishor TilokaniNo ratings yet

- Solar Energy Handbook BarcapDocument396 pagesSolar Energy Handbook BarcapClaudio SalinasNo ratings yet

- Q3 09 FinalDocument2 pagesQ3 09 FinalHeng Chong KwangNo ratings yet

- India Solar Handbook 2016 PDFDocument33 pagesIndia Solar Handbook 2016 PDFalkanm750No ratings yet

- 2jan13 - ASEAN Small CapsDocument11 pages2jan13 - ASEAN Small Capsqwerty1991srNo ratings yet

- Company Analysis Uge International (UGE - TSXV // UGEIF-PINK)Document27 pagesCompany Analysis Uge International (UGE - TSXV // UGEIF-PINK)tomave1No ratings yet

- Why India Could Be The World's Most Important Solar Market: Travis Hoium More Articles CommentsDocument6 pagesWhy India Could Be The World's Most Important Solar Market: Travis Hoium More Articles CommentsShakthi RatnakumaranNo ratings yet

- US Solar Market Insight - 2013 YIR - Executive SummaryDocument22 pagesUS Solar Market Insight - 2013 YIR - Executive SummaryNguyen Doan QuyetNo ratings yet

- Adani Write-UpDocument6 pagesAdani Write-UpadithyaNo ratings yet

- RHB Equity 360° - 19 July 2010 (O&G, Berjaya Retail Technical: Genting, UEM Land) - 19/7/2010Document3 pagesRHB Equity 360° - 19 July 2010 (O&G, Berjaya Retail Technical: Genting, UEM Land) - 19/7/2010Rhb InvestNo ratings yet

- Political EconomicalDocument15 pagesPolitical EconomicalRaymond PascualNo ratings yet

- Top 10 Solar Trends For 2011Document3 pagesTop 10 Solar Trends For 2011hmm14No ratings yet

- Chapter3 - Economic Growth QuestionsDocument6 pagesChapter3 - Economic Growth QuestionsvietzergNo ratings yet

- Below Is The Verbatim Transcript. Also Watch The Accompanying VideoDocument2 pagesBelow Is The Verbatim Transcript. Also Watch The Accompanying VideoJason FernandesNo ratings yet

- Good News Amid The Influx of Bad NewsDocument3 pagesGood News Amid The Influx of Bad Newsjan gatchallanNo ratings yet

- Business Plan of Solar SystemDocument31 pagesBusiness Plan of Solar SystemIsrar AhmadNo ratings yet

- BRIDGE To INDIA India Solar Handbook 2015 Online 1Document28 pagesBRIDGE To INDIA India Solar Handbook 2015 Online 1Nithya Susan VargheseNo ratings yet

- TexttDocument3 pagesTexttjakife8633No ratings yet

- RHB Equity 360° - 13 September 2010 (Emas Kiara, Banks, Mah Sing, SP Setia Technical: TDC, WCT)Document4 pagesRHB Equity 360° - 13 September 2010 (Emas Kiara, Banks, Mah Sing, SP Setia Technical: TDC, WCT)Rhb InvestNo ratings yet

- 1127 Course SharingDocument7 pages1127 Course Sharingshanizam ariffinNo ratings yet

- Byte Case StudyDocument17 pagesByte Case StudyWael_Barakat_3179100% (1)

- Launch Vodafone in Pakistan StrategiesDocument45 pagesLaunch Vodafone in Pakistan StrategiesshNo ratings yet

- 1116 Course SharingDocument8 pages1116 Course Sharingshanizam ariffinNo ratings yet

- Is Malaysia Ready For The Renewable Energy EraDocument7 pagesIs Malaysia Ready For The Renewable Energy EraMr. HNo ratings yet

- Budget 2012-13: Pragmatism Must Dictate: by Abu Yousuf Md. Abdullah, PHDDocument4 pagesBudget 2012-13: Pragmatism Must Dictate: by Abu Yousuf Md. Abdullah, PHDAshfaqul Haq ChowdhuryNo ratings yet

- Entrepreneurship Business PlanDocument35 pagesEntrepreneurship Business PlanUmar FarooqNo ratings yet

- Long Term FinancingDocument15 pagesLong Term FinancingPriyanshu BhattacharyaNo ratings yet

- Improving The Policies of Solar Energy in Pakistan: Current ProgressDocument5 pagesImproving The Policies of Solar Energy in Pakistan: Current ProgressabidNo ratings yet

- ECO720 Global and Regional Economic Development FinalsDocument13 pagesECO720 Global and Regional Economic Development FinalsJohn TanNo ratings yet

- Suzlon - An Investment CaseDocument5 pagesSuzlon - An Investment CaseAbhilasha BansalNo ratings yet

- The India Solar HandbookDocument44 pagesThe India Solar Handbookamasssk22108No ratings yet

- Redwan Afrid Avin - 19104022 - BUS203 - Section 4Document5 pagesRedwan Afrid Avin - 19104022 - BUS203 - Section 4Redwan Afrid AvinNo ratings yet

- 3 A New Singaporean Growth Model Can Energize Emerging AsiaDocument5 pages3 A New Singaporean Growth Model Can Energize Emerging AsiaYudi KhoNo ratings yet

- Solar Energy Au1910330 AasthagalaniDocument15 pagesSolar Energy Au1910330 AasthagalaniAastha GalaniNo ratings yet

- Case of AJL Capital Equities-FinalDocument8 pagesCase of AJL Capital Equities-FinalDavy RoseNo ratings yet

- Singapore Property Weekly Issue 89Document16 pagesSingapore Property Weekly Issue 89Propwise.sgNo ratings yet

- Executive SummaryDocument23 pagesExecutive SummaryZahid Bin IslamNo ratings yet

- Potential Impact of COVID-19 On Indian EconomyDocument7 pagesPotential Impact of COVID-19 On Indian EconomyHarshit Kumar SinghNo ratings yet

- PWC Real Estate 2020Document40 pagesPWC Real Estate 2020jcschiaffino100% (1)

- Next Pot of Gold!Document10 pagesNext Pot of Gold!Aryan SharmaNo ratings yet

- Lu Nam Anh Rough DraftDocument7 pagesLu Nam Anh Rough Draftsvxnv88kynNo ratings yet

- EY Middle East and North Africa Cleantech SurveyDocument24 pagesEY Middle East and North Africa Cleantech SurveylassasaNo ratings yet

- Suzlon AnalysisDocument31 pagesSuzlon AnalysisSushil KumarNo ratings yet

- RHB Equity 360° (Strategy, Market, Plantation, Telecom, Steel, Faber, KPJ, PetGas Technical: DRB-Hicom) - 01/04/2010Document6 pagesRHB Equity 360° (Strategy, Market, Plantation, Telecom, Steel, Faber, KPJ, PetGas Technical: DRB-Hicom) - 01/04/2010Rhb InvestNo ratings yet

- SectoralUpdate 03012014Document13 pagesSectoralUpdate 03012014ashish10mcaNo ratings yet

- Assignment On Telecommunication Industry in BangladeshDocument23 pagesAssignment On Telecommunication Industry in BangladeshMd.Hafizur RahamanNo ratings yet

- Prediction Consensus - News English SpeakingDocument5 pagesPrediction Consensus - News English Speaking노진성No ratings yet

- Market Size: LG PakistanDocument3 pagesMarket Size: LG PakistanAmir AliNo ratings yet

- Business Confidence SaggingDocument7 pagesBusiness Confidence SagginghellonelsonNo ratings yet

- The State of Lagos Housing Market Report TEASER N75000 PERDocument21 pagesThe State of Lagos Housing Market Report TEASER N75000 PEROkewole Olayemi SamuelNo ratings yet

- Solar Facts & Figures - Southeast Asia 2018Document38 pagesSolar Facts & Figures - Southeast Asia 2018TeeBoneNo ratings yet

- Stock MarketDocument7 pagesStock Marketapi-375962513No ratings yet

- Global Wind Report 2010Document72 pagesGlobal Wind Report 2010Uğur ÖzkanNo ratings yet

- China's New Energy Revolution: How the World Super Power is Fostering Economic Development and Sustainable Growth through Thin-Film Solar TechnologyFrom EverandChina's New Energy Revolution: How the World Super Power is Fostering Economic Development and Sustainable Growth through Thin-Film Solar TechnologyNo ratings yet

- Freedom Unleashed: How to Make Malaysia a Tax Free CountryFrom EverandFreedom Unleashed: How to Make Malaysia a Tax Free CountryRating: 5 out of 5 stars5/5 (1)

- Defying the Market (Review and Analysis of the Leebs' Book)From EverandDefying the Market (Review and Analysis of the Leebs' Book)No ratings yet

- Philippines: Energy Sector Assessment, Strategy, and Road MapFrom EverandPhilippines: Energy Sector Assessment, Strategy, and Road MapNo ratings yet

- 234 LK 23 LK 428 G 3 OhDocument3 pages234 LK 23 LK 428 G 3 OhDannyNo ratings yet

- Fae 5 y 4 U 6 J 5 Nrythew 35546Document2 pagesFae 5 y 4 U 6 J 5 Nrythew 35546DannyNo ratings yet

- 234 LK 3 y 53 Het 23 LK 428 G 3 Oh 8759Document4 pages234 LK 3 y 53 Het 23 LK 428 G 3 Oh 8759DannyNo ratings yet

- 234 LK 23 LK 428 G 3 Ohw 2 R 098 y 1 TH 2 GoqDocument3 pages234 LK 23 LK 428 G 3 Ohw 2 R 098 y 1 TH 2 GoqDannyNo ratings yet

- 234 LK 23 LK 428 G 3 Ohi 7 Qef 97Document9 pages234 LK 23 LK 428 G 3 Ohi 7 Qef 97DannyNo ratings yet

- 234 LK 23 LK 428 G 3 Oh 8759Document6 pages234 LK 23 LK 428 G 3 Oh 8759DannyNo ratings yet

- ACG StarterDocument1 pageACG StarterLeo HiterozaNo ratings yet

- Marketing Information SystemDocument3 pagesMarketing Information SystemsanjayNo ratings yet

- Scrap Specifications CircularDocument57 pagesScrap Specifications Circulargiám địnhNo ratings yet

- Devops MCQ PDFDocument6 pagesDevops MCQ PDFSaad Mohamed SaadNo ratings yet

- IBM Power Systems Cloud Security Guide: Protect IT Infrastructure in All LayersDocument220 pagesIBM Power Systems Cloud Security Guide: Protect IT Infrastructure in All Layersbenmagha9904No ratings yet

- Proforma Architect - Owner Agreement: Very Important NotesDocument11 pagesProforma Architect - Owner Agreement: Very Important NotesJean Erika Bermudo BisoñaNo ratings yet

- MKT 005 Module 6 SASDocument5 pagesMKT 005 Module 6 SASconandetic123No ratings yet

- 2014 Elec HD FS CKTruck 100713 ChevroletDocument247 pages2014 Elec HD FS CKTruck 100713 ChevroletREINALDO GONZALEZNo ratings yet

- Emg ManualDocument20 pagesEmg ManualSalih AnwarNo ratings yet

- Aditya Vikram Verma - CVDocument2 pagesAditya Vikram Verma - CVAdityaVikramVermaNo ratings yet

- Fleck SXT Timer: Service ManualDocument24 pagesFleck SXT Timer: Service ManualdracuojiNo ratings yet

- CBME 102 REviewerDocument17 pagesCBME 102 REviewerEilen Joyce BisnarNo ratings yet

- Self-Efficacy Mediated Spiritual Leadership On Citizenship Behavior Towards The Environment of Employees at Harapan Keluarga HospitalDocument7 pagesSelf-Efficacy Mediated Spiritual Leadership On Citizenship Behavior Towards The Environment of Employees at Harapan Keluarga HospitalInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- On Annemarie Mols The Body MultipleDocument4 pagesOn Annemarie Mols The Body MultipleMAGALY GARCIA RINCONNo ratings yet

- Supplemental-Guide GenderQuestWkbkTeensDocument9 pagesSupplemental-Guide GenderQuestWkbkTeensPaula ZuccoloNo ratings yet

- Parametric & Non Parametric TestDocument8 pagesParametric & Non Parametric TestAngelica Alejandro100% (1)

- Competency Enhancing Courses Jan June2023Document2 pagesCompetency Enhancing Courses Jan June2023Yashveer TakooryNo ratings yet

- Visto-Resume 26710306Document1 pageVisto-Resume 26710306api-350663722No ratings yet

- Phenomena of Double RefractionDocument5 pagesPhenomena of Double RefractionMahendra PandaNo ratings yet

- Setting Goals: Throughout This Course You Have Gone Through The Process of Education and Career/Life PlanningDocument4 pagesSetting Goals: Throughout This Course You Have Gone Through The Process of Education and Career/Life PlanningMuhammad AbdullahNo ratings yet

- TRA 02 Lifting of Skid Units During Rig MovesDocument3 pagesTRA 02 Lifting of Skid Units During Rig MovesPirlo PoloNo ratings yet

- Thesis Statement About Business AdministrationDocument4 pagesThesis Statement About Business Administrationokxyghxff100% (2)

- Art Meta-Analyses of Experimental Data in An PDFDocument12 pagesArt Meta-Analyses of Experimental Data in An PDFIonela HoteaNo ratings yet

- Performix™ High Speed Dissolver - Technical DataDocument1 pagePerformix™ High Speed Dissolver - Technical DataNegash JaferNo ratings yet

- Performance TaskDocument6 pagesPerformance TaskPrinces Aliesa Bulanadi100% (1)

- Ashcroft Dial GaugeDocument1 pageAshcroft Dial GaugeReva Astra DiptaNo ratings yet

- Troy-Bilt 019191 PDFDocument34 pagesTroy-Bilt 019191 PDFSteven W. NinichuckNo ratings yet

- Job Shop Scheduling Vs Flow Shop SchedulingDocument11 pagesJob Shop Scheduling Vs Flow Shop SchedulingMatthew MhlongoNo ratings yet

- Docusign: Customer Success Case Study SamplerDocument7 pagesDocusign: Customer Success Case Study Samplerozge100% (1)