Download as doc, pdf, or txt

You might also like

- IT AUDIT Questionnaire (IT Audit)Document10 pagesIT AUDIT Questionnaire (IT Audit)jkpdbnlbsg75% (4)

- Pat English Year 4 Paper 2Document8 pagesPat English Year 4 Paper 2Siti Amalina NadiaNo ratings yet

- BMC of Al Ikhsan SDN BHD PDFDocument16 pagesBMC of Al Ikhsan SDN BHD PDFBranden NgNo ratings yet

- Lake Case StudyDocument3 pagesLake Case StudyVictor. HuamaniNo ratings yet

- Chap 1 - Tutorial QDocument3 pagesChap 1 - Tutorial QHanis ZahiraNo ratings yet

- Ews DG CWSN Result 2021 22Document1,422 pagesEws DG CWSN Result 2021 22Satyam DeyNo ratings yet

- SAAD Question BankDocument21 pagesSAAD Question BankKisyenene JamusiNo ratings yet

- Disruptive Innovation in Dentistry: What It Is and What Could Be NextDocument6 pagesDisruptive Innovation in Dentistry: What It Is and What Could Be NextgneiNo ratings yet

- HCL Ecp TSS Noi 0619 106 PDFDocument10 pagesHCL Ecp TSS Noi 0619 106 PDFtushar jainNo ratings yet

- Final Research ProposalDocument7 pagesFinal Research ProposalPriyashna Vedna GourdealeNo ratings yet

- IT Audit CH 12Document13 pagesIT Audit CH 12Ganessa RolandNo ratings yet

- RDM221 - 1 - 13Document113 pagesRDM221 - 1 - 13Jimson SulitNo ratings yet

- Redwan Ali Research Proposal For ALR FinalDocument11 pagesRedwan Ali Research Proposal For ALR Finalyared girmaNo ratings yet

- Abstrak Pemakalah Setali 2019Document159 pagesAbstrak Pemakalah Setali 2019Jefry AdityaNo ratings yet

- Far Act 9.1Document28 pagesFar Act 9.1Sree Mathi SuntheriNo ratings yet

- Sample Research PROPOSALDocument48 pagesSample Research PROPOSALNUR ELYANA SHAHEERA SAIFUL LIZANNo ratings yet

- CePBFO Guideline FTRDocument18 pagesCePBFO Guideline FTRmiraNo ratings yet

- EconomicsDocument44 pagesEconomicsVishrut ChhajerNo ratings yet

- Bosch LTDDocument50 pagesBosch LTDmanishsngh24No ratings yet

- HBET2303 AssignmentDocument16 pagesHBET2303 AssignmentJamlevisyon JouningNo ratings yet

- Tax Law Assignment 2015 November 29Document5 pagesTax Law Assignment 2015 November 29Samuel NgangaNo ratings yet

- Section A - Group 4 - Distribution ChannelsDocument30 pagesSection A - Group 4 - Distribution ChannelsSasi SarvamNo ratings yet

- Digital RecordkeepingDocument85 pagesDigital Recordkeepingbesar winartoNo ratings yet

- Chapter 1170Document44 pagesChapter 1170MussoorieNo ratings yet

- BAFDocument100 pagesBAFiftikharhayderNo ratings yet

- Personal Profile: Curriculum VitaeDocument3 pagesPersonal Profile: Curriculum Vitaecumar ElmiNo ratings yet

- Inventory Management and JIT Group AssignmentDocument24 pagesInventory Management and JIT Group AssignmenthuleNo ratings yet

- Analisis Pertumbuhan Zakat Pada Aplikasi Zakat Online Dompet DhuafaDocument10 pagesAnalisis Pertumbuhan Zakat Pada Aplikasi Zakat Online Dompet DhuafaNyonyaKimNo ratings yet

- Cuestionario Inglés MLQ.Document19 pagesCuestionario Inglés MLQ.Gabriela DuarteNo ratings yet

- Topic 3 Theoritical Perspective of Policy Decision MakingDocument46 pagesTopic 3 Theoritical Perspective of Policy Decision MakingIzatul ShimaNo ratings yet

- Axiata Company StudyDocument14 pagesAxiata Company StudyluciusNo ratings yet

- 22PGD205 OmDocument5 pages22PGD205 OmRohit KumarNo ratings yet

- HMOB 4022docx MozaidDocument5 pagesHMOB 4022docx MozaidMOZAIDNo ratings yet

- Date: 11 March 2021 MR Rahul Sharma Rze2 Mahavi Enclave New Delhi New Delhi 110045 Delhi Policy No.: 16811926 Mobile No.: Xxxxxx3693Document6 pagesDate: 11 March 2021 MR Rahul Sharma Rze2 Mahavi Enclave New Delhi New Delhi 110045 Delhi Policy No.: 16811926 Mobile No.: Xxxxxx3693Rahul SharmaNo ratings yet

- Group Assignment Acc116Document9 pagesGroup Assignment Acc116Nurul AzlinNo ratings yet

- Kumpulan 5 - Report Case 2 (AP Cars SDN BHD)Document22 pagesKumpulan 5 - Report Case 2 (AP Cars SDN BHD)Hospital RembauNo ratings yet

- Bis Final Exam NotesDocument27 pagesBis Final Exam NotesTEH HUI SHEAN BB21110834No ratings yet

- OPM560 Test AHMR Kedah FinalDocument4 pagesOPM560 Test AHMR Kedah FinalSITI NORADLINA ROSLINo ratings yet

- Recruitment and Selection Processes of "Metlife Bangladesh" Submitted ToDocument23 pagesRecruitment and Selection Processes of "Metlife Bangladesh" Submitted Tofahim shahriyarNo ratings yet

- Group A ProjectDocument34 pagesGroup A ProjectMD.Jebon AhmedNo ratings yet

- New Equivalence Board of Bse Odisha List 11.06.2019Document4 pagesNew Equivalence Board of Bse Odisha List 11.06.2019Dharmen NialNo ratings yet

- The Impact of Brands On Consumer PurchasDocument6 pagesThe Impact of Brands On Consumer PurchasKovai MTNo ratings yet

- Research ReportDocument71 pagesResearch ReportSagar DixitNo ratings yet

- Screenshot 2021-12-27 at 4.06.56 PMDocument48 pagesScreenshot 2021-12-27 at 4.06.56 PMVishnu WadhwaNo ratings yet

- Assignment 4Document14 pagesAssignment 4Nur KarimaNo ratings yet

- AirtelDocument17 pagesAirtelVrinda SethiNo ratings yet

- Case Study of M & E in Sri LankaDocument22 pagesCase Study of M & E in Sri LankaFred Wekesa WafulaNo ratings yet

- EV Hindi Policy-2022 FinalDocument22 pagesEV Hindi Policy-2022 FinalAmrish TrivediNo ratings yet

- Research DraftDocument124 pagesResearch DraftGiano Charl FernandezNo ratings yet

- Marketing MGT Feasibility Study Dec 24,2019Document16 pagesMarketing MGT Feasibility Study Dec 24,2019Worash Engidaw100% (1)

- Final Assignment: Mct1074 Business Intelligence and AnalyticsDocument28 pagesFinal Assignment: Mct1074 Business Intelligence and AnalyticsAhmad Shahir NohNo ratings yet

- SachinRajani FinalReport K235Document58 pagesSachinRajani FinalReport K235Mansi RathiNo ratings yet

- Internship Report 1Document43 pagesInternship Report 1rushda asmatNo ratings yet

- Ari Peskoe Letter To Sen. FrentzDocument2 pagesAri Peskoe Letter To Sen. FrentzMike McFeelyNo ratings yet

- Dharthi Dredging ResumeDocument2 pagesDharthi Dredging ResumeJ Parameswara RaoNo ratings yet

- Shobhit Singh: Male, 26 YearsDocument2 pagesShobhit Singh: Male, 26 YearsZero IndiaNo ratings yet

- Final Edit of Bata InternshipDocument24 pagesFinal Edit of Bata InternshipkumarNo ratings yet

- Major Industrial Belts in IndiaDocument28 pagesMajor Industrial Belts in Indiasubramonian100% (1)

- Akshay MistryDocument3 pagesAkshay MistryLoveleenNo ratings yet

- AL Chemistry I A+ ExamDocument10 pagesAL Chemistry I A+ Examjoker boyNo ratings yet

- Aditi Tiwari - DM21E25 Individual-1Document8 pagesAditi Tiwari - DM21E25 Individual-1Rahul kumarNo ratings yet

- Jasdeep SynopsisDocument8 pagesJasdeep SynopsisNageshwar SinghNo ratings yet

- A Historical Perspective in The Development of Accounting StandardsDocument7 pagesA Historical Perspective in The Development of Accounting StandardsPamela Ledesma SusonNo ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- Far660 - July 2020 Set 1 SolutionDocument8 pagesFar660 - July 2020 Set 1 SolutionHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 SolutionDocument7 pagesFar660 - Special Feb 2020 SolutionHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 QuestionDocument5 pagesFar660 - Special Feb 2020 QuestionHanis ZahiraNo ratings yet

- Far660 - Dec 2019 QuestionDocument5 pagesFar660 - Dec 2019 QuestionHanis ZahiraNo ratings yet

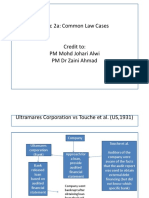

- TOPIC 2a 2 Common Law CasesDocument7 pagesTOPIC 2a 2 Common Law CasesHanis ZahiraNo ratings yet

- CHAPTER 4 International Professional Practice Framework IPPFDocument14 pagesCHAPTER 4 International Professional Practice Framework IPPFHanis ZahiraNo ratings yet

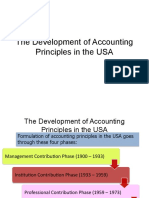

- Development of Accounting Principles in The UsaDocument6 pagesDevelopment of Accounting Principles in The UsaHanis ZahiraNo ratings yet

- TOPIC 6 - Implication of IT On IADocument38 pagesTOPIC 6 - Implication of IT On IAHanis ZahiraNo ratings yet

- CHAPTER 6 Quality Assurance and Improvement ProgramDocument20 pagesCHAPTER 6 Quality Assurance and Improvement ProgramHanis ZahiraNo ratings yet

- TOPIC 2a 1 Auditor S Legal LiabilityDocument56 pagesTOPIC 2a 1 Auditor S Legal LiabilityHanis ZahiraNo ratings yet

- Topic 1 MIA by LawsDocument70 pagesTopic 1 MIA by LawsHanis ZahiraNo ratings yet

- CHAPTER 5 Managing The Internal Audit FunctionDocument31 pagesCHAPTER 5 Managing The Internal Audit FunctionHanis ZahiraNo ratings yet

- CHAPTER 8 Investigation of FraudDocument45 pagesCHAPTER 8 Investigation of FraudHanis ZahiraNo ratings yet

- 02 Chapter 2 - Corporate Governance MechanismDocument19 pages02 Chapter 2 - Corporate Governance MechanismHanis ZahiraNo ratings yet

- 01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceDocument30 pages01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceHanis ZahiraNo ratings yet

- CHAPTER 3 Risk and Control FazDocument22 pagesCHAPTER 3 Risk and Control FazHanis ZahiraNo ratings yet

- CHAPTER 1 Overview of Internal Auditing FazDocument22 pagesCHAPTER 1 Overview of Internal Auditing FazHanis ZahiraNo ratings yet

- QSP Quality and Safety Plan For Railway Civil WorksDocument43 pagesQSP Quality and Safety Plan For Railway Civil Worksvinodshukla25No ratings yet

- ISO-Audit-Reports-27.02.2020-to 28.02.2020Document15 pagesISO-Audit-Reports-27.02.2020-to 28.02.2020Vaibhav SinghNo ratings yet

- Sample Auditor S Report On Financial Statements of A Priv Co ISA 700Document6 pagesSample Auditor S Report On Financial Statements of A Priv Co ISA 700Salvador BrionesNo ratings yet

- SOP 20-005 Sampling InspectionDocument9 pagesSOP 20-005 Sampling InspectionsushmaxNo ratings yet

- Financing Agreement: Credit Number 7161-Zr Grant Number E0850-ZrDocument29 pagesFinancing Agreement: Credit Number 7161-Zr Grant Number E0850-Zrpaul henriNo ratings yet

- Third-party-Risk-Management Joa Eng 0317Document6 pagesThird-party-Risk-Management Joa Eng 0317jmonsa11No ratings yet

- MIS IN UNILEVERIT, Privacy, Security, Supply and Customer Relationship12/10/2012Document20 pagesMIS IN UNILEVERIT, Privacy, Security, Supply and Customer Relationship12/10/2012rahishah13No ratings yet

- DO 062 s2018Document19 pagesDO 062 s2018Glenn FabiculanaNo ratings yet

- Wesfarmers: Risk AssessmentDocument14 pagesWesfarmers: Risk AssessmentSuman BeraNo ratings yet

- SQF Quality Code Ed 8.1Document49 pagesSQF Quality Code Ed 8.1Luis GallegosNo ratings yet

- Topic Outline For Public Accounting and BudgetingDocument8 pagesTopic Outline For Public Accounting and Budgetingsabel sardilla100% (1)

- HSE ResumeDocument13 pagesHSE Resumesathya2040No ratings yet

- TSGR3#8 (99) D66: Agenda Item: Source: TitleDocument4 pagesTSGR3#8 (99) D66: Agenda Item: Source: TitleAhmet SaatNo ratings yet

- SAP Project: Superuser Information Pack (Central Admin)Document19 pagesSAP Project: Superuser Information Pack (Central Admin)Hidayat AliNo ratings yet

- Ch12 Auditing-Theory-12Document16 pagesCh12 Auditing-Theory-12Ara Marie MagnayeNo ratings yet

- Rajagiri Rubber 2014Document74 pagesRajagiri Rubber 2014Anonymous NnVgCXDwNo ratings yet

- Sample Strategic IA PlanDocument34 pagesSample Strategic IA PlanSheyam Selvaraj100% (1)

- Food Safety OfficerDocument5 pagesFood Safety OfficersivaguruaksNo ratings yet

- Audit of IT Governance Based On COBIT 5 Assessments: A Case StudyDocument8 pagesAudit of IT Governance Based On COBIT 5 Assessments: A Case StudyFaisal Fahri FerdiansyahNo ratings yet

- Engender Health Malawi Positions Advertisement AmendedDocument10 pagesEngender Health Malawi Positions Advertisement AmendedJohn Richard KasalikaNo ratings yet

- Chapter - I: 1.2 Objectives of The StudyDocument16 pagesChapter - I: 1.2 Objectives of The StudySugunasugiNo ratings yet

- Chapter 1 - Overview of Government Accounting (Notes)Document6 pagesChapter 1 - Overview of Government Accounting (Notes)Angela Denisse FranciscoNo ratings yet

- Chapter 6 The Search For Evidence ExplainedDocument27 pagesChapter 6 The Search For Evidence ExplainedNathali TjahjadiNo ratings yet

- Mayur Rajendra SonawaneDocument10 pagesMayur Rajendra SonawaneMayur SonawaneNo ratings yet

- Accountant Auditor Financial Analyst in Chicago IL Resume Raj ShahDocument3 pagesAccountant Auditor Financial Analyst in Chicago IL Resume Raj ShahRajShah5No ratings yet

- Full Download PDF of (Ebook PDF) Managing Quality Integrating The Supply Chain 6th All ChapterDocument43 pagesFull Download PDF of (Ebook PDF) Managing Quality Integrating The Supply Chain 6th All Chapterebrstorie100% (5)

- Beximco Annual 2020 21Document116 pagesBeximco Annual 2020 21Abu Sadik Md. NafiNo ratings yet

- Unit 4 VouchingDocument22 pagesUnit 4 VouchingAmit PatelNo ratings yet