Download as docx, pdf, or txt

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Pas 12 Income TaxesDocument4 pagesPas 12 Income TaxesFabrienne Kate Eugenio Liberato100% (1)

- Chapter 4Document37 pagesChapter 4Christine Anne ValdezNo ratings yet

- A INCOME TAXATION Final ExamDocument13 pagesA INCOME TAXATION Final ExamCresel ReposoNo ratings yet

- 01 IntaxDocument5 pages01 IntaxAbigail VergaraNo ratings yet

- Notes Chapter 2 FARDocument5 pagesNotes Chapter 2 FARcpacfa100% (16)

- How To Lower Your TaxesDocument2 pagesHow To Lower Your TaxesPhia CustodioNo ratings yet

- Profits and Gains of Business - JBIMSDocument85 pagesProfits and Gains of Business - JBIMSSwapnil ManeNo ratings yet

- De La Salle Lipa: Intermediate Accounting 3 Income and Expense Items Affecting Deferred TaxesDocument4 pagesDe La Salle Lipa: Intermediate Accounting 3 Income and Expense Items Affecting Deferred TaxesJere Mae MarananNo ratings yet

- "Isolated Activity": Sybbi / Sybaf PGBP Direct Taxation-II Chapter 5:-Profits & Gains of Business or ProfessionDocument5 pages"Isolated Activity": Sybbi / Sybaf PGBP Direct Taxation-II Chapter 5:-Profits & Gains of Business or Professionas2207530No ratings yet

- Deferred Tax Accounting - Lecture NotesDocument6 pagesDeferred Tax Accounting - Lecture Notesmax pNo ratings yet

- Pas 12 Income TaxesDocument3 pagesPas 12 Income TaxesKristalen ArmandoNo ratings yet

- PICPA NO - Corporate Income TaxDocument80 pagesPICPA NO - Corporate Income TaxMerlyn M. Casibang Jr.No ratings yet

- Capital Gains and Losses: Ebook Summary - Chapter 12Document1 pageCapital Gains and Losses: Ebook Summary - Chapter 12arianxxxNo ratings yet

- CHAPTER 13 - Principles of DeductionDocument5 pagesCHAPTER 13 - Principles of DeductionDeviane CalabriaNo ratings yet

- Ind AS 12Document37 pagesInd AS 12Amal P TomyNo ratings yet

- ToA 10 Income Tax StudentDocument4 pagesToA 10 Income Tax Studentlana del reyNo ratings yet

- Financial Accounting and ReportingDocument6 pagesFinancial Accounting and Reportingsinatoyakoto051No ratings yet

- Income TaxesDocument11 pagesIncome TaxesamNo ratings yet

- Deductions On Gross IncomeDocument6 pagesDeductions On Gross IncomeJamaica DavidNo ratings yet

- FARreviewerDocument5 pagesFARreviewerKimNo ratings yet

- Concept of IncomeDocument3 pagesConcept of IncomeNoroNo ratings yet

- Accounting Crash CourseDocument7 pagesAccounting Crash CourseschmooflaNo ratings yet

- Ifrs at A Glance: IAS 12 Income TaxesDocument4 pagesIfrs at A Glance: IAS 12 Income Taxeslina_siscanu6356No ratings yet

- Fabm 2Document8 pagesFabm 2CAYABAN, RISHA MARIE DV.No ratings yet

- Capital Gains Tax (Ampongan)Document11 pagesCapital Gains Tax (Ampongan)didit.canonNo ratings yet

- Income, Tax Treatment and Mode of Filing 2020Document2 pagesIncome, Tax Treatment and Mode of Filing 2020francis dungcaNo ratings yet

- Vat & OptDocument14 pagesVat & OptDaphnie BoloNo ratings yet

- Zyna Taxation Reviewer PDFDocument8 pagesZyna Taxation Reviewer PDFShekinah MonrealNo ratings yet

- Business Income &expensesDocument6 pagesBusiness Income &expensesNurain Nabilah ZakariyaNo ratings yet

- International Tax: Dominican Republic Highlights 2019Document4 pagesInternational Tax: Dominican Republic Highlights 2019Juan Enrique GuilianiNo ratings yet

- P&R AnalysisDocument29 pagesP&R Analysiscontact.xinanneNo ratings yet

- Chap 13 - Income From BusinessDocument14 pagesChap 13 - Income From BusinessMuhammad Saad UmarNo ratings yet

- Title I. General Provisions: Taxation I - Income TaxationDocument43 pagesTitle I. General Provisions: Taxation I - Income TaxationGe MendozaNo ratings yet

- Taxation I EditedDocument43 pagesTaxation I EditedJayzel LaureanoNo ratings yet

- Percentage Tax in The PhilippinesDocument3 pagesPercentage Tax in The PhilippinesfrazieNo ratings yet

- Chapter 9Document3 pagesChapter 9kjudani1207No ratings yet

- Session 1 - Gross Income - Inclusions and ExclusionsDocument13 pagesSession 1 - Gross Income - Inclusions and ExclusionsABBIE GRACE DELA CRUZNo ratings yet

- MSA 2 - Taxation NotesDocument19 pagesMSA 2 - Taxation NotesadilfarooqaNo ratings yet

- Ind As 12: Income Taxes: Current Tax Temporary Difference: TaxableDocument2 pagesInd As 12: Income Taxes: Current Tax Temporary Difference: Taxablechandrakumar k pNo ratings yet

- 113 Module 1 - INTODUCTORY NOTES AND TRADE PAYABLES AND ACCRUED LIABILITIESDocument4 pages113 Module 1 - INTODUCTORY NOTES AND TRADE PAYABLES AND ACCRUED LIABILITIESRay SanzeninNo ratings yet

- PAS 12 INCOME TAXES Cont With ProbsDocument8 pagesPAS 12 INCOME TAXES Cont With ProbsFabrienne Kate Eugenio Liberato100% (1)

- CHAPTER 9 Regular Income TaxDocument8 pagesCHAPTER 9 Regular Income TaxAlyssa BerangberangNo ratings yet

- Jpia-Hau: Business and Transfer TaxationDocument12 pagesJpia-Hau: Business and Transfer Taxationronniel tiglaoNo ratings yet

- BSTX Reviewer (Midterm)Document7 pagesBSTX Reviewer (Midterm)alaine daphneNo ratings yet

- A. Intax NotesDocument13 pagesA. Intax NotesIssy BNo ratings yet

- Fabm ReviewerDocument5 pagesFabm ReviewerHeaven Krysthel Bless R. SacsacNo ratings yet

- Allowable Deductions (Taxation Review)Document82 pagesAllowable Deductions (Taxation Review)Prie DitucalanNo ratings yet

- Tax.3301-3 Accounting Methods and PeriodsDocument2 pagesTax.3301-3 Accounting Methods and PeriodsDena Heart OrenioNo ratings yet

- Notes - Output VatDocument4 pagesNotes - Output VatSunny DaeNo ratings yet

- Notes in ReceivablesDocument9 pagesNotes in ReceivablesAnj HwanNo ratings yet

- (ACCCOB2) Chapters 3-5 Receivables, Investments, InventoryDocument11 pages(ACCCOB2) Chapters 3-5 Receivables, Investments, InventoryMichaella PurgananNo ratings yet

- PGBP - Final NSDocument32 pagesPGBP - Final NSblacklyli31No ratings yet

- Reporting Interview GuideDocument7 pagesReporting Interview Guideidrees bajjarNo ratings yet

- ACTAX-3153-N002-Intro To Income Taxation PDFDocument5 pagesACTAX-3153-N002-Intro To Income Taxation PDFJwyneth Royce DenolanNo ratings yet

- LU6 Capital AllowancesDocument31 pagesLU6 Capital AllowancesabasoomarishaaqNo ratings yet

- Gross Income Deductions - Lecture Handout PDFDocument4 pagesGross Income Deductions - Lecture Handout PDFKarl RendonNo ratings yet

- TAX 667 Topic 8 Tax Planning For CompanyDocument63 pagesTAX 667 Topic 8 Tax Planning For Companyzarif nezukoNo ratings yet

- Chapter 11 TaxDocument11 pagesChapter 11 Taxkp_popinjNo ratings yet

- Deccan Chronicle Holdings Limited No. 5th Floor, B.M.T.C Commercial Comples, 80ft Road, Koramangala. Benguluru - 560 095Document1 pageDeccan Chronicle Holdings Limited No. 5th Floor, B.M.T.C Commercial Comples, 80ft Road, Koramangala. Benguluru - 560 095David PenNo ratings yet

- Monthly Salary SlipDocument13 pagesMonthly Salary Slipsridhar sridharNo ratings yet

- Income Tax Statement For The Financial Year 2022-23 of K.sasiDHAR On 09-01-2023Document8 pagesIncome Tax Statement For The Financial Year 2022-23 of K.sasiDHAR On 09-01-2023Katari SasidharNo ratings yet

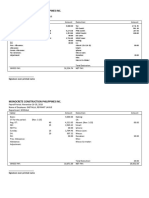

- Monocrete Construction Philippines Inc.: - Signature Over Printed NameDocument1 pageMonocrete Construction Philippines Inc.: - Signature Over Printed NameCherish Gale B. BoloNo ratings yet

- Ws 2Document7 pagesWs 2Lê Hồng PhướcNo ratings yet

- Income Tax Payment Challan: PSID #: 21114984Document1 pageIncome Tax Payment Challan: PSID #: 21114984Zia Sultan AwanNo ratings yet

- 2316 Sep 2021 ENCS - Final - CorrectedDocument1 page2316 Sep 2021 ENCS - Final - Correctedchelleabogado27No ratings yet

- India Tile Gallery 404 29-Apr-23 Immrdiate 28-Apr-23: CGST SGST Round OffDocument1 pageIndia Tile Gallery 404 29-Apr-23 Immrdiate 28-Apr-23: CGST SGST Round OffManya BhosaleNo ratings yet

- RMC No 85-2017Document2 pagesRMC No 85-2017Karen Balisacan Segundo Ruiz100% (1)

- 3-TAX PLANNING (Planning Your Tax Strategy)Document9 pages3-TAX PLANNING (Planning Your Tax Strategy)Nur DinieNo ratings yet

- Account Symphony TheatreDocument1,821 pagesAccount Symphony Theatresuryagc0% (1)

- TF 00000049Document2 pagesTF 00000049Anonymous Wzyn7DB2kLNo ratings yet

- Income Tax Fundamentals 2015 33rd Edition Whittenburg Test BankDocument31 pagesIncome Tax Fundamentals 2015 33rd Edition Whittenburg Test Bankrefineternpho4100% (27)

- Vendor Verification FormDocument1 pageVendor Verification FormMichael L.No ratings yet

- Yadadri Bhuvanagiri - Pochampally - MPPS Danthur - 36200901402 - P200901402 - 20231109 - 000007 - Green Chalk BoardsDocument2 pagesYadadri Bhuvanagiri - Pochampally - MPPS Danthur - 36200901402 - P200901402 - 20231109 - 000007 - Green Chalk BoardsdurgaprasadNo ratings yet

- MI - SL - 23!24!141-Sales - Invoice-Jaipur Smile Dental Clinic DR Bhaskar GuptaDocument1 pageMI - SL - 23!24!141-Sales - Invoice-Jaipur Smile Dental Clinic DR Bhaskar GuptaBhaskar GuptaNo ratings yet

- Tax Invoice Nxg-20220029: Nextgen BroadbandDocument1 pageTax Invoice Nxg-20220029: Nextgen BroadbandKaranNo ratings yet

- AARPW1885E - Show Cause Notice For Proceedings Us 148A - 1041373372 (1) - 23032022Document2 pagesAARPW1885E - Show Cause Notice For Proceedings Us 148A - 1041373372 (1) - 23032022Sukalp WarhekarNo ratings yet

- Income Chargeable Under The Head Income From Other Sources - Attempt ReviewDocument4 pagesIncome Chargeable Under The Head Income From Other Sources - Attempt Reviewaarishak786No ratings yet

- Annex F RR 11-2018Document1 pageAnnex F RR 11-2018ynid wageNo ratings yet

- Naqsh Automation - VFDDocument1 pageNaqsh Automation - VFDKrishNo ratings yet

- GST CHALLAnDocument1 pageGST CHALLAnVibhav AnasaneNo ratings yet

- Deal Sheet - Furio7hd CBC - DR Milk Food ProductDocument6 pagesDeal Sheet - Furio7hd CBC - DR Milk Food ProductRahul BhagatNo ratings yet

- F3 Mock Answers 201603Document3 pagesF3 Mock Answers 201603getcultured69No ratings yet

- BIR Books of Accounts Registration SlipDocument2 pagesBIR Books of Accounts Registration SlipAngieLlantoCuriosoNo ratings yet

- Esso Standard Eastern vs. CommissionerDocument2 pagesEsso Standard Eastern vs. CommissionerlexxNo ratings yet

- Amit ConstDocument1 pageAmit Constks4427552No ratings yet

- Anurag Revised Salary Breakup FY23-24Document2 pagesAnurag Revised Salary Breakup FY23-24SathyanarayanaAmbatiNo ratings yet

- Invoice Copy 1Document1 pageInvoice Copy 1vrrav7694No ratings yet