Download as pdf or txt

You might also like

- In The Kitchen - BB Major - MN0259662Document8 pagesIn The Kitchen - BB Major - MN0259662lieke100% (2)

- Method Statement Installation of Duct BankDocument63 pagesMethod Statement Installation of Duct BankGerry Dwi Putra100% (2)

- BIR RULING NO. 1102-18: Tata Consultancy Services (Philippines), IncDocument3 pagesBIR RULING NO. 1102-18: Tata Consultancy Services (Philippines), IncKathleen Leynes100% (1)

- Bir Ruling No. 1243-18 - JvsDocument3 pagesBir Ruling No. 1243-18 - Jvsjohn allen MarillaNo ratings yet

- Complaint Daniel L Gelb Plaza I Inc Tom Petters BankruptcyDocument24 pagesComplaint Daniel L Gelb Plaza I Inc Tom Petters BankruptcyCamdenCanary100% (1)

- Negligence NotesDocument6 pagesNegligence Noteshouselanta75% (4)

- 2007 Central - Country - Estate - Inc.20220602 11 1vb3vtdDocument3 pages2007 Central - Country - Estate - Inc.20220602 11 1vb3vtdRen Mar CruzNo ratings yet

- Bir Ruling No. JV-187-21Document4 pagesBir Ruling No. JV-187-21Ren Mar CruzNo ratings yet

- 2006 BIR - Ruling - DA 432 06 - 20210505 13 1t6tcx6Document3 pages2006 BIR - Ruling - DA 432 06 - 20210505 13 1t6tcx6Boss NikNo ratings yet

- 2009 CKL - Real - Estate - Corp.20220525 12 1gi6gubDocument3 pages2009 CKL - Real - Estate - Corp.20220525 12 1gi6gubRen Mar CruzNo ratings yet

- Bir Ruling Da C 296 727 09Document3 pagesBir Ruling Da C 296 727 09doraemoanNo ratings yet

- 5701-1991-Conveyance of The Real Property by The20210505-12-1o05w8wDocument2 pages5701-1991-Conveyance of The Real Property by The20210505-12-1o05w8wCarlo AlfonsoNo ratings yet

- COCOSDE Legal Basis of Condominiums and Condominium Plan by LEE, Elixabeth S. (Leeleebeth)Document5 pagesCOCOSDE Legal Basis of Condominiums and Condominium Plan by LEE, Elixabeth S. (Leeleebeth)ELIXABETH LEENo ratings yet

- 1999 BIR - Ruling - DA 087 99 - 20210505 13 16oil1yDocument2 pages1999 BIR - Ruling - DA 087 99 - 20210505 13 16oil1yJM CBNo ratings yet

- 2008-BIR Ruling (DA - C-182 559-08)Document8 pages2008-BIR Ruling (DA - C-182 559-08)Jay MirandaNo ratings yet

- LB DST Deposit For Future Stock SubscriptionDocument3 pagesLB DST Deposit For Future Stock SubscriptionVence EugalcaNo ratings yet

- Mantto Prev. CavDocument9 pagesMantto Prev. CavKaren Daniela AnayaNo ratings yet

- BIR RulingDocument3 pagesBIR RulingyakyakxxNo ratings yet

- ITAD RULING NO. 009-03 Dated January 16, 2003Document4 pagesITAD RULING NO. 009-03 Dated January 16, 2003Kriszan ManiponNo ratings yet

- Bir Ruling Da JV 039 379 078Document5 pagesBir Ruling Da JV 039 379 078Alfred Hernandez CampañanoNo ratings yet

- Sample PMS Terms and ConditionsDocument12 pagesSample PMS Terms and ConditionsJosh Qc OngNo ratings yet

- 2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmDocument4 pages2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmrian.lee.b.tiangcoNo ratings yet

- LVM Const. v. F.T. SanchezDocument6 pagesLVM Const. v. F.T. SanchezJm BrjNo ratings yet

- BIR Ruling No. 039-97 Dated 03april1997 (STT, No Transfer of Beneficial Ownership)Document3 pagesBIR Ruling No. 039-97 Dated 03april1997 (STT, No Transfer of Beneficial Ownership)Hailin QuintosNo ratings yet

- Post Qua Report ARFF San JoseDocument5 pagesPost Qua Report ARFF San JoseKim Patrick VictoriaNo ratings yet

- Itad Bir Ruling No. 328-12: September 3, 2012 September 3, 2012Document3 pagesItad Bir Ruling No. 328-12: September 3, 2012 September 3, 2012nathalie velasquezNo ratings yet

- Civil Service Commission v. BerayDocument14 pagesCivil Service Commission v. Beraysharief abantasNo ratings yet

- G & W Architects, Engineers and Project Consultants Co. v. Commissioner of Internal Revenue, C.T.A. Case No. 8604, (August 16, 2016) PDFDocument20 pagesG & W Architects, Engineers and Project Consultants Co. v. Commissioner of Internal Revenue, C.T.A. Case No. 8604, (August 16, 2016) PDFKriszan ManiponNo ratings yet

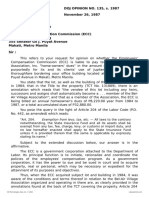

- DOJ Opinion No. 135 S. 1987Document2 pagesDOJ Opinion No. 135 S. 1987Dione Klarisse GuevaraNo ratings yet

- Philex Mining Corporation v. CIR, 551 SCRA 428, 16 April 2008Document11 pagesPhilex Mining Corporation v. CIR, 551 SCRA 428, 16 April 2008RPSA CPANo ratings yet

- DMCIHI - 021 Declaration of Cash Dividends - Final - April 4Document13 pagesDMCIHI - 021 Declaration of Cash Dividends - Final - April 4counsellorsNo ratings yet

- 037-16 Bir Ruling 191086-2016-BIR - RULING - NO. - 037-16Document3 pages037-16 Bir Ruling 191086-2016-BIR - RULING - NO. - 037-16KC AtinonNo ratings yet

- Da 404 05Document4 pagesDa 404 05fatmaaleahNo ratings yet

- For The Year 2021 Non-Stock Corporation: Alternate Mobile NumberDocument6 pagesFor The Year 2021 Non-Stock Corporation: Alternate Mobile NumberJon Carlo CastronuevoNo ratings yet

- 8 Medina Vs City of Baguio 1952Document3 pages8 Medina Vs City of Baguio 1952SDN HelplineNo ratings yet

- BIR Ruling ECCP 068-08Document4 pagesBIR Ruling ECCP 068-08Kendra Miranda LorinNo ratings yet

- Post Qua Report Tower San JoseDocument5 pagesPost Qua Report Tower San JoseKim Patrick VictoriaNo ratings yet

- Authorizing Resolution of IDA September 11, 2019 (PILOT Amendment) (Nut Brown Realty, LLC) (4841-0629-3667 3)Document5 pagesAuthorizing Resolution of IDA September 11, 2019 (PILOT Amendment) (Nut Brown Realty, LLC) (4841-0629-3667 3)Kelsey O'ConnorNo ratings yet

- BIR Ruling No 455-07Document7 pagesBIR Ruling No 455-07Peggy SalazarNo ratings yet

- 3-2021-51109 - Certificate of Registration (New Law New Rules) - B-2022-43740Document5 pages3-2021-51109 - Certificate of Registration (New Law New Rules) - B-2022-43740JimBeeNo ratings yet

- Bir Ruling Da 108 07Document9 pagesBir Ruling Da 108 07Ylmir_1989No ratings yet

- BIR - Ruling DA-263-00 (20 June 2000)Document2 pagesBIR - Ruling DA-263-00 (20 June 2000)josephine.t.ycongNo ratings yet

- First Balfour, Inc.-MRAIL, Inc. Joint VentureDocument4 pagesFirst Balfour, Inc.-MRAIL, Inc. Joint VentureVince Lupango (imistervince)No ratings yet

- Bir Ruling No. 812-18Document1 pageBir Ruling No. 812-18Godfrey TejadaNo ratings yet

- 2022 Taisei DMCI - Joint - Venture20220922 12 13fnp5dDocument4 pages2022 Taisei DMCI - Joint - Venture20220922 12 13fnp5dVince Lupango (imistervince)No ratings yet

- For The Year Ended December 31, 2021 With Comparative Figures For December 31, 2020Document8 pagesFor The Year Ended December 31, 2021 With Comparative Figures For December 31, 2020WenjunNo ratings yet

- BIR Ruling DA-143-06Document4 pagesBIR Ruling DA-143-06joefieNo ratings yet

- Lowe Ruling (BIR Ruling (DA - (C-283) 705-09)Document3 pagesLowe Ruling (BIR Ruling (DA - (C-283) 705-09)Kriszan ManiponNo ratings yet

- Dalisay v. SSSDocument23 pagesDalisay v. SSSCaryl EstradaNo ratings yet

- BIR Ruling No. 123-2018Document3 pagesBIR Ruling No. 123-2018AizaNo ratings yet

- Philex Mining Corp Vs CirDocument8 pagesPhilex Mining Corp Vs CirIrish Joi TapalesNo ratings yet

- Post Qua Report ARFF PlaridelDocument5 pagesPost Qua Report ARFF PlaridelKim Patrick VictoriaNo ratings yet

- BIR RULING (DA-203-06) : April 3, 2006Document2 pagesBIR RULING (DA-203-06) : April 3, 2006Richard100% (1)

- CHW Contract 2020Document12 pagesCHW Contract 2020Zkarea BashtaweNo ratings yet

- 038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9Document4 pages038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9KC AtinonNo ratings yet

- SEC Opinion (November 16, 1982) Atty. Leonen R. GutierrezDocument3 pagesSEC Opinion (November 16, 1982) Atty. Leonen R. GutierrezAlyssa Marie MartinezNo ratings yet

- Revenue Memorandum Circular No. 13-85: SubjectDocument4 pagesRevenue Memorandum Circular No. 13-85: SubjectAemie JordanNo ratings yet

- BIR Ruling (DA-455-07) August 17, 2007Document11 pagesBIR Ruling (DA-455-07) August 17, 2007Raiya AngelaNo ratings yet

- RMC 55-2010Document0 pagesRMC 55-2010Peggy SalazarNo ratings yet

- Third Division: DecisionDocument15 pagesThird Division: DecisionApril IsidroNo ratings yet

- 01 Jul 2023 - 03 Jul 2026 (AAAA)Document2 pages01 Jul 2023 - 03 Jul 2026 (AAAA)kriforbizNo ratings yet

- Guaranty CasesDocument148 pagesGuaranty CasesJoanne LontokNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- SPA Sample Pre-TrialDocument2 pagesSPA Sample Pre-TrialAlfred Hernandez CampañanoNo ratings yet

- Authorization Letter IBP MakatiDocument1 pageAuthorization Letter IBP MakatiAlfred Hernandez CampañanoNo ratings yet

- Certification NotaryDocument1 pageCertification NotaryAlfred Hernandez CampañanoNo ratings yet

- Affidavit of Loss - AhcDocument1 pageAffidavit of Loss - AhcAlfred Hernandez CampañanoNo ratings yet

- AR Moi2Document1 pageAR Moi2Alfred Hernandez CampañanoNo ratings yet

- QuitclaimDocument2 pagesQuitclaimAlfred Hernandez CampañanoNo ratings yet

- Bir Ruling Da JV 039 379 078Document5 pagesBir Ruling Da JV 039 379 078Alfred Hernandez CampañanoNo ratings yet

- JCC Decision - Complaints Against Parker J - 11 June 2020 - FinalDocument17 pagesJCC Decision - Complaints Against Parker J - 11 June 2020 - Finaljillian100% (1)

- Module 4 - Part1Document10 pagesModule 4 - Part1Bea Mae AQUINONo ratings yet

- Bar Exam Tips and Secrets - Atty. MortelDocument4 pagesBar Exam Tips and Secrets - Atty. MortelKaren HaleyNo ratings yet

- Omnibus - TintinDocument1 pageOmnibus - TintinJules Arc CastronuevoNo ratings yet

- Futures Rep Motion by Takata Re Roger FrankelDocument13 pagesFutures Rep Motion by Takata Re Roger FrankelKirk HartleyNo ratings yet

- Fatca and Real Estate Infrastructure FundsDocument4 pagesFatca and Real Estate Infrastructure FundsJustine991No ratings yet

- Equitable Insurance vs. Transmodal InternationalDocument2 pagesEquitable Insurance vs. Transmodal InternationalJohn Mark RevillaNo ratings yet

- Bacsin v. WahimanDocument5 pagesBacsin v. WahimanChriscelle Ann PimentelNo ratings yet

- The Contradictions of LibertarianismDocument18 pagesThe Contradictions of LibertarianismLeandro Domiciano100% (1)

- 7.20.22 Jordan Grassley Letter To DOJDocument5 pages7.20.22 Jordan Grassley Letter To DOJFox News0% (1)

- OCRPfizer 1 RedactedDocument46 pagesOCRPfizer 1 RedactedJamie WhiteNo ratings yet

- Pinellas Deputy George Moffet Jr. Plea DUI To Reckless DrivingDocument2 pagesPinellas Deputy George Moffet Jr. Plea DUI To Reckless DrivingJames McLynasNo ratings yet

- Bates V Post Office Claimants' Appendix of AuthoritiesDocument93 pagesBates V Post Office Claimants' Appendix of AuthoritiesNick WallisNo ratings yet

- The Memoirs Elpidio QuirinoDocument137 pagesThe Memoirs Elpidio QuirinoAdrian Asi0% (1)

- Introduction To LawDocument13 pagesIntroduction To LawWISDOM-INGOODFAITHNo ratings yet

- Pesigan v. Angeles, 129 SCRA 174 (1984)Document4 pagesPesigan v. Angeles, 129 SCRA 174 (1984)Hann Faye BabaelNo ratings yet

- Republic of The Philippines, Petitioner, vs. Jennifer B. CAGANDAHAN, RespondentDocument78 pagesRepublic of The Philippines, Petitioner, vs. Jennifer B. CAGANDAHAN, RespondentCedrick Contado Susi BocoNo ratings yet

- Patnode Unlimited Stalking OrderDocument81 pagesPatnode Unlimited Stalking OrderWilliam N. GriggNo ratings yet

- UST Faculty Union v. BitonioDocument5 pagesUST Faculty Union v. BitonioEmir Mendoza100% (1)

- Cknowledgement: SOURAV AGARWAL, Research Assistant in Law, Indian Institute of Legal Studies, For HisDocument19 pagesCknowledgement: SOURAV AGARWAL, Research Assistant in Law, Indian Institute of Legal Studies, For HisArkaprava BhowmikNo ratings yet

- CTA EB Case No. 250 and 255Document25 pagesCTA EB Case No. 250 and 255trina tsai100% (1)

- Rongitsch V Diversified Adjustment Service Inc Civil Cover SheetDocument1 pageRongitsch V Diversified Adjustment Service Inc Civil Cover SheetghostgripNo ratings yet

- Heirs of Jose Lim Vs Juliet Villa Lim Case DigestDocument1 pageHeirs of Jose Lim Vs Juliet Villa Lim Case DigestNovi Mari NobleNo ratings yet

- Facts of The Case:: (G.R. No. 32329. March 23, 1929.) in Re Luis B. Tagorda Duran & Lim For RespondentDocument2 pagesFacts of The Case:: (G.R. No. 32329. March 23, 1929.) in Re Luis B. Tagorda Duran & Lim For RespondentCherry BepitelNo ratings yet

- PSA 53 - Information Note On Private InvestigatorsDocument2 pagesPSA 53 - Information Note On Private Investigatorssimon martin ryderNo ratings yet

- Position Paper Final DraftDocument13 pagesPosition Paper Final DraftAshley Kate Patalinjug100% (1)

- 13263-Article Text-56700-1-10-20150221Document12 pages13263-Article Text-56700-1-10-20150221Lazarus Kadett NdivayeleNo ratings yet