Download as xlsx, pdf, or txt

You might also like

- Etextbook PDF For Financial Management Theory Practice 15th by EugeneDocument62 pagesEtextbook PDF For Financial Management Theory Practice 15th by Eugenekenneth.mccrary981100% (46)

- Spiceland SM ch11 PDFDocument79 pagesSpiceland SM ch11 PDFmas aziz100% (3)

- By The Sea Biscuit Company - Case Analysis - Group 6 - Section G - PGDM 1Document12 pagesBy The Sea Biscuit Company - Case Analysis - Group 6 - Section G - PGDM 1Pranav Dev SinghNo ratings yet

- Charmingly Personally YoursDocument8 pagesCharmingly Personally YoursRica PresbiteroNo ratings yet

- Workshop 2 Qs As Introduction To A FDocument18 pagesWorkshop 2 Qs As Introduction To A FYeoh Tze ShinNo ratings yet

- Spring Strawberry Salad With ChickenDocument3 pagesSpring Strawberry Salad With Chickenkaku0% (1)

- FINAC1 Problems Solutions 1Document81 pagesFINAC1 Problems Solutions 1Aiziel Orense60% (5)

- WorldCom CaseDocument6 pagesWorldCom CaseBella Eve100% (1)

- Costs of Destroyed ProductDocument15 pagesCosts of Destroyed ProductMae TomeldenNo ratings yet

- Sol ch16Document12 pagesSol ch16Mae CruzNo ratings yet

- 3341 Chapter 16 ProblemsDocument11 pages3341 Chapter 16 ProblemsGrace Love Yzyry LuNo ratings yet

- ACCT3203 Week 3 Tutorial Questions Joint Products S2 2022: Product Separable Costs Sales ValueDocument7 pagesACCT3203 Week 3 Tutorial Questions Joint Products S2 2022: Product Separable Costs Sales ValueJingwen YangNo ratings yet

- EXERCICE Cost Accounting 16-16Document3 pagesEXERCICE Cost Accounting 16-16Amanda VeronikaNo ratings yet

- Module 9 Problems - MrnakDocument9 pagesModule 9 Problems - MrnakJenny MrnakNo ratings yet

- ACCT303 Chapter 16Document40 pagesACCT303 Chapter 16Cừu Ngây NgôNo ratings yet

- Production and Operation Management-PARDUCHO, NICOLE S.A-Course Requirement 2Document11 pagesProduction and Operation Management-PARDUCHO, NICOLE S.A-Course Requirement 2NicoleParduchoNo ratings yet

- Joint Products & by Products - 2440011362 - Rogger SeptryaDocument2 pagesJoint Products & by Products - 2440011362 - Rogger SeptryaRogger SeptryaNo ratings yet

- UnitronDocument9 pagesUnitronIvan Naufal PriadyNo ratings yet

- CVPDocument9 pagesCVPClei UbandoNo ratings yet

- This Template Is Not Capable of Detailed Financial AnalysisDocument35 pagesThis Template Is Not Capable of Detailed Financial AnalysisAlexNo ratings yet

- Sample Fryer Rabbit Budget PDFDocument2 pagesSample Fryer Rabbit Budget PDFGrace NacionalNo ratings yet

- Asset Turnover Sales Asset Sales Birr 160,000Document3 pagesAsset Turnover Sales Asset Sales Birr 160,000Abdi Z leaderNo ratings yet

- BA 117 SolutionsDocument19 pagesBA 117 SolutionsAlaine Milka GosycoNo ratings yet

- Muhammad Nabil Faid - Kelompok 1 - Latihan Soal AKMENDocument11 pagesMuhammad Nabil Faid - Kelompok 1 - Latihan Soal AKMENdcwd9yryjhNo ratings yet

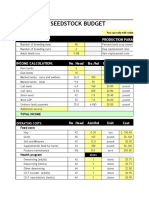

- 2016 Sheep Seedstock Budget: Annual LambingDocument8 pages2016 Sheep Seedstock Budget: Annual LambingGeros dienosNo ratings yet

- Quiz 2 Managerial AccountingDocument24 pagesQuiz 2 Managerial Accountingmaha13aljasmiNo ratings yet

- Case 5 Ans - Charmingly YoursDocument4 pagesCase 5 Ans - Charmingly YoursVaness Grace Aniban100% (4)

- OjoylanJenny - Charmingly (Case#5)Document5 pagesOjoylanJenny - Charmingly (Case#5)Jenny Ojoylan100% (1)

- ALMT ConsomerDocument2 pagesALMT Consomersbaids35No ratings yet

- Constructing A Downtown Parking Lot in DraperDocument7 pagesConstructing A Downtown Parking Lot in DraperWater MelonNo ratings yet

- Sample Dairy Beef BudgetDocument2 pagesSample Dairy Beef BudgetUniversity of Bohol Professional StudiesNo ratings yet

- AdministracionDocument49 pagesAdministracionLuis MonteroNo ratings yet

- Class Case 6 - Charmingly, Personalli, YoursDocument5 pagesClass Case 6 - Charmingly, Personalli, Yours9ry5gsghybNo ratings yet

- 2016 Wool Sheep Enterprise Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentDocument19 pages2016 Wool Sheep Enterprise Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentGeros dienosNo ratings yet

- Solution Guide - Accounting For Labor CostDocument4 pagesSolution Guide - Accounting For Labor CostMirasolNo ratings yet

- Certificate in Accounting Level 2/series 3-2009Document14 pagesCertificate in Accounting Level 2/series 3-2009Hein Linn Kyaw100% (1)

- Expenses: Event Budget Muffin Top Beside Knutsford ExpressDocument2 pagesExpenses: Event Budget Muffin Top Beside Knutsford ExpressHjort HenryNo ratings yet

- Coconut-Farm Plan and BudgetDocument1 pageCoconut-Farm Plan and Budgetmarkgil199080% (5)

- Pasicolan, Mark Joshua BSA 3206: Absorption CostingDocument6 pagesPasicolan, Mark Joshua BSA 3206: Absorption CostingMark Joshua PasicolanNo ratings yet

- Esoft BBDocument1 pageEsoft BBDulanja OmeshNo ratings yet

- Dhaka University of Engineering & Technology: Course Title: Course NoDocument7 pagesDhaka University of Engineering & Technology: Course Title: Course NoUnjila PromiNo ratings yet

- Financial Plan - JanaDocument4 pagesFinancial Plan - JanajemmieNo ratings yet

- Unitron - Teuku AldefaDocument2 pagesUnitron - Teuku AldefaTeuku AldefaNo ratings yet

- Target - 320+87+114 (521) /2 261Document4 pagesTarget - 320+87+114 (521) /2 261sneha patelNo ratings yet

- RD FinancialDocument42 pagesRD FinancialAmranul HaqueNo ratings yet

- CostAcc CaseCh06 ADocument3 pagesCostAcc CaseCh06 ANhư TrầnNo ratings yet

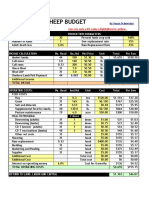

- 2013 Sample Sheep Budget: Annual LambingDocument10 pages2013 Sample Sheep Budget: Annual LambingGeros dienosNo ratings yet

- Direct Marketing Analysis: Gross Margin Per Unit Direct Mail Cost Per UnitDocument4 pagesDirect Marketing Analysis: Gross Margin Per Unit Direct Mail Cost Per UnitiPakistanNo ratings yet

- Joint Products & by Products: Solutions To Assignment ProblemsDocument5 pagesJoint Products & by Products: Solutions To Assignment ProblemsXNo ratings yet

- Sarwanam Threater Balance SheetDocument3 pagesSarwanam Threater Balance SheetsiddhaNo ratings yet

- 1256 ArruejoDocument4 pages1256 ArruejoTitania ErzaNo ratings yet

- Eurl Aman Eclairage - 2024 - 0040Document1 pageEurl Aman Eclairage - 2024 - 0040Kamelia AISSANINo ratings yet

- Profit Rate and Return On Capital Employed: Moh. Ihya' UlumuddinDocument11 pagesProfit Rate and Return On Capital Employed: Moh. Ihya' UlumuddinKKM 37 2023No ratings yet

- CurrentDocument1 pageCurrentasifhasan.jsr2910No ratings yet

- Budget For 100 Conventional BroilersDocument3 pagesBudget For 100 Conventional BroilersMary Jessah LumbabNo ratings yet

- Function 28 August 2010Document7 pagesFunction 28 August 2010Deighton ShimNo ratings yet

- Product: Chocolate Cupcakes Yield:: Costing 1Document8 pagesProduct: Chocolate Cupcakes Yield:: Costing 1Allysa Joyce Regoso PunoNo ratings yet

- 1 Minimum Price Per ShortsDocument5 pages1 Minimum Price Per Shortsboerd77No ratings yet

- BROILERSDocument2 pagesBROILERSthatolicious49No ratings yet

- Stock Details - LM GorceDocument3 pagesStock Details - LM Gorcekavithma3085No ratings yet

- Production ExpensesDocument1 pageProduction ExpensesmercyinifielateNo ratings yet

- MMZG533 Manufacturing Planning & Control: Monkey Business AssignmentDocument17 pagesMMZG533 Manufacturing Planning & Control: Monkey Business AssignmentnaveenNo ratings yet

- Healthy Bread DelightDocument11 pagesHealthy Bread DelightSetty HakeemaNo ratings yet

- ASM Product Opportunity Spreadsheet2Document48 pagesASM Product Opportunity Spreadsheet2Yash SNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Topic 8 Receivable Financing Rev Students 653Document39 pagesTopic 8 Receivable Financing Rev Students 653Nemalai VitalNo ratings yet

- No. 4-24 Page 140Document6 pagesNo. 4-24 Page 140Nemalai VitalNo ratings yet

- No. 4-20-21 Page 138-139Document6 pagesNo. 4-20-21 Page 138-139Nemalai VitalNo ratings yet

- No.4-22-23 Page 139Document4 pagesNo.4-22-23 Page 139Nemalai VitalNo ratings yet

- No. 4-31,4-32,4-33 Page 143-144Document12 pagesNo. 4-31,4-32,4-33 Page 143-144Nemalai VitalNo ratings yet

- No. 4-37 Page 146Document6 pagesNo. 4-37 Page 146Nemalai VitalNo ratings yet

- Intermediate Accounting 1Document22 pagesIntermediate Accounting 1Nemalai VitalNo ratings yet

- Topic 4rev StudentsDocument31 pagesTopic 4rev StudentsNemalai VitalNo ratings yet

- Chapter 6 Bank ReconciliationRev StudentsDocument20 pagesChapter 6 Bank ReconciliationRev StudentsNemalai VitalNo ratings yet

- Topic 7 Receivables Rev StudentsDocument74 pagesTopic 7 Receivables Rev StudentsNemalai VitalNo ratings yet

- Topic 4rev (Students)Document36 pagesTopic 4rev (Students)Nemalai VitalNo ratings yet

- Ne Malai - 6 - Exercise CalculationDocument27 pagesNe Malai - 6 - Exercise CalculationNemalai VitalNo ratings yet

- Class Xii Accountancy 8.cash Flow Statement Competency - Based Test ItemsDocument27 pagesClass Xii Accountancy 8.cash Flow Statement Competency - Based Test ItemsjashanjeetNo ratings yet

- AHM13e Chapter - 03 - Solution To Problems and Key To CasesDocument24 pagesAHM13e Chapter - 03 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Irctc: Accounting Report On Comparative and Ratio Analysis OFDocument14 pagesIrctc: Accounting Report On Comparative and Ratio Analysis OFSoumya Sumana SendNo ratings yet

- © The Institute of Chartered Accountants of India: TH STDocument46 pages© The Institute of Chartered Accountants of India: TH STheikNo ratings yet

- Literature Review On Comparative Financial AnalysisDocument6 pagesLiterature Review On Comparative Financial Analysisc5sd1aqjNo ratings yet

- Cuet Ug Section Ii Domain Specific Subject Accountancy Book Keeping Entrance Test Guide RPH Editorial Board Full ChapterDocument68 pagesCuet Ug Section Ii Domain Specific Subject Accountancy Book Keeping Entrance Test Guide RPH Editorial Board Full Chapterkatrina.vera416100% (5)

- End Term On 24.09.2019 FR MBA 2019-21 Term IDocument10 pagesEnd Term On 24.09.2019 FR MBA 2019-21 Term Ideliciousfood463No ratings yet

- 568 - LLC Tax Return FormDocument7 pages568 - LLC Tax Return FormAndreana Dumpling WilliamsNo ratings yet

- BA991 Activity Guide Chapter 3Document12 pagesBA991 Activity Guide Chapter 3vanessaNo ratings yet

- المحاسبة باللغة الانجليزية ٤Document16 pagesالمحاسبة باللغة الانجليزية ٤wead888No ratings yet

- Case Study Solution PDFDocument6 pagesCase Study Solution PDFNaomi Alberg-BlijdNo ratings yet

- Leac 205Document47 pagesLeac 205Jyoti SinghNo ratings yet

- Corporation NotesDocument5 pagesCorporation NotesPrestine Faith SalinasNo ratings yet

- Accounting LM3Document6 pagesAccounting LM3Nathan Kurt LeeNo ratings yet

- P1-02 Loans and ReceivablesDocument5 pagesP1-02 Loans and ReceivablesRachel LeachonNo ratings yet

- FINANCIAL STATEMENTS: Preparation and PresentationDocument39 pagesFINANCIAL STATEMENTS: Preparation and PresentationPaul BanuaNo ratings yet

- Question Paper For The Position: Audit & Accounts Officer TimeDocument2 pagesQuestion Paper For The Position: Audit & Accounts Officer TimeM A Fazal & Co.No ratings yet

- Bueno Salud Care Audit Report 21-22Document31 pagesBueno Salud Care Audit Report 21-22Sameer ParwaniNo ratings yet

- Financial Accounting Theory and Analysis Text and Cases 11th Edition Schroeder Solutions ManualDocument26 pagesFinancial Accounting Theory and Analysis Text and Cases 11th Edition Schroeder Solutions Manualhildabacvvz100% (34)

- Home Office and Branch AccountingDocument7 pagesHome Office and Branch AccountingRujean Salar AltejarNo ratings yet

- Solutions Mock Test Investment in Associate and Accounts PayableDocument16 pagesSolutions Mock Test Investment in Associate and Accounts PayableCIRILO EMIL BAYLOSISNo ratings yet

- Balance SheetDocument1 pageBalance Sheetvenkateshvinayakam6753No ratings yet

- Solution AldineDocument8 pagesSolution AldineAkshay TulshyanNo ratings yet

- Comparative Balance SheetDocument8 pagesComparative Balance Sheet1028No ratings yet

- Ch. 16 - Distribution To ShareholdersDocument28 pagesCh. 16 - Distribution To ShareholdersLara FloresNo ratings yet