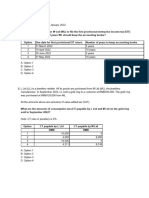

CIT Questions

CIT Questions

You might also like

- Multiple Choice Questions. F6. CLC.2020. PIT and CIT. 12 Feb 2020Document19 pagesMultiple Choice Questions. F6. CLC.2020. PIT and CIT. 12 Feb 2020MinhDuong100% (1)

- Tutorial 6 - 2024Document4 pagesTutorial 6 - 2024Giang Dương HươngNo ratings yet

- Corporate Income Tax Excercise BFIDocument3 pagesCorporate Income Tax Excercise BFInga vuNo ratings yet

- Corporate Income Tax: Section A - Multiple Choice QuestionsDocument24 pagesCorporate Income Tax: Section A - Multiple Choice QuestionsWanda NguyenNo ratings yet

- CBE June 2021 - QDocument10 pagesCBE June 2021 - QNguyễn Hồng NgọcNo ratings yet

- Tax Tong Hop Summary of A Vast Array of Questions That Students Can Use To Review BeforeDocument31 pagesTax Tong Hop Summary of A Vast Array of Questions That Students Can Use To Review Beforelinhtruong17082004No ratings yet

- CBE June 22 - QDocument8 pagesCBE June 22 - QNguyễn Hồng NgọcNo ratings yet

- Tut TaxDocument6 pagesTut TaxKieu Anh Bui LeNo ratings yet

- Tutorial 7 - 2024Document4 pagesTutorial 7 - 2024Giang Dương HươngNo ratings yet

- Case Study - CLC - Chapter 4Document5 pagesCase Study - CLC - Chapter 4Thái Nữ Hoàng AnhNo ratings yet

- Taxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mDocument32 pagesTaxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mnga vuNo ratings yet

- TXCHN 2022 Dec QDocument18 pagesTXCHN 2022 Dec Qshaunzacharia007No ratings yet

- Adjusting Entries A. Short ProblemsDocument3 pagesAdjusting Entries A. Short ProblemsFeiya LiuNo ratings yet

- Quiz 2 With Correct AnswersDocument7 pagesQuiz 2 With Correct AnswersmarietorianoNo ratings yet

- PBT1 Mock ExamDocument8 pagesPBT1 Mock ExamLee NguyenNo ratings yet

- Case Study - Chapter 1 2 3 4 - 2Document5 pagesCase Study - Chapter 1 2 3 4 - 2Lê Ngọc Vân NhiNo ratings yet

- Suggested Answers Global Financial Reporting StandardsDocument49 pagesSuggested Answers Global Financial Reporting StandardsNagabhushanaNo ratings yet

- Accounting Sample ProblemsDocument9 pagesAccounting Sample Problemsjoong wanNo ratings yet

- Problems - Final ExaminationDocument3 pagesProblems - Final Examinationjhell de la cruzNo ratings yet

- 21-22 QUIZ-1 With SolutionsDocument3 pages21-22 QUIZ-1 With SolutionsShubham BansalNo ratings yet

- Reviewer Interm 2Document3 pagesReviewer Interm 2Mae DionisioNo ratings yet

- A. C. Fair Value After Reconditioning CostDocument3 pagesA. C. Fair Value After Reconditioning CostJamie RamosNo ratings yet

- LiabilitiesDocument3 pagesLiabilitiesFrederick AbellaNo ratings yet

- Quiz MTDocument6 pagesQuiz MTClara MacallingNo ratings yet

- Tutorial 3 WHT DiscussDocument6 pagesTutorial 3 WHT DiscussAqila Syakirah IVNo ratings yet

- FAR-06 Earnings Per ShareDocument4 pagesFAR-06 Earnings Per ShareKim Cristian Maaño50% (2)

- Corporate Income Tax: Section A - Multiple Choice QuestionsDocument36 pagesCorporate Income Tax: Section A - Multiple Choice QuestionsWanda NguyenNo ratings yet

- Ministry of FinanceDocument2 pagesMinistry of FinanceYến Hoàng LêNo ratings yet

- CIT Exercises - June 2020 - ACEDocument16 pagesCIT Exercises - June 2020 - ACEKHUÊ TRẦN ÁINo ratings yet

- TX - Mock test - Đề bàiDocument16 pagesTX - Mock test - Đề bàiPhán Tiêu TiềnNo ratings yet

- PA1 Mock ExamDocument18 pagesPA1 Mock Examyciamyr67% (3)

- F6 VAT QuestionsDocument9 pagesF6 VAT QuestionsHuỳnh TrungNo ratings yet

- All Level Two Coc QuestionsDocument15 pagesAll Level Two Coc Questionsabelu habite neriNo ratings yet

- AfarDocument18 pagesAfarFleo GardivoNo ratings yet

- AFAR PracDocument13 pagesAFAR PracTeofel John Alvizo PantaleonNo ratings yet

- Tutorial 7Document4 pagesTutorial 7kien tranNo ratings yet

- ACC 201-Review Questions FIDocument3 pagesACC 201-Review Questions FIAlbert AcheampongNo ratings yet

- 103 CompilationDocument12 pages103 CompilationLyn AbudaNo ratings yet

- Direct - Tax - Laws Model QuestionsDocument8 pagesDirect - Tax - Laws Model QuestionsAlexis ParrisNo ratings yet

- Attempt All QuestionsDocument5 pagesAttempt All QuestionsApurva SrivastavaNo ratings yet

- Accounting For RevenuesDocument7 pagesAccounting For Revenuesvijayranjan1983No ratings yet

- Ce On Current LiabilitiesDocument3 pagesCe On Current LiabilitiesCharles TuazonNo ratings yet

- Mock Exam Paper: Time AllowedDocument9 pagesMock Exam Paper: Time AllowedVannak2015No ratings yet

- Tutorial 8Document6 pagesTutorial 8Waruna PrabhaswaraNo ratings yet

- F6 Midterm Test QuestionDocument11 pagesF6 Midterm Test QuestionChippu AnhNo ratings yet

- Sample Midterm Exam Solution PDFDocument17 pagesSample Midterm Exam Solution PDFtomar_muditNo ratings yet

- Quiz 14P - Income TaxDocument5 pagesQuiz 14P - Income TaxDolaypanNo ratings yet

- Chapter 2Document8 pagesChapter 2cindyNo ratings yet

- F1 - Financial OperationsDocument20 pagesF1 - Financial OperationsZHANG EmilyNo ratings yet

- Questions and Problems 2022Document22 pagesQuestions and Problems 2022Thu PhạmNo ratings yet

- VAT IllustrationsDocument2 pagesVAT IllustrationsBảo BờmNo ratings yet

- 21-22 Comprehensive Exam Solution Part-ADocument4 pages21-22 Comprehensive Exam Solution Part-Af20221197No ratings yet

- Questions and Problems Chapter 1. Corporate Finance Overview QuestionsDocument44 pagesQuestions and Problems Chapter 1. Corporate Finance Overview QuestionsVan ThanhNo ratings yet

- Quick Quiz 1 SS 2021 B (Que)Document3 pagesQuick Quiz 1 SS 2021 B (Que)Tiana Ling Jiunn LiNo ratings yet

- QP Acct 1001d June 2020Document9 pagesQP Acct 1001d June 2020Jaya IndiraNo ratings yet

- All Level 2 Coc Questions Simple To Approach 1 Docx 802a3df9f39Document14 pagesAll Level 2 Coc Questions Simple To Approach 1 Docx 802a3df9f39ibsituabdelaNo ratings yet

- NOTES PROBLEMS ACCTG-323-newDocument3 pagesNOTES PROBLEMS ACCTG-323-newJoyluxxiNo ratings yet

- Practice Problems - Notes and Loans Receivable: General InstructionsDocument2 pagesPractice Problems - Notes and Loans Receivable: General Instructionseia aieNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

Download as pdf or txt

You might also like

- Multiple Choice Questions. F6. CLC.2020. PIT and CIT. 12 Feb 2020Document19 pagesMultiple Choice Questions. F6. CLC.2020. PIT and CIT. 12 Feb 2020MinhDuong100% (1)

- Tutorial 6 - 2024Document4 pagesTutorial 6 - 2024Giang Dương HươngNo ratings yet

- Corporate Income Tax Excercise BFIDocument3 pagesCorporate Income Tax Excercise BFInga vuNo ratings yet

- Corporate Income Tax: Section A - Multiple Choice QuestionsDocument24 pagesCorporate Income Tax: Section A - Multiple Choice QuestionsWanda NguyenNo ratings yet

- CBE June 2021 - QDocument10 pagesCBE June 2021 - QNguyễn Hồng NgọcNo ratings yet

- Tax Tong Hop Summary of A Vast Array of Questions That Students Can Use To Review BeforeDocument31 pagesTax Tong Hop Summary of A Vast Array of Questions That Students Can Use To Review Beforelinhtruong17082004No ratings yet

- CBE June 22 - QDocument8 pagesCBE June 22 - QNguyễn Hồng NgọcNo ratings yet

- Tut TaxDocument6 pagesTut TaxKieu Anh Bui LeNo ratings yet

- Tutorial 7 - 2024Document4 pagesTutorial 7 - 2024Giang Dương HươngNo ratings yet

- Case Study - CLC - Chapter 4Document5 pagesCase Study - CLC - Chapter 4Thái Nữ Hoàng AnhNo ratings yet

- Taxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mDocument32 pagesTaxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mnga vuNo ratings yet

- TXCHN 2022 Dec QDocument18 pagesTXCHN 2022 Dec Qshaunzacharia007No ratings yet

- Adjusting Entries A. Short ProblemsDocument3 pagesAdjusting Entries A. Short ProblemsFeiya LiuNo ratings yet

- Quiz 2 With Correct AnswersDocument7 pagesQuiz 2 With Correct AnswersmarietorianoNo ratings yet

- PBT1 Mock ExamDocument8 pagesPBT1 Mock ExamLee NguyenNo ratings yet

- Case Study - Chapter 1 2 3 4 - 2Document5 pagesCase Study - Chapter 1 2 3 4 - 2Lê Ngọc Vân NhiNo ratings yet

- Suggested Answers Global Financial Reporting StandardsDocument49 pagesSuggested Answers Global Financial Reporting StandardsNagabhushanaNo ratings yet

- Accounting Sample ProblemsDocument9 pagesAccounting Sample Problemsjoong wanNo ratings yet

- Problems - Final ExaminationDocument3 pagesProblems - Final Examinationjhell de la cruzNo ratings yet

- 21-22 QUIZ-1 With SolutionsDocument3 pages21-22 QUIZ-1 With SolutionsShubham BansalNo ratings yet

- Reviewer Interm 2Document3 pagesReviewer Interm 2Mae DionisioNo ratings yet

- A. C. Fair Value After Reconditioning CostDocument3 pagesA. C. Fair Value After Reconditioning CostJamie RamosNo ratings yet

- LiabilitiesDocument3 pagesLiabilitiesFrederick AbellaNo ratings yet

- Quiz MTDocument6 pagesQuiz MTClara MacallingNo ratings yet

- Tutorial 3 WHT DiscussDocument6 pagesTutorial 3 WHT DiscussAqila Syakirah IVNo ratings yet

- FAR-06 Earnings Per ShareDocument4 pagesFAR-06 Earnings Per ShareKim Cristian Maaño50% (2)

- Corporate Income Tax: Section A - Multiple Choice QuestionsDocument36 pagesCorporate Income Tax: Section A - Multiple Choice QuestionsWanda NguyenNo ratings yet

- Ministry of FinanceDocument2 pagesMinistry of FinanceYến Hoàng LêNo ratings yet

- CIT Exercises - June 2020 - ACEDocument16 pagesCIT Exercises - June 2020 - ACEKHUÊ TRẦN ÁINo ratings yet

- TX - Mock test - Đề bàiDocument16 pagesTX - Mock test - Đề bàiPhán Tiêu TiềnNo ratings yet

- PA1 Mock ExamDocument18 pagesPA1 Mock Examyciamyr67% (3)

- F6 VAT QuestionsDocument9 pagesF6 VAT QuestionsHuỳnh TrungNo ratings yet

- All Level Two Coc QuestionsDocument15 pagesAll Level Two Coc Questionsabelu habite neriNo ratings yet

- AfarDocument18 pagesAfarFleo GardivoNo ratings yet

- AFAR PracDocument13 pagesAFAR PracTeofel John Alvizo PantaleonNo ratings yet

- Tutorial 7Document4 pagesTutorial 7kien tranNo ratings yet

- ACC 201-Review Questions FIDocument3 pagesACC 201-Review Questions FIAlbert AcheampongNo ratings yet

- 103 CompilationDocument12 pages103 CompilationLyn AbudaNo ratings yet

- Direct - Tax - Laws Model QuestionsDocument8 pagesDirect - Tax - Laws Model QuestionsAlexis ParrisNo ratings yet

- Attempt All QuestionsDocument5 pagesAttempt All QuestionsApurva SrivastavaNo ratings yet

- Accounting For RevenuesDocument7 pagesAccounting For Revenuesvijayranjan1983No ratings yet

- Ce On Current LiabilitiesDocument3 pagesCe On Current LiabilitiesCharles TuazonNo ratings yet

- Mock Exam Paper: Time AllowedDocument9 pagesMock Exam Paper: Time AllowedVannak2015No ratings yet

- Tutorial 8Document6 pagesTutorial 8Waruna PrabhaswaraNo ratings yet

- F6 Midterm Test QuestionDocument11 pagesF6 Midterm Test QuestionChippu AnhNo ratings yet

- Sample Midterm Exam Solution PDFDocument17 pagesSample Midterm Exam Solution PDFtomar_muditNo ratings yet

- Quiz 14P - Income TaxDocument5 pagesQuiz 14P - Income TaxDolaypanNo ratings yet

- Chapter 2Document8 pagesChapter 2cindyNo ratings yet

- F1 - Financial OperationsDocument20 pagesF1 - Financial OperationsZHANG EmilyNo ratings yet

- Questions and Problems 2022Document22 pagesQuestions and Problems 2022Thu PhạmNo ratings yet

- VAT IllustrationsDocument2 pagesVAT IllustrationsBảo BờmNo ratings yet

- 21-22 Comprehensive Exam Solution Part-ADocument4 pages21-22 Comprehensive Exam Solution Part-Af20221197No ratings yet

- Questions and Problems Chapter 1. Corporate Finance Overview QuestionsDocument44 pagesQuestions and Problems Chapter 1. Corporate Finance Overview QuestionsVan ThanhNo ratings yet

- Quick Quiz 1 SS 2021 B (Que)Document3 pagesQuick Quiz 1 SS 2021 B (Que)Tiana Ling Jiunn LiNo ratings yet

- QP Acct 1001d June 2020Document9 pagesQP Acct 1001d June 2020Jaya IndiraNo ratings yet

- All Level 2 Coc Questions Simple To Approach 1 Docx 802a3df9f39Document14 pagesAll Level 2 Coc Questions Simple To Approach 1 Docx 802a3df9f39ibsituabdelaNo ratings yet

- NOTES PROBLEMS ACCTG-323-newDocument3 pagesNOTES PROBLEMS ACCTG-323-newJoyluxxiNo ratings yet

- Practice Problems - Notes and Loans Receivable: General InstructionsDocument2 pagesPractice Problems - Notes and Loans Receivable: General Instructionseia aieNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet