Download as docx, pdf, or txt

You might also like

- Intermediate Accounting IFRS 3rd EditionDocument20 pagesIntermediate Accounting IFRS 3rd EditionMalik MaulanaNo ratings yet

- Business Research Methods Assignment - Mayur HypermarketDocument3 pagesBusiness Research Methods Assignment - Mayur Hypermarketmurtaza mannanNo ratings yet

- Global Logistics & Supply Chain Management Chapter 7 MCQDocument21 pagesGlobal Logistics & Supply Chain Management Chapter 7 MCQVeninsta Yap100% (3)

- Appraisal RightDocument7 pagesAppraisal Rightriamaealapit3No ratings yet

- Appraisal Right - RCCDocument2 pagesAppraisal Right - RCCFlorencio AlimanNo ratings yet

- Turner Vs Lorenzo ShippingDocument3 pagesTurner Vs Lorenzo ShippingTrisha CastilloNo ratings yet

- Mercado, Floriemae S. BSA 2 Exercise 10Document6 pagesMercado, Floriemae S. BSA 2 Exercise 10Floriemae MercadoNo ratings yet

- Title X Appraisal RightDocument3 pagesTitle X Appraisal RightMeAnn TumbagaNo ratings yet

- TITLE X (Appraisal Right)Document2 pagesTITLE X (Appraisal Right)Princess Ann Mendegorin100% (1)

- Stocks and StockholdersDocument12 pagesStocks and Stockholders123No ratings yet

- Title X Appraisal RightDocument9 pagesTitle X Appraisal RightIan Ray PaglinawanNo ratings yet

- Corporation Sec.75 85Document37 pagesCorporation Sec.75 85iseonggyeong302No ratings yet

- Corpo - Appraisal Right Non Stock CorporationsDocument13 pagesCorpo - Appraisal Right Non Stock CorporationsRiza Zaira MateoNo ratings yet

- Stocks and StockholdersDocument4 pagesStocks and StockholdersCleinJonTiuNo ratings yet

- Corp Sec Notes 5Document15 pagesCorp Sec Notes 5Jorge BandolaNo ratings yet

- RCC Corpo 4Document8 pagesRCC Corpo 4Joan Ashley ViernesNo ratings yet

- Chapter-6 Allotment of SecuritiesDocument8 pagesChapter-6 Allotment of SecuritiesCA CS Umang RataniNo ratings yet

- Or Other Disposition of All or Substantially All of The Corporate Property and Assets As Provided in The Code andDocument3 pagesOr Other Disposition of All or Substantially All of The Corporate Property and Assets As Provided in The Code andRafael JuicoNo ratings yet

- Notes On Stock and StockholdersDocument19 pagesNotes On Stock and Stockholderscharmagne cuevasNo ratings yet

- CDC LawDocument8 pagesCDC LawNawazNo ratings yet

- Appraisal RightDocument10 pagesAppraisal RightkristineroseNo ratings yet

- TITLE-X-to-XII-copy 2-MergedDocument13 pagesTITLE-X-to-XII-copy 2-MergedHoney MacanaNo ratings yet

- LAW2WEEK5ADocument10 pagesLAW2WEEK5AAaliah Rain EdejerNo ratings yet

- Title Vii Stocks and StockholdersDocument7 pagesTitle Vii Stocks and StockholdersMeAnn TumbagaNo ratings yet

- Share Capital PDFDocument6 pagesShare Capital PDFKajal MattuNo ratings yet

- Private Company Limited by Shares Regulations FormDocument17 pagesPrivate Company Limited by Shares Regulations FormGerard 'Rockefeller' YitamkeyNo ratings yet

- RFBT Lesson 5 To 8Document30 pagesRFBT Lesson 5 To 8Marshall HylesNo ratings yet

- Rights of StockholdersDocument3 pagesRights of StockholdersJei Essa AlmiasNo ratings yet

- Dark Cyan White Minimalist English Functions of Communication PresentationDocument52 pagesDark Cyan White Minimalist English Functions of Communication PresentationJamaira CruzNo ratings yet

- Law On Corporation Summary Part 4Document10 pagesLaw On Corporation Summary Part 4Angel Nhova Pepito OmalayNo ratings yet

- Title X Appraisal RightDocument26 pagesTitle X Appraisal RightMaryjane De GuzmanNo ratings yet

- Title X: By: Niah Winnie D. DayritDocument20 pagesTitle X: By: Niah Winnie D. DayritNiah Winnie DayritNo ratings yet

- Unit 8Document10 pagesUnit 8RonelleNo ratings yet

- Corporate Law PSDA: Submitted ToDocument7 pagesCorporate Law PSDA: Submitted ToharshkumraNo ratings yet

- Company Regulation SampleDocument13 pagesCompany Regulation SampleJames Oludele Etu67% (3)

- Buslaw RecitDocument22 pagesBuslaw RecitRonron De ChavezNo ratings yet

- SharesDocument6 pagesSharesgoyalb06062004No ratings yet

- Corporation Notes Title IV-XVDocument19 pagesCorporation Notes Title IV-XVSharn Linzi Buan MontañoNo ratings yet

- (B) Share Capital of A CompanyDocument34 pages(B) Share Capital of A CompanyGhulam Murtaza KoraiNo ratings yet

- SCL QaDocument13 pagesSCL QaAdrielle FloretesNo ratings yet

- Section 235-240Document5 pagesSection 235-240anjalim.ballb2021No ratings yet

- Turner v. Lorenzo ShippingDocument2 pagesTurner v. Lorenzo ShippingCamil Santos0% (1)

- Convertible Promissory Note Template 1Document6 pagesConvertible Promissory Note Template 1David Jay Mor100% (5)

- 2nd Share Capital of A CompanyDocument34 pages2nd Share Capital of A Companywaqasjaved869673No ratings yet

- Subscription ContractDocument11 pagesSubscription ContractDJ ULRICHNo ratings yet

- Appraisal RightDocument7 pagesAppraisal RightAyra BernabeNo ratings yet

- Lesson 1 RIGHT OF APPRAISALDocument6 pagesLesson 1 RIGHT OF APPRAISALDi CanNo ratings yet

- Revised Corporation Code Part3Document6 pagesRevised Corporation Code Part3not funny didn't laughNo ratings yet

- Mna Sqeeout and MoreDocument12 pagesMna Sqeeout and Moresomya jainNo ratings yet

- RFBT Review Corporation MergerDocument10 pagesRFBT Review Corporation Mergerduguitjinky20.svcNo ratings yet

- Wa0004.Document15 pagesWa0004.Ýøgësh ÑäyãkNo ratings yet

- Paragraph 4Document3 pagesParagraph 4feng miNo ratings yet

- F. Corporate Powers and Voting RequirementsDocument5 pagesF. Corporate Powers and Voting RequirementsallyzhapNo ratings yet

- Rights Issue My NotesDocument5 pagesRights Issue My Notesfriendsforever3405No ratings yet

- Title X. - Appraisal RightDocument2 pagesTitle X. - Appraisal RightAlyn SimNo ratings yet

- Doctrine of Indivisibility of Subscription ContractDocument18 pagesDoctrine of Indivisibility of Subscription ContractAngelaNo ratings yet

- Transfer and Transmission of SharesDocument31 pagesTransfer and Transmission of SharesSiddhant SodhiaNo ratings yet

- Capital Shares and ShareholdersDocument14 pagesCapital Shares and Shareholdersjisansalehin1No ratings yet

- PraushDocument9 pagesPraushAMIT BARDHAN MOHANTYNo ratings yet

- Crowdfunding on SteroidsFrom EverandCrowdfunding on SteroidsRating: 3 out of 5 stars3/5 (1)

- PrayerDocument1 pagePrayerRaynamae SalayaNo ratings yet

- MAGNETISM WPS Office11Document3 pagesMAGNETISM WPS Office11Raynamae SalayaNo ratings yet

- Cabaron P - RFBT4 - Ivi - Bsa3Document2 pagesCabaron P - RFBT4 - Ivi - Bsa3Raynamae SalayaNo ratings yet

- 601Document2 pages601Raynamae SalayaNo ratings yet

- 604Document2 pages604Raynamae SalayaNo ratings yet

- 603Document2 pages603Raynamae SalayaNo ratings yet

- 602Document2 pages602Raynamae SalayaNo ratings yet

- 605Document2 pages605Raynamae SalayaNo ratings yet

- 606Document2 pages606Raynamae SalayaNo ratings yet

- 608Document2 pages608Raynamae SalayaNo ratings yet

- 609Document2 pages609Raynamae SalayaNo ratings yet

- 2.1 Organizational StructureDocument2 pages2.1 Organizational StructureRaynamae SalayaNo ratings yet

- 610Document2 pages610Raynamae SalayaNo ratings yet

- Adoption of By-Laws: Delegation WithdrawalDocument2 pagesAdoption of By-Laws: Delegation WithdrawalRaynamae SalayaNo ratings yet

- Document FlowchartsDocument2 pagesDocument FlowchartsRaynamae SalayaNo ratings yet

- 5.3 Fraud and Accountants Definitions of FraudDocument2 pages5.3 Fraud and Accountants Definitions of FraudRaynamae SalayaNo ratings yet

- Exercise of Corporate PowerDocument2 pagesExercise of Corporate PowerRaynamae SalayaNo ratings yet

- 615Document2 pages615Raynamae SalayaNo ratings yet

- True TrueDocument3 pagesTrue TrueRaynamae SalayaNo ratings yet

- 614Document2 pages614Raynamae SalayaNo ratings yet

- 1.7. Presiding Officer in Meetings: Directors' or Trustees' MeetingsDocument2 pages1.7. Presiding Officer in Meetings: Directors' or Trustees' MeetingsRaynamae SalayaNo ratings yet

- Engr. Prof. Peter OnwualuDocument35 pagesEngr. Prof. Peter OnwualuOladimeji TaiwoNo ratings yet

- Schlegelmilch 2003Document18 pagesSchlegelmilch 2003Prijoy JaniNo ratings yet

- Application For Loan Restructuring: (Under R.A. 9679)Document2 pagesApplication For Loan Restructuring: (Under R.A. 9679)Lovely Clarisse LaureanoNo ratings yet

- Jul 16 Exam Adv Inv + AnswDocument8 pagesJul 16 Exam Adv Inv + AnswTina ChanNo ratings yet

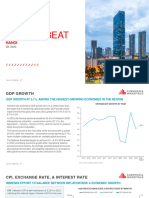

- Vietnam 2023q4 CW Market Beat Hanoi - en CombinedDocument36 pagesVietnam 2023q4 CW Market Beat Hanoi - en CombinedVu Ha NguyenNo ratings yet

- SAP Transaction CodesDocument10 pagesSAP Transaction Codesnanduri.aparna161No ratings yet

- Registrar and Transfer AgentsDocument7 pagesRegistrar and Transfer AgentsjatinNo ratings yet

- Classification of Reserves and ResourcesDocument27 pagesClassification of Reserves and Resourcesnina chentsovaNo ratings yet

- RBI Issues SARFAESI Act 2002 Guidelines and Directions As Amendment Upto 30th June 2015Document26 pagesRBI Issues SARFAESI Act 2002 Guidelines and Directions As Amendment Upto 30th June 2015Kapil Dev SaggiNo ratings yet

- Activity 9 Global CityDocument2 pagesActivity 9 Global CitySamuel J. PabloNo ratings yet

- MIS and Banking IntroductionDocument5 pagesMIS and Banking IntroductionVaibhav GuptaNo ratings yet

- Determinants of Price Earnings RatioDocument13 pagesDeterminants of Price Earnings RatioFalguni ChowdhuryNo ratings yet

- Tata Steel Corus Acquisition Financial DetailsDocument6 pagesTata Steel Corus Acquisition Financial DetailsSandarbh Agarwal0% (1)

- Services Marketing Midterm ExamDocument7 pagesServices Marketing Midterm ExamNH PrinceNo ratings yet

- Max Weber On Law and The Rise of CapitalismDocument35 pagesMax Weber On Law and The Rise of CapitalismTomás AguerreNo ratings yet

- The Impacts of UnemploymentDocument3 pagesThe Impacts of UnemploymentjimNo ratings yet

- State of Housing BookDocument50 pagesState of Housing Bookjorge uturNo ratings yet

- AB City Council Prelim Finance Report - Mark CiommoDocument35 pagesAB City Council Prelim Finance Report - Mark CiommoharrymattisonNo ratings yet

- Annual Report 2020 21 VFinalDocument400 pagesAnnual Report 2020 21 VFinalKshitij SrivastavaNo ratings yet

- Pink - Not Sure But Possible Answer Orange - Wrong Answer Note For Questions With Computations: Your Answer Should Be A Whole Number. Do Not UseDocument26 pagesPink - Not Sure But Possible Answer Orange - Wrong Answer Note For Questions With Computations: Your Answer Should Be A Whole Number. Do Not UseGene Albert LopezNo ratings yet

- 15 Index NumberDocument5 pages15 Index NumberAjib BayuNo ratings yet

- SAP Certified Application Associate - Financial Accounting With SAP ERP - FullDocument41 pagesSAP Certified Application Associate - Financial Accounting With SAP ERP - FullMohammed Nawaz ShariffNo ratings yet

- Unit 2-1Document39 pagesUnit 2-1LOOPY GAMINGNo ratings yet

- Review QuestionsDocument4 pagesReview Questionsnguyen ngoc lanNo ratings yet

- Toyota Production System PDFDocument7 pagesToyota Production System PDFZaib RehmanNo ratings yet

- What Is Multi OrgDocument3 pagesWhat Is Multi Orglog_anupamNo ratings yet

- SPYKAR JEANS (1) ................ WordDocument21 pagesSPYKAR JEANS (1) ................ WordNishant Bhimraj Ramteke75% (4)