Download as pdf or txt

You might also like

- Kahn 160711 Ma MCQDocument1 pageKahn 160711 Ma MCQZaineb Mora SadikNo ratings yet

- AFAR - PreWeek - May 2022Document31 pagesAFAR - PreWeek - May 2022Miguel ManagoNo ratings yet

- Joint Arrangements: Use The Following Information For Questions 1 and 2Document1 pageJoint Arrangements: Use The Following Information For Questions 1 and 2Mary Jescho Vidal AmpilNo ratings yet

- Business Cup Level 1 Quiz BeeDocument28 pagesBusiness Cup Level 1 Quiz BeeRowellPaneloSalapareNo ratings yet

- Acctg 2Document2 pagesAcctg 2Shayne EsmeroNo ratings yet

- FIL 124 - Final TestDocument16 pagesFIL 124 - Final TestChavey Jean V. RenidoNo ratings yet

- Partnership Formation Discussion ProblemsDocument2 pagesPartnership Formation Discussion ProblemsMicca AndraeNo ratings yet

- Balbin, Ma. Margarette P. Assignment #1Document7 pagesBalbin, Ma. Margarette P. Assignment #1Margaveth P. BalbinNo ratings yet

- Pinnacle Far Preweek May 2022Document32 pagesPinnacle Far Preweek May 2022Miguel ManagoNo ratings yet

- Multiple-Choice-Questions FinalDocument3 pagesMultiple-Choice-Questions FinalFreann Sharisse AustriaNo ratings yet

- Additional InformationDocument6 pagesAdditional InformationBabylyn NavarroNo ratings yet

- DissolutionDocument3 pagesDissolutionDonna Mae HernandezNo ratings yet

- AFAR - Partnership OperationsDocument3 pagesAFAR - Partnership OperationsCleofe Mae Piñero AseñasNo ratings yet

- Partnership Liquidation: Answer: (D)Document2 pagesPartnership Liquidation: Answer: (D)Ivy BautistaNo ratings yet

- IntAcc Quiz 1 PDFDocument9 pagesIntAcc Quiz 1 PDFMyles Ninon LazoNo ratings yet

- Basic Concepts of PartnershipDocument7 pagesBasic Concepts of PartnershipKhim CortezNo ratings yet

- AFAR-01 (Partnership Formation and Operations)Document6 pagesAFAR-01 (Partnership Formation and Operations)Ruth RodriguezNo ratings yet

- Cpa Review School of The Philippines ManilaDocument4 pagesCpa Review School of The Philippines Manilaxara mizpahNo ratings yet

- Review Session 3 Conceptual FrameworkDocument16 pagesReview Session 3 Conceptual Frameworkalyanna alanoNo ratings yet

- AFAR-01 PartnershipDocument6 pagesAFAR-01 PartnershipRamainne Ronquillo0% (1)

- AdvaccDocument3 pagesAdvaccMontessa GuelasNo ratings yet

- Partnership ReviewerDocument11 pagesPartnership Reviewerbae joohyun0% (1)

- AfarDocument14 pagesAfarPaulo MiguelNo ratings yet

- Partnership Operations: QuizDocument8 pagesPartnership Operations: QuizLee SuarezNo ratings yet

- AFAR 01 Partnership FormationDocument9 pagesAFAR 01 Partnership FormationHatterlessNo ratings yet

- Advanced Financial Accounting and Reporting (Partnership)Document5 pagesAdvanced Financial Accounting and Reporting (Partnership)Mike C Buceta100% (1)

- Problems: Problem 4 - 1Document4 pagesProblems: Problem 4 - 1KioNo ratings yet

- Ae100 Partnership Operations Notes and Sample ProblemsDocument3 pagesAe100 Partnership Operations Notes and Sample ProblemsJrm mendesNo ratings yet

- Prelim Quiz 02 Partnerhsip OperationDocument9 pagesPrelim Quiz 02 Partnerhsip OperationGarp BarrocaNo ratings yet

- Cup-Management Advisory ServicesDocument7 pagesCup-Management Advisory ServicesJerauld BucolNo ratings yet

- Reviewer 1 Fundamentals of Accounting 2 PDFDocument13 pagesReviewer 1 Fundamentals of Accounting 2 PDFelminvaldez80% (5)

- FAR2 CHAPTER 1 (PG 1-13)Document13 pagesFAR2 CHAPTER 1 (PG 1-13)Layla MainNo ratings yet

- 03 Partnership Dissolution ANSWERDocument4 pages03 Partnership Dissolution ANSWERKrizza Mae MendozaNo ratings yet

- Partnership Mock ExamDocument15 pagesPartnership Mock ExamPerbielyn BasinilloNo ratings yet

- Partnership 1 PDFDocument12 pagesPartnership 1 PDFShane TorrieNo ratings yet

- Reviewer - ParCorDocument13 pagesReviewer - ParCoramiNo ratings yet

- SATURDAYDocument20 pagesSATURDAYkristine bandaviaNo ratings yet

- AC-42-Lec-Midterm-test-bank - Answer KeyDocument9 pagesAC-42-Lec-Midterm-test-bank - Answer KeyEunice CatubayNo ratings yet

- AFAR Q1 Pre-Week SolMan - MAY 2019Document13 pagesAFAR Q1 Pre-Week SolMan - MAY 2019Aj PacaldoNo ratings yet

- Additional ProblemsDocument3 pagesAdditional Problems가 푸 레멜 린 메No ratings yet

- Prelim Take-Home ExamDocument8 pagesPrelim Take-Home ExamMelanie SamsonaNo ratings yet

- CMPC131Document15 pagesCMPC131Nhel AlvaroNo ratings yet

- AFAR 01 Partnership FormationDocument9 pagesAFAR 01 Partnership FormationJohn Rey BallesterosNo ratings yet

- Partnership HCC CttoDocument7 pagesPartnership HCC CttoKenncy100% (1)

- DocxDocument13 pagesDocxMingNo ratings yet

- Partnership Q1Document3 pagesPartnership Q1Lorraine Mae RobridoNo ratings yet

- Partnership: INTPRAB Notes From Brian Lim HDV/DNGDocument28 pagesPartnership: INTPRAB Notes From Brian Lim HDV/DNGAbegail Llobo Gitana100% (1)

- Acp 101 MexamDocument5 pagesAcp 101 MexamLyca SorianoNo ratings yet

- AfarDocument3 pagesAfarLeizzamar BayadogNo ratings yet

- Partnership Operations Assignment 2Document1 pagePartnership Operations Assignment 2Rona S. Pepino - AguirreNo ratings yet

- Auditing Theory 4th ExaminationDocument12 pagesAuditing Theory 4th ExaminationKathleenNo ratings yet

- Practical Accounting 2: Theory & Practice Advance Accounting Partnership - Formation & AdmissionDocument46 pagesPractical Accounting 2: Theory & Practice Advance Accounting Partnership - Formation & AdmissionKeith Anthony AmorNo ratings yet

- Accounting For PartnershipsDocument10 pagesAccounting For PartnershipsRicaRhayaMangahasNo ratings yet

- Partnership Dissolution ProblemsDocument9 pagesPartnership Dissolution ProblemsKristel DayritNo ratings yet

- Law Example Quiz ReviewDocument5 pagesLaw Example Quiz ReviewyelzNo ratings yet

- Intermediate Acctg A 1 10Document10 pagesIntermediate Acctg A 1 10Leonila RiveraNo ratings yet

- QUESTIONS BANK Ch14 BODADocument18 pagesQUESTIONS BANK Ch14 BODAISLAM KHALED ZSCNo ratings yet

- Accounting For Special Transactions Prelim Examination: Use The Following Information For The Next Two QuestionsDocument24 pagesAccounting For Special Transactions Prelim Examination: Use The Following Information For The Next Two QuestionsArtisan82% (11)

- Practice Qs Chap 13HDocument4 pagesPractice Qs Chap 13HSuy YanghearNo ratings yet

- AdvacDocument13 pagesAdvacAmie Jane MirandaNo ratings yet

- Ac 16 MidtermDocument20 pagesAc 16 MidtermMarjorie AmpongNo ratings yet

- Accounting For Special Transactions Final Grading ExaminationDocument20 pagesAccounting For Special Transactions Final Grading ExaminationJoody CatacutanNo ratings yet

- Capital Gain Sums With SolutionDocument10 pagesCapital Gain Sums With Solutionkomil bogharaNo ratings yet

- Ratio Analysis (Divya Jadi Booti)Document85 pagesRatio Analysis (Divya Jadi Booti)Michael AdhikariNo ratings yet

- HDFC ERGO General Insurance Company Limited 2nd Floor, Potluri Castle, Dwarakanagar, VSP, 16, Vishakapatnam - 530 016Document2 pagesHDFC ERGO General Insurance Company Limited 2nd Floor, Potluri Castle, Dwarakanagar, VSP, 16, Vishakapatnam - 530 016Siva rajNo ratings yet

- CSEC POA January 2018 P1Document10 pagesCSEC POA January 2018 P1Boppy VevoNo ratings yet

- Money and Banking NotesDocument9 pagesMoney and Banking NotesLuisLoNo ratings yet

- Restoration TableDocument2 pagesRestoration TableMuhammad Farooq AwanNo ratings yet

- VIDYA SAGAR (Audit)Document5 pagesVIDYA SAGAR (Audit)Prem ThakurNo ratings yet

- Strategies of UTI and HDFC Mutual FundsDocument81 pagesStrategies of UTI and HDFC Mutual FundsGarg familyNo ratings yet

- Chapter 5 Advanced AccountingDocument19 pagesChapter 5 Advanced AccountingMarife De Leon VillalonNo ratings yet

- What Is FortfaitingDocument3 pagesWhat Is FortfaitingRAMESHBABUNo ratings yet

- Timeline of The Lehman Brothers CollapseDocument3 pagesTimeline of The Lehman Brothers CollapseJonas MondalaNo ratings yet

- STMT CHIP 001 CPVQ000076 Jul2022Document9 pagesSTMT CHIP 001 CPVQ000076 Jul2022Yenobot ObotNo ratings yet

- Notes On Daily TransactionsDocument51 pagesNotes On Daily TransactionsCyndy NgwenNo ratings yet

- FINANCE FOR EXECUTIVES (AutoRecovered)Document5 pagesFINANCE FOR EXECUTIVES (AutoRecovered)suruchi singhNo ratings yet

- Emerging Practices in Mobile Microinsurance: Camilo TéllezDocument8 pagesEmerging Practices in Mobile Microinsurance: Camilo TéllezTheodorah Gaelle MadzyNo ratings yet

- Hand Out NO 11 Clearing and SettlementDocument9 pagesHand Out NO 11 Clearing and SettlementAbdul basitNo ratings yet

- Important Instructions For Filling Ach Mandate Form: HdfcbankltdDocument1 pageImportant Instructions For Filling Ach Mandate Form: HdfcbankltdFUTURE NEXTTIMENo ratings yet

- Sba 2.0Document1 pageSba 2.0Operation BluepayNo ratings yet

- Merchant Opportunities Fund OverviewDocument1 pageMerchant Opportunities Fund OverviewhoopburnNo ratings yet

- Accounts INterview QuestionsDocument4 pagesAccounts INterview QuestionsRinkal MalaviyaNo ratings yet

- Cambridge O Level: Accounting 7707/23 October/November 2022Document18 pagesCambridge O Level: Accounting 7707/23 October/November 2022FahadNo ratings yet

- Financial InclusionDocument6 pagesFinancial InclusionsignNo ratings yet

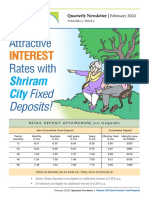

- Attractive Rates With: InterestDocument4 pagesAttractive Rates With: Interestdharam singhNo ratings yet

- Altum Credo - New CAM Format For NBFC Clean VersionDocument19 pagesAltum Credo - New CAM Format For NBFC Clean VersionSwarna SinghNo ratings yet

- ProposalsDocument25 pagesProposalsDinaraas Tulu100% (1)

- ICICI Prudential Passive Multi-Asset Fund of Funds (Distributor Version) - RevisedDocument34 pagesICICI Prudential Passive Multi-Asset Fund of Funds (Distributor Version) - RevisedBhuvaneswaran ParthibanNo ratings yet

- Post Test AK2Document51 pagesPost Test AK2thalita najellaNo ratings yet

- BAGNPES Quiz 5 R FinalDocument3 pagesBAGNPES Quiz 5 R FinalJan lessthan4No ratings yet