(2023) 148 Taxmann - Com 184 (Bombay) (08-03-2023) Digi1 Electronics (P.) Ltd. vs. Assistant Commissioner of Income Tax-13

(2023) 148 Taxmann - Com 184 (Bombay) (08-03-2023) Digi1 Electronics (P.) Ltd. vs. Assistant Commissioner of Income Tax-13

You might also like

- Smart Communications, Inc. vs. Municipality of Malvar, BatangasDocument3 pagesSmart Communications, Inc. vs. Municipality of Malvar, BatangasRaquel Doquenia100% (2)

- First Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument9 pagesFirst Division: Republic of The Philippines Court of Tax Appeals Quezon CityAemie JordanNo ratings yet

- Instructions For The Transferee (Buyer)Document1 pageInstructions For The Transferee (Buyer)Devu GautamNo ratings yet

- Cir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Document8 pagesCir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Cristy Yaun-CabagnotNo ratings yet

- Kusum Gupta v. ITO (Delhi HC)Document6 pagesKusum Gupta v. ITO (Delhi HC)Avar LambaNo ratings yet

- 213037-2018-Coca-Cola Bottlers Philippines Inc. V.Document11 pages213037-2018-Coca-Cola Bottlers Philippines Inc. V.CamshtNo ratings yet

- Chargeback Card InternetDocument16 pagesChargeback Card InternetFlaviub23No ratings yet

- COMMISSIONER OF INTERNAL REVENUE Vs METRO STAR SUPERAMADocument1 pageCOMMISSIONER OF INTERNAL REVENUE Vs METRO STAR SUPERAMACharles Roger RayaNo ratings yet

- CIR Vs Metro StarDocument4 pagesCIR Vs Metro StarJohnde MartinezNo ratings yet

- Western Mindanao Power Corporation vs. Commissioner of Internal RevenueDocument7 pagesWestern Mindanao Power Corporation vs. Commissioner of Internal RevenueJonjon BeeNo ratings yet

- 10 - CIR v. Yusen Logistics Center, Inc.Document3 pages10 - CIR v. Yusen Logistics Center, Inc.Carlota VillaromanNo ratings yet

- TDS U - S. 194J Not Deductible On Payment For Outright Purchase of Copyright and Technical Know-HowDocument10 pagesTDS U - S. 194J Not Deductible On Payment For Outright Purchase of Copyright and Technical Know-HowheyaanshNo ratings yet

- (2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Document2 pages(2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Jai ModiNo ratings yet

- October 2020 Tax AlertDocument5 pagesOctober 2020 Tax AlertRheneir MoraNo ratings yet

- CTA_2D_CV_09713_A_2020OCT14_ASSDocument8 pagesCTA_2D_CV_09713_A_2020OCT14_ASSPaulNo ratings yet

- 36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0Document10 pages36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0ervingabralagbonNo ratings yet

- Court of Tax Appeal: Chairperson, andDocument19 pagesCourt of Tax Appeal: Chairperson, andJason MergalNo ratings yet

- Revised Concept Papere RegistrationDocument3 pagesRevised Concept Papere RegistrationayanNo ratings yet

- Kuwait Airways Corp. v. Commissioner of Internal RevenueDocument12 pagesKuwait Airways Corp. v. Commissioner of Internal Revenueedcbess23No ratings yet

- Tax Department Takes Up 68,000 Cases For E-Veri Cation: All You Need To Know About e - Veri Cation SchemeDocument3 pagesTax Department Takes Up 68,000 Cases For E-Veri Cation: All You Need To Know About e - Veri Cation SchemeSudhir BhargavaNo ratings yet

- Green Valley Marketing Corp. v. Commissioner of Internal Revenue, C.T.A. Case No. 8988, (November 3, 2017) PDFDocument42 pagesGreen Valley Marketing Corp. v. Commissioner of Internal Revenue, C.T.A. Case No. 8988, (November 3, 2017) PDFKriszan ManiponNo ratings yet

- Demand Pre - Intimation LetterDocument2 pagesDemand Pre - Intimation LetterAMIT TIWARINo ratings yet

- Tax DigestDocument11 pagesTax DigestSarah Jane Fabricante BehigaNo ratings yet

- Smart Communications vs. Municipality of MalvarDocument3 pagesSmart Communications vs. Municipality of MalvarClark Edward Runes Uytico0% (1)

- CIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerDocument15 pagesCIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerSoftdynamiteNo ratings yet

- CIR v. Enron Subic Power CorporationDocument2 pagesCIR v. Enron Subic Power CorporationGain DeeNo ratings yet

- CIR Vs Migrant PagbilaoDocument12 pagesCIR Vs Migrant PagbilaoMelo Ponce de Leon100% (1)

- CIR vs. FitnessByDesign - SCRADocument28 pagesCIR vs. FitnessByDesign - SCRALouis AngelesNo ratings yet

- CIR v. Metro Star SupremaDocument3 pagesCIR v. Metro Star SupremaNichol Uriel ArcaNo ratings yet

- Gross Income CasesDocument80 pagesGross Income CasesapperdapperNo ratings yet

- FAN Without PAN Violates Due Process - ArticleDocument3 pagesFAN Without PAN Violates Due Process - ArticleCkey ArNo ratings yet

- CTA Case No. 24 (CTA Case No 6170)Document7 pagesCTA Case No. 24 (CTA Case No 6170)Jeffrey JosolNo ratings yet

- Research On NIRCDocument6 pagesResearch On NIRCFrancis RubioNo ratings yet

- Understanding Electronic Invoicing System in The PhilippinesDocument27 pagesUnderstanding Electronic Invoicing System in The PhilippinesSUMIT KUMAR AGARWALANo ratings yet

- Cta 3D Ac 00248 D 2023apr19 OthDocument14 pagesCta 3D Ac 00248 D 2023apr19 OthFirenze PHNo ratings yet

- Excess Input Tax or Creditable Input: - Second DivisionDocument29 pagesExcess Input Tax or Creditable Input: - Second DivisionAsHervea AbanteNo ratings yet

- (Rajasthan) / (2022) 447 ITR 698 (Rajasthan) (29-06-2022)Document6 pages(Rajasthan) / (2022) 447 ITR 698 (Rajasthan) (29-06-2022)rigiyanNo ratings yet

- E-Way Bill Under GST (Nmims)Document8 pagesE-Way Bill Under GST (Nmims)Mitali BiswasNo ratings yet

- Sec 68 - Case LawsDocument2 pagesSec 68 - Case LawsShreNo ratings yet

- Calcutta Discount Co. Ltd. v. ITO: (1961) 41 ITR 191 (SC) (1967) 63 ITR 219 (SC)Document6 pagesCalcutta Discount Co. Ltd. v. ITO: (1961) 41 ITR 191 (SC) (1967) 63 ITR 219 (SC)rigiyanNo ratings yet

- RemediesDocument36 pagesRemediesDaryll Gayle AsuncionNo ratings yet

- SC Tax Decision2Document45 pagesSC Tax Decision2Jasreel DomasingNo ratings yet

- CIR Vs First ExpressDocument7 pagesCIR Vs First ExpressGhreighz GalinatoNo ratings yet

- Electronic Way BillDocument6 pagesElectronic Way BillKumariNo ratings yet

- Assam Instruction No. 13 2023 GSTDocument2 pagesAssam Instruction No. 13 2023 GSTCA Kaushik Ranjan GoswamiNo ratings yet

- Qatar Airways Vs Cir 2020 Case DigestDocument2 pagesQatar Airways Vs Cir 2020 Case DigestJunia Dungaya100% (1)

- CIR V Eron Subic PowerDocument5 pagesCIR V Eron Subic PowerYoo Si JinNo ratings yet

- Cir Vs Metro Super Rama DigestDocument2 pagesCir Vs Metro Super Rama DigestKobe BryantNo ratings yet

- CIR vs. Eron Subic Power CorporationDocument5 pagesCIR vs. Eron Subic Power CorporationJohn FerarenNo ratings yet

- UntitledDocument5 pagesUntitledharsh hgNo ratings yet

- Unit 18Document20 pagesUnit 18Raja SahilNo ratings yet

- Petitioner's Arguments:: The IssueDocument19 pagesPetitioner's Arguments:: The IssueBarnie BingNo ratings yet

- CIR v. Spouses Magaan, G.R. No. 232663, May 3, 2021Document2 pagesCIR v. Spouses Magaan, G.R. No. 232663, May 3, 2021John Cyrus DangananNo ratings yet

- 2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioDocument7 pages2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioThe Chartered Professional NewsletterNo ratings yet

- CIR Vs Isabela Cultural Corporation (ICC)Document11 pagesCIR Vs Isabela Cultural Corporation (ICC)Victor LimNo ratings yet

- FAN Without PAN Violates Due ProcessDocument2 pagesFAN Without PAN Violates Due ProcessDesiree SencoNo ratings yet

- Cir v. Mirant Pagbilao CorporationDocument16 pagesCir v. Mirant Pagbilao CorporationSiobhan RobinNo ratings yet

- Taxation Doctrines 2Document18 pagesTaxation Doctrines 2KCNo ratings yet

- Bank of America NT & Sa, The Commissioner of Internal RevenueDocument4 pagesBank of America NT & Sa, The Commissioner of Internal RevenueHADTUGINo ratings yet

- 21St Century Computer Solutions: A Manual Accounting SimulationFrom Everand21St Century Computer Solutions: A Manual Accounting SimulationNo ratings yet

- (2023) 148 Taxmann - Com 185 (Bombay) (08-03-2023) Jetair (P.) Ltd. vs. Deputy Commissioner of Income-Tax Central Circle-5Document1 page(2023) 148 Taxmann - Com 185 (Bombay) (08-03-2023) Jetair (P.) Ltd. vs. Deputy Commissioner of Income-Tax Central Circle-5Jai ModiNo ratings yet

- (2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Document2 pages(2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Jai ModiNo ratings yet

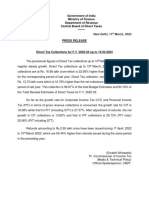

- Government of India Ministry of Finance Department of Revenue Central Board of Direct TaxesDocument1 pageGovernment of India Ministry of Finance Department of Revenue Central Board of Direct TaxesJai ModiNo ratings yet

- V K SubramaniDocument4 pagesV K SubramaniJai ModiNo ratings yet

- Government of India Ministry of Finance Department of Revenue Central Board of Direct TaxesDocument2 pagesGovernment of India Ministry of Finance Department of Revenue Central Board of Direct TaxesJai ModiNo ratings yet

- (2023) 147 Taxmann - Com 446 (Raipur - Trib.) - (2022) 100 ITR (T) 195 (Raipur - Trib.) (26-07-2022) Assistant Commissioner of Income-Tax vs. Sanjay Kumar KocharDocument16 pages(2023) 147 Taxmann - Com 446 (Raipur - Trib.) - (2022) 100 ITR (T) 195 (Raipur - Trib.) (26-07-2022) Assistant Commissioner of Income-Tax vs. Sanjay Kumar KocharJai ModiNo ratings yet

- SCM & PE Theory Book by Dani Sir PDFDocument41 pagesSCM & PE Theory Book by Dani Sir PDFJai ModiNo ratings yet

- (2023) 147 Taxmann - Com 449 (Nagpur - Trib.) (07-10-2022) Krushi Vibhag Karmchari Vrund Sahakari Pat Sanstha Maryadit vs. Income-Tax OfficerDocument6 pages(2023) 147 Taxmann - Com 449 (Nagpur - Trib.) (07-10-2022) Krushi Vibhag Karmchari Vrund Sahakari Pat Sanstha Maryadit vs. Income-Tax OfficerJai ModiNo ratings yet

- Samier AC 2017 Islamic Public Administration Tradition Historical TheoreticalDocument19 pagesSamier AC 2017 Islamic Public Administration Tradition Historical TheoreticalJunaid AliNo ratings yet

- Jurisidiction of Courts in Criminal ProcedureDocument5 pagesJurisidiction of Courts in Criminal ProcedurePéddiéGréiéNo ratings yet

- Quant Checklist 424 by Aashish Arora For Bank Exams 2023Document107 pagesQuant Checklist 424 by Aashish Arora For Bank Exams 2023saurabh.rasse2409No ratings yet

- Java Exam Preparation Model TestnDocument8 pagesJava Exam Preparation Model TestnLindiNo ratings yet

- Developing Living Cities From Analysis To Action PDFDocument314 pagesDeveloping Living Cities From Analysis To Action PDFKien VuNo ratings yet

- Pmxavd800 001Document1 pagePmxavd800 001nathan.howNo ratings yet

- 4 6021613740347099891Document18 pages4 6021613740347099891abdiNo ratings yet

- Oil and Natural Gas Corporation Ltd. Vasai East Development ProjectDocument7 pagesOil and Natural Gas Corporation Ltd. Vasai East Development Projectmathew1965No ratings yet

- Creating Activex Controls in VC++Document28 pagesCreating Activex Controls in VC++stalinbalusamyNo ratings yet

- 2024 Filipino English Client Satisfaction Measurement SurveyDocument2 pages2024 Filipino English Client Satisfaction Measurement Surveyjeanylyn anacanNo ratings yet

- A64 Datasheet V1.1 PDFDocument64 pagesA64 Datasheet V1.1 PDFpedisoj465No ratings yet

- TLE - AFA - FISH - PROCESSING 7 - 8 - w3Document4 pagesTLE - AFA - FISH - PROCESSING 7 - 8 - w3Marilyn Lamigo Bristol100% (1)

- KG30 SupremeManual 12-26-12 CompleteDocument116 pagesKG30 SupremeManual 12-26-12 CompleteDavid Oswaldo Nino BohorquezNo ratings yet

- 3 s2.0 B9780128211397002233 Main PDFDocument8 pages3 s2.0 B9780128211397002233 Main PDFJulio Cesar de SouzaNo ratings yet

- Bootable USB Pen Drive Has Many Advantages Over Other Boot DrivesDocument3 pagesBootable USB Pen Drive Has Many Advantages Over Other Boot DrivesDebaditya ChakrabortyNo ratings yet

- Annex 11 Monitoring and Evaluation ToolDocument6 pagesAnnex 11 Monitoring and Evaluation ToolKathrine Jane LunaNo ratings yet

- Rear Suspension: Group 34Document6 pagesRear Suspension: Group 34Davit OmegaNo ratings yet

- XE700D液压挖掘机技术规格书Document22 pagesXE700D液压挖掘机技术规格书abangNo ratings yet

- 9.igtr Aurangabad MCCM QualfileDocument23 pages9.igtr Aurangabad MCCM QualfilewarekarNo ratings yet

- Basic College Mathematics 9th Edition Lial Test Bank 1Document39 pagesBasic College Mathematics 9th Edition Lial Test Bank 1james100% (38)

- A Research Study of A Three Commercial BuildingDocument12 pagesA Research Study of A Three Commercial BuildingBianca bayangNo ratings yet

- Ladaga vs. MapaguDocument5 pagesLadaga vs. MapaguGenerosa GenosaNo ratings yet

- 1.python Language Fundamentals PDFDocument31 pages1.python Language Fundamentals PDFPrayas Kb100% (1)

- Event Budget - Scout CampDocument6 pagesEvent Budget - Scout CampBobbyNichols0% (1)

- Mtap Reviewer GR 6 2ND QDocument3 pagesMtap Reviewer GR 6 2ND QMaria Clariza CastilloNo ratings yet

- Research Data Management by DR RC GaurDocument29 pagesResearch Data Management by DR RC Gaursudheer babu arumbakaNo ratings yet

- The Risk of Material Misstatement (RMM) Audit Procedures - Response To Risks & Evaluating The Audit Verification Obtained.Document4 pagesThe Risk of Material Misstatement (RMM) Audit Procedures - Response To Risks & Evaluating The Audit Verification Obtained.Dr.Mohammad Wahid Abdullah KhanNo ratings yet

- BE Form 7 SCHOOL ACCOMPLISHMENT REPORTDocument7 pagesBE Form 7 SCHOOL ACCOMPLISHMENT REPORTRuth LarraquelNo ratings yet

- Review ChapterDocument13 pagesReview ChaptermirosehNo ratings yet

- Craft: CopywritingDocument216 pagesCraft: CopywritingZaborra100% (1)

Download as pdf or txt

You might also like

- Smart Communications, Inc. vs. Municipality of Malvar, BatangasDocument3 pagesSmart Communications, Inc. vs. Municipality of Malvar, BatangasRaquel Doquenia100% (2)

- First Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument9 pagesFirst Division: Republic of The Philippines Court of Tax Appeals Quezon CityAemie JordanNo ratings yet

- Instructions For The Transferee (Buyer)Document1 pageInstructions For The Transferee (Buyer)Devu GautamNo ratings yet

- Cir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Document8 pagesCir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Cristy Yaun-CabagnotNo ratings yet

- Kusum Gupta v. ITO (Delhi HC)Document6 pagesKusum Gupta v. ITO (Delhi HC)Avar LambaNo ratings yet

- 213037-2018-Coca-Cola Bottlers Philippines Inc. V.Document11 pages213037-2018-Coca-Cola Bottlers Philippines Inc. V.CamshtNo ratings yet

- Chargeback Card InternetDocument16 pagesChargeback Card InternetFlaviub23No ratings yet

- COMMISSIONER OF INTERNAL REVENUE Vs METRO STAR SUPERAMADocument1 pageCOMMISSIONER OF INTERNAL REVENUE Vs METRO STAR SUPERAMACharles Roger RayaNo ratings yet

- CIR Vs Metro StarDocument4 pagesCIR Vs Metro StarJohnde MartinezNo ratings yet

- Western Mindanao Power Corporation vs. Commissioner of Internal RevenueDocument7 pagesWestern Mindanao Power Corporation vs. Commissioner of Internal RevenueJonjon BeeNo ratings yet

- 10 - CIR v. Yusen Logistics Center, Inc.Document3 pages10 - CIR v. Yusen Logistics Center, Inc.Carlota VillaromanNo ratings yet

- TDS U - S. 194J Not Deductible On Payment For Outright Purchase of Copyright and Technical Know-HowDocument10 pagesTDS U - S. 194J Not Deductible On Payment For Outright Purchase of Copyright and Technical Know-HowheyaanshNo ratings yet

- (2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Document2 pages(2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Jai ModiNo ratings yet

- October 2020 Tax AlertDocument5 pagesOctober 2020 Tax AlertRheneir MoraNo ratings yet

- CTA_2D_CV_09713_A_2020OCT14_ASSDocument8 pagesCTA_2D_CV_09713_A_2020OCT14_ASSPaulNo ratings yet

- 36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0Document10 pages36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0ervingabralagbonNo ratings yet

- Court of Tax Appeal: Chairperson, andDocument19 pagesCourt of Tax Appeal: Chairperson, andJason MergalNo ratings yet

- Revised Concept Papere RegistrationDocument3 pagesRevised Concept Papere RegistrationayanNo ratings yet

- Kuwait Airways Corp. v. Commissioner of Internal RevenueDocument12 pagesKuwait Airways Corp. v. Commissioner of Internal Revenueedcbess23No ratings yet

- Tax Department Takes Up 68,000 Cases For E-Veri Cation: All You Need To Know About e - Veri Cation SchemeDocument3 pagesTax Department Takes Up 68,000 Cases For E-Veri Cation: All You Need To Know About e - Veri Cation SchemeSudhir BhargavaNo ratings yet

- Green Valley Marketing Corp. v. Commissioner of Internal Revenue, C.T.A. Case No. 8988, (November 3, 2017) PDFDocument42 pagesGreen Valley Marketing Corp. v. Commissioner of Internal Revenue, C.T.A. Case No. 8988, (November 3, 2017) PDFKriszan ManiponNo ratings yet

- Demand Pre - Intimation LetterDocument2 pagesDemand Pre - Intimation LetterAMIT TIWARINo ratings yet

- Tax DigestDocument11 pagesTax DigestSarah Jane Fabricante BehigaNo ratings yet

- Smart Communications vs. Municipality of MalvarDocument3 pagesSmart Communications vs. Municipality of MalvarClark Edward Runes Uytico0% (1)

- CIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerDocument15 pagesCIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerSoftdynamiteNo ratings yet

- CIR v. Enron Subic Power CorporationDocument2 pagesCIR v. Enron Subic Power CorporationGain DeeNo ratings yet

- CIR Vs Migrant PagbilaoDocument12 pagesCIR Vs Migrant PagbilaoMelo Ponce de Leon100% (1)

- CIR vs. FitnessByDesign - SCRADocument28 pagesCIR vs. FitnessByDesign - SCRALouis AngelesNo ratings yet

- CIR v. Metro Star SupremaDocument3 pagesCIR v. Metro Star SupremaNichol Uriel ArcaNo ratings yet

- Gross Income CasesDocument80 pagesGross Income CasesapperdapperNo ratings yet

- FAN Without PAN Violates Due Process - ArticleDocument3 pagesFAN Without PAN Violates Due Process - ArticleCkey ArNo ratings yet

- CTA Case No. 24 (CTA Case No 6170)Document7 pagesCTA Case No. 24 (CTA Case No 6170)Jeffrey JosolNo ratings yet

- Research On NIRCDocument6 pagesResearch On NIRCFrancis RubioNo ratings yet

- Understanding Electronic Invoicing System in The PhilippinesDocument27 pagesUnderstanding Electronic Invoicing System in The PhilippinesSUMIT KUMAR AGARWALANo ratings yet

- Cta 3D Ac 00248 D 2023apr19 OthDocument14 pagesCta 3D Ac 00248 D 2023apr19 OthFirenze PHNo ratings yet

- Excess Input Tax or Creditable Input: - Second DivisionDocument29 pagesExcess Input Tax or Creditable Input: - Second DivisionAsHervea AbanteNo ratings yet

- (Rajasthan) / (2022) 447 ITR 698 (Rajasthan) (29-06-2022)Document6 pages(Rajasthan) / (2022) 447 ITR 698 (Rajasthan) (29-06-2022)rigiyanNo ratings yet

- E-Way Bill Under GST (Nmims)Document8 pagesE-Way Bill Under GST (Nmims)Mitali BiswasNo ratings yet

- Sec 68 - Case LawsDocument2 pagesSec 68 - Case LawsShreNo ratings yet

- Calcutta Discount Co. Ltd. v. ITO: (1961) 41 ITR 191 (SC) (1967) 63 ITR 219 (SC)Document6 pagesCalcutta Discount Co. Ltd. v. ITO: (1961) 41 ITR 191 (SC) (1967) 63 ITR 219 (SC)rigiyanNo ratings yet

- RemediesDocument36 pagesRemediesDaryll Gayle AsuncionNo ratings yet

- SC Tax Decision2Document45 pagesSC Tax Decision2Jasreel DomasingNo ratings yet

- CIR Vs First ExpressDocument7 pagesCIR Vs First ExpressGhreighz GalinatoNo ratings yet

- Electronic Way BillDocument6 pagesElectronic Way BillKumariNo ratings yet

- Assam Instruction No. 13 2023 GSTDocument2 pagesAssam Instruction No. 13 2023 GSTCA Kaushik Ranjan GoswamiNo ratings yet

- Qatar Airways Vs Cir 2020 Case DigestDocument2 pagesQatar Airways Vs Cir 2020 Case DigestJunia Dungaya100% (1)

- CIR V Eron Subic PowerDocument5 pagesCIR V Eron Subic PowerYoo Si JinNo ratings yet

- Cir Vs Metro Super Rama DigestDocument2 pagesCir Vs Metro Super Rama DigestKobe BryantNo ratings yet

- CIR vs. Eron Subic Power CorporationDocument5 pagesCIR vs. Eron Subic Power CorporationJohn FerarenNo ratings yet

- UntitledDocument5 pagesUntitledharsh hgNo ratings yet

- Unit 18Document20 pagesUnit 18Raja SahilNo ratings yet

- Petitioner's Arguments:: The IssueDocument19 pagesPetitioner's Arguments:: The IssueBarnie BingNo ratings yet

- CIR v. Spouses Magaan, G.R. No. 232663, May 3, 2021Document2 pagesCIR v. Spouses Magaan, G.R. No. 232663, May 3, 2021John Cyrus DangananNo ratings yet

- 2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioDocument7 pages2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioThe Chartered Professional NewsletterNo ratings yet

- CIR Vs Isabela Cultural Corporation (ICC)Document11 pagesCIR Vs Isabela Cultural Corporation (ICC)Victor LimNo ratings yet

- FAN Without PAN Violates Due ProcessDocument2 pagesFAN Without PAN Violates Due ProcessDesiree SencoNo ratings yet

- Cir v. Mirant Pagbilao CorporationDocument16 pagesCir v. Mirant Pagbilao CorporationSiobhan RobinNo ratings yet

- Taxation Doctrines 2Document18 pagesTaxation Doctrines 2KCNo ratings yet

- Bank of America NT & Sa, The Commissioner of Internal RevenueDocument4 pagesBank of America NT & Sa, The Commissioner of Internal RevenueHADTUGINo ratings yet

- 21St Century Computer Solutions: A Manual Accounting SimulationFrom Everand21St Century Computer Solutions: A Manual Accounting SimulationNo ratings yet

- (2023) 148 Taxmann - Com 185 (Bombay) (08-03-2023) Jetair (P.) Ltd. vs. Deputy Commissioner of Income-Tax Central Circle-5Document1 page(2023) 148 Taxmann - Com 185 (Bombay) (08-03-2023) Jetair (P.) Ltd. vs. Deputy Commissioner of Income-Tax Central Circle-5Jai ModiNo ratings yet

- (2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Document2 pages(2023) 147 Taxmann - Com 440 (Calcutta) (28-11-2022) Principal Commissioner of Income-Tax vs. Bridge and Building Construction Co. (P.) Ltd.Jai ModiNo ratings yet

- Government of India Ministry of Finance Department of Revenue Central Board of Direct TaxesDocument1 pageGovernment of India Ministry of Finance Department of Revenue Central Board of Direct TaxesJai ModiNo ratings yet

- V K SubramaniDocument4 pagesV K SubramaniJai ModiNo ratings yet

- Government of India Ministry of Finance Department of Revenue Central Board of Direct TaxesDocument2 pagesGovernment of India Ministry of Finance Department of Revenue Central Board of Direct TaxesJai ModiNo ratings yet

- (2023) 147 Taxmann - Com 446 (Raipur - Trib.) - (2022) 100 ITR (T) 195 (Raipur - Trib.) (26-07-2022) Assistant Commissioner of Income-Tax vs. Sanjay Kumar KocharDocument16 pages(2023) 147 Taxmann - Com 446 (Raipur - Trib.) - (2022) 100 ITR (T) 195 (Raipur - Trib.) (26-07-2022) Assistant Commissioner of Income-Tax vs. Sanjay Kumar KocharJai ModiNo ratings yet

- SCM & PE Theory Book by Dani Sir PDFDocument41 pagesSCM & PE Theory Book by Dani Sir PDFJai ModiNo ratings yet

- (2023) 147 Taxmann - Com 449 (Nagpur - Trib.) (07-10-2022) Krushi Vibhag Karmchari Vrund Sahakari Pat Sanstha Maryadit vs. Income-Tax OfficerDocument6 pages(2023) 147 Taxmann - Com 449 (Nagpur - Trib.) (07-10-2022) Krushi Vibhag Karmchari Vrund Sahakari Pat Sanstha Maryadit vs. Income-Tax OfficerJai ModiNo ratings yet

- Samier AC 2017 Islamic Public Administration Tradition Historical TheoreticalDocument19 pagesSamier AC 2017 Islamic Public Administration Tradition Historical TheoreticalJunaid AliNo ratings yet

- Jurisidiction of Courts in Criminal ProcedureDocument5 pagesJurisidiction of Courts in Criminal ProcedurePéddiéGréiéNo ratings yet

- Quant Checklist 424 by Aashish Arora For Bank Exams 2023Document107 pagesQuant Checklist 424 by Aashish Arora For Bank Exams 2023saurabh.rasse2409No ratings yet

- Java Exam Preparation Model TestnDocument8 pagesJava Exam Preparation Model TestnLindiNo ratings yet

- Developing Living Cities From Analysis To Action PDFDocument314 pagesDeveloping Living Cities From Analysis To Action PDFKien VuNo ratings yet

- Pmxavd800 001Document1 pagePmxavd800 001nathan.howNo ratings yet

- 4 6021613740347099891Document18 pages4 6021613740347099891abdiNo ratings yet

- Oil and Natural Gas Corporation Ltd. Vasai East Development ProjectDocument7 pagesOil and Natural Gas Corporation Ltd. Vasai East Development Projectmathew1965No ratings yet

- Creating Activex Controls in VC++Document28 pagesCreating Activex Controls in VC++stalinbalusamyNo ratings yet

- 2024 Filipino English Client Satisfaction Measurement SurveyDocument2 pages2024 Filipino English Client Satisfaction Measurement Surveyjeanylyn anacanNo ratings yet

- A64 Datasheet V1.1 PDFDocument64 pagesA64 Datasheet V1.1 PDFpedisoj465No ratings yet

- TLE - AFA - FISH - PROCESSING 7 - 8 - w3Document4 pagesTLE - AFA - FISH - PROCESSING 7 - 8 - w3Marilyn Lamigo Bristol100% (1)

- KG30 SupremeManual 12-26-12 CompleteDocument116 pagesKG30 SupremeManual 12-26-12 CompleteDavid Oswaldo Nino BohorquezNo ratings yet

- 3 s2.0 B9780128211397002233 Main PDFDocument8 pages3 s2.0 B9780128211397002233 Main PDFJulio Cesar de SouzaNo ratings yet

- Bootable USB Pen Drive Has Many Advantages Over Other Boot DrivesDocument3 pagesBootable USB Pen Drive Has Many Advantages Over Other Boot DrivesDebaditya ChakrabortyNo ratings yet

- Annex 11 Monitoring and Evaluation ToolDocument6 pagesAnnex 11 Monitoring and Evaluation ToolKathrine Jane LunaNo ratings yet

- Rear Suspension: Group 34Document6 pagesRear Suspension: Group 34Davit OmegaNo ratings yet

- XE700D液压挖掘机技术规格书Document22 pagesXE700D液压挖掘机技术规格书abangNo ratings yet

- 9.igtr Aurangabad MCCM QualfileDocument23 pages9.igtr Aurangabad MCCM QualfilewarekarNo ratings yet

- Basic College Mathematics 9th Edition Lial Test Bank 1Document39 pagesBasic College Mathematics 9th Edition Lial Test Bank 1james100% (38)

- A Research Study of A Three Commercial BuildingDocument12 pagesA Research Study of A Three Commercial BuildingBianca bayangNo ratings yet

- Ladaga vs. MapaguDocument5 pagesLadaga vs. MapaguGenerosa GenosaNo ratings yet

- 1.python Language Fundamentals PDFDocument31 pages1.python Language Fundamentals PDFPrayas Kb100% (1)

- Event Budget - Scout CampDocument6 pagesEvent Budget - Scout CampBobbyNichols0% (1)

- Mtap Reviewer GR 6 2ND QDocument3 pagesMtap Reviewer GR 6 2ND QMaria Clariza CastilloNo ratings yet

- Research Data Management by DR RC GaurDocument29 pagesResearch Data Management by DR RC Gaursudheer babu arumbakaNo ratings yet

- The Risk of Material Misstatement (RMM) Audit Procedures - Response To Risks & Evaluating The Audit Verification Obtained.Document4 pagesThe Risk of Material Misstatement (RMM) Audit Procedures - Response To Risks & Evaluating The Audit Verification Obtained.Dr.Mohammad Wahid Abdullah KhanNo ratings yet

- BE Form 7 SCHOOL ACCOMPLISHMENT REPORTDocument7 pagesBE Form 7 SCHOOL ACCOMPLISHMENT REPORTRuth LarraquelNo ratings yet

- Review ChapterDocument13 pagesReview ChaptermirosehNo ratings yet

- Craft: CopywritingDocument216 pagesCraft: CopywritingZaborra100% (1)