Template 26 Internal Audit Planning Memorandum

Template 26 Internal Audit Planning Memorandum

You might also like

- Linear System Theory 2 e SolDocument106 pagesLinear System Theory 2 e SolShruti Mahadik78% (23)

- Audit Planning MemoDocument9 pagesAudit Planning MemoJerald Oliver Macabaya100% (1)

- Audit Planning MemoDocument10 pagesAudit Planning MemoChyrra ALed ZuRc100% (3)

- Audit Planning Memo - SampleDocument11 pagesAudit Planning Memo - SampleAsh100% (1)

- Audit Planning and Risk Assessment New SlidesDocument38 pagesAudit Planning and Risk Assessment New SlidesAdeel AhmadNo ratings yet

- BSBMGT517 Assessment 1 - Short AnswerDocument12 pagesBSBMGT517 Assessment 1 - Short AnswerThayse CarrijoNo ratings yet

- 141 ISACA NACACS Auditing IT Projects Audit ProgramDocument85 pages141 ISACA NACACS Auditing IT Projects Audit ProgramkirwanicholasNo ratings yet

- Audit ProcessDocument2 pagesAudit Processrajahmati_28No ratings yet

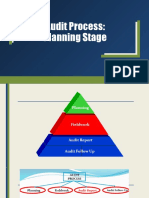

- Audit Process: Planning StageDocument25 pagesAudit Process: Planning StageNelsie Grace PinedaNo ratings yet

- Audit PlanDocument3 pagesAudit PlanMin JeeNo ratings yet

- Checklist For Standards On Internal Audit ( Sia')Document12 pagesChecklist For Standards On Internal Audit ( Sia')VaspeoNo ratings yet

- Performing Internal AuditDocument16 pagesPerforming Internal AuditLaksamanaNo ratings yet

- Unit 7 - Audit CompletionDocument36 pagesUnit 7 - Audit CompletionOlivia HenryNo ratings yet

- Audit PlanningDocument9 pagesAudit PlanninggumiNo ratings yet

- Manual On Internal AuditDocument178 pagesManual On Internal AuditVirencarpediem100% (8)

- SP Audit Plan For SMEDocument8 pagesSP Audit Plan For SMEChiah ChyiNo ratings yet

- Planning FileDocument64 pagesPlanning FileMian Tahir WaseemNo ratings yet

- Manual of Internal AuditDocument178 pagesManual of Internal AuditRahul Dhanwate100% (1)

- BAICS AppendixesDocument7 pagesBAICS AppendixesDenmark CostanillaNo ratings yet

- Audit Process IsasDocument96 pagesAudit Process Isastaniy87100% (1)

- Audit Process: Here Click HereDocument3 pagesAudit Process: Here Click HereShailesh Gosai100% (1)

- Cpa Review School of The Philippines: Related Psas: Psa 300, 310, 320, 520 and 570Document5 pagesCpa Review School of The Philippines: Related Psas: Psa 300, 310, 320, 520 and 570Ma Yra YmataNo ratings yet

- Fish Bone DiagramDocument4 pagesFish Bone DiagramPatrice Elaine PillaNo ratings yet

- Chapter FourDocument16 pagesChapter FourGebrekiros ArayaNo ratings yet

- FAM Points - Ch9Document37 pagesFAM Points - Ch9ALISA ASIFNo ratings yet

- 1.5 Iacop Audit Planning Guidance 3 06 18Document16 pages1.5 Iacop Audit Planning Guidance 3 06 18lakshman1234sterNo ratings yet

- Performing Effective Internal AuditsDocument6 pagesPerforming Effective Internal Auditseskelapamudah enakNo ratings yet

- 141 ISACA NACACS Auditing IT Projects Audit ProgramDocument86 pages141 ISACA NACACS Auditing IT Projects Audit Programkautaliya100% (6)

- Audit ProcessDocument4 pagesAudit ProcessNyakashaiaja kennethNo ratings yet

- Audit Program: A. Planning and Administration SectionDocument3 pagesAudit Program: A. Planning and Administration SectionIzZa Rivera0% (1)

- How To Prepare An Audit PlanDocument8 pagesHow To Prepare An Audit PlanJay Ann100% (1)

- Form 4Document18 pagesForm 4JULLIE CARMELLE H. CHATTONo ratings yet

- Internal Audit DocumentsDocument9 pagesInternal Audit DocumentsAnonymous iI88LtNo ratings yet

- Audit Report Form Stage 2Document11 pagesAudit Report Form Stage 2muthuswamy77No ratings yet

- Year Ended - : Wire DisbursementsDocument7 pagesYear Ended - : Wire DisbursementsChinh Le DinhNo ratings yet

- Annex 4.4 Audit Report Template (Model)Document45 pagesAnnex 4.4 Audit Report Template (Model)Gideon HilardeNo ratings yet

- AUDITING PRINCIPLE Complete-Diploma Notes 2020Document153 pagesAUDITING PRINCIPLE Complete-Diploma Notes 2020Kethia Kahashi100% (1)

- ACCT3014 Lecture12 s12013Document41 pagesACCT3014 Lecture12 s12013thomashong313No ratings yet

- A. Planning: Audit ObjectivesDocument5 pagesA. Planning: Audit ObjectivesChinh Le DinhNo ratings yet

- Understanding The Audit Process Updated 04-10-08 - PDF VersionDocument2 pagesUnderstanding The Audit Process Updated 04-10-08 - PDF VersionLUTGARD JUNIARDYNo ratings yet

- UGS Corporations Internal Audit ProtocolDocument5 pagesUGS Corporations Internal Audit ProtocolbturkistaniNo ratings yet

- New Audit Plan ISADocument6 pagesNew Audit Plan ISAindrawanNo ratings yet

- NOTES - Audit Planning and Analytical ProceduresDocument9 pagesNOTES - Audit Planning and Analytical ProceduresDahlia BloomsNo ratings yet

- Audit PlanningDocument15 pagesAudit Planningemc2_mcv75% (4)

- Project CycleDocument14 pagesProject CycleMohsin HossainNo ratings yet

- Unit 2 Audit ProcessDocument5 pagesUnit 2 Audit ProcessGokul.S 20BCP0010No ratings yet

- ACT 380 - Major Final Assignment Spring 2020Document13 pagesACT 380 - Major Final Assignment Spring 2020Jesin Estiana100% (1)

- Auditing and Assurance-Pdf-1Document236 pagesAuditing and Assurance-Pdf-1Thomas Kungu100% (1)

- Completing The AuditDocument5 pagesCompleting The Auditmrs leeNo ratings yet

- Business Case TemplateDocument9 pagesBusiness Case TemplateVenkatesh NenavathNo ratings yet

- TOPIC 4 Audit Planning - Part 1 & 2Document57 pagesTOPIC 4 Audit Planning - Part 1 & 2SITI HAMIZAH HAMZAHNo ratings yet

- Study Guide - PrelimDocument3 pagesStudy Guide - PrelimGellie Vale T. ManagbanagNo ratings yet

- Chapter 3 AudDocument17 pagesChapter 3 AudMoti BekeleNo ratings yet

- Group 8 Internal AuditingDocument7 pagesGroup 8 Internal AuditingZakyaNo ratings yet

- 3 Audit PlanningDocument16 pages3 Audit PlanningHussain MustunNo ratings yet

- Allama Iqbal Open University: MBA Banking & FinanceDocument22 pagesAllama Iqbal Open University: MBA Banking & FinanceawaisleoNo ratings yet

- At.1609 - Audit Planning - An OverviewDocument6 pagesAt.1609 - Audit Planning - An Overviewnaztig_017No ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Audit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19From EverandAudit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19No ratings yet

- WYPFJAG31 Jan Doc AGAPPDocument16 pagesWYPFJAG31 Jan Doc AGAPPNajihah Che MatNo ratings yet

- LCRCA Audit Strategy Memorandum 2020-21Document36 pagesLCRCA Audit Strategy Memorandum 2020-21Najihah Che MatNo ratings yet

- Item 7.0 Transport For The North Audit Strategy Memorandum 2018 19Document19 pagesItem 7.0 Transport For The North Audit Strategy Memorandum 2018 19Najihah Che MatNo ratings yet

- External Auditor - Audit Strategy MemorandumsDocument34 pagesExternal Auditor - Audit Strategy MemorandumsNajihah Che MatNo ratings yet

- 08 2019 20 External Audit Strategy Memorandum - 0Document24 pages08 2019 20 External Audit Strategy Memorandum - 0Najihah Che Mat100% (1)

- DCC Audit Strategy MemorandumDocument16 pagesDCC Audit Strategy MemorandumNajihah Che MatNo ratings yet

- Barking Up The Wrong Tree. OnDocument14 pagesBarking Up The Wrong Tree. OnTimothy HulsingaNo ratings yet

- 824pm - 22.EPRA JOURNALS 15646Document7 pages824pm - 22.EPRA JOURNALS 15646garimanevtiyaNo ratings yet

- HRD Audit and Its MethodologyDocument21 pagesHRD Audit and Its MethodologyAbhinandan ⎝⏠⏝⏝⏠⎠ Seth0% (2)

- Roadscholarb16 1Document1 pageRoadscholarb16 1api-282829097No ratings yet

- An Exploratory Research On Customer Satisfaction of Super Shop in Bangladesh''Document23 pagesAn Exploratory Research On Customer Satisfaction of Super Shop in Bangladesh''এ.বি.এস. আশিকNo ratings yet

- Safe Staffing Literature Review AnaDocument9 pagesSafe Staffing Literature Review Anac5sd1aqj100% (1)

- Effects of Career-Related Continuous LearningDocument13 pagesEffects of Career-Related Continuous Learningsachin_kheraNo ratings yet

- Product Management ReviewerDocument8 pagesProduct Management ReviewerJm Almario BautistaNo ratings yet

- Lecture 3-Speed Studies (Spot Speed)Document11 pagesLecture 3-Speed Studies (Spot Speed)Matt DesignNo ratings yet

- CPP Proc Ug 38 0804Document165 pagesCPP Proc Ug 38 0804janeNo ratings yet

- Human Resource Department Rolein Employee Retention Acasestudyof HRpracticesofbankin NepalDocument20 pagesHuman Resource Department Rolein Employee Retention Acasestudyof HRpracticesofbankin NepalAnup AcharyaNo ratings yet

- The Myth of The Absent Black Father - ThinkProgress PDFDocument4 pagesThe Myth of The Absent Black Father - ThinkProgress PDFBishara WilsonNo ratings yet

- Taiwan Island and Sister Cities Paradipl PDFDocument38 pagesTaiwan Island and Sister Cities Paradipl PDFReyhan Muhammad FachryNo ratings yet

- MMPC-005 Quantitative AnalysisDocument4 pagesMMPC-005 Quantitative Analysisbhavan pNo ratings yet

- The Influence of Emotional Intelligence On Job Burnout and Job Performance Mediating Effect of Psychological CapitalDocument11 pagesThe Influence of Emotional Intelligence On Job Burnout and Job Performance Mediating Effect of Psychological Capitalcem hocaNo ratings yet

- Ch01-Casesstudy For UMADocument3 pagesCh01-Casesstudy For UMAjklbnm12345100% (1)

- Real Statistics Using ExcelprintDocument7 pagesReal Statistics Using Excelprintamin jamalNo ratings yet

- Tasksheet Masters Thesis Padmaja SathiyamoorthyDocument2 pagesTasksheet Masters Thesis Padmaja Sathiyamoorthyumarhayat3587No ratings yet

- Consumer Buying Behavior Towards Two-Wheeler Scooters: With Special Reference To Nagpur City (Maharashtra, India)Document21 pagesConsumer Buying Behavior Towards Two-Wheeler Scooters: With Special Reference To Nagpur City (Maharashtra, India)Padmakar ShahareNo ratings yet

- The Professional Competence of Teachers: Which Qualities, Attitudes, Skills and Knowledge Contribute To A Teacher's Effectiveness?Document21 pagesThe Professional Competence of Teachers: Which Qualities, Attitudes, Skills and Knowledge Contribute To A Teacher's Effectiveness?karl credoNo ratings yet

- Stat 202: Hypothesis Testing Practice ProblemsDocument3 pagesStat 202: Hypothesis Testing Practice ProblemsBao GanNo ratings yet

- PJC h2 Math p2 SolutionsDocument7 pagesPJC h2 Math p2 SolutionsjimmytanlimlongNo ratings yet

- Pertmaster Risk RegisterDocument8 pagesPertmaster Risk RegisterDhanes PratitaNo ratings yet

- Chi-Square of Independence Araza, Gulferic, LucabanDocument39 pagesChi-Square of Independence Araza, Gulferic, LucabanVenusNo ratings yet

- CK 12 Basic Algebra Concepts B v16 Jli s1Document780 pagesCK 12 Basic Algebra Concepts B v16 Jli s1Phil Beckett100% (1)

- Advertising Ethics and Viewers Perception Towards Surrogate AdvertisingDocument66 pagesAdvertising Ethics and Viewers Perception Towards Surrogate AdvertisingSrijith ShivanNo ratings yet

- Traumatic Intracerebral Hemorrhage: Risk Factors Associated With ProgressionDocument35 pagesTraumatic Intracerebral Hemorrhage: Risk Factors Associated With ProgressionPavel SebastianNo ratings yet

- The Relation Between Customers and Brand Equity (Unilever-Lux)Document76 pagesThe Relation Between Customers and Brand Equity (Unilever-Lux)gl101100% (3)

- 4332bQAM601 - Statistics For ManagementDocument6 pages4332bQAM601 - Statistics For ManagementvickkyNo ratings yet

Download as pdf or txt

You might also like

- Linear System Theory 2 e SolDocument106 pagesLinear System Theory 2 e SolShruti Mahadik78% (23)

- Audit Planning MemoDocument9 pagesAudit Planning MemoJerald Oliver Macabaya100% (1)

- Audit Planning MemoDocument10 pagesAudit Planning MemoChyrra ALed ZuRc100% (3)

- Audit Planning Memo - SampleDocument11 pagesAudit Planning Memo - SampleAsh100% (1)

- Audit Planning and Risk Assessment New SlidesDocument38 pagesAudit Planning and Risk Assessment New SlidesAdeel AhmadNo ratings yet

- BSBMGT517 Assessment 1 - Short AnswerDocument12 pagesBSBMGT517 Assessment 1 - Short AnswerThayse CarrijoNo ratings yet

- 141 ISACA NACACS Auditing IT Projects Audit ProgramDocument85 pages141 ISACA NACACS Auditing IT Projects Audit ProgramkirwanicholasNo ratings yet

- Audit ProcessDocument2 pagesAudit Processrajahmati_28No ratings yet

- Audit Process: Planning StageDocument25 pagesAudit Process: Planning StageNelsie Grace PinedaNo ratings yet

- Audit PlanDocument3 pagesAudit PlanMin JeeNo ratings yet

- Checklist For Standards On Internal Audit ( Sia')Document12 pagesChecklist For Standards On Internal Audit ( Sia')VaspeoNo ratings yet

- Performing Internal AuditDocument16 pagesPerforming Internal AuditLaksamanaNo ratings yet

- Unit 7 - Audit CompletionDocument36 pagesUnit 7 - Audit CompletionOlivia HenryNo ratings yet

- Audit PlanningDocument9 pagesAudit PlanninggumiNo ratings yet

- Manual On Internal AuditDocument178 pagesManual On Internal AuditVirencarpediem100% (8)

- SP Audit Plan For SMEDocument8 pagesSP Audit Plan For SMEChiah ChyiNo ratings yet

- Planning FileDocument64 pagesPlanning FileMian Tahir WaseemNo ratings yet

- Manual of Internal AuditDocument178 pagesManual of Internal AuditRahul Dhanwate100% (1)

- BAICS AppendixesDocument7 pagesBAICS AppendixesDenmark CostanillaNo ratings yet

- Audit Process IsasDocument96 pagesAudit Process Isastaniy87100% (1)

- Audit Process: Here Click HereDocument3 pagesAudit Process: Here Click HereShailesh Gosai100% (1)

- Cpa Review School of The Philippines: Related Psas: Psa 300, 310, 320, 520 and 570Document5 pagesCpa Review School of The Philippines: Related Psas: Psa 300, 310, 320, 520 and 570Ma Yra YmataNo ratings yet

- Fish Bone DiagramDocument4 pagesFish Bone DiagramPatrice Elaine PillaNo ratings yet

- Chapter FourDocument16 pagesChapter FourGebrekiros ArayaNo ratings yet

- FAM Points - Ch9Document37 pagesFAM Points - Ch9ALISA ASIFNo ratings yet

- 1.5 Iacop Audit Planning Guidance 3 06 18Document16 pages1.5 Iacop Audit Planning Guidance 3 06 18lakshman1234sterNo ratings yet

- Performing Effective Internal AuditsDocument6 pagesPerforming Effective Internal Auditseskelapamudah enakNo ratings yet

- 141 ISACA NACACS Auditing IT Projects Audit ProgramDocument86 pages141 ISACA NACACS Auditing IT Projects Audit Programkautaliya100% (6)

- Audit ProcessDocument4 pagesAudit ProcessNyakashaiaja kennethNo ratings yet

- Audit Program: A. Planning and Administration SectionDocument3 pagesAudit Program: A. Planning and Administration SectionIzZa Rivera0% (1)

- How To Prepare An Audit PlanDocument8 pagesHow To Prepare An Audit PlanJay Ann100% (1)

- Form 4Document18 pagesForm 4JULLIE CARMELLE H. CHATTONo ratings yet

- Internal Audit DocumentsDocument9 pagesInternal Audit DocumentsAnonymous iI88LtNo ratings yet

- Audit Report Form Stage 2Document11 pagesAudit Report Form Stage 2muthuswamy77No ratings yet

- Year Ended - : Wire DisbursementsDocument7 pagesYear Ended - : Wire DisbursementsChinh Le DinhNo ratings yet

- Annex 4.4 Audit Report Template (Model)Document45 pagesAnnex 4.4 Audit Report Template (Model)Gideon HilardeNo ratings yet

- AUDITING PRINCIPLE Complete-Diploma Notes 2020Document153 pagesAUDITING PRINCIPLE Complete-Diploma Notes 2020Kethia Kahashi100% (1)

- ACCT3014 Lecture12 s12013Document41 pagesACCT3014 Lecture12 s12013thomashong313No ratings yet

- A. Planning: Audit ObjectivesDocument5 pagesA. Planning: Audit ObjectivesChinh Le DinhNo ratings yet

- Understanding The Audit Process Updated 04-10-08 - PDF VersionDocument2 pagesUnderstanding The Audit Process Updated 04-10-08 - PDF VersionLUTGARD JUNIARDYNo ratings yet

- UGS Corporations Internal Audit ProtocolDocument5 pagesUGS Corporations Internal Audit ProtocolbturkistaniNo ratings yet

- New Audit Plan ISADocument6 pagesNew Audit Plan ISAindrawanNo ratings yet

- NOTES - Audit Planning and Analytical ProceduresDocument9 pagesNOTES - Audit Planning and Analytical ProceduresDahlia BloomsNo ratings yet

- Audit PlanningDocument15 pagesAudit Planningemc2_mcv75% (4)

- Project CycleDocument14 pagesProject CycleMohsin HossainNo ratings yet

- Unit 2 Audit ProcessDocument5 pagesUnit 2 Audit ProcessGokul.S 20BCP0010No ratings yet

- ACT 380 - Major Final Assignment Spring 2020Document13 pagesACT 380 - Major Final Assignment Spring 2020Jesin Estiana100% (1)

- Auditing and Assurance-Pdf-1Document236 pagesAuditing and Assurance-Pdf-1Thomas Kungu100% (1)

- Completing The AuditDocument5 pagesCompleting The Auditmrs leeNo ratings yet

- Business Case TemplateDocument9 pagesBusiness Case TemplateVenkatesh NenavathNo ratings yet

- TOPIC 4 Audit Planning - Part 1 & 2Document57 pagesTOPIC 4 Audit Planning - Part 1 & 2SITI HAMIZAH HAMZAHNo ratings yet

- Study Guide - PrelimDocument3 pagesStudy Guide - PrelimGellie Vale T. ManagbanagNo ratings yet

- Chapter 3 AudDocument17 pagesChapter 3 AudMoti BekeleNo ratings yet

- Group 8 Internal AuditingDocument7 pagesGroup 8 Internal AuditingZakyaNo ratings yet

- 3 Audit PlanningDocument16 pages3 Audit PlanningHussain MustunNo ratings yet

- Allama Iqbal Open University: MBA Banking & FinanceDocument22 pagesAllama Iqbal Open University: MBA Banking & FinanceawaisleoNo ratings yet

- At.1609 - Audit Planning - An OverviewDocument6 pagesAt.1609 - Audit Planning - An Overviewnaztig_017No ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Audit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19From EverandAudit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19No ratings yet

- WYPFJAG31 Jan Doc AGAPPDocument16 pagesWYPFJAG31 Jan Doc AGAPPNajihah Che MatNo ratings yet

- LCRCA Audit Strategy Memorandum 2020-21Document36 pagesLCRCA Audit Strategy Memorandum 2020-21Najihah Che MatNo ratings yet

- Item 7.0 Transport For The North Audit Strategy Memorandum 2018 19Document19 pagesItem 7.0 Transport For The North Audit Strategy Memorandum 2018 19Najihah Che MatNo ratings yet

- External Auditor - Audit Strategy MemorandumsDocument34 pagesExternal Auditor - Audit Strategy MemorandumsNajihah Che MatNo ratings yet

- 08 2019 20 External Audit Strategy Memorandum - 0Document24 pages08 2019 20 External Audit Strategy Memorandum - 0Najihah Che Mat100% (1)

- DCC Audit Strategy MemorandumDocument16 pagesDCC Audit Strategy MemorandumNajihah Che MatNo ratings yet

- Barking Up The Wrong Tree. OnDocument14 pagesBarking Up The Wrong Tree. OnTimothy HulsingaNo ratings yet

- 824pm - 22.EPRA JOURNALS 15646Document7 pages824pm - 22.EPRA JOURNALS 15646garimanevtiyaNo ratings yet

- HRD Audit and Its MethodologyDocument21 pagesHRD Audit and Its MethodologyAbhinandan ⎝⏠⏝⏝⏠⎠ Seth0% (2)

- Roadscholarb16 1Document1 pageRoadscholarb16 1api-282829097No ratings yet

- An Exploratory Research On Customer Satisfaction of Super Shop in Bangladesh''Document23 pagesAn Exploratory Research On Customer Satisfaction of Super Shop in Bangladesh''এ.বি.এস. আশিকNo ratings yet

- Safe Staffing Literature Review AnaDocument9 pagesSafe Staffing Literature Review Anac5sd1aqj100% (1)

- Effects of Career-Related Continuous LearningDocument13 pagesEffects of Career-Related Continuous Learningsachin_kheraNo ratings yet

- Product Management ReviewerDocument8 pagesProduct Management ReviewerJm Almario BautistaNo ratings yet

- Lecture 3-Speed Studies (Spot Speed)Document11 pagesLecture 3-Speed Studies (Spot Speed)Matt DesignNo ratings yet

- CPP Proc Ug 38 0804Document165 pagesCPP Proc Ug 38 0804janeNo ratings yet

- Human Resource Department Rolein Employee Retention Acasestudyof HRpracticesofbankin NepalDocument20 pagesHuman Resource Department Rolein Employee Retention Acasestudyof HRpracticesofbankin NepalAnup AcharyaNo ratings yet

- The Myth of The Absent Black Father - ThinkProgress PDFDocument4 pagesThe Myth of The Absent Black Father - ThinkProgress PDFBishara WilsonNo ratings yet

- Taiwan Island and Sister Cities Paradipl PDFDocument38 pagesTaiwan Island and Sister Cities Paradipl PDFReyhan Muhammad FachryNo ratings yet

- MMPC-005 Quantitative AnalysisDocument4 pagesMMPC-005 Quantitative Analysisbhavan pNo ratings yet

- The Influence of Emotional Intelligence On Job Burnout and Job Performance Mediating Effect of Psychological CapitalDocument11 pagesThe Influence of Emotional Intelligence On Job Burnout and Job Performance Mediating Effect of Psychological Capitalcem hocaNo ratings yet

- Ch01-Casesstudy For UMADocument3 pagesCh01-Casesstudy For UMAjklbnm12345100% (1)

- Real Statistics Using ExcelprintDocument7 pagesReal Statistics Using Excelprintamin jamalNo ratings yet

- Tasksheet Masters Thesis Padmaja SathiyamoorthyDocument2 pagesTasksheet Masters Thesis Padmaja Sathiyamoorthyumarhayat3587No ratings yet

- Consumer Buying Behavior Towards Two-Wheeler Scooters: With Special Reference To Nagpur City (Maharashtra, India)Document21 pagesConsumer Buying Behavior Towards Two-Wheeler Scooters: With Special Reference To Nagpur City (Maharashtra, India)Padmakar ShahareNo ratings yet

- The Professional Competence of Teachers: Which Qualities, Attitudes, Skills and Knowledge Contribute To A Teacher's Effectiveness?Document21 pagesThe Professional Competence of Teachers: Which Qualities, Attitudes, Skills and Knowledge Contribute To A Teacher's Effectiveness?karl credoNo ratings yet

- Stat 202: Hypothesis Testing Practice ProblemsDocument3 pagesStat 202: Hypothesis Testing Practice ProblemsBao GanNo ratings yet

- PJC h2 Math p2 SolutionsDocument7 pagesPJC h2 Math p2 SolutionsjimmytanlimlongNo ratings yet

- Pertmaster Risk RegisterDocument8 pagesPertmaster Risk RegisterDhanes PratitaNo ratings yet

- Chi-Square of Independence Araza, Gulferic, LucabanDocument39 pagesChi-Square of Independence Araza, Gulferic, LucabanVenusNo ratings yet

- CK 12 Basic Algebra Concepts B v16 Jli s1Document780 pagesCK 12 Basic Algebra Concepts B v16 Jli s1Phil Beckett100% (1)

- Advertising Ethics and Viewers Perception Towards Surrogate AdvertisingDocument66 pagesAdvertising Ethics and Viewers Perception Towards Surrogate AdvertisingSrijith ShivanNo ratings yet

- Traumatic Intracerebral Hemorrhage: Risk Factors Associated With ProgressionDocument35 pagesTraumatic Intracerebral Hemorrhage: Risk Factors Associated With ProgressionPavel SebastianNo ratings yet

- The Relation Between Customers and Brand Equity (Unilever-Lux)Document76 pagesThe Relation Between Customers and Brand Equity (Unilever-Lux)gl101100% (3)

- 4332bQAM601 - Statistics For ManagementDocument6 pages4332bQAM601 - Statistics For ManagementvickkyNo ratings yet