Download as pdf or txt

You might also like

- Dokumen - Pub Drafting and Negotiating International Commercial Contracts A Practical Guide With Icc Model Contracts 3nbsped 9284204100 9789284204106Document374 pagesDokumen - Pub Drafting and Negotiating International Commercial Contracts A Practical Guide With Icc Model Contracts 3nbsped 9284204100 9789284204106lavam56223No ratings yet

- International Economics 8th Edition Husted Test BankDocument10 pagesInternational Economics 8th Edition Husted Test Bankjethrodavide6qi100% (28)

- 12-09-2012Document32 pages12-09-2012El Rinos100% (5)

- Solutions Manual To End-of-Chapter QuestionsDocument6 pagesSolutions Manual To End-of-Chapter QuestionsV GeghamyanNo ratings yet

- Bank of AmericaDocument8 pagesBank of AmericaAnne SanvictoresNo ratings yet

- Bleb 298841Document2 pagesBleb 298841DiegoCastilloNo ratings yet

- Amwest Surety Insurance Company v. Republic National Bank, 977 F.2d 122, 4th Cir. (1992)Document13 pagesAmwest Surety Insurance Company v. Republic National Bank, 977 F.2d 122, 4th Cir. (1992)Scribd Government DocsNo ratings yet

- Sound of Market Street, Inc. v. Continental Bank International, 819 F.2d 384, 3rd Cir. (1987)Document15 pagesSound of Market Street, Inc. v. Continental Bank International, 819 F.2d 384, 3rd Cir. (1987)Scribd Government DocsNo ratings yet

- Kerr-Mcgee Chemical Corporation, A Delaware Corporation v. Federal Deposit Insurance Corporation, 872 F.2d 971, 11th Cir. (1989)Document6 pagesKerr-Mcgee Chemical Corporation, A Delaware Corporation v. Federal Deposit Insurance Corporation, 872 F.2d 971, 11th Cir. (1989)Scribd Government DocsNo ratings yet

- Bank of AmericaDocument10 pagesBank of AmericakrnNo ratings yet

- Published United States Court of Appeals For The Fourth CircuitDocument6 pagesPublished United States Court of Appeals For The Fourth CircuitScribd Government DocsNo ratings yet

- The First National Bank and Trust Company of Oklahoma City, Oklahoma v. United States Fidelity and Guaranty Company, A Corporation, and John Fawcett, 347 F.2d 945, 1st Cir. (1965)Document5 pagesThe First National Bank and Trust Company of Oklahoma City, Oklahoma v. United States Fidelity and Guaranty Company, A Corporation, and John Fawcett, 347 F.2d 945, 1st Cir. (1965)Scribd Government DocsNo ratings yet

- First Nat. Bank in Plant City v. Dickinson, 396 U.S. 122 (1969)Document14 pagesFirst Nat. Bank in Plant City v. Dickinson, 396 U.S. 122 (1969)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Tenth CircuitDocument10 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- Consolidated Aluminum Corporation v. Bank of Virginia and Graf-Comm., Inc., 704 F.2d 136, 4th Cir. (1983)Document5 pagesConsolidated Aluminum Corporation v. Bank of Virginia and Graf-Comm., Inc., 704 F.2d 136, 4th Cir. (1983)Scribd Government DocsNo ratings yet

- Bank of America v. Barr, CUMcv-09-207 (Cumberland Super. CT., 2010)Document9 pagesBank of America v. Barr, CUMcv-09-207 (Cumberland Super. CT., 2010)Chris BuckNo ratings yet

- The First National Bank of Alexander City v. Avondale Mills Bevelle Employees Federal Credit Union, in Liquidation, 967 F.2d 556, 1st Cir. (1992)Document7 pagesThe First National Bank of Alexander City v. Avondale Mills Bevelle Employees Federal Credit Union, in Liquidation, 967 F.2d 556, 1st Cir. (1992)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Third CircuitDocument8 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- CaseDocument21 pagesCaseLeeChristineEveAlmiraNo ratings yet

- Cases On Letters of CreditDocument71 pagesCases On Letters of CreditAnonymous aJzKiPCZwNo ratings yet

- Flagship Cruises, Ltd. v. New England Merchants National Bank of Boston, and Chemical Bank, 569 F.2d 699, 1st Cir. (1978)Document8 pagesFlagship Cruises, Ltd. v. New England Merchants National Bank of Boston, and Chemical Bank, 569 F.2d 699, 1st Cir. (1978)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Third CircuitDocument16 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals, Fifth CircuitDocument8 pagesUnited States Court of Appeals, Fifth CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals, Eleventh CircuitDocument12 pagesUnited States Court of Appeals, Eleventh CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals, Tenth CircuitDocument8 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals, Fifth CircuitDocument10 pagesUnited States Court of Appeals, Fifth CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals, Third CircuitDocument20 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Fed. Carr. Cas. P 84,019 McCall Engineering Company, Incorporated v. Federal Express Corporation, 81 F.3d 28, 4th Cir. (1996)Document5 pagesFed. Carr. Cas. P 84,019 McCall Engineering Company, Incorporated v. Federal Express Corporation, 81 F.3d 28, 4th Cir. (1996)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Third CircuitDocument17 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Marino Industries Corp., Cross-Appellee v. The Chase Manhattan Bank, N.A., Cross-Appellant, 686 F.2d 112, 2d Cir. (1982)Document11 pagesMarino Industries Corp., Cross-Appellee v. The Chase Manhattan Bank, N.A., Cross-Appellant, 686 F.2d 112, 2d Cir. (1982)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Tenth CircuitDocument8 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals, Tenth CircuitDocument8 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- 07 Bank of America, NT and SA V Associated Citizens Bank (G.R. No. 141001 - May 21, 2009)Document4 pages07 Bank of America, NT and SA V Associated Citizens Bank (G.R. No. 141001 - May 21, 2009)teepeeNo ratings yet

- United States Court of Appeals, Fifth CircuitDocument14 pagesUnited States Court of Appeals, Fifth CircuitScribd Government DocsNo ratings yet

- M.J.F.M. Kools, Doing Business As Kools de Visser v. Citibank, N.A., 73 F.3d 5, 2d Cir. (1995)Document5 pagesM.J.F.M. Kools, Doing Business As Kools de Visser v. Citibank, N.A., 73 F.3d 5, 2d Cir. (1995)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Third CircuitDocument9 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- BPI V de Reny FabricsDocument5 pagesBPI V de Reny FabricsJan Igor GalinatoNo ratings yet

- FDIC v. Kane, 148 F.3d 36, 1st Cir. (1998)Document6 pagesFDIC v. Kane, 148 F.3d 36, 1st Cir. (1998)Scribd Government DocsNo ratings yet

- Bony V Bruscuelas Robo Attorney Refer To Authorities 3 12Document32 pagesBony V Bruscuelas Robo Attorney Refer To Authorities 3 12John Nehmatallah100% (1)

- United States Court of Appeals, Tenth CircuitDocument5 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals For The Second Circuit: Docket Nos. 98-9269, 98-9270 August Term, 1998Document6 pagesUnited States Court of Appeals For The Second Circuit: Docket Nos. 98-9269, 98-9270 August Term, 1998Scribd Government DocsNo ratings yet

- Banco Nacional de Desarrollo v. Mellon Bank, N.A., Appeal of Banco Nacional de Desarrollo, in No. 83-5247. Appeal of Mellon Bank, N.A., in No. 83-5272, 726 F.2d 87, 3rd Cir. (1984)Document9 pagesBanco Nacional de Desarrollo v. Mellon Bank, N.A., Appeal of Banco Nacional de Desarrollo, in No. 83-5247. Appeal of Mellon Bank, N.A., in No. 83-5272, 726 F.2d 87, 3rd Cir. (1984)Scribd Government DocsNo ratings yet

- Savarin Corporation v. National Bank of Pakistan, and S.H.A. Sharbatly, 447 F.2d 727, 2d Cir. (1971)Document8 pagesSavarin Corporation v. National Bank of Pakistan, and S.H.A. Sharbatly, 447 F.2d 727, 2d Cir. (1971)Scribd Government DocsNo ratings yet

- In Re Softalk Publishing Co., Inc., Debtor. The Webb Company, A Minnesota Corporation v. First City Bank, 856 F.2d 1328, 1st Cir. (1988)Document7 pagesIn Re Softalk Publishing Co., Inc., Debtor. The Webb Company, A Minnesota Corporation v. First City Bank, 856 F.2d 1328, 1st Cir. (1988)Scribd Government DocsNo ratings yet

- Bank of America V CADocument4 pagesBank of America V CAJNMGNo ratings yet

- American Express Co. v. Koerner, 452 U.S. 233 (1981)Document12 pagesAmerican Express Co. v. Koerner, 452 U.S. 233 (1981)Scribd Government DocsNo ratings yet

- United States v. Reader's Digest Association, Inc., 662 F.2d 955, 3rd Cir. (1981)Document23 pagesUnited States v. Reader's Digest Association, Inc., 662 F.2d 955, 3rd Cir. (1981)Scribd Government DocsNo ratings yet

- Bernard A. Schlifke and Harvey Kallick, D/B/A K & S Investments Co., A Partnership v. Seafirst Corp. and Seattle-First National Bank, 866 F.2d 935, 1st Cir. (1989)Document21 pagesBernard A. Schlifke and Harvey Kallick, D/B/A K & S Investments Co., A Partnership v. Seafirst Corp. and Seattle-First National Bank, 866 F.2d 935, 1st Cir. (1989)Scribd Government DocsNo ratings yet

- Philippine National Bank vs. Cua, 861 SCRA 569Document15 pagesPhilippine National Bank vs. Cua, 861 SCRA 569Athena Jeunnesse Mae Martinez TriaNo ratings yet

- G.R. No. 173905 April 23, 2010 ANTHONY L. NG, Petitioner, vs. PEOPLE OF THE PHILIPPINES, RespondentDocument2 pagesG.R. No. 173905 April 23, 2010 ANTHONY L. NG, Petitioner, vs. PEOPLE OF THE PHILIPPINES, RespondentAthena SantosNo ratings yet

- NOT PrecedentialDocument20 pagesNOT PrecedentialScribd Government DocsNo ratings yet

- Special Commercial Laws Digest No. 1Document99 pagesSpecial Commercial Laws Digest No. 1Marie ClemNo ratings yet

- Last AssignmentDocument60 pagesLast AssignmentJun TabuNo ratings yet

- In Re United States of America, Ex Rel. S. Prawer and Company v. Fleet Bank of Maine, 24 F.3d 320, 1st Cir. (1994)Document23 pagesIn Re United States of America, Ex Rel. S. Prawer and Company v. Fleet Bank of Maine, 24 F.3d 320, 1st Cir. (1994)Scribd Government DocsNo ratings yet

- Bangayan vs. RCBCDocument27 pagesBangayan vs. RCBCjonbelzaNo ratings yet

- Federal Deposit Insurance Corporation v. Avery Cashion, III, 4th Cir. (2013)Document33 pagesFederal Deposit Insurance Corporation v. Avery Cashion, III, 4th Cir. (2013)Scribd Government Docs100% (1)

- In Re David Louis Cohn, Debtor. Insurance Company of North America v. David Louis Cohn, 54 F.3d 1108, 3rd Cir. (1995)Document17 pagesIn Re David Louis Cohn, Debtor. Insurance Company of North America v. David Louis Cohn, 54 F.3d 1108, 3rd Cir. (1995)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Eleventh CircuitDocument10 pagesUnited States Court of Appeals, Eleventh CircuitScribd Government DocsNo ratings yet

- Doc. 153-1 - Affidavit of R. Lance FloresDocument13 pagesDoc. 153-1 - Affidavit of R. Lance FloresR. Lance FloresNo ratings yet

- United States Court of Appeals, Third CircuitDocument14 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- The Exchange National Bank of Olean v. Insurance Company of North America, 341 F.2d 673, 2d Cir. (1965)Document5 pagesThe Exchange National Bank of Olean v. Insurance Company of North America, 341 F.2d 673, 2d Cir. (1965)Scribd Government DocsNo ratings yet

- PDIC vs. CA (G.R. No. 118917 December 22, 1997) - 5Document5 pagesPDIC vs. CA (G.R. No. 118917 December 22, 1997) - 5Amir Nazri KaibingNo ratings yet

- Security State Bank, Pharr, Texas v. Paul A. Baty, 439 F.2d 910, 10th Cir. (1971)Document4 pagesSecurity State Bank, Pharr, Texas v. Paul A. Baty, 439 F.2d 910, 10th Cir. (1971)Scribd Government DocsNo ratings yet

- Letters of Credit and Documentary Collections: An Export and Import GuideFrom EverandLetters of Credit and Documentary Collections: An Export and Import GuideRating: 1 out of 5 stars1/5 (1)

- ALE2 2023 Week-6 ReadingDocument6 pagesALE2 2023 Week-6 ReadingTâm MinhNo ratings yet

- ALE2 - 2023 - Week 3 - ReadingDocument3 pagesALE2 - 2023 - Week 3 - ReadingTâm MinhNo ratings yet

- URC Case US Court Seminar - SV.P1Document9 pagesURC Case US Court Seminar - SV.P1Tâm MinhNo ratings yet

- ALE1 - 2022 - Week 9 - Reading and Listening ExercisesDocument4 pagesALE1 - 2022 - Week 9 - Reading and Listening ExercisesTâm MinhNo ratings yet

- PreviewpdfDocument36 pagesPreviewpdfTâm MinhNo ratings yet

- ALE1 2022 Week 8 Office MemorandumDocument4 pagesALE1 2022 Week 8 Office MemorandumTâm MinhNo ratings yet

- World Trade Organisation: SWAYAM MOOC Business EnvironmentDocument26 pagesWorld Trade Organisation: SWAYAM MOOC Business EnvironmentHems MadaviNo ratings yet

- Evil Women and Dynastic Collapse TracingDocument135 pagesEvil Women and Dynastic Collapse TracingMu YakshaNo ratings yet

- Vietnam - Local Charges/Service Fees: Container Cleaning Charge CLCDocument2 pagesVietnam - Local Charges/Service Fees: Container Cleaning Charge CLCTrang Thu TNo ratings yet

- Explain Contract Act, 1872 and State The Essentials To The ContractDocument18 pagesExplain Contract Act, 1872 and State The Essentials To The ContractPRINCESS PlayZNo ratings yet

- GBM AssignmentDocument18 pagesGBM AssignmentSowmya KaranamNo ratings yet

- Hlcubo1221091769 TDocument2 pagesHlcubo1221091769 TJeson RamjiteNo ratings yet

- South Asian Association For Regional CooperationDocument19 pagesSouth Asian Association For Regional CooperationAsif KureishiNo ratings yet

- Lesson 5 - Economic Integration Among CountriesDocument26 pagesLesson 5 - Economic Integration Among CountriesrylNo ratings yet

- مكونات المحيط الخارجي و أثرها على دخول المؤسسات الجزائرية إلى الأسواق الدولية دراسة عينة من المؤسسات الجزائرية المصدرةDocument31 pagesمكونات المحيط الخارجي و أثرها على دخول المؤسسات الجزائرية إلى الأسواق الدولية دراسة عينة من المؤسسات الجزائرية المصدرةadel.com.2004No ratings yet

- D/P, D/A and Their Use in International Sales TransactionsDocument5 pagesD/P, D/A and Their Use in International Sales TransactionsSoniya KhuramNo ratings yet

- The General Agreement On Tariffs and Trade (GATT) and World Trade OrganizationDocument20 pagesThe General Agreement On Tariffs and Trade (GATT) and World Trade OrganizationCristian PALMANo ratings yet

- WTO Success - No Trade Agreement But No Trade War - VOX, CEPR Policy Portal PDFDocument3 pagesWTO Success - No Trade Agreement But No Trade War - VOX, CEPR Policy Portal PDFTanatsiwa DambuzaNo ratings yet

- MSC - IBEF - Entrance PatternDocument82 pagesMSC - IBEF - Entrance PatternMadhav Khemka100% (1)

- Doha and Bali PackageDocument4 pagesDoha and Bali PackageSami ullah khan BabarNo ratings yet

- Aero 023Document1 pageAero 023Ebrahim AlgunaidNo ratings yet

- Chapter Three Global Affair-3Document59 pagesChapter Three Global Affair-3Ermi ZuruNo ratings yet

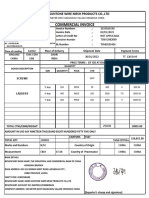

- Commercial InvoiceDocument1 pageCommercial Invoicesanjeev1910No ratings yet

- Asian Regionalism: Presented By: Christian Tactay Teejay Lance Pascua Victor Angelo Alejandro Bsa 2-ADocument43 pagesAsian Regionalism: Presented By: Christian Tactay Teejay Lance Pascua Victor Angelo Alejandro Bsa 2-AVictor Angelo AlejandroNo ratings yet

- Contemporary Foreign and Economic PoliciesDocument7 pagesContemporary Foreign and Economic Policiesrose ann rayoNo ratings yet

- Bài Ôn Tập Cuối KỳDocument8 pagesBài Ôn Tập Cuối KỳJennie LacNo ratings yet

- MGID40-F22 - Class 3Document14 pagesMGID40-F22 - Class 3totogggg16No ratings yet

- NEW UPDATED COURSE OUTLINE OME 322 International Marketing - 1Document19 pagesNEW UPDATED COURSE OUTLINE OME 322 International Marketing - 1Mwanuzi BabyegeyaNo ratings yet

- Pharmacutical IndustryDocument135 pagesPharmacutical Industryimran2662No ratings yet

- CHP 11 m19f59!23!15 Chicken PawsDocument1 pageCHP 11 m19f59!23!15 Chicken PawsSamrin JehangirNo ratings yet

- BRICS - Brazil Russia India China South Africa - PapertyariDocument2 pagesBRICS - Brazil Russia India China South Africa - Papertyaritatiana postolachiNo ratings yet

- Doing Business With International Agreement ReviewerDocument3 pagesDoing Business With International Agreement Reviewersatriajea.faustino.eNo ratings yet