Download as pdf or txt

You might also like

- Xitsonga Novel XimitantsengeleDocument77 pagesXitsonga Novel Ximitantsengelekwetsimohope05100% (2)

- GRADE 9 - Maths - Trace The Concept - Teacher DocumentDocument101 pagesGRADE 9 - Maths - Trace The Concept - Teacher DocumentmariahcopisoNo ratings yet

- Paralysed Child's Parents Demand AnswersDocument7 pagesParalysed Child's Parents Demand AnswersnangamsoNo ratings yet

- SBA Mathematics Teacher Guide EnglishDocument46 pagesSBA Mathematics Teacher Guide EnglishNtsakow Mbekie IINo ratings yet

- Unit 1 MiniMatura - Answer KeyDocument1 pageUnit 1 MiniMatura - Answer KeyŁukasz Gil67% (3)

- UNIT PLAN - Principles of Accounts: Unit Topic: Double EntryDocument10 pagesUNIT PLAN - Principles of Accounts: Unit Topic: Double Entryapi-627345932No ratings yet

- Accounting Self Study Guide - Grade 10 - 12Document155 pagesAccounting Self Study Guide - Grade 10 - 12jgrzadka2No ratings yet

- Michael Ymer Planning DayDocument3 pagesMichael Ymer Planning Dayapi-511483529No ratings yet

- Form 1 PhysicsDocument37 pagesForm 1 PhysicsEng Bahanza80% (5)

- Simple Interest Worksheet 01Document2 pagesSimple Interest Worksheet 01A.Benson0% (1)

- Search For The Graf SpeeDocument5 pagesSearch For The Graf SpeeChristina Chavez Clinton0% (1)

- Home Economics ActivityDocument6 pagesHome Economics ActivityJerwin Arteche DalinaNo ratings yet

- GET Economics & Management Sciences Grades 7 - 9Document107 pagesGET Economics & Management Sciences Grades 7 - 9Goodwill Mahlatse100% (1)

- Grade 12 Learners GuideDocument51 pagesGrade 12 Learners GuidesaneleNo ratings yet

- Grade 10 First Period Physics NotesDocument20 pagesGrade 10 First Period Physics NotesAlphonso Tulay100% (2)

- 2020 BSTD Grade 12 Term 2 Activities According To The New AtpDocument18 pages2020 BSTD Grade 12 Term 2 Activities According To The New AtpAngelinaNo ratings yet

- Syllabus - Grade 8 ScienceDocument32 pagesSyllabus - Grade 8 ScienceArlance Sandra Marie MedinaNo ratings yet

- Math 9 Week 1 Day 2Document7 pagesMath 9 Week 1 Day 2Meleza Joy SaturNo ratings yet

- Grade 11 Exponential Functions ReviewDocument3 pagesGrade 11 Exponential Functions ReviewDangeloNo ratings yet

- 2024 Accounting Grade 10 Learners Notes Session 1-5Document101 pages2024 Accounting Grade 10 Learners Notes Session 1-5tshireletsoseloane2No ratings yet

- Math9 q1 Mod2of8 Illustrationsofquadraticequations v2Document24 pagesMath9 q1 Mod2of8 Illustrationsofquadraticequations v2Layva BahaliNo ratings yet

- April-July 2020 3 Term Primary 3: Scheme of Work For Primary 1, 2 and 3Document2 pagesApril-July 2020 3 Term Primary 3: Scheme of Work For Primary 1, 2 and 3Ashley JosephNo ratings yet

- GRD 7 LO T3 and T4 2018 Learner BookDocument50 pagesGRD 7 LO T3 and T4 2018 Learner BookBotle MakotanyaneNo ratings yet

- Life Sciences Grade 10 Learner Support Document MAFUMANI SECONDARYDocument40 pagesLife Sciences Grade 10 Learner Support Document MAFUMANI SECONDARYdeveloping habit and lifestyle of praise and worshNo ratings yet

- Worksheet 14 5.2 TaxationDocument2 pagesWorksheet 14 5.2 TaxationMuhammad Fareed0% (1)

- Mathsclinic Smartprep GR10 Eng V1.1Document36 pagesMathsclinic Smartprep GR10 Eng V1.1Ebrahim Rayned100% (1)

- Lesson Plan Daily Commerce PD Form 5Document6 pagesLesson Plan Daily Commerce PD Form 5Sweetie Pinkie100% (1)

- Corvs - Grade 7 Lesson Plan Exemplar Term 1 - March2021Document16 pagesCorvs - Grade 7 Lesson Plan Exemplar Term 1 - March2021Africa Maria BernalNo ratings yet

- Business Mathematics Worksheet Week 3Document4 pagesBusiness Mathematics Worksheet Week 3300980 Pitombayog NHS100% (1)

- English Grade 10 Notes 2 - Research IntroductionDocument1 pageEnglish Grade 10 Notes 2 - Research IntroductionaxxNo ratings yet

- 2.1: Use Integers and Rational NumbersDocument3 pages2.1: Use Integers and Rational NumbersPrincess GinezNo ratings yet

- Obe Syllabus in College AlgebraDocument8 pagesObe Syllabus in College AlgebraMichael FigueroaNo ratings yet

- Grade 9 Math - FactoringDocument4 pagesGrade 9 Math - FactoringJerson Yhuwel100% (1)

- Lesson Plan Number and ConversionsDocument10 pagesLesson Plan Number and Conversionsapi-285978629No ratings yet

- G9 - Q1 - Wk.7-LessonEdit Done Na DoneDocument30 pagesG9 - Q1 - Wk.7-LessonEdit Done Na DoneLee C. SorianoNo ratings yet

- Business Studies Grade 12 Notes On Legislation FinalDocument25 pagesBusiness Studies Grade 12 Notes On Legislation Finalrelebogile sekgololoNo ratings yet

- Worksheet On AnnuitiesDocument2 pagesWorksheet On AnnuitiesKurt SoNo ratings yet

- Lesson Plan - Repeating Decimals and Related FractionsDocument3 pagesLesson Plan - Repeating Decimals and Related Fractionsapi-298545735No ratings yet

- Grade 9 Social Studies Textbook CbseDocument3 pagesGrade 9 Social Studies Textbook CbseKurtNo ratings yet

- Samkange and SamkangeDocument9 pagesSamkange and SamkangeAnonymous vaQiOm2No ratings yet

- GRADE 10 Updated Core Notes 2022 Paper 2Document55 pagesGRADE 10 Updated Core Notes 2022 Paper 2cyonela5No ratings yet

- Economic and Management Sciences Grade 9 1.1Document152 pagesEconomic and Management Sciences Grade 9 1.1Blackhawk NetNo ratings yet

- GR 10 Business Studies 3 in 1 Extracts TASDocument16 pagesGR 10 Business Studies 3 in 1 Extracts TASPhumerh NtanzihhNo ratings yet

- E-Mathematics 10: Grade 10. Rex Book Store, Inc. Grade 10. Rex Book Store, IncDocument5 pagesE-Mathematics 10: Grade 10. Rex Book Store, Inc. Grade 10. Rex Book Store, IncEm-jayL.SantelicesNo ratings yet

- Chapter 6 - Ratio and ProportionDocument7 pagesChapter 6 - Ratio and ProportionnbhaNo ratings yet

- Business Studies Self Study-Guide - Forms of OwnershipDocument32 pagesBusiness Studies Self Study-Guide - Forms of Ownershipshreeshail_mp6009No ratings yet

- Grade 7 Mathematics Platinum Navigation PackDocument81 pagesGrade 7 Mathematics Platinum Navigation Packitumeleng senooaneNo ratings yet

- Grade 10 Mathematics Platinum Navigation PackDocument80 pagesGrade 10 Mathematics Platinum Navigation PackNcumo MpanzaNo ratings yet

- OrganisingDocument55 pagesOrganisingskirubaarunNo ratings yet

- Physical Science Teacher GuideDocument28 pagesPhysical Science Teacher GuideJj JjNo ratings yet

- Grade 10 Science (Physics) SchemesDocument3 pagesGrade 10 Science (Physics) SchemesDavies MasumbaNo ratings yet

- S3 - Measures of Central Tendency of Grouped DataDocument24 pagesS3 - Measures of Central Tendency of Grouped DataJoboy FritzNo ratings yet

- Diamond Stone International School IGCSE Weekly Lesson PlanDocument2 pagesDiamond Stone International School IGCSE Weekly Lesson PlanjanithaNo ratings yet

- Function and RelationDocument28 pagesFunction and RelationMarjory GuillemerNo ratings yet

- Tourism Grade 10 2022 Gauteng Compiled BookletsDocument119 pagesTourism Grade 10 2022 Gauteng Compiled BookletsboyteephamoodyNo ratings yet

- Standard Form - Lesson PlanDocument6 pagesStandard Form - Lesson PlangamesNo ratings yet

- Teaching Guide - EMS - 7Document36 pagesTeaching Guide - EMS - 7MIKEMPHALONo ratings yet

- Lesson Plan in Grade 8 MathematicsDocument3 pagesLesson Plan in Grade 8 Mathematicschari cruzmanNo ratings yet

- Business Statistics Session 4Document37 pagesBusiness Statistics Session 4hans100% (1)

- Week Five:: Reporting andDocument38 pagesWeek Five:: Reporting andIzham ShabdeanNo ratings yet

- FABM1 - LAS - 9 - Nature of Transaction of A Mdsg. BusDocument8 pagesFABM1 - LAS - 9 - Nature of Transaction of A Mdsg. BusVenus Ariate100% (1)

- Fabm Module03 File01Document8 pagesFabm Module03 File01PREFIX THAT IS LONG - Lester LoutteNo ratings yet

- Bean GameDocument4 pagesBean Gameadriana espinoza de los monterosNo ratings yet

- Wcms 584176Document41 pagesWcms 584176adriana espinoza de los monterosNo ratings yet

- Key Stage 4 Computing Non GcseDocument14 pagesKey Stage 4 Computing Non Gcseadriana espinoza de los monterosNo ratings yet

- Lesson Plan Project Management - 0Document6 pagesLesson Plan Project Management - 0adriana espinoza de los monterosNo ratings yet

- Shark Tank Project MR Haugers Economics Class HHSDocument6 pagesShark Tank Project MR Haugers Economics Class HHSadriana espinoza de los monterosNo ratings yet

- Academic Calendar 2022-2023Document1 pageAcademic Calendar 2022-2023AssunçãoNo ratings yet

- Ikenberry, John (2014) - The Illusion of Geopolitics.Document9 pagesIkenberry, John (2014) - The Illusion of Geopolitics.David RamírezNo ratings yet

- Smoking During Pregnancy FinalDocument14 pagesSmoking During Pregnancy Finalapi-232728488No ratings yet

- Arabic Diglossia - Jeremy PalmerDocument15 pagesArabic Diglossia - Jeremy PalmerTaliba RoumaniyaNo ratings yet

- FINALLY DTOT Matrix KindergartenDocument3 pagesFINALLY DTOT Matrix KindergartenJaymar Kevin PadayaoNo ratings yet

- Practitioner Guide Georgia English 20130516Document310 pagesPractitioner Guide Georgia English 20130516OSGFNo ratings yet

- Essay 1Document3 pagesEssay 1api-607929863No ratings yet

- 2 The Riseofthe RenaissanceDocument32 pages2 The Riseofthe RenaissanceHoneyGracia BrionesNo ratings yet

- Spouses Guanio V Makati Shangri-LaDocument2 pagesSpouses Guanio V Makati Shangri-LaCinNo ratings yet

- Waimiri Atroari GrammarDocument187 pagesWaimiri Atroari GrammarjjlajomNo ratings yet

- ConsonantsDocument23 pagesConsonantsanna39No ratings yet

- E. S. LYONS vs. C. W. ROSENSTOCKDocument4 pagesE. S. LYONS vs. C. W. ROSENSTOCKMarvin A GamboaNo ratings yet

- Jurisdiction of The Supreme CourtDocument1 pageJurisdiction of The Supreme CourtInnah A Jose Vergara-Huerta100% (1)

- MPA - Policy Paper (R.simbahon)Document80 pagesMPA - Policy Paper (R.simbahon)Robert SimbahonNo ratings yet

- CS615-MidTerm MCQs With Reference Solved by ArslanDocument16 pagesCS615-MidTerm MCQs With Reference Solved by ArslanHabib AhmedNo ratings yet

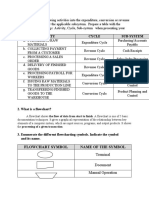

- Activity Cycle Sub-System: Flowchart Symbol Name of The SymbolDocument3 pagesActivity Cycle Sub-System: Flowchart Symbol Name of The SymbolALLIAH CARL MANUELLE PASCASIONo ratings yet

- DOH-HHRDB Healthcare Workers (Physicians)Document41 pagesDOH-HHRDB Healthcare Workers (Physicians)VERA FilesNo ratings yet

- The Romantic Movement As ADocument7 pagesThe Romantic Movement As ATANBIR RAHAMANNo ratings yet

- Optimise B1+ - End of The YearDocument5 pagesOptimise B1+ - End of The YearItsasoAmezaga100% (1)

- Genre Analysis On Racial StereotypeDocument4 pagesGenre Analysis On Racial Stereotypeapi-316855715No ratings yet

- Combined Knitting Conversion TableDocument1 pageCombined Knitting Conversion TableKatarina Ivic-UcovicNo ratings yet

- Introduction e CommerceDocument84 pagesIntroduction e CommerceMohd FirdausNo ratings yet

- 1 Aloandro Ben Bakr - BeatrizDocument1 page1 Aloandro Ben Bakr - BeatrizDavid DayNo ratings yet

- Case Study GoogleplexDocument6 pagesCase Study GoogleplexRoger Madorell100% (1)

- British Yearbook of International Law 1977 Crawford 93 182Document90 pagesBritish Yearbook of International Law 1977 Crawford 93 182irony91No ratings yet

- Ignacy Jan Paderewski A Discography of His European RecordingsDocument9 pagesIgnacy Jan Paderewski A Discography of His European RecordingsCody NguyenNo ratings yet

- What Is Strategic Positioning?Document8 pagesWhat Is Strategic Positioning?Michael YohannesNo ratings yet

- Unit 1. Health, Safety and Welfare in Construction and The Built EnvironmentDocument14 pagesUnit 1. Health, Safety and Welfare in Construction and The Built EnvironmentIhuhwa Marta TauNo ratings yet