Download as xlsx, pdf, or txt

You might also like

- Manufacturing Account Worked Example Question 13Document6 pagesManufacturing Account Worked Example Question 13Roshan Ramkhalawon100% (1)

- Global Stocks ResourcesDocument48 pagesGlobal Stocks ResourcesAvinash KumarNo ratings yet

- Individual Assignment Holcim Lafarge PDFDocument17 pagesIndividual Assignment Holcim Lafarge PDFMuhammad Hassan AhmadNo ratings yet

- PS Set 1 - 2Document61 pagesPS Set 1 - 2Rithesh KNo ratings yet

- Assignment 2 - CMADocument9 pagesAssignment 2 - CMAVivek SharanNo ratings yet

- MAC2601-SuggestedsolutionOct November2013Document12 pagesMAC2601-SuggestedsolutionOct November2013DINEO PRUDENCE NONGNo ratings yet

- CA Work Sheet Unit 2Document23 pagesCA Work Sheet Unit 2Shalini SavioNo ratings yet

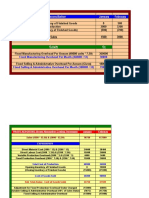

- Sno Description Cost in Rs Cost in RsDocument8 pagesSno Description Cost in Rs Cost in RsCH NAIRNo ratings yet

- CostingDocument46 pagesCostingRaghav KhakholiaNo ratings yet

- Cost SheetDocument13 pagesCost SheetsvermaupesNo ratings yet

- Prime Cost 2940000 Conversion Cost Work Cost (Gross) 4140000Document4 pagesPrime Cost 2940000 Conversion Cost Work Cost (Gross) 4140000Shachin ShibiNo ratings yet

- Assignment On Cost SheetDocument3 pagesAssignment On Cost SheetRashmi KumariNo ratings yet

- Q1.What Is Meant by Cost Sheet?explain The Importance of Cost SheetDocument4 pagesQ1.What Is Meant by Cost Sheet?explain The Importance of Cost SheetHeena SorenNo ratings yet

- Flow of Sequence of All Costs Including Work in ProgressDocument7 pagesFlow of Sequence of All Costs Including Work in ProgressUmesh AroraNo ratings yet

- Cost SheetDocument4 pagesCost Sheetpravinmore1589No ratings yet

- UntitledDocument3 pagesUntitledVatsal ChangoiwalaNo ratings yet

- TUGAS - Riphal Muchzaivi (2204106010024)Document2 pagesTUGAS - Riphal Muchzaivi (2204106010024)riphalwibuNo ratings yet

- Cost Sheet: (-) Sales of WastageDocument1 pageCost Sheet: (-) Sales of WastageAuras Raj PantaNo ratings yet

- A - Mock PSPM Set 1Document5 pagesA - Mock PSPM Set 1IZZAH NUR ATHIRAH BINTI AZLI MoeNo ratings yet

- XYZ Ice Cream CompanyDocument2 pagesXYZ Ice Cream CompanyTanjib Rahman NiloyNo ratings yet

- Cost Sheet ProblemsDocument11 pagesCost Sheet ProblemsPrem RajNo ratings yet

- Problem 2-29Document6 pagesProblem 2-29Love IslamNo ratings yet

- 30 Dec COST SHEET - PGDMDocument15 pages30 Dec COST SHEET - PGDMPoonamNo ratings yet

- OBE - COST QB With ANSWERS - FINALDocument92 pagesOBE - COST QB With ANSWERS - FINALPavi NishaNo ratings yet

- Cost Sheet ProblemsDocument5 pagesCost Sheet ProblemsshamilaNo ratings yet

- Cost Sheet 1Document6 pagesCost Sheet 1Tamilselvi ANo ratings yet

- Job Costing Question Bank SSDocument6 pagesJob Costing Question Bank SSTamaraNo ratings yet

- Cost & Management AccountingDocument3 pagesCost & Management AccountingAnurag AwasthiNo ratings yet

- Cost & Management Accounting Assignment 2023Document6 pagesCost & Management Accounting Assignment 2023riya.shah2701No ratings yet

- Assignment: Table of ContentDocument9 pagesAssignment: Table of ContentAhsanur HossainNo ratings yet

- Cost Accounting 1Document4 pagesCost Accounting 1Rohan RalliNo ratings yet

- CS Uthkarsh PaiDocument9 pagesCS Uthkarsh Paiankita sahuNo ratings yet

- Cost Sheet of Nikhil Baker's For The Period 1st October-31st October, 2021Document2 pagesCost Sheet of Nikhil Baker's For The Period 1st October-31st October, 2021UBSHimanshu KumarNo ratings yet

- Group-8 F2 CCE-2 CMA Cost SheetDocument12 pagesGroup-8 F2 CCE-2 CMA Cost SheetNAMRATANo ratings yet

- Cost Sheet DetailedDocument5 pagesCost Sheet DetailedSimran JainNo ratings yet

- Hospital Supply Solution (Document15 pagesHospital Supply Solution (sakshi upadhyayNo ratings yet

- Solution To Compiled QuestionsDocument7 pagesSolution To Compiled Questionslovia mensahNo ratings yet

- Cost HeetDocument4 pagesCost HeetYuvnesh KumarNo ratings yet

- Cost N Management AccountingDocument4 pagesCost N Management AccountingChoudharyPremNo ratings yet

- Costsheet (Subham)Document3 pagesCostsheet (Subham)amijit93No ratings yet

- Cost Concepts - Cost SheetDocument24 pagesCost Concepts - Cost SheetFaraz SiddiquiNo ratings yet

- Session#15Document5 pagesSession#15Saurabh Kumar BJ22041No ratings yet

- Problem 2 - Paper Set - 1: Statement of CostDocument3 pagesProblem 2 - Paper Set - 1: Statement of CostBALAJI DASAPPAJINo ratings yet

- Dorrit and Dorrbie Maufacturig AccountDocument5 pagesDorrit and Dorrbie Maufacturig AccountToniann GordonNo ratings yet

- Factory Over Head: Particular UNIT-1000 AmountDocument2 pagesFactory Over Head: Particular UNIT-1000 AmountPintu MaharanaNo ratings yet

- New Microsoft Excel WorksheetDocument2 pagesNew Microsoft Excel WorksheetPintu MaharanaNo ratings yet

- Cma Budget ExcelDocument6 pagesCma Budget ExcelDristi SinghNo ratings yet

- Cost SheetDocument20 pagesCost SheetVannoj AbhinavNo ratings yet

- Cost Sheet TemplatesDocument26 pagesCost Sheet TemplatessukeshNo ratings yet

- DAIBB Accounting 2020Document14 pagesDAIBB Accounting 2020BelalHossainNo ratings yet

- Cost Sheet 19.08.2020Document6 pagesCost Sheet 19.08.2020VISHAGAN MNo ratings yet

- Illustration Questions 7Document3 pagesIllustration Questions 7mohammedahalys100% (1)

- Unit 3 Part 1 - CostingDocument17 pagesUnit 3 Part 1 - CostingPrarthana R Industrial EngineeringNo ratings yet

- Acc Assignment Sem 2Document23 pagesAcc Assignment Sem 2Luqman HaqimNo ratings yet

- CMA Assignment Problem Set 1Document4 pagesCMA Assignment Problem Set 1Antesh SinghNo ratings yet

- J. Jarvis Trial Balance As at 31 December 2010Document3 pagesJ. Jarvis Trial Balance As at 31 December 2010Ahmad HaqqyNo ratings yet

- Empire Enterprise Statament of Account For Profit and Loss As at 31 December 2015 RM RM RMDocument3 pagesEmpire Enterprise Statament of Account For Profit and Loss As at 31 December 2015 RM RM RMJasmin JimmyNo ratings yet

- Excel Practise Questions and SolutionsDocument18 pagesExcel Practise Questions and SolutionsFahad NadeemNo ratings yet

- Costing LDocument4 pagesCosting LgogunikhilNo ratings yet

- COGS F2F Practise Questions With SolutionsDocument5 pagesCOGS F2F Practise Questions With Solutionsak8ballpool111No ratings yet

- Direct Material CostDocument29 pagesDirect Material CostRaj DharodNo ratings yet

- (M-2) Process Costing & Material Pricing Sums 3Document24 pages(M-2) Process Costing & Material Pricing Sums 3Yolo GuyNo ratings yet

- (M-5) Budgeting 2Document26 pages(M-5) Budgeting 2Yolo GuyNo ratings yet

- EVS Module 3Document37 pagesEVS Module 3Yolo GuyNo ratings yet

- (M-4) - Marginal Costing & CVP Analysis Formulas 2Document2 pages(M-4) - Marginal Costing & CVP Analysis Formulas 2Yolo GuyNo ratings yet

- (M-2) Job, Batch, Operating Costing 4Document13 pages(M-2) Job, Batch, Operating Costing 4Yolo GuyNo ratings yet

- EVS Module 5Document32 pagesEVS Module 5Yolo GuyNo ratings yet

- EVS Module 4Document71 pagesEVS Module 4Yolo GuyNo ratings yet

- Behavioral Science - Case StudyDocument3 pagesBehavioral Science - Case StudyYolo GuyNo ratings yet

- Business Accountancy Module 1Document49 pagesBusiness Accountancy Module 1Yolo Guy100% (1)

- MRTP and Competition Act 2002Document12 pagesMRTP and Competition Act 2002Yolo GuyNo ratings yet

- Kraft - Heins - M&A CaseDocument1 pageKraft - Heins - M&A CaseDouglas MarangonNo ratings yet

- CH17Document70 pagesCH17SeranityNo ratings yet

- Mas Capital Budgeting ReviewersDocument16 pagesMas Capital Budgeting ReviewersNo Mi ViNo ratings yet

- BLESS 20121209 00003 941541 financial5ROC CREDocument2 pagesBLESS 20121209 00003 941541 financial5ROC CREEcho WackoNo ratings yet

- Working Capital ProjectDocument48 pagesWorking Capital ProjectkunjapNo ratings yet

- The Rise of Romanian UnicornsDocument11 pagesThe Rise of Romanian UnicornsViorica Madalina ManuNo ratings yet

- Citizen Charter April 2023Document25 pagesCitizen Charter April 2023Parody CentralNo ratings yet

- Phillip Capital Fy21Document22 pagesPhillip Capital Fy21harshbhutra1234No ratings yet

- Bài Tập Buổi 1 FA1 (F3)Document4 pagesBài Tập Buổi 1 FA1 (F3)nhtrangclcNo ratings yet

- Week 6 Go LiveDocument3 pagesWeek 6 Go Livewriter topNo ratings yet

- PAS 1 - Presentation of FS For LMSDocument72 pagesPAS 1 - Presentation of FS For LMSnot funny didn't laughNo ratings yet

- Costing Homework SolutionsDocument97 pagesCosting Homework SolutionsKunal BhansaliNo ratings yet

- Long-Term Debt-Paying AbilityDocument23 pagesLong-Term Debt-Paying AbilitymohamedNo ratings yet

- SelectComfortCorporation 10Q 20151112 PDFDocument340 pagesSelectComfortCorporation 10Q 20151112 PDFMirsab RizviNo ratings yet

- Financial Analysis - J.C. Penney Company, Inc., Through A Subsidiary, Operates Department Stores in The United States and Puerto RicoDocument8 pagesFinancial Analysis - J.C. Penney Company, Inc., Through A Subsidiary, Operates Department Stores in The United States and Puerto RicoQ.M.S Advisors LLCNo ratings yet

- Rates 104 - Debt Instruments 1Document42 pagesRates 104 - Debt Instruments 1ssj7cjqq2dNo ratings yet

- Eac694 Group Case Study Yates Control SystemDocument11 pagesEac694 Group Case Study Yates Control SystemVisha KupusamyNo ratings yet

- Dewan Cement Industry Ratio AnalysisDocument15 pagesDewan Cement Industry Ratio AnalysisMuhammad Usama Mahmood0% (1)

- FIN300 Homework 1Document7 pagesFIN300 Homework 1JohnNo ratings yet

- 1-Cost SheetDocument68 pages1-Cost SheetPapia SenNo ratings yet

- ACCT 312 - Exam 2 (Part 1) - Spring 2022 FinalDocument8 pagesACCT 312 - Exam 2 (Part 1) - Spring 2022 FinalMercy Jerop KimutaiNo ratings yet

- Answers To Problem Sets: How Corporations Issue SecuritiesDocument10 pagesAnswers To Problem Sets: How Corporations Issue Securitiesmandy YiuNo ratings yet

- 0 Courrier PruebaDocument12 pages0 Courrier PruebaBorisvc8No ratings yet

- 2017 MJ Q4 Bond & Credit RatingDocument27 pages2017 MJ Q4 Bond & Credit RatingZi Yuan XuNo ratings yet

- Wharton PE Certificate ProgramDocument29 pagesWharton PE Certificate ProgramRayanNo ratings yet

- Russel Microcap IndexDocument4 pagesRussel Microcap IndexMark SchraderNo ratings yet

- Discounted Cash Flow Analysis - Uber Technologies, Inc. (Unlevered DCF)Document9 pagesDiscounted Cash Flow Analysis - Uber Technologies, Inc. (Unlevered DCF)Haysam TayyabNo ratings yet

- 12 AccountancyDocument48 pages12 Accountancyraghu monnappaNo ratings yet