Download as pdf or txt

You might also like

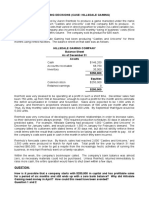

- Hillsdale Gaming Case AnalysisDocument2 pagesHillsdale Gaming Case AnalysisIan Grey100% (7)

- Sample Small Law Firm Chart of AccountsDocument3 pagesSample Small Law Firm Chart of AccountsYasmin ZainuzzamanNo ratings yet

- Cash BudgetingDocument14 pagesCash BudgetingJo Ryl100% (1)

- San Beda College Alabang Homework Exercise-Act851RDocument4 pagesSan Beda College Alabang Homework Exercise-Act851RJomel BaptistaNo ratings yet

- Cash Budget Format and Its Explanation With Solved ExampleDocument8 pagesCash Budget Format and Its Explanation With Solved ExamplePui YanNo ratings yet

- Asset Quality Management in BankDocument13 pagesAsset Quality Management in Bankswendadsilva100% (4)

- Drivers of Industry Financial StructureDocument2 pagesDrivers of Industry Financial StructureVikas Tiwari100% (1)

- To Make The Necessary Entries and Calculate The Gain or LossDocument5 pagesTo Make The Necessary Entries and Calculate The Gain or LossMaryam IkhlaqeNo ratings yet

- Mid Term Advanced Accounting 2 - Negina - 19 April 2021Document2 pagesMid Term Advanced Accounting 2 - Negina - 19 April 2021NybexysNo ratings yet

- FM Assignment 8 - Group 4Document9 pagesFM Assignment 8 - Group 4Puspita RamadhaniaNo ratings yet

- Accounting For Overseas TransactionsDocument25 pagesAccounting For Overseas TransactionshaibomagicNo ratings yet

- 2-Quiz Chapter 9 Foreign Currency TransactionDocument2 pages2-Quiz Chapter 9 Foreign Currency Transactionnoproblem 5555No ratings yet

- Module 3 - FRADocument251 pagesModule 3 - FRAsrish.srccNo ratings yet

- 0 Accounting For Merchandising BusinessDocument114 pages0 Accounting For Merchandising BusinessIan RanilopaNo ratings yet

- Accounting Principles 2: Plant Assets, Natural Resources, and Intangible AssetsDocument11 pagesAccounting Principles 2: Plant Assets, Natural Resources, and Intangible AssetsramiNo ratings yet

- Government of Canada Market Debt InstrumentsDocument3 pagesGovernment of Canada Market Debt InstrumentsfelixniefeiusNo ratings yet

- O Brien Industries Inc Is A Book Publisher The Comparative UnclassifiedDocument1 pageO Brien Industries Inc Is A Book Publisher The Comparative Unclassifiedtrilocksp SinghNo ratings yet

- 5C Auditing Review Mr. Jonathan C. Tipay: Additional Data Relating December Sales FollowDocument2 pages5C Auditing Review Mr. Jonathan C. Tipay: Additional Data Relating December Sales FollowMicah P. CastroNo ratings yet

- Ulep - Future ValueDocument4 pagesUlep - Future ValueNoel BajadaNo ratings yet

- P2 - FXCY, FS Consolidation.O2016Document11 pagesP2 - FXCY, FS Consolidation.O2016Darwin Competente LagranNo ratings yet

- Vanguard Corporation Is A Distributor of Food Products The CorporationDocument1 pageVanguard Corporation Is A Distributor of Food Products The Corporationtrilocksp SinghNo ratings yet

- Activity #5 Foreign Currency Transactions and Translation of FSDocument3 pagesActivity #5 Foreign Currency Transactions and Translation of FSddddddaaaaeeeeNo ratings yet

- IFMDocument4 pagesIFMAshwitha KarkeraNo ratings yet

- Avoidance of Financial RestrictionsDocument6 pagesAvoidance of Financial RestrictionsFelyJoy MagallonesNo ratings yet

- BudgetingDocument9 pagesBudgetingshobi_300033% (3)

- Master BudgetingDocument20 pagesMaster Budgetingaaravdhamija100No ratings yet

- Chapter 8Document17 pagesChapter 8Jamaica DavidNo ratings yet

- Fabm 1 - 6 1Document10 pagesFabm 1 - 6 1awitakintoNo ratings yet

- Dan Corporation Started Operations On January 1Document1 pageDan Corporation Started Operations On January 1Mayuki TakizawaNo ratings yet

- Lecture 3 International Acc ECUDocument37 pagesLecture 3 International Acc ECUmariam raafatNo ratings yet

- Hedging Strategy Using FuturesDocument40 pagesHedging Strategy Using FuturesAnuj Negi1880No ratings yet

- Inventory ValuationDocument6 pagesInventory ValuationAnique buttNo ratings yet

- Apllied Auditing Q&ADocument10 pagesApllied Auditing Q&APeterJorgeVillarante100% (2)

- 2008-03-11 001150 ObmarioDocument5 pages2008-03-11 001150 Obmariovignesh__mNo ratings yet

- Insurance Claim 18-34 - Watermark1Document17 pagesInsurance Claim 18-34 - Watermark1GOVIND LOKARENo ratings yet

- Chapter 10 - Adjusting The RecordsDocument24 pagesChapter 10 - Adjusting The RecordsJesseca JosafatNo ratings yet

- Foreign ExchangeDocument20 pagesForeign ExchangeMohammad Asraf Ul HaqueNo ratings yet

- BUSN 2011 Tutorial Questions For Week 8Document2 pagesBUSN 2011 Tutorial Questions For Week 8nongvinhkiet2001No ratings yet

- Brant On Banking Began Operations On January 1 2015 BrantDocument1 pageBrant On Banking Began Operations On January 1 2015 BrantTaimur TechnologistNo ratings yet

- 3rd LectureDocument4 pages3rd LectureHarpal Singh HansNo ratings yet

- Programmazione e Controllo Esercizi Capitolo 7aDocument14 pagesProgrammazione e Controllo Esercizi Capitolo 7aMavzky RoqueNo ratings yet

- FRA and SWAPSDocument49 pagesFRA and SWAPSBluesinhaNo ratings yet

- GOC - Rates - July 2019 - CompleteDocument6 pagesGOC - Rates - July 2019 - CompleteAkbar ShaikNo ratings yet

- Techniques of Asset/liability Management: Futures, Options, and SwapsDocument43 pagesTechniques of Asset/liability Management: Futures, Options, and SwapsSushmita BarlaNo ratings yet

- FC Trans Rem - NotesDocument3 pagesFC Trans Rem - NotesVenz LacreNo ratings yet

- The Following Data Have Been Extracted From The Financial StatementsDocument1 pageThe Following Data Have Been Extracted From The Financial Statementstrilocksp SinghNo ratings yet

- 15 International FinanceDocument16 pages15 International FinanceRishabh SehrawatNo ratings yet

- Soal Se Akm 2 PDFDocument3 pagesSoal Se Akm 2 PDFrakhaNo ratings yet

- Review: Adjusting Entries: NameDocument4 pagesReview: Adjusting Entries: NameJohn BushNo ratings yet

- Auditing ProblemDocument11 pagesAuditing ProblemNicole Gole CruzNo ratings yet

- SKRTDocument4 pagesSKRTTrisha RafalloNo ratings yet

- Types of Adjusting Entries (CH 4)Document5 pagesTypes of Adjusting Entries (CH 4)Ashna KoshalNo ratings yet

- Finance - Exam 3Document15 pagesFinance - Exam 3Neeta Joshi50% (6)

- AfarDocument11 pagesAfarDonna Mae HernandezNo ratings yet

- Homework On Current Liabilities PDFDocument3 pagesHomework On Current Liabilities PDFJenneth RegalaNo ratings yet

- Cash BudgetingDocument5 pagesCash BudgetingAnissa GeddesNo ratings yet

- Exercise Advanced Accounting SolutionsDocument14 pagesExercise Advanced Accounting SolutionsMiko Victoria Vargas75% (4)

- Fix 336Document6 pagesFix 336Bánh BaoNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Homeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransFrom EverandHomeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransNo ratings yet

- How to Buy & Track 30-Year Treasury Bonds: Financial Freedom, #51From EverandHow to Buy & Track 30-Year Treasury Bonds: Financial Freedom, #51No ratings yet

- My High-Yield Savings Account: Year in Review 2022: Financial Freedom, #101From EverandMy High-Yield Savings Account: Year in Review 2022: Financial Freedom, #101No ratings yet

- Ordinar Y LevelDocument16 pagesOrdinar Y LevelPantuan SizweNo ratings yet

- Max Life Fast Trak Super LeafletDocument4 pagesMax Life Fast Trak Super Leafletmantoo kumarNo ratings yet

- ANZ BankDocument6 pagesANZ BankВлад АнгелNo ratings yet

- Retail Tech Trends 2020Document53 pagesRetail Tech Trends 2020Mike EdwardsNo ratings yet

- Whitepaper NETFLOW VS DPIDocument2 pagesWhitepaper NETFLOW VS DPIMarvin nduko bosireNo ratings yet

- Ew9678 8Document3 pagesEw9678 8jkufNo ratings yet

- PO BOX 177, SAFAT 13002, KUWAIT, C.R. 81300, Share Capital-16500000 16500000, 81300 . ., , 13002 177: . .Document1 pagePO BOX 177, SAFAT 13002, KUWAIT, C.R. 81300, Share Capital-16500000 16500000, 81300 . ., , 13002 177: . .nizamNo ratings yet

- Cisco 300-715 Flashcards Quizlet 31Document4 pagesCisco 300-715 Flashcards Quizlet 31lingNo ratings yet

- zNID-GPON-GE-6024T - DZSDocument4 pageszNID-GPON-GE-6024T - DZSKAREEEMNo ratings yet

- Jlb9Vjgvqugclwirblgxvmh: 10318132-001 Muhammad FareedDocument38 pagesJlb9Vjgvqugclwirblgxvmh: 10318132-001 Muhammad FareedAbuAbdullah KhanNo ratings yet

- Types of CompensationDocument22 pagesTypes of CompensationSampathhrNo ratings yet

- Confirmation For Booking ID 126072138Document1 pageConfirmation For Booking ID 126072138weiyet93No ratings yet

- Appendix I Specimen of Advice of Maturity Date To Term Deposit Account HoldersDocument11 pagesAppendix I Specimen of Advice of Maturity Date To Term Deposit Account HoldersRuchi SharmaNo ratings yet

- Esigned Kyc Stock PDFDocument27 pagesEsigned Kyc Stock PDFsantanu chowdhuryNo ratings yet

- Statement of ConfidentialityDocument3 pagesStatement of ConfidentialityKotadiya ChiragNo ratings yet

- 6.1 Vouchers PDFDocument3 pages6.1 Vouchers PDFrababNo ratings yet

- On Cyber SecurityDocument8 pagesOn Cyber SecuritySsbacademy SNo ratings yet

- Accounts ReceivableDocument5 pagesAccounts ReceivableDianna DayawonNo ratings yet

- 631 1200 1 SMDocument7 pages631 1200 1 SMngcheeguan020729No ratings yet

- Letter of CreditDocument4 pagesLetter of Creditrapols9100% (1)

- Acct Statement XX8038 12102023Document5 pagesAcct Statement XX8038 12102023middeslifesciencesNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceLoan LoanNo ratings yet

- International Economics L ModDocument7 pagesInternational Economics L ModTesfu HettoNo ratings yet

- Narrative ReportDocument8 pagesNarrative ReportJohn Maynard Resquid SalazarNo ratings yet

- Auditing and Assurance Services 7th Edition Louwers Test BankDocument42 pagesAuditing and Assurance Services 7th Edition Louwers Test Bankaaronowen27102002ker100% (42)

- Money and Banking Q&ADocument9 pagesMoney and Banking Q&AKrrish WaliaNo ratings yet

- Chapter 4-QUESTIONSDocument6 pagesChapter 4-QUESTIONSDanica GravitoNo ratings yet