Download as pdf or txt

You might also like

- Harvard Business Review Via GWMSIST - BBVA Compass: Marketing Resource AllocationDocument8 pagesHarvard Business Review Via GWMSIST - BBVA Compass: Marketing Resource AllocationAlex Singleton100% (2)

- Reinventing the Family Firm: A Guide to How Enterprising Family Business Owners Build a PortfolioFrom EverandReinventing the Family Firm: A Guide to How Enterprising Family Business Owners Build a PortfolioNo ratings yet

- Family Business in India: Performance, Challenges and Improvement MeasuresDocument22 pagesFamily Business in India: Performance, Challenges and Improvement Measuresmanjusri lalNo ratings yet

- Cat 1 Amos Taxation LawDocument9 pagesCat 1 Amos Taxation LawAmos Mogere100% (1)

- Camel Analysis Meezan BankDocument11 pagesCamel Analysis Meezan BankHabiba PashaNo ratings yet

- Performance of Family Business in Malaysia: Aissa Mosbah Sultan Rehman Serief Kalsom Abd WahabDocument7 pagesPerformance of Family Business in Malaysia: Aissa Mosbah Sultan Rehman Serief Kalsom Abd WahabAmin Akasyaf100% (1)

- Corporate Governance and Firm Performance: A Comparative Analysis Between Listed Family and Non-Family Firms in JapanDocument20 pagesCorporate Governance and Firm Performance: A Comparative Analysis Between Listed Family and Non-Family Firms in JapanHafiz Saddique MalikNo ratings yet

- Governance of Large Family Companies in TraditionaDocument16 pagesGovernance of Large Family Companies in TraditionaShameem MuhammedNo ratings yet

- The Family Firm's Performance A Literature ReviewDocument5 pagesThe Family Firm's Performance A Literature ReviewAmy DayalNo ratings yet

- Meeting 1 Benefit SMDocument16 pagesMeeting 1 Benefit SMamelia putriNo ratings yet

- Family BusinessDocument22 pagesFamily BusinessDaniel MakauNo ratings yet

- Jurnal Jovita PDFDocument18 pagesJurnal Jovita PDFkeizya winda yulianaNo ratings yet

- ProposalDocument12 pagesProposalKingsley AddaeNo ratings yet

- Corporate Governance and Firm Performance An Analysis of Family and Nonfamily Controlled Firms2011pakistan Development ReviewDocument16 pagesCorporate Governance and Firm Performance An Analysis of Family and Nonfamily Controlled Firms2011pakistan Development ReviewKhả Ái ĐặngNo ratings yet

- Cultural Factors in Chinese Family Business Performance ThailandDocument15 pagesCultural Factors in Chinese Family Business Performance Thailandaleeyah leysonNo ratings yet

- Gill Kaur 2016 Family Involvement in Business and Financial Performance A Panel Data AnalysisDocument26 pagesGill Kaur 2016 Family Involvement in Business and Financial Performance A Panel Data AnalysisShameem MuhammedNo ratings yet

- 09 2021 Corporate Social Responsibility of Family Controlled Firms in TaiwanDocument25 pages09 2021 Corporate Social Responsibility of Family Controlled Firms in TaiwanBionic MixitNo ratings yet

- Ijim 231174155Document22 pagesIjim 231174155errachna78No ratings yet

- Determinants of Longevity of Family Owned BusinessesDocument16 pagesDeterminants of Longevity of Family Owned Businessesesta11No ratings yet

- Nguvo 24 January 2023 Chapter 1 MasterDocument11 pagesNguvo 24 January 2023 Chapter 1 MastertichaonamuzekenyiNo ratings yet

- Board Mechanisms and Malaysian Family Companies' PerformanceDocument12 pagesBoard Mechanisms and Malaysian Family Companies' Performanceadriana GarridoNo ratings yet

- The Relationship Between Innovation, Knowledge, and Performance in Family and Non-Family Firms: An Analysis of SmesDocument20 pagesThe Relationship Between Innovation, Knowledge, and Performance in Family and Non-Family Firms: An Analysis of SmesVelyNo ratings yet

- LiguoriEW Web14 1 PDFDocument15 pagesLiguoriEW Web14 1 PDFgroelandNo ratings yet

- Context and Uniqueness of Family Busniesses 2015Document30 pagesContext and Uniqueness of Family Busniesses 2015AREEBA SULEMANNo ratings yet

- Family BusinessDocument18 pagesFamily BusinessPratikNo ratings yet

- Banker Directors and Firm Performance Are Family Fi 2018 Future Business JoDocument15 pagesBanker Directors and Firm Performance Are Family Fi 2018 Future Business JoLydia KusumadewiNo ratings yet

- A Survey of Asian Family Business ResearchDocument48 pagesA Survey of Asian Family Business ResearchRicky FernandoNo ratings yet

- Corporate Governance, Family Ownership and Earnings Management: Emerging Market EvidenceDocument17 pagesCorporate Governance, Family Ownership and Earnings Management: Emerging Market EvidenceShaamAhmedNo ratings yet

- Financial Performance of Privately Held FirmsDocument24 pagesFinancial Performance of Privately Held Firmscuteeangel1No ratings yet

- Measuringperformancein FBresearchpublishedversionDocument46 pagesMeasuringperformancein FBresearchpublishedversionTITIS WAHYUNINo ratings yet

- Family Enterprise and Technological Innovati 2022 Journal of Business ResearDocument14 pagesFamily Enterprise and Technological Innovati 2022 Journal of Business ResearAmir ElkassasNo ratings yet

- #2 - Preparing To Read A Research Article and Writing Summaries From Multiple SourcesDocument13 pages#2 - Preparing To Read A Research Article and Writing Summaries From Multiple Sourcesyanuardi2790No ratings yet

- Is The Family An Asset or Liability For Firm PerformanceDocument17 pagesIs The Family An Asset or Liability For Firm PerformancethaiNo ratings yet

- SSRN Id3812443Document13 pagesSSRN Id3812443Dharmendra DclanaNo ratings yet

- The Quality of Internal Control Bardhan2015 PDFDocument21 pagesThe Quality of Internal Control Bardhan2015 PDFBerthelo KuedaNo ratings yet

- Indian Family BusinessesDocument22 pagesIndian Family BusinessesShveta VatasNo ratings yet

- Board Mechanisms and Malaysian Family Companies PDocument13 pagesBoard Mechanisms and Malaysian Family Companies PKingsley AddaeNo ratings yet

- Document 1Document54 pagesDocument 1Abdel AyourNo ratings yet

- Dinh ETP2021Document33 pagesDinh ETP2021Donal D MEcNo ratings yet

- Strategic Entrepreneurship and Performance: An Institutional Perspective On Indian Family BusinessesDocument39 pagesStrategic Entrepreneurship and Performance: An Institutional Perspective On Indian Family BusinessesLejandra MNo ratings yet

- Smith, M. (2005)Document25 pagesSmith, M. (2005)JhggNo ratings yet

- Agency Theory Family BusinessDocument8 pagesAgency Theory Family Businessusef100% (1)

- Kinship-Based Problems Affecting The Employee Performance: A Study Case of Family Business in Developing City in IndonesiaDocument21 pagesKinship-Based Problems Affecting The Employee Performance: A Study Case of Family Business in Developing City in IndonesiaGlobal Research and Development ServicesNo ratings yet

- The Moderating Effect of Intellectual Capital On The Relationship Between Corporate Governance and Companies Performance in PakistanDocument11 pagesThe Moderating Effect of Intellectual Capital On The Relationship Between Corporate Governance and Companies Performance in PakistanDharmiani DharmiNo ratings yet

- Diversification, Propping and Monitoring - Business Groups, Firm Performance and The Indian Economic TransitionDocument48 pagesDiversification, Propping and Monitoring - Business Groups, Firm Performance and The Indian Economic TransitionAvik MukherjeeNo ratings yet

- Females' Representation in The Boardroom and Their Impact On Financial Distress: An Evidence From Family Businesses in IndiaDocument11 pagesFemales' Representation in The Boardroom and Their Impact On Financial Distress: An Evidence From Family Businesses in IndiaElvira NovianNo ratings yet

- Corporate Governance in Family Owned BusinessesDocument11 pagesCorporate Governance in Family Owned BusinessesAlexander DeckerNo ratings yet

- Factors Influencing Fam Bus DecisionsDocument21 pagesFactors Influencing Fam Bus DecisionsSudipto DuttaNo ratings yet

- Family Ownership and Different Legal EnvironmentsDocument6 pagesFamily Ownership and Different Legal EnvironmentsMarjNo ratings yet

- Diversification, Resource Concentration, and Business Group PerformanceDocument17 pagesDiversification, Resource Concentration, and Business Group PerformancemsekerNo ratings yet

- Nguvo Chapter 1-3 FinalDocument58 pagesNguvo Chapter 1-3 FinaltichaonamuzekenyiNo ratings yet

- Quinn, M., Hiebl, M. R. W., Moores, K., & Craig, J. B. (2018). Future research on management accounting and control in family firms suggestions linked to architecture, governance, entrepreneurship and stewardDocument28 pagesQuinn, M., Hiebl, M. R. W., Moores, K., & Craig, J. B. (2018). Future research on management accounting and control in family firms suggestions linked to architecture, governance, entrepreneurship and stewardjosephyh.tsoNo ratings yet

- Running Head: 1: Application #3: Comparing Common Issues in Family Business GloballyDocument9 pagesRunning Head: 1: Application #3: Comparing Common Issues in Family Business GloballyBrimerNo ratings yet

- Family-Ownership, or Founder-CEO, Does It Matter, For The Firm Performance?Document6 pagesFamily-Ownership, or Founder-CEO, Does It Matter, For The Firm Performance?Central Asian StudiesNo ratings yet

- Journal of Banking & Finance: Jungwook Shim, Hiroyuki OkamuroDocument11 pagesJournal of Banking & Finance: Jungwook Shim, Hiroyuki OkamuroHana MarzoukNo ratings yet

- 1 s2.0 S0148296322001497 MainDocument12 pages1 s2.0 S0148296322001497 MainChairunnisa NisaNo ratings yet

- Ownership Structure, Corporate Governance and Firm Performance (#352663) - 363593Document10 pagesOwnership Structure, Corporate Governance and Firm Performance (#352663) - 363593mrzia996No ratings yet

- FAMILY OWNERS Do - Family - Firms - Outperform - Non-Family - Ones - A - PanelDocument52 pagesFAMILY OWNERS Do - Family - Firms - Outperform - Non-Family - Ones - A - PanelEnny HaryantiNo ratings yet

- Framework of The StudyDocument24 pagesFramework of The StudyZamantha TiangcoNo ratings yet

- Family Leadership Succession and Firm Performance: The Moderating Effect of Tacit Idiosyncratic Firm KnowledgeDocument9 pagesFamily Leadership Succession and Firm Performance: The Moderating Effect of Tacit Idiosyncratic Firm KnowledgemilinrakeshNo ratings yet

- 9143 AamDocument32 pages9143 AamKhaled BarakatNo ratings yet

- Organizational Homeostasis - The Reason your Business, Corporation, and Government will never Fail again, But FlourishFrom EverandOrganizational Homeostasis - The Reason your Business, Corporation, and Government will never Fail again, But FlourishNo ratings yet

- Study of Marketing Mix of Maruti SuzukiDocument96 pagesStudy of Marketing Mix of Maruti SuzukiAjayNo ratings yet

- Brand PortfolioDocument1 pageBrand PortfolioAjayNo ratings yet

- Familybusiness PDFDocument11 pagesFamilybusiness PDFAjayNo ratings yet

- Study of Customer Satisfaction Towards Services Offered by Maruti Suzuki in Wardha CityDocument60 pagesStudy of Customer Satisfaction Towards Services Offered by Maruti Suzuki in Wardha CityAjayNo ratings yet

- Volkswagen Case StudyDocument3 pagesVolkswagen Case StudyAjayNo ratings yet

- Family Business PDFDocument18 pagesFamily Business PDFAjayNo ratings yet

- Quick Notes PEZADocument8 pagesQuick Notes PEZAVic FabeNo ratings yet

- Advantages of AdvertisingDocument4 pagesAdvantages of Advertisingali khanNo ratings yet

- Problem For Total Quality ManagementDocument7 pagesProblem For Total Quality ManagementReb RenNo ratings yet

- Mago Et AlDocument4 pagesMago Et AlSonia PortugaleteNo ratings yet

- Financing Decision: Compiled By: RabachDocument14 pagesFinancing Decision: Compiled By: RabachRafael M. BachanichaNo ratings yet

- ANANAYO-Case Analysis - Assignment 6Document1 pageANANAYO-Case Analysis - Assignment 6Cherie Soriano AnanayoNo ratings yet

- Howden Capabilities Oct 2017 ScreenDocument68 pagesHowden Capabilities Oct 2017 ScreenukdealsNo ratings yet

- WHO STOLE THE AMERICAN DREAM? (Random House, 2012) Academic FlyerDocument2 pagesWHO STOLE THE AMERICAN DREAM? (Random House, 2012) Academic FlyerRandomHouseAcademicNo ratings yet

- Card SheetDocument21 pagesCard SheetJohn MillerNo ratings yet

- SPK Akugrosir 2018 (Staff Gudang) in EnglishDocument3 pagesSPK Akugrosir 2018 (Staff Gudang) in EnglishBimo Mahendra PutraNo ratings yet

- RMK Akl Hal 544-549Document5 pagesRMK Akl Hal 544-549Dizzy nindyaNo ratings yet

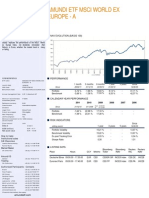

- Amundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - MDocument2 pagesAmundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - Mhp24714303No ratings yet

- Comprehensive Audit of Balance Sheet and Income Statement AccountsDocument25 pagesComprehensive Audit of Balance Sheet and Income Statement AccountsLuigi Enderez Balucan100% (1)

- Farward ContractsDocument31 pagesFarward ContractsTayyaba YounasNo ratings yet

- ACCTG - 1 - Chapter 1 & 2Document39 pagesACCTG - 1 - Chapter 1 & 2Aldeguer Joy PenetranteNo ratings yet

- Acculi Labs' Lyfas PDFDocument8 pagesAcculi Labs' Lyfas PDFHbNo ratings yet

- Seatwork Chapter 9 - Accounting Cycle of A Service BusinessDocument3 pagesSeatwork Chapter 9 - Accounting Cycle of A Service BusinessANNANo ratings yet

- 19BMC205B - Unit1 - Nature of Banking BusinessDocument102 pages19BMC205B - Unit1 - Nature of Banking BusinessTenny .BNo ratings yet

- Group10 SecBDocument9 pagesGroup10 SecBRAHUL ARORANo ratings yet

- A Literature Review On Social Enterprise: Yuting Zhang & Yong LiDocument6 pagesA Literature Review On Social Enterprise: Yuting Zhang & Yong LiJEFFREY WILLIAMS P M 20221013No ratings yet

- Taxtion Law Unit IIDocument44 pagesTaxtion Law Unit IIMathew KanichayNo ratings yet

- BSB52415 Diploma of Marketing and Communication: BSBCRT501 - Originate and Develop Concepts Assessment 1 - ProjectDocument4 pagesBSB52415 Diploma of Marketing and Communication: BSBCRT501 - Originate and Develop Concepts Assessment 1 - ProjectAtcharaNo ratings yet

- Deakin Business Administration Accounting UnitDocument45 pagesDeakin Business Administration Accounting UnitYasiru MahindaratneNo ratings yet

- International Relations and Current Affairs: Answer: (D)Document3 pagesInternational Relations and Current Affairs: Answer: (D)Mujahid Ali0% (1)

- A Feasibility Study: Effectiveness of Using Coupon To Increase The Sales of Boodle Meals Offered by Hub-Eat Boardgame CaféDocument19 pagesA Feasibility Study: Effectiveness of Using Coupon To Increase The Sales of Boodle Meals Offered by Hub-Eat Boardgame CaféJanine GalangNo ratings yet

- The Presentation Is Only Illustrative and Not ExhausitiveDocument97 pagesThe Presentation Is Only Illustrative and Not ExhausitiveUjjwal AnandNo ratings yet

- 6 Miscellaneous TransactionsDocument4 pages6 Miscellaneous TransactionsRichel ArmayanNo ratings yet