Download as pdf or txt

You might also like

- 08 Konys Inc 3Document18 pages08 Konys Inc 3RohanMohapatraNo ratings yet

- Tutorial 4 Capital Investment Decisions 1Document4 pagesTutorial 4 Capital Investment Decisions 1phillip HaulNo ratings yet

- Ques On Capital BudgetingDocument5 pagesQues On Capital BudgetingMonika KauraNo ratings yet

- QuesDocument5 pagesQuesMonika KauraNo ratings yet

- Annual Worth IRR Capital Recovery CostDocument30 pagesAnnual Worth IRR Capital Recovery CostadvikapriyaNo ratings yet

- CBE - Corporate Finance - SPJG - FinalDocument16 pagesCBE - Corporate Finance - SPJG - FinalNguyễn QuyênNo ratings yet

- Required:: Project A Would CostDocument10 pagesRequired:: Project A Would CostSad CharlieNo ratings yet

- Ma 2Document3 pagesMa 2123 123No ratings yet

- Theoretical and Conceptual Questions: (See Notes or Textbook)Document4 pagesTheoretical and Conceptual Questions: (See Notes or Textbook)raymondNo ratings yet

- ACF ProblemsDocument11 pagesACF Problemsnithinnick66No ratings yet

- Worksheet#3-MCQ-2018 .PDF Engineering EconomyDocument6 pagesWorksheet#3-MCQ-2018 .PDF Engineering EconomyOmar F'Kassar0% (1)

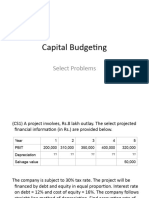

- Capital Budgeting - Select ExercisesDocument12 pagesCapital Budgeting - Select ExercisesNitin MauryaNo ratings yet

- Worksheet#3 MCQ 2016Document6 pagesWorksheet#3 MCQ 2016YaserNo ratings yet

- Exam2505 2012Document8 pagesExam2505 2012Gemeda GirmaNo ratings yet

- Theoretical and Conceptual Questions: (See Notes or Textbook)Document14 pagesTheoretical and Conceptual Questions: (See Notes or Textbook)raymondNo ratings yet

- Investment Appraisal Camb AL New (1) RIKZY EESADocument14 pagesInvestment Appraisal Camb AL New (1) RIKZY EESAAyesha ZainabNo ratings yet

- 2015-Spring-F18-CIA Revision Practice QuestionsDocument2 pages2015-Spring-F18-CIA Revision Practice QuestionsMayal AhmedNo ratings yet

- Practice 6 - QuestionsDocument4 pagesPractice 6 - QuestionsantialonsoNo ratings yet

- Questions - Investment AppraisalDocument2 pagesQuestions - Investment Appraisalpercy mapetere100% (1)

- HCPM Tutorial 6 Project Finance and AppraisalDocument3 pagesHCPM Tutorial 6 Project Finance and AppraisalAjay MeenaNo ratings yet

- Capital Budgeting: Workshop Questions: Finance & Financial ManagementDocument12 pagesCapital Budgeting: Workshop Questions: Finance & Financial ManagementJuan SanguinetiNo ratings yet

- Skkk4173 Assignment #4 2016Document4 pagesSkkk4173 Assignment #4 2016Fhairna BaharulraziNo ratings yet

- 8 Problems On Investment Analysis Vi 1646808679735Document1 page8 Problems On Investment Analysis Vi 1646808679735Risshi AgrawalNo ratings yet

- 10.2 BASTRCSX Learning Activity 9 and 10 - StudentsDocument4 pages10.2 BASTRCSX Learning Activity 9 and 10 - Studentssam imperialNo ratings yet

- Inc. IrrDocument9 pagesInc. IrrtanmayeeNo ratings yet

- Exercise On CVP - CB PDFDocument3 pagesExercise On CVP - CB PDFqwertNo ratings yet

- Cash Flow Probability Cash Flow Probability Proj A Proj B Proj A Year Project A Project B Expected Value Discount Rate PV (Encf)Document10 pagesCash Flow Probability Cash Flow Probability Proj A Proj B Proj A Year Project A Project B Expected Value Discount Rate PV (Encf)hardik100No ratings yet

- Tutorial Questions - Capital Budgeting 2023-1Document16 pagesTutorial Questions - Capital Budgeting 2023-1Richie Ric JuniorNo ratings yet

- Capital Budgeting-1Document3 pagesCapital Budgeting-1Uma NNo ratings yet

- Ii Semester Endterm Examination March 2016Document2 pagesIi Semester Endterm Examination March 2016Nithyananda PatelNo ratings yet

- Assignment#2Document3 pagesAssignment#2Wuhao KoNo ratings yet

- Ex.C.BudgetDocument3 pagesEx.C.BudgetGeethika NayanaprabhaNo ratings yet

- Capita Budgeting QuestionsDocument5 pagesCapita Budgeting QuestionsSULEIMANNo ratings yet

- Capital Budgeting-ProblemsDocument5 pagesCapital Budgeting-ProblemsUday Gowda50% (2)

- Considering $542,000 Payback Payback Period ProjectDocument5 pagesConsidering $542,000 Payback Payback Period ProjectRaibatul AdawiyahNo ratings yet

- Tutorial Sheet - 1 (UNIT-1)Document5 pagesTutorial Sheet - 1 (UNIT-1)Frederick DugayNo ratings yet

- Econ F315 1923 CM 2017 1Document3 pagesEcon F315 1923 CM 2017 1Abhishek GhoshNo ratings yet

- Papc QP 3Document2 pagesPapc QP 3ಡಾ. ರವೀಶ್ ಎನ್ ಎಸ್No ratings yet

- Inc. IrrDocument9 pagesInc. IrrPromaNo ratings yet

- Investment Appraisal/capital Investment: Page 1 of 20Document20 pagesInvestment Appraisal/capital Investment: Page 1 of 20parwez_0505No ratings yet

- Docslide - Us Assignment 2 55844503ab61cDocument4 pagesDocslide - Us Assignment 2 55844503ab61cAhmedNo ratings yet

- Problems of Capital BudgetingDocument4 pagesProblems of Capital Budgetingm agarwalNo ratings yet

- Additional Questions for practiceDocument7 pagesAdditional Questions for practicesuman.roy23-25No ratings yet

- CF - PWS - 5Document3 pagesCF - PWS - 5cyclo tronNo ratings yet

- Project Investment TimingDocument3 pagesProject Investment TimingIrene CheronoNo ratings yet

- Capital Budgeting Practice Questions QueDocument9 pagesCapital Budgeting Practice Questions QuemawandeNo ratings yet

- Engineering Management 3000/5039: Tutorial Set 6Document4 pagesEngineering Management 3000/5039: Tutorial Set 6Sahan100% (1)

- Adfm Iii 2015-17Document3 pagesAdfm Iii 2015-17Nithyananda PatelNo ratings yet

- PS 4 Spring 2021Document2 pagesPS 4 Spring 2021sybiltan123No ratings yet

- Assignment 3 Calculation Questions - 151099758Document12 pagesAssignment 3 Calculation Questions - 151099758Pankaj KhannaNo ratings yet

- Investment Appraisal Review QuestionsDocument5 pagesInvestment Appraisal Review QuestionsGadafi FuadNo ratings yet

- Corporate Finance - Problem Set 03Document8 pagesCorporate Finance - Problem Set 03chaosgw999No ratings yet

- FFM Updated AnswersDocument79 pagesFFM Updated AnswersSrikrishnan S100% (1)

- Capital Budgeting Exercise1Document14 pagesCapital Budgeting Exercise1rohini jha0% (1)

- Capital BudgetingDocument6 pagesCapital BudgetingTarmak LyonNo ratings yet

- LixingcunDocument7 pagesLixingcunmuhammad iman bin kamarudinNo ratings yet

- Iii Semester Endterm Examination November 2016Document3 pagesIii Semester Endterm Examination November 2016Gautam KumarNo ratings yet

- Capital Budgeting: Key Topics To KnowDocument11 pagesCapital Budgeting: Key Topics To KnowBernardo KristineNo ratings yet

- Practice Question For Capital Budgeting: Ans: NPV (P) Rs. 5381, NPV (Q) Rs. 3814Document3 pagesPractice Question For Capital Budgeting: Ans: NPV (P) Rs. 5381, NPV (Q) Rs. 3814Sumit Kumar SahooNo ratings yet

- Economic Insights from Input–Output Tables for Asia and the PacificFrom EverandEconomic Insights from Input–Output Tables for Asia and the PacificNo ratings yet

- Economics of Climate Change Mitigation in Central and West AsiaFrom EverandEconomics of Climate Change Mitigation in Central and West AsiaNo ratings yet

- ARR Tutorial QuestionsDocument2 pagesARR Tutorial QuestionsTheresia RobertNo ratings yet

- Tutorial 4Document1 pageTutorial 4Theresia RobertNo ratings yet

- Tutorial 3Document1 pageTutorial 3Theresia RobertNo ratings yet

- Tutorial 2Document1 pageTutorial 2Theresia RobertNo ratings yet

- pp04Document83 pagespp04sadiaNo ratings yet

- Cost Theory and EstimateDocument35 pagesCost Theory and EstimateThe New Expose AdminNo ratings yet

- UNI 20171127080809034827 1175449 uniROC PrepaidDocument6 pagesUNI 20171127080809034827 1175449 uniROC PrepaidSiew Meng WongNo ratings yet

- Topic 3-4Document14 pagesTopic 3-4Janely BucogNo ratings yet

- EcoDocument300 pagesEcosnj384No ratings yet

- Beximco Chapter 2Document15 pagesBeximco Chapter 2Tanvir Ahmed Rana100% (2)

- Verification of Assets and Liabilities: Basic ConceptsDocument59 pagesVerification of Assets and Liabilities: Basic ConceptsHarikrishnaNo ratings yet

- 3 CFSDocument65 pages3 CFSRocky Bassig100% (1)

- Accounting With AnswersDocument5 pagesAccounting With AnswersGian Karlo Pagarigan50% (2)

- Arvind MillsDocument33 pagesArvind MillshasmukhNo ratings yet

- Equity Research On FMCG SectorDocument41 pagesEquity Research On FMCG SectorRahul Tilak0% (1)

- AmbujaDocument2 pagesAmbujaMohammad DishanNo ratings yet

- IFRS 5, Non-Current Assets Held For Sale and Discontinued Operations: Practical Guide To Application and Expected ChangesDocument42 pagesIFRS 5, Non-Current Assets Held For Sale and Discontinued Operations: Practical Guide To Application and Expected ChangesJahidul ShahNo ratings yet

- Abda LKT Des 2014Document119 pagesAbda LKT Des 2014sleepy platoNo ratings yet

- Chapter 15 - Mergers and AcquisitionsDocument63 pagesChapter 15 - Mergers and AcquisitionsBahzad BalochNo ratings yet

- Partnership Dissolution: Accounting For Special TransactionsDocument58 pagesPartnership Dissolution: Accounting For Special TransactionsjaneNo ratings yet

- Acerinox DissertationDocument42 pagesAcerinox DissertationPrabhdeep singhNo ratings yet

- Handout Fin Man 2305Document7 pagesHandout Fin Man 2305Sheena Gallentes LeysonNo ratings yet

- College Accounting A Contemporary Approach 3rd Edition Haddock Price Farina ISBN Solution ManualDocument22 pagesCollege Accounting A Contemporary Approach 3rd Edition Haddock Price Farina ISBN Solution Manualdonald100% (28)

- Leverage & Risk AnalysisDocument11 pagesLeverage & Risk AnalysisAnkush ChoudharyNo ratings yet

- Working Capital: Estimation and Calculation: de Luna, Regina Carla D. AIME330 - AQ1ArDocument5 pagesWorking Capital: Estimation and Calculation: de Luna, Regina Carla D. AIME330 - AQ1ArRegina De LunaNo ratings yet

- Garlington Technologies Inc S 2013 Financial Statements Are Shown Here Balance SheetDocument1 pageGarlington Technologies Inc S 2013 Financial Statements Are Shown Here Balance SheetAmit PandeyNo ratings yet

- Create A Debt Amortization Schedule For The Following Loan CaseDocument11 pagesCreate A Debt Amortization Schedule For The Following Loan CaseShivamKhareNo ratings yet

- Ross 10e Chap008 StudentDocument42 pagesRoss 10e Chap008 StudentValentin MardonNo ratings yet

- Advanced Corporate Accounting ACCT612Document4 pagesAdvanced Corporate Accounting ACCT612sajid vermaNo ratings yet

- Chapter 2 Part 1 - Ratio AnalysisDocument23 pagesChapter 2 Part 1 - Ratio AnalysisMohamed HosnyNo ratings yet

- Joel Amos Periodic InventoryDocument7 pagesJoel Amos Periodic InventoryJasmine P. Manlungat - EMERALDNo ratings yet

- Managerial Economics in A Global Economy, 5th Edition by Dominick SalvatoreDocument24 pagesManagerial Economics in A Global Economy, 5th Edition by Dominick SalvatoreSaurabh SharmaNo ratings yet

- Solutions To Assigned Exercises Ch2Document17 pagesSolutions To Assigned Exercises Ch2Charmaine Bernados BrucalNo ratings yet