Accounts

Accounts

You might also like

- TCA 1 Questions ACDocument9 pagesTCA 1 Questions ACCristian MazurNo ratings yet

- Content ACCOUNTSDocument7 pagesContent ACCOUNTSjhanvi tandonNo ratings yet

- December 2021 StatementDocument4 pagesDecember 2021 StatementCamila Alejandra Paredes CamposNo ratings yet

- Account Assigment DDDocument6 pagesAccount Assigment DDlubna ghazalNo ratings yet

- Balance Sheet MSDocument7 pagesBalance Sheet MSpavan kumarNo ratings yet

- Section 2 Group 6 FADMDocument77 pagesSection 2 Group 6 FADMRavi KumarNo ratings yet

- Bharat PetrolDocument10 pagesBharat Petroljhanvi tandonNo ratings yet

- BS TataDocument18 pagesBS Tataitubanerjee28No ratings yet

- FA Ratios AssignmentDocument61 pagesFA Ratios AssignmentShambhavi SinhaNo ratings yet

- Group Project - ACCDocument17 pagesGroup Project - ACCLovie GuptaNo ratings yet

- Cost and Management AccountingDocument24 pagesCost and Management AccountingRaina AnishaNo ratings yet

- Group 23 FAC102 ExcelDocument112 pagesGroup 23 FAC102 ExcelrajeshNo ratings yet

- GroupNo04 Assignmet03 YashChavanDocument6 pagesGroupNo04 Assignmet03 YashChavanyashchavan957No ratings yet

- Beneish M ScoreDocument45 pagesBeneish M ScoreAnshu RaiNo ratings yet

- Business Valuation End TermDocument19 pagesBusiness Valuation End TermVaishali GuptaNo ratings yet

- Balance Sheet of Tata Communications: - in Rs. Cr.Document24 pagesBalance Sheet of Tata Communications: - in Rs. Cr.ankush birlaNo ratings yet

- Statement of Profit and Losss Account For The Year Ended 31 ST March 2019Document9 pagesStatement of Profit and Losss Account For The Year Ended 31 ST March 2019Chirag SinghNo ratings yet

- Tata Consultancy ServicesDocument6 pagesTata Consultancy ServicesHarshad PawarNo ratings yet

- Balance Sheet of Life Insurance Corporation of IndiaDocument5 pagesBalance Sheet of Life Insurance Corporation of IndiaPuru JainNo ratings yet

- Finanacial Ratios of HPCLDocument10 pagesFinanacial Ratios of HPCLriyaNo ratings yet

- Ratios of HDFC BankDocument50 pagesRatios of HDFC BankrupaliNo ratings yet

- Assingment SCM SEM4 - 1Document17 pagesAssingment SCM SEM4 - 1KARTHIYAENI VNo ratings yet

- Financial StatementsDocument14 pagesFinancial Statementsthenal kulandaianNo ratings yet

- Hindalco Company's Finance DepartmentDocument14 pagesHindalco Company's Finance DepartmentJaydeep SolankiNo ratings yet

- Financial Management: A Practical Exam Project Report On The Course ofDocument62 pagesFinancial Management: A Practical Exam Project Report On The Course ofshubham shelkeNo ratings yet

- Accounts Assign RatiosDocument58 pagesAccounts Assign Ratiosmamtachaudhary6966No ratings yet

- Balance Sheet I PowerDocument2 pagesBalance Sheet I PowersachdeepsinghsalujaNo ratings yet

- ASHIKDocument21 pagesASHIKmohammedaashik.f2022No ratings yet

- PVR RatioDocument14 pagesPVR RatioApurwa SawarkarNo ratings yet

- Tata Power Balance SheetDocument2 pagesTata Power Balance Sheetakankshakhushi12No ratings yet

- Balance Sheet of Godrej Industries 2021-22Document4 pagesBalance Sheet of Godrej Industries 2021-22Rahul NayakNo ratings yet

- Company Info - Print Financials WordDocument2 pagesCompany Info - Print Financials Wordvivek shuklaNo ratings yet

- Balance Sheet of Zuari GlobalDocument4 pagesBalance Sheet of Zuari GlobalmaheshfbNo ratings yet

- Ratio Analysis of (TCS & Infosys) (Shree Cement & Utratech Cement) AdvancedDocument67 pagesRatio Analysis of (TCS & Infosys) (Shree Cement & Utratech Cement) AdvancedmaneNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print Financials001AAYUSH NANDANo ratings yet

- Chapter 3: Finance Department " Tata Steel LTD": Profit & Loss AccountDocument4 pagesChapter 3: Finance Department " Tata Steel LTD": Profit & Loss Account1075SYBPATEL DHRUVNo ratings yet

- Shipping Corp - Comparative StatementDocument3 pagesShipping Corp - Comparative StatementAkshay SinghNo ratings yet

- FM Assignment (Shilpa Kathuroju-48)Document37 pagesFM Assignment (Shilpa Kathuroju-48)shilpaNo ratings yet

- Agency ProblemDocument10 pagesAgency ProblemKARNATI CHARAN 2028331No ratings yet

- Britannia (MA) Group 2Document33 pagesBritannia (MA) Group 2SimarpreetNo ratings yet

- 2nd LinkDocument8 pages2nd Linktechsagadme.109No ratings yet

- Birla RatioDocument22 pagesBirla RatioveeraranjithNo ratings yet

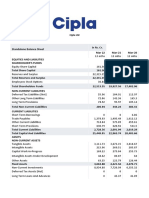

- Cipla LTDDocument6 pagesCipla LTDscribd sogawNo ratings yet

- Accountancy ProjectDocument27 pagesAccountancy ProjectSherin nashwaNo ratings yet

- Assignment1 PDFDocument93 pagesAssignment1 PDFNaman NandwanaNo ratings yet

- Balance Sheet of NLC IndiaDocument8 pagesBalance Sheet of NLC IndiaSweety RoyNo ratings yet

- Itc Balance SheetDocument2 pagesItc Balance SheetRGNNishant BhatiXIIENo ratings yet

- Waa Solar Financial AnalysisDocument18 pagesWaa Solar Financial AnalysisINBASEKARAN PNo ratings yet

- Financial Report of Shivam Cement by SampurnaDocument24 pagesFinancial Report of Shivam Cement by SampurnaSampurna PoudelNo ratings yet

- Abdullah Cia 3Document48 pagesAbdullah Cia 3Maurya KNo ratings yet

- Balance Sheet of Bajaj FinanceDocument8 pagesBalance Sheet of Bajaj FinanceAJ SuriNo ratings yet

- HDFCDocument11 pagesHDFCAshwani KumarNo ratings yet

- PROFITDocument3 pagesPROFITaditya malikNo ratings yet

- Financial Statement AnalysisDocument18 pagesFinancial Statement AnalysisEashaa SaraogiNo ratings yet

- Acc pdf1Document25 pagesAcc pdf1kJSAksdjNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialsDivya PandeyNo ratings yet

- Adani Green Balance SheetDocument2 pagesAdani Green Balance SheetTaksh DhamiNo ratings yet

- Group 13 Bajaj AutoDocument6 pagesGroup 13 Bajaj AutoKshitij MaheshwaryNo ratings yet

- CMA CIA 3 YateeDocument38 pagesCMA CIA 3 YateeYATEE TRIVEDI 21111660No ratings yet

- WSP Financial Analysis V1.4Document68 pagesWSP Financial Analysis V1.4maruthimallepalliNo ratings yet

- Comparative Balance SheetDocument8 pagesComparative Balance Sheet1028No ratings yet

- Comman Size Analysis of Income StatementDocument11 pagesComman Size Analysis of Income Statement4 7No ratings yet

- Mustkim TDocument63 pagesMustkim TArshad ShaikhNo ratings yet

- iCARE Special Lecture Considering The Work of Other PractitionersDocument24 pagesiCARE Special Lecture Considering The Work of Other PractitionersMark Gelo WinchesterNo ratings yet

- Financial Education and Investor AwarenessDocument9 pagesFinancial Education and Investor Awarenessgethu.akiNo ratings yet

- Geometric ProgressionsDocument2 pagesGeometric ProgressionsSandhiya SureshNo ratings yet

- Financial Institutions and MarketsDocument84 pagesFinancial Institutions and Marketsemre kutayNo ratings yet

- Samudera Indonesia TBK - 30 Jun 2023Document115 pagesSamudera Indonesia TBK - 30 Jun 2023cahaya napitupuluNo ratings yet

- Common Application Form For Debt and Liquid Schemes (Please Fill in Block Letters)Document3 pagesCommon Application Form For Debt and Liquid Schemes (Please Fill in Block Letters)Anand NiyogiNo ratings yet

- Objective: Session 15 - External and Internal AuditDocument18 pagesObjective: Session 15 - External and Internal AuditZohair HumayunNo ratings yet

- Intermediate Accounting 1 ReceivablesDocument6 pagesIntermediate Accounting 1 ReceivablesKristine Jewel MirandaNo ratings yet

- BDO Official ReceiptsDocument6 pagesBDO Official ReceiptsGareth TiuNo ratings yet

- Audit-II-Chapter 6Document11 pagesAudit-II-Chapter 6mulunehNo ratings yet

- Formular Rezervare DfdsDocument1 pageFormular Rezervare Dfdscriss5078No ratings yet

- CRING Bank Facilitator by SPEDocument27 pagesCRING Bank Facilitator by SPEDaniel AdrianNo ratings yet

- Mba Financial AssgDocument10 pagesMba Financial Assgseifu deraraNo ratings yet

- Finance For HR: Pitabas MohantyDocument29 pagesFinance For HR: Pitabas MohantyNeeraj SNo ratings yet

- Ashoka Buildcon Limited: Healthy Business Outlook StaysDocument6 pagesAshoka Buildcon Limited: Healthy Business Outlook StaysdarshanmadeNo ratings yet

- A Study of Non Performing Assets With Special Reference To Icici BankDocument58 pagesA Study of Non Performing Assets With Special Reference To Icici BankrimcyNo ratings yet

- Consortium AdvancesDocument10 pagesConsortium Advancesmedhekar_renukaNo ratings yet

- FinancialDocument2 pagesFinancialgeorge muchuhaNo ratings yet

- CH 2Document2 pagesCH 2Aryan RawatNo ratings yet

- Cambrian Mall Banking Centre - Sault Sainte Marie, Ontario Banking - CIBCDocument3 pagesCambrian Mall Banking Centre - Sault Sainte Marie, Ontario Banking - CIBCGopi NathNo ratings yet

- Limitations of Ratio Analysis: Creative AccountingDocument2 pagesLimitations of Ratio Analysis: Creative AccountingGerron ThomasNo ratings yet

- Fin 433 Assigment Spring 2021Document5 pagesFin 433 Assigment Spring 2021ishmam faiyajNo ratings yet

- Banking On Non Bankinbanking-On-Non-Banking-Finance-CompaniesDocument32 pagesBanking On Non Bankinbanking-On-Non-Banking-Finance-CompaniesBharat LimayeNo ratings yet

- Assignment No. 1 (2802)Document4 pagesAssignment No. 1 (2802)Uzair MayaNo ratings yet

- Kunal Project PDFDocument79 pagesKunal Project PDFRohit KumarNo ratings yet

- This Study Resource Was: QuestionsDocument5 pagesThis Study Resource Was: QuestionsXNo ratings yet

Download as docx, pdf, or txt

You might also like

- TCA 1 Questions ACDocument9 pagesTCA 1 Questions ACCristian MazurNo ratings yet

- Content ACCOUNTSDocument7 pagesContent ACCOUNTSjhanvi tandonNo ratings yet

- December 2021 StatementDocument4 pagesDecember 2021 StatementCamila Alejandra Paredes CamposNo ratings yet

- Account Assigment DDDocument6 pagesAccount Assigment DDlubna ghazalNo ratings yet

- Balance Sheet MSDocument7 pagesBalance Sheet MSpavan kumarNo ratings yet

- Section 2 Group 6 FADMDocument77 pagesSection 2 Group 6 FADMRavi KumarNo ratings yet

- Bharat PetrolDocument10 pagesBharat Petroljhanvi tandonNo ratings yet

- BS TataDocument18 pagesBS Tataitubanerjee28No ratings yet

- FA Ratios AssignmentDocument61 pagesFA Ratios AssignmentShambhavi SinhaNo ratings yet

- Group Project - ACCDocument17 pagesGroup Project - ACCLovie GuptaNo ratings yet

- Cost and Management AccountingDocument24 pagesCost and Management AccountingRaina AnishaNo ratings yet

- Group 23 FAC102 ExcelDocument112 pagesGroup 23 FAC102 ExcelrajeshNo ratings yet

- GroupNo04 Assignmet03 YashChavanDocument6 pagesGroupNo04 Assignmet03 YashChavanyashchavan957No ratings yet

- Beneish M ScoreDocument45 pagesBeneish M ScoreAnshu RaiNo ratings yet

- Business Valuation End TermDocument19 pagesBusiness Valuation End TermVaishali GuptaNo ratings yet

- Balance Sheet of Tata Communications: - in Rs. Cr.Document24 pagesBalance Sheet of Tata Communications: - in Rs. Cr.ankush birlaNo ratings yet

- Statement of Profit and Losss Account For The Year Ended 31 ST March 2019Document9 pagesStatement of Profit and Losss Account For The Year Ended 31 ST March 2019Chirag SinghNo ratings yet

- Tata Consultancy ServicesDocument6 pagesTata Consultancy ServicesHarshad PawarNo ratings yet

- Balance Sheet of Life Insurance Corporation of IndiaDocument5 pagesBalance Sheet of Life Insurance Corporation of IndiaPuru JainNo ratings yet

- Finanacial Ratios of HPCLDocument10 pagesFinanacial Ratios of HPCLriyaNo ratings yet

- Ratios of HDFC BankDocument50 pagesRatios of HDFC BankrupaliNo ratings yet

- Assingment SCM SEM4 - 1Document17 pagesAssingment SCM SEM4 - 1KARTHIYAENI VNo ratings yet

- Financial StatementsDocument14 pagesFinancial Statementsthenal kulandaianNo ratings yet

- Hindalco Company's Finance DepartmentDocument14 pagesHindalco Company's Finance DepartmentJaydeep SolankiNo ratings yet

- Financial Management: A Practical Exam Project Report On The Course ofDocument62 pagesFinancial Management: A Practical Exam Project Report On The Course ofshubham shelkeNo ratings yet

- Accounts Assign RatiosDocument58 pagesAccounts Assign Ratiosmamtachaudhary6966No ratings yet

- Balance Sheet I PowerDocument2 pagesBalance Sheet I PowersachdeepsinghsalujaNo ratings yet

- ASHIKDocument21 pagesASHIKmohammedaashik.f2022No ratings yet

- PVR RatioDocument14 pagesPVR RatioApurwa SawarkarNo ratings yet

- Tata Power Balance SheetDocument2 pagesTata Power Balance Sheetakankshakhushi12No ratings yet

- Balance Sheet of Godrej Industries 2021-22Document4 pagesBalance Sheet of Godrej Industries 2021-22Rahul NayakNo ratings yet

- Company Info - Print Financials WordDocument2 pagesCompany Info - Print Financials Wordvivek shuklaNo ratings yet

- Balance Sheet of Zuari GlobalDocument4 pagesBalance Sheet of Zuari GlobalmaheshfbNo ratings yet

- Ratio Analysis of (TCS & Infosys) (Shree Cement & Utratech Cement) AdvancedDocument67 pagesRatio Analysis of (TCS & Infosys) (Shree Cement & Utratech Cement) AdvancedmaneNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print Financials001AAYUSH NANDANo ratings yet

- Chapter 3: Finance Department " Tata Steel LTD": Profit & Loss AccountDocument4 pagesChapter 3: Finance Department " Tata Steel LTD": Profit & Loss Account1075SYBPATEL DHRUVNo ratings yet

- Shipping Corp - Comparative StatementDocument3 pagesShipping Corp - Comparative StatementAkshay SinghNo ratings yet

- FM Assignment (Shilpa Kathuroju-48)Document37 pagesFM Assignment (Shilpa Kathuroju-48)shilpaNo ratings yet

- Agency ProblemDocument10 pagesAgency ProblemKARNATI CHARAN 2028331No ratings yet

- Britannia (MA) Group 2Document33 pagesBritannia (MA) Group 2SimarpreetNo ratings yet

- 2nd LinkDocument8 pages2nd Linktechsagadme.109No ratings yet

- Birla RatioDocument22 pagesBirla RatioveeraranjithNo ratings yet

- Cipla LTDDocument6 pagesCipla LTDscribd sogawNo ratings yet

- Accountancy ProjectDocument27 pagesAccountancy ProjectSherin nashwaNo ratings yet

- Assignment1 PDFDocument93 pagesAssignment1 PDFNaman NandwanaNo ratings yet

- Balance Sheet of NLC IndiaDocument8 pagesBalance Sheet of NLC IndiaSweety RoyNo ratings yet

- Itc Balance SheetDocument2 pagesItc Balance SheetRGNNishant BhatiXIIENo ratings yet

- Waa Solar Financial AnalysisDocument18 pagesWaa Solar Financial AnalysisINBASEKARAN PNo ratings yet

- Financial Report of Shivam Cement by SampurnaDocument24 pagesFinancial Report of Shivam Cement by SampurnaSampurna PoudelNo ratings yet

- Abdullah Cia 3Document48 pagesAbdullah Cia 3Maurya KNo ratings yet

- Balance Sheet of Bajaj FinanceDocument8 pagesBalance Sheet of Bajaj FinanceAJ SuriNo ratings yet

- HDFCDocument11 pagesHDFCAshwani KumarNo ratings yet

- PROFITDocument3 pagesPROFITaditya malikNo ratings yet

- Financial Statement AnalysisDocument18 pagesFinancial Statement AnalysisEashaa SaraogiNo ratings yet

- Acc pdf1Document25 pagesAcc pdf1kJSAksdjNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialsDivya PandeyNo ratings yet

- Adani Green Balance SheetDocument2 pagesAdani Green Balance SheetTaksh DhamiNo ratings yet

- Group 13 Bajaj AutoDocument6 pagesGroup 13 Bajaj AutoKshitij MaheshwaryNo ratings yet

- CMA CIA 3 YateeDocument38 pagesCMA CIA 3 YateeYATEE TRIVEDI 21111660No ratings yet

- WSP Financial Analysis V1.4Document68 pagesWSP Financial Analysis V1.4maruthimallepalliNo ratings yet

- Comparative Balance SheetDocument8 pagesComparative Balance Sheet1028No ratings yet

- Comman Size Analysis of Income StatementDocument11 pagesComman Size Analysis of Income Statement4 7No ratings yet

- Mustkim TDocument63 pagesMustkim TArshad ShaikhNo ratings yet

- iCARE Special Lecture Considering The Work of Other PractitionersDocument24 pagesiCARE Special Lecture Considering The Work of Other PractitionersMark Gelo WinchesterNo ratings yet

- Financial Education and Investor AwarenessDocument9 pagesFinancial Education and Investor Awarenessgethu.akiNo ratings yet

- Geometric ProgressionsDocument2 pagesGeometric ProgressionsSandhiya SureshNo ratings yet

- Financial Institutions and MarketsDocument84 pagesFinancial Institutions and Marketsemre kutayNo ratings yet

- Samudera Indonesia TBK - 30 Jun 2023Document115 pagesSamudera Indonesia TBK - 30 Jun 2023cahaya napitupuluNo ratings yet

- Common Application Form For Debt and Liquid Schemes (Please Fill in Block Letters)Document3 pagesCommon Application Form For Debt and Liquid Schemes (Please Fill in Block Letters)Anand NiyogiNo ratings yet

- Objective: Session 15 - External and Internal AuditDocument18 pagesObjective: Session 15 - External and Internal AuditZohair HumayunNo ratings yet

- Intermediate Accounting 1 ReceivablesDocument6 pagesIntermediate Accounting 1 ReceivablesKristine Jewel MirandaNo ratings yet

- BDO Official ReceiptsDocument6 pagesBDO Official ReceiptsGareth TiuNo ratings yet

- Audit-II-Chapter 6Document11 pagesAudit-II-Chapter 6mulunehNo ratings yet

- Formular Rezervare DfdsDocument1 pageFormular Rezervare Dfdscriss5078No ratings yet

- CRING Bank Facilitator by SPEDocument27 pagesCRING Bank Facilitator by SPEDaniel AdrianNo ratings yet

- Mba Financial AssgDocument10 pagesMba Financial Assgseifu deraraNo ratings yet

- Finance For HR: Pitabas MohantyDocument29 pagesFinance For HR: Pitabas MohantyNeeraj SNo ratings yet

- Ashoka Buildcon Limited: Healthy Business Outlook StaysDocument6 pagesAshoka Buildcon Limited: Healthy Business Outlook StaysdarshanmadeNo ratings yet

- A Study of Non Performing Assets With Special Reference To Icici BankDocument58 pagesA Study of Non Performing Assets With Special Reference To Icici BankrimcyNo ratings yet

- Consortium AdvancesDocument10 pagesConsortium Advancesmedhekar_renukaNo ratings yet

- FinancialDocument2 pagesFinancialgeorge muchuhaNo ratings yet

- CH 2Document2 pagesCH 2Aryan RawatNo ratings yet

- Cambrian Mall Banking Centre - Sault Sainte Marie, Ontario Banking - CIBCDocument3 pagesCambrian Mall Banking Centre - Sault Sainte Marie, Ontario Banking - CIBCGopi NathNo ratings yet

- Limitations of Ratio Analysis: Creative AccountingDocument2 pagesLimitations of Ratio Analysis: Creative AccountingGerron ThomasNo ratings yet

- Fin 433 Assigment Spring 2021Document5 pagesFin 433 Assigment Spring 2021ishmam faiyajNo ratings yet

- Banking On Non Bankinbanking-On-Non-Banking-Finance-CompaniesDocument32 pagesBanking On Non Bankinbanking-On-Non-Banking-Finance-CompaniesBharat LimayeNo ratings yet

- Assignment No. 1 (2802)Document4 pagesAssignment No. 1 (2802)Uzair MayaNo ratings yet

- Kunal Project PDFDocument79 pagesKunal Project PDFRohit KumarNo ratings yet

- This Study Resource Was: QuestionsDocument5 pagesThis Study Resource Was: QuestionsXNo ratings yet