Download as pdf or txt

You might also like

- Accounting Standard SummaryDocument35 pagesAccounting Standard SummaryNikita Kukreja67% (3)

- Topic-8 Difference Between Indian Accounting Standards and IfrsDocument69 pagesTopic-8 Difference Between Indian Accounting Standards and IfrsPahul Walia83% (6)

- Income Computation and Disclosure Standard (Icds) : CA. Ritesh MittalDocument143 pagesIncome Computation and Disclosure Standard (Icds) : CA. Ritesh MittalSubrat MohapatraNo ratings yet

- Icds - Rae 2021Document50 pagesIcds - Rae 2021Priya RanaNo ratings yet

- Accounting StandradsDocument21 pagesAccounting Standrads119936232141No ratings yet

- FRRB IssuesDocument47 pagesFRRB IssuesAayushi AroraNo ratings yet

- Impact Analysis - ICDSDocument50 pagesImpact Analysis - ICDSRaghavendra RahulNo ratings yet

- Income Computation and Disclosure Standards: ICDS 2016 Ca Farooq HaqueDocument33 pagesIncome Computation and Disclosure Standards: ICDS 2016 Ca Farooq HaqueDheeraj SharmaNo ratings yet

- Financial Accounting: Aarsh SainiDocument37 pagesFinancial Accounting: Aarsh SainiAarsh SainiNo ratings yet

- Index: SR No Particulars Page NoDocument33 pagesIndex: SR No Particulars Page NoKaran KhatriNo ratings yet

- Accounting StandardsDocument28 pagesAccounting StandardsIbrahim BashaNo ratings yet

- TaxmannPPT Impact of Ind AS On Corporate Tax 1686937084Document32 pagesTaxmannPPT Impact of Ind AS On Corporate Tax 1686937084Praveen KumarNo ratings yet

- Accounting Standard-1Document27 pagesAccounting Standard-1Kshitiz TripathiNo ratings yet

- Accounting Standards IndiaDocument49 pagesAccounting Standards IndiaDivij KumarNo ratings yet

- Accounting StandardsDocument50 pagesAccounting StandardsMadhurima MitraNo ratings yet

- As Quick PDFDocument23 pagesAs Quick PDFChandreshNo ratings yet

- Accounting Standards 5Document13 pagesAccounting Standards 5prash1820No ratings yet

- (Income Computation & Disclosure Standards) : Income in Light of IcdsDocument25 pages(Income Computation & Disclosure Standards) : Income in Light of IcdsEswarReddyEegaNo ratings yet

- As 1 - Disclosure of Accounting PoliciesDocument20 pagesAs 1 - Disclosure of Accounting Policiestaurianniki100% (1)

- 1.3) Accounting StandardsDocument15 pages1.3) Accounting StandardsF93 SHIFA KHANNo ratings yet

- Accounts & Adv Account BookDocument308 pagesAccounts & Adv Account Bookvishnuverma100% (1)

- ASFR - Unit 2 - 2024Document89 pagesASFR - Unit 2 - 2024vishalsingh9669No ratings yet

- Indian Accounting Standards (Indas) : Practical Aspects, Case Studies and Recent Developments - Presented by Jatin KanabarDocument46 pagesIndian Accounting Standards (Indas) : Practical Aspects, Case Studies and Recent Developments - Presented by Jatin KanabarKANADARPARNo ratings yet

- Accounting StandardsDocument20 pagesAccounting StandardsApaar GoyalNo ratings yet

- References BitCoinDocument27 pagesReferences BitCoinVeerNo ratings yet

- Afm Module A SummaryDocument73 pagesAfm Module A SummaryAditya KaushalNo ratings yet

- On COVID-19 Impact PDFDocument47 pagesOn COVID-19 Impact PDFmuralitharannNo ratings yet

- 115 Financial AccountingDocument115 pages115 Financial AccountingAbhishek IyerNo ratings yet

- 00 Tapovan Advanced Accounting Free Fasttrack Batch BenchmarkDocument144 pages00 Tapovan Advanced Accounting Free Fasttrack Batch BenchmarkDhiraj JaiswalNo ratings yet

- Accounting Standards 32Document91 pagesAccounting Standards 32bathinisridhar100% (3)

- Accounting Standards S.ClementDocument109 pagesAccounting Standards S.Clementabhi_chess22No ratings yet

- Accounting StandardsDocument109 pagesAccounting StandardsJugal Shah100% (1)

- Chapter14-Accounting Conventions and PoliceDocument33 pagesChapter14-Accounting Conventions and Policelove_oct22100% (1)

- CA CS VIJAY SARDA VSMART Academy 8956651954Document9 pagesCA CS VIJAY SARDA VSMART Academy 8956651954naga jaganNo ratings yet

- Accounts 3Document12 pagesAccounts 3latestNo ratings yet

- Accounting StandardDocument58 pagesAccounting StandardKarthik SeshadriNo ratings yet

- Lecture 1 FSADocument26 pagesLecture 1 FSAvuthithuylinh9a007No ratings yet

- Disclosure of Accounting Policies: ObjectivesDocument8 pagesDisclosure of Accounting Policies: ObjectivesrazorNo ratings yet

- IFRS Pocket GuideDocument77 pagesIFRS Pocket GuideJennyNo ratings yet

- Disclosures Under ICDSDocument11 pagesDisclosures Under ICDScadrjainNo ratings yet

- Account BookDocument311 pagesAccount BookRam patharvat100% (1)

- Summaries of International Accounting StandardsDocument69 pagesSummaries of International Accounting Standardsmaryam rajputtNo ratings yet

- 44AD As and What NotDocument82 pages44AD As and What NotParikshitNo ratings yet

- 6 - IasDocument25 pages6 - Iasking brothersNo ratings yet

- Ind-AS PDFDocument4 pagesInd-AS PDFManish MalikNo ratings yet

- Indian Accounting StandardsDocument26 pagesIndian Accounting StandardsISHANJALI MADAAN 219005No ratings yet

- Accounting Standards Tanmay AroraDocument133 pagesAccounting Standards Tanmay AroratanmayaroraNo ratings yet

- Accounting Standards Board (ASB) in 1977Document15 pagesAccounting Standards Board (ASB) in 1977ashish kumar jhaNo ratings yet

- Accounting Standards Board (ASB) in 1977Document15 pagesAccounting Standards Board (ASB) in 1977amit kathaitNo ratings yet

- Assignment 1 Describe The System of Developing Indian Accounting StandardsDocument20 pagesAssignment 1 Describe The System of Developing Indian Accounting StandardsShashank100% (1)

- Accounting Standard 170417Document32 pagesAccounting Standard 170417selvam sNo ratings yet

- AS Theory CA IPCC I & IIDocument19 pagesAS Theory CA IPCC I & IICaramakr ManthaNo ratings yet

- Nestle Project - AccountsDocument31 pagesNestle Project - AccountsNishant Shah75% (4)

- Presented by Ajesh Mukundan PDocument17 pagesPresented by Ajesh Mukundan PAjesh Mukundan P100% (1)

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- Chapter 6 Designing Global Supply Chain NetworksDocument22 pagesChapter 6 Designing Global Supply Chain NetworksRashadafaneh100% (1)

- Lobrigas Unit3 Topic2 AssessmentDocument6 pagesLobrigas Unit3 Topic2 AssessmentClaudine LobrigasNo ratings yet

- Final Exam Cheat Sheet ADM1340Document11 pagesFinal Exam Cheat Sheet ADM1340Chaz PresserNo ratings yet

- AccountancyDocument19 pagesAccountancyAmit VermaNo ratings yet

- Section L9: Office Phone Email Office HoursDocument9 pagesSection L9: Office Phone Email Office HoursSanjana ManikandanNo ratings yet

- Compensation Project 1Document10 pagesCompensation Project 1Digital EraNo ratings yet

- Partnership Study GuideDocument21 pagesPartnership Study GuideAngelo Henry AbellarNo ratings yet

- Batch 18 1st Preboard (P1)Document14 pagesBatch 18 1st Preboard (P1)Jericho PedragosaNo ratings yet

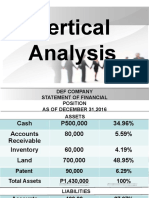

- Vertical AnalysisDocument8 pagesVertical AnalysisHannah Mae BautistaNo ratings yet

- S - Ch7 - Long Term Objectives and StrategiesDocument31 pagesS - Ch7 - Long Term Objectives and StrategiesYion LekNo ratings yet

- International Relations and Current Affairs: Answer: (D)Document3 pagesInternational Relations and Current Affairs: Answer: (D)Mujahid Ali0% (1)

- Day Trading by Matthew MayburyDocument52 pagesDay Trading by Matthew MayburyXRM09090% (1)

- How To Use Binary Options StrategiesDocument28 pagesHow To Use Binary Options Strategiessumilang100% (1)

- Percentage Practice QsDocument14 pagesPercentage Practice Qsshawbikky26No ratings yet

- TOR Capital Invesment Planning (CIP)Document45 pagesTOR Capital Invesment Planning (CIP)ode syahrunNo ratings yet

- 2014 Mba Brochure - McGill University CanadaDocument23 pages2014 Mba Brochure - McGill University CanadaAlda ArdeliaNo ratings yet

- Date of Establishment: 1981: - Vision and Core Values: "We Believe Our Core Values Drive Us in Every Endeavour."Document6 pagesDate of Establishment: 1981: - Vision and Core Values: "We Believe Our Core Values Drive Us in Every Endeavour."Akhila AyyappanNo ratings yet

- Law and Economics ProjectDocument12 pagesLaw and Economics ProjectSankalp PatelNo ratings yet

- QSB ProfessionalDocument76 pagesQSB ProfessionalAdeniran AfolamiNo ratings yet

- FIN 254 - Chapter 1Document23 pagesFIN 254 - Chapter 1habibNo ratings yet

- Econ 2113 - Homework 2Document4 pagesEcon 2113 - Homework 2NamanNo ratings yet

- 19 Valuation of Goodwill PDFDocument5 pages19 Valuation of Goodwill PDF801chiru801100% (1)

- A Study On Financial Performance of Axis Bank in Comparison of HDFC Bank and Icici BankDocument99 pagesA Study On Financial Performance of Axis Bank in Comparison of HDFC Bank and Icici Bankjenish modiNo ratings yet

- Jorc Geo e STT MDocument176 pagesJorc Geo e STT MAde PrayudaNo ratings yet

- Nepal TaxDocument7 pagesNepal Taxsanjay kafleNo ratings yet

- LANDBANK Weaccess Terms and ConditionsDocument4 pagesLANDBANK Weaccess Terms and ConditionsSabang High School (Region IV-B - Oriental Mindoro)No ratings yet

- Chapter 6 Special Situations - ModuleDocument3 pagesChapter 6 Special Situations - ModuleJoannah maeNo ratings yet

- Module 2 ENTREPRENEURSHIPDocument26 pagesModule 2 ENTREPRENEURSHIPTricia Ann A. SodsodNo ratings yet

- Adi Setia - Islamic Transactional LawDocument42 pagesAdi Setia - Islamic Transactional LawAmru Khalid SazaliNo ratings yet

- Act1204-Quiz No. 4 Wit AnsDocument5 pagesAct1204-Quiz No. 4 Wit AnsmarkNo ratings yet