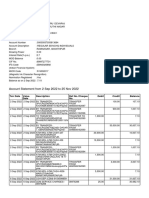

MULTIFINANCING

MULTIFINANCING

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Lion FundDocument4 pagesThe Lion Fundforbesadmin100% (1)

- Online Cash PaluwaganDocument1 pageOnline Cash PaluwaganNapoleonPascualNo ratings yet

- Reserved MattersDocument3 pagesReserved MattersWong kang xianNo ratings yet

- Valuation of Orion PharmaDocument25 pagesValuation of Orion PharmaKola0% (1)

- WorldCom Fraud PPT (Accounting Learning)Document12 pagesWorldCom Fraud PPT (Accounting Learning)蒲睿灵No ratings yet

- Bab 6,7,8,9 Canvas BMCDocument19 pagesBab 6,7,8,9 Canvas BMCAl HadidNo ratings yet

- MOCK - MCQ PracticeDocument10 pagesMOCK - MCQ PracticeArjun RastogiNo ratings yet

- ACF L 4 ExamDocument5 pagesACF L 4 ExamJemal SeidNo ratings yet

- Account Statement From 2 Sep 2022 To 25 Nov 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 2 Sep 2022 To 25 Nov 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRaju BhaiNo ratings yet

- Chola MS Insurance Annual Report 2019 20Document139 pagesChola MS Insurance Annual Report 2019 20happy39No ratings yet

- Book-Keeping, Book-Keeping & Accounts (IAS) PDFDocument118 pagesBook-Keeping, Book-Keeping & Accounts (IAS) PDFEngery Man100% (2)

- Interim Report Q1 2024 15 05 2024Document87 pagesInterim Report Q1 2024 15 05 2024bisengalievasNo ratings yet

- China Evergrande WINDING UP OF THE COMPANY APPOINTMENT OF JOINT AND SEVERALDocument2 pagesChina Evergrande WINDING UP OF THE COMPANY APPOINTMENT OF JOINT AND SEVERALchukingfungNo ratings yet

- Review of LitertaureDocument6 pagesReview of LitertaureeshuNo ratings yet

- Solutions To End-Of-Chapter Problems 11Document6 pagesSolutions To End-Of-Chapter Problems 11weeeeeshNo ratings yet

- ACCO 30023 - Accounting For Business Combination (IM)Document74 pagesACCO 30023 - Accounting For Business Combination (IM)rachel banana hammockNo ratings yet

- Advanced Financial Accounting Course OutlineDocument5 pagesAdvanced Financial Accounting Course OutlineEriqNo ratings yet

- Current Account BrochureDocument8 pagesCurrent Account BrochureNitin BNo ratings yet

- Operating and Financial Leverage: Block, Hirt, and DanielsenDocument31 pagesOperating and Financial Leverage: Block, Hirt, and DanielsenOona NiallNo ratings yet

- DECEMBER 31, 2018 (In Rupiah) : PT - Jayatama Cash Flow ReportDocument3 pagesDECEMBER 31, 2018 (In Rupiah) : PT - Jayatama Cash Flow ReportSiti zahqiahNo ratings yet

- Rights and Duties of Company AuditorDocument8 pagesRights and Duties of Company AuditorShaji JkNo ratings yet

- Prada Hec Paris Case StudyDocument9 pagesPrada Hec Paris Case StudyelatobouloNo ratings yet

- Comparative & Common Size 2024 SPCCDocument23 pagesComparative & Common Size 2024 SPCCborichaharsha08No ratings yet

- Atlas Honda: Analysis of Financial Statements Balance SheetDocument4 pagesAtlas Honda: Analysis of Financial Statements Balance Sheetrouf786No ratings yet

- HDFC Equity Fund SIP JourneyDocument2 pagesHDFC Equity Fund SIP JourneyVasu TrivediNo ratings yet

- 1Document5 pages1firoozdasmanNo ratings yet

- Ansaldo STS: An Unexpected Stop On A High Speed LineDocument5 pagesAnsaldo STS: An Unexpected Stop On A High Speed LinecarlonewmannNo ratings yet

- SBR 2012 - Dec - QDocument7 pagesSBR 2012 - Dec - QAliNo ratings yet

- Ukk 2023 P2-Kunci Jawaban RevDocument47 pagesUkk 2023 P2-Kunci Jawaban RevSaepul RohmanNo ratings yet

- Brand Equity MMMDocument36 pagesBrand Equity MMMmwings24No ratings yet

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Lion FundDocument4 pagesThe Lion Fundforbesadmin100% (1)

- Online Cash PaluwaganDocument1 pageOnline Cash PaluwaganNapoleonPascualNo ratings yet

- Reserved MattersDocument3 pagesReserved MattersWong kang xianNo ratings yet

- Valuation of Orion PharmaDocument25 pagesValuation of Orion PharmaKola0% (1)

- WorldCom Fraud PPT (Accounting Learning)Document12 pagesWorldCom Fraud PPT (Accounting Learning)蒲睿灵No ratings yet

- Bab 6,7,8,9 Canvas BMCDocument19 pagesBab 6,7,8,9 Canvas BMCAl HadidNo ratings yet

- MOCK - MCQ PracticeDocument10 pagesMOCK - MCQ PracticeArjun RastogiNo ratings yet

- ACF L 4 ExamDocument5 pagesACF L 4 ExamJemal SeidNo ratings yet

- Account Statement From 2 Sep 2022 To 25 Nov 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 2 Sep 2022 To 25 Nov 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRaju BhaiNo ratings yet

- Chola MS Insurance Annual Report 2019 20Document139 pagesChola MS Insurance Annual Report 2019 20happy39No ratings yet

- Book-Keeping, Book-Keeping & Accounts (IAS) PDFDocument118 pagesBook-Keeping, Book-Keeping & Accounts (IAS) PDFEngery Man100% (2)

- Interim Report Q1 2024 15 05 2024Document87 pagesInterim Report Q1 2024 15 05 2024bisengalievasNo ratings yet

- China Evergrande WINDING UP OF THE COMPANY APPOINTMENT OF JOINT AND SEVERALDocument2 pagesChina Evergrande WINDING UP OF THE COMPANY APPOINTMENT OF JOINT AND SEVERALchukingfungNo ratings yet

- Review of LitertaureDocument6 pagesReview of LitertaureeshuNo ratings yet

- Solutions To End-Of-Chapter Problems 11Document6 pagesSolutions To End-Of-Chapter Problems 11weeeeeshNo ratings yet

- ACCO 30023 - Accounting For Business Combination (IM)Document74 pagesACCO 30023 - Accounting For Business Combination (IM)rachel banana hammockNo ratings yet

- Advanced Financial Accounting Course OutlineDocument5 pagesAdvanced Financial Accounting Course OutlineEriqNo ratings yet

- Current Account BrochureDocument8 pagesCurrent Account BrochureNitin BNo ratings yet

- Operating and Financial Leverage: Block, Hirt, and DanielsenDocument31 pagesOperating and Financial Leverage: Block, Hirt, and DanielsenOona NiallNo ratings yet

- DECEMBER 31, 2018 (In Rupiah) : PT - Jayatama Cash Flow ReportDocument3 pagesDECEMBER 31, 2018 (In Rupiah) : PT - Jayatama Cash Flow ReportSiti zahqiahNo ratings yet

- Rights and Duties of Company AuditorDocument8 pagesRights and Duties of Company AuditorShaji JkNo ratings yet

- Prada Hec Paris Case StudyDocument9 pagesPrada Hec Paris Case StudyelatobouloNo ratings yet

- Comparative & Common Size 2024 SPCCDocument23 pagesComparative & Common Size 2024 SPCCborichaharsha08No ratings yet

- Atlas Honda: Analysis of Financial Statements Balance SheetDocument4 pagesAtlas Honda: Analysis of Financial Statements Balance Sheetrouf786No ratings yet

- HDFC Equity Fund SIP JourneyDocument2 pagesHDFC Equity Fund SIP JourneyVasu TrivediNo ratings yet

- 1Document5 pages1firoozdasmanNo ratings yet

- Ansaldo STS: An Unexpected Stop On A High Speed LineDocument5 pagesAnsaldo STS: An Unexpected Stop On A High Speed LinecarlonewmannNo ratings yet

- SBR 2012 - Dec - QDocument7 pagesSBR 2012 - Dec - QAliNo ratings yet

- Ukk 2023 P2-Kunci Jawaban RevDocument47 pagesUkk 2023 P2-Kunci Jawaban RevSaepul RohmanNo ratings yet

- Brand Equity MMMDocument36 pagesBrand Equity MMMmwings24No ratings yet