ARIMA Models and Intervention Analysis - R-Bloggers

ARIMA Models and Intervention Analysis - R-Bloggers

You might also like

- Kassambara, Alboukadel - Machine Learning Essentials - Practical Guide in R (2018)Document424 pagesKassambara, Alboukadel - Machine Learning Essentials - Practical Guide in R (2018)Mrcrismath g100% (1)

- Study PlanDocument3 pagesStudy PlanYan Kyaw100% (1)

- Principal Components Analysis and Redundancy AnalysisDocument18 pagesPrincipal Components Analysis and Redundancy AnalysisJosé António PereiraNo ratings yet

- Reading Keys Projectable New Edition The United PDFDocument7 pagesReading Keys Projectable New Edition The United PDFNisan BaharNo ratings yet

- Vis Corel Matrix Using CoringDocument17 pagesVis Corel Matrix Using CoringsambalasakthiNo ratings yet

- Boruta Feature Selection in R - DataCampDocument18 pagesBoruta Feature Selection in R - DataCamphabeeb4saNo ratings yet

- R PCA (Principal Component Analysis) - DataCampDocument54 pagesR PCA (Principal Component Analysis) - DataCampUMESH D RNo ratings yet

- RBasics HandoutDocument6 pagesRBasics HandoutHassan AlsafiNo ratings yet

- R Handbook - Regression For Count DataDocument13 pagesR Handbook - Regression For Count Dataclyn.beeNo ratings yet

- Likert-Plots and Grouped Likert-Plots #Rstats - R-BloggersDocument7 pagesLikert-Plots and Grouped Likert-Plots #Rstats - R-BloggersLeonardo Talavera CamposNo ratings yet

- The Art of Data Visualization - Learn 7 Visualizations in RDocument15 pagesThe Art of Data Visualization - Learn 7 Visualizations in RHéctor W Moreno QNo ratings yet

- Package Gesca': R Topics DocumentedDocument15 pagesPackage Gesca': R Topics DocumentedfarisNo ratings yet

- Template For GigaByte Journal Update SubmissionsDocument8 pagesTemplate For GigaByte Journal Update SubmissionsniyawnaniyawNo ratings yet

- LRresidualsDocument9 pagesLRresidualsandreas KAPSALISNo ratings yet

- Assignment 2Document18 pagesAssignment 2Manas GuptaNo ratings yet

- Multivariate Forecasting in Tableau With R - R-BloggersDocument15 pagesMultivariate Forecasting in Tableau With R - R-Bloggersmalli karjunNo ratings yet

- Beginners Tutorial For Regular Expressions in Python - Python LearningDocument23 pagesBeginners Tutorial For Regular Expressions in Python - Python LearningArun SomashekarNo ratings yet

- Thesis For FreeDocument7 pagesThesis For Freewbrgaygld100% (2)

- Everything You Need To Know About Linear Regression - by Sushant Patrikar - Towards Data ScienceDocument20 pagesEverything You Need To Know About Linear Regression - by Sushant Patrikar - Towards Data SciencephilipNo ratings yet

- Lasso Regression Using Glmnet For Binary Outcome - Cross Validated PDFDocument4 pagesLasso Regression Using Glmnet For Binary Outcome - Cross Validated PDFMartyanto TedjoNo ratings yet

- Good SomethingDocument14 pagesGood SomethingYasser NaguibNo ratings yet

- Risk-Neutral Pricing Techniques and Examples: November 2018Document25 pagesRisk-Neutral Pricing Techniques and Examples: November 2018Kapil AgrawalNo ratings yet

- Topic 3-SPSS and STATADocument73 pagesTopic 3-SPSS and STATABlessings50100% (1)

- Pes1ug22cs841 Sudeep G Lab1Document37 pagesPes1ug22cs841 Sudeep G Lab1nishkarshNo ratings yet

- Survey Paper On String MatchingDocument4 pagesSurvey Paper On String MatchingSaurabh KumarNo ratings yet

- Database Similarity Searching: Irit Orr Shifra Ben DorDocument76 pagesDatabase Similarity Searching: Irit Orr Shifra Ben DorRishabh JainNo ratings yet

- Using R For Basic Statistical AnalysisDocument11 pagesUsing R For Basic Statistical AnalysisNile SethNo ratings yet

- Literature Review On Arima ModelsDocument4 pagesLiterature Review On Arima Modelsafdtywgdu100% (1)

- Relationship Between Genetic Algorithms and Ant Colony Optimization AlgorithmsDocument11 pagesRelationship Between Genetic Algorithms and Ant Colony Optimization Algorithmspratikshah2No ratings yet

- Package Bayeslogit': R Topics DocumentedDocument15 pagesPackage Bayeslogit': R Topics Documentedsdiana66No ratings yet

- Spat Stat Quick RefDocument32 pagesSpat Stat Quick Refzarcone7No ratings yet

- PCA - Analysis in R - DataCampDocument20 pagesPCA - Analysis in R - DataCampCleaver BrightNo ratings yet

- Design Patterns ExplainedDocument1,072 pagesDesign Patterns Explainedsportsmanrahul0% (1)

- Pairwise Sequ Datab: Appos® ©mimfoimrdaifcltesDocument25 pagesPairwise Sequ Datab: Appos® ©mimfoimrdaifcltesVed ClassesNo ratings yet

- Chapter 7 Quality Improvement TechniquesDocument28 pagesChapter 7 Quality Improvement TechniquesmuhadirNo ratings yet

- Sequence Alignment and SearchingDocument54 pagesSequence Alignment and SearchingMudit MisraNo ratings yet

- Chapter 1Document42 pagesChapter 1Mandar Priya PhatakNo ratings yet

- Thesis Bat AlgorithmDocument8 pagesThesis Bat Algorithmogjbvqvcf100% (2)

- PSY3200 U2 AS PsyStatsDocument6 pagesPSY3200 U2 AS PsyStatsPETER KARANJANo ratings yet

- Manual Stata MultilevelDocument371 pagesManual Stata MultilevelJaime CazaNo ratings yet

- FIT3152 Data Analytics. Tutorial 01: Introduction To R. Review of Basic StatisticsDocument4 pagesFIT3152 Data Analytics. Tutorial 01: Introduction To R. Review of Basic Statisticshazel nuttNo ratings yet

- Prais Winsten RegressionDocument33 pagesPrais Winsten Regressionel.cadejoNo ratings yet

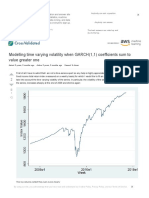

- Maximum Likelihood - Modelling Time Varying Volatility When GARCH (1,1) Coefficients Sum To Value Greater One - Cross ValidatedDocument4 pagesMaximum Likelihood - Modelling Time Varying Volatility When GARCH (1,1) Coefficients Sum To Value Greater One - Cross ValidatedJosé-Manuel Martin CoronadoNo ratings yet

- 01 - Introduction To R and RStudioDocument6 pages01 - Introduction To R and RStudiokarpoviguessNo ratings yet

- Regression Tree ThesisDocument4 pagesRegression Tree Thesiskellylindemannmadison100% (2)

- Culpepper 2010Document6 pagesCulpepper 2010Rayhan XhanNo ratings yet

- 7QC ToolsDocument36 pages7QC Toolssweety1188100% (1)

- Stata Demo 3 Econ 396A F2016Document12 pagesStata Demo 3 Econ 396A F2016morry123No ratings yet

- Factor-ChapterDocument26 pagesFactor-ChapterAstrid MarwahNo ratings yet

- Negative Binomial Regression - R Data Analysis ExamplesDocument11 pagesNegative Binomial Regression - R Data Analysis ExamplesFhano HendrianNo ratings yet

- Synthpop: An R Package For Generating Synthetic Versions of Sensitive Microdata For Statistical Disclosure ControlDocument9 pagesSynthpop: An R Package For Generating Synthetic Versions of Sensitive Microdata For Statistical Disclosure Controlmevtorres1977No ratings yet

- Introduction To The R Package PLSPM: Gaston Sanchez, Laura Trinchera, Giorgio RussolilloDocument10 pagesIntroduction To The R Package PLSPM: Gaston Sanchez, Laura Trinchera, Giorgio Russolilloomkar_puri5277No ratings yet

- Data Visualization Using RDocument26 pagesData Visualization Using Rshiva shangariNo ratings yet

- AerDocument6 pagesAerchuck89No ratings yet

- What Is Exploratory Data Analysis?: IntuitionDocument8 pagesWhat Is Exploratory Data Analysis?: IntuitionLakshmi KakarlaNo ratings yet

- Regression and Classification - Supervised Machine Learning - GeeksforGeeksDocument9 pagesRegression and Classification - Supervised Machine Learning - GeeksforGeeksbsudheertecNo ratings yet

- Difference Between Classification and RegressionDocument1 pageDifference Between Classification and RegressionSajid BhattNo ratings yet

- Statistics - SodsDocument45 pagesStatistics - SodsHiren ChauhanNo ratings yet

- Unit IiDocument14 pagesUnit IiDr. R. K. Selvakesavan PSGRKCWNo ratings yet

- SOC260 Demo 8Document4 pagesSOC260 Demo 8kiaufNo ratings yet

- Multivariate Analysis of Mixed Type Data: The Pcamixdata R PackageDocument32 pagesMultivariate Analysis of Mixed Type Data: The Pcamixdata R PackageAhmed GamalNo ratings yet

- Log-Linear Modeling: Concepts, Interpretation, and ApplicationFrom EverandLog-Linear Modeling: Concepts, Interpretation, and ApplicationNo ratings yet

- Cdi 1 Slide 30 To 55Document27 pagesCdi 1 Slide 30 To 55Cristine AvancenaNo ratings yet

- Elementary - Progress Exam-2Document9 pagesElementary - Progress Exam-2Eland ExamsNo ratings yet

- Revision CP 4Document35 pagesRevision CP 4Victor OdipoNo ratings yet

- R AssignmentDocument2 pagesR AssignmentKapardhi kkNo ratings yet

- Plot Gardening - Write Faster, W - Chris FoxDocument147 pagesPlot Gardening - Write Faster, W - Chris FoxAna AlencarNo ratings yet

- Checklist For Equipment Inspection Lifting Tools - TacklesDocument2 pagesChecklist For Equipment Inspection Lifting Tools - TacklesAsaf Ibn RasheedNo ratings yet

- Psat NMSQT Practice Test 2Document25 pagesPsat NMSQT Practice Test 2mahmudNo ratings yet

- Visonic KP-140 PG2 User' S GuideDocument4 pagesVisonic KP-140 PG2 User' S GuideHome_SecurityNo ratings yet

- Receiverbook - Online Receiver Directory - HomeDocument1 pageReceiverbook - Online Receiver Directory - Homekennymckornic5334No ratings yet

- Oumh1203 English For WritDocument14 pagesOumh1203 English For WritPuneswaran UmapathyNo ratings yet

- Analysis of Marketing Communication Tools and SalesDocument8 pagesAnalysis of Marketing Communication Tools and SalesAlexander DeckerNo ratings yet

- Editor - Juan A. Martinez-Velasco - Transient Analysis of Power Systems - A Practical Approach (2020, John Wiley & Sons) - Libgen - LiDocument610 pagesEditor - Juan A. Martinez-Velasco - Transient Analysis of Power Systems - A Practical Approach (2020, John Wiley & Sons) - Libgen - LiDDdivyaNo ratings yet

- Peavey Rockmaster PreampDocument1 pagePeavey Rockmaster PreampFrancisco FerrerNo ratings yet

- SJ Belotti Hughes Pianomortari PDFDocument40 pagesSJ Belotti Hughes Pianomortari PDFakita_1610No ratings yet

- Usman Najam Introduction of Research ScholarDocument10 pagesUsman Najam Introduction of Research ScholarUsmanNo ratings yet

- Amps Flat GainDocument3 pagesAmps Flat GainJaime Misael JalifeNo ratings yet

- Assignment 4 Solution PDFDocument19 pagesAssignment 4 Solution PDFabimalainNo ratings yet

- Car's Disc Brake Picture: Firdaus Putra KuswoyoDocument5 pagesCar's Disc Brake Picture: Firdaus Putra KuswoyoFirdaus Kuswoyo100% (1)

- Effects of Different Charcoal Concentration On The Growth and Yield of Okra PlantDocument2 pagesEffects of Different Charcoal Concentration On The Growth and Yield of Okra PlantWahahahaha suck my dickNo ratings yet

- MUCLecture 2022 51954485Document21 pagesMUCLecture 2022 51954485Mr AliNo ratings yet

- Preasure Exerted by Liquids Class Notes PDF by Sahaj AhujaDocument7 pagesPreasure Exerted by Liquids Class Notes PDF by Sahaj AhujaSahaj AhujaNo ratings yet

- MUltis EP 2Document1 pageMUltis EP 2dnoaisapsNo ratings yet

- Defence Account CodeDocument41 pagesDefence Account Codem kNo ratings yet

- Tunneling Brochure English 04Document7 pagesTunneling Brochure English 04xcvNo ratings yet

- MTCP ETN Server EDocument3 pagesMTCP ETN Server EcardonPTNo ratings yet

- 01 Identifying Challenges of Construction Industry in IndiaDocument15 pages01 Identifying Challenges of Construction Industry in IndiaPranav100% (1)

- Personality DisordersDocument35 pagesPersonality DisordersEsraRamosNo ratings yet

- DT266 SeriesDocument7 pagesDT266 SeriesCOSTELNo ratings yet

Download as pdf or txt

You might also like

- Kassambara, Alboukadel - Machine Learning Essentials - Practical Guide in R (2018)Document424 pagesKassambara, Alboukadel - Machine Learning Essentials - Practical Guide in R (2018)Mrcrismath g100% (1)

- Study PlanDocument3 pagesStudy PlanYan Kyaw100% (1)

- Principal Components Analysis and Redundancy AnalysisDocument18 pagesPrincipal Components Analysis and Redundancy AnalysisJosé António PereiraNo ratings yet

- Reading Keys Projectable New Edition The United PDFDocument7 pagesReading Keys Projectable New Edition The United PDFNisan BaharNo ratings yet

- Vis Corel Matrix Using CoringDocument17 pagesVis Corel Matrix Using CoringsambalasakthiNo ratings yet

- Boruta Feature Selection in R - DataCampDocument18 pagesBoruta Feature Selection in R - DataCamphabeeb4saNo ratings yet

- R PCA (Principal Component Analysis) - DataCampDocument54 pagesR PCA (Principal Component Analysis) - DataCampUMESH D RNo ratings yet

- RBasics HandoutDocument6 pagesRBasics HandoutHassan AlsafiNo ratings yet

- R Handbook - Regression For Count DataDocument13 pagesR Handbook - Regression For Count Dataclyn.beeNo ratings yet

- Likert-Plots and Grouped Likert-Plots #Rstats - R-BloggersDocument7 pagesLikert-Plots and Grouped Likert-Plots #Rstats - R-BloggersLeonardo Talavera CamposNo ratings yet

- The Art of Data Visualization - Learn 7 Visualizations in RDocument15 pagesThe Art of Data Visualization - Learn 7 Visualizations in RHéctor W Moreno QNo ratings yet

- Package Gesca': R Topics DocumentedDocument15 pagesPackage Gesca': R Topics DocumentedfarisNo ratings yet

- Template For GigaByte Journal Update SubmissionsDocument8 pagesTemplate For GigaByte Journal Update SubmissionsniyawnaniyawNo ratings yet

- LRresidualsDocument9 pagesLRresidualsandreas KAPSALISNo ratings yet

- Assignment 2Document18 pagesAssignment 2Manas GuptaNo ratings yet

- Multivariate Forecasting in Tableau With R - R-BloggersDocument15 pagesMultivariate Forecasting in Tableau With R - R-Bloggersmalli karjunNo ratings yet

- Beginners Tutorial For Regular Expressions in Python - Python LearningDocument23 pagesBeginners Tutorial For Regular Expressions in Python - Python LearningArun SomashekarNo ratings yet

- Thesis For FreeDocument7 pagesThesis For Freewbrgaygld100% (2)

- Everything You Need To Know About Linear Regression - by Sushant Patrikar - Towards Data ScienceDocument20 pagesEverything You Need To Know About Linear Regression - by Sushant Patrikar - Towards Data SciencephilipNo ratings yet

- Lasso Regression Using Glmnet For Binary Outcome - Cross Validated PDFDocument4 pagesLasso Regression Using Glmnet For Binary Outcome - Cross Validated PDFMartyanto TedjoNo ratings yet

- Good SomethingDocument14 pagesGood SomethingYasser NaguibNo ratings yet

- Risk-Neutral Pricing Techniques and Examples: November 2018Document25 pagesRisk-Neutral Pricing Techniques and Examples: November 2018Kapil AgrawalNo ratings yet

- Topic 3-SPSS and STATADocument73 pagesTopic 3-SPSS and STATABlessings50100% (1)

- Pes1ug22cs841 Sudeep G Lab1Document37 pagesPes1ug22cs841 Sudeep G Lab1nishkarshNo ratings yet

- Survey Paper On String MatchingDocument4 pagesSurvey Paper On String MatchingSaurabh KumarNo ratings yet

- Database Similarity Searching: Irit Orr Shifra Ben DorDocument76 pagesDatabase Similarity Searching: Irit Orr Shifra Ben DorRishabh JainNo ratings yet

- Using R For Basic Statistical AnalysisDocument11 pagesUsing R For Basic Statistical AnalysisNile SethNo ratings yet

- Literature Review On Arima ModelsDocument4 pagesLiterature Review On Arima Modelsafdtywgdu100% (1)

- Relationship Between Genetic Algorithms and Ant Colony Optimization AlgorithmsDocument11 pagesRelationship Between Genetic Algorithms and Ant Colony Optimization Algorithmspratikshah2No ratings yet

- Package Bayeslogit': R Topics DocumentedDocument15 pagesPackage Bayeslogit': R Topics Documentedsdiana66No ratings yet

- Spat Stat Quick RefDocument32 pagesSpat Stat Quick Refzarcone7No ratings yet

- PCA - Analysis in R - DataCampDocument20 pagesPCA - Analysis in R - DataCampCleaver BrightNo ratings yet

- Design Patterns ExplainedDocument1,072 pagesDesign Patterns Explainedsportsmanrahul0% (1)

- Pairwise Sequ Datab: Appos® ©mimfoimrdaifcltesDocument25 pagesPairwise Sequ Datab: Appos® ©mimfoimrdaifcltesVed ClassesNo ratings yet

- Chapter 7 Quality Improvement TechniquesDocument28 pagesChapter 7 Quality Improvement TechniquesmuhadirNo ratings yet

- Sequence Alignment and SearchingDocument54 pagesSequence Alignment and SearchingMudit MisraNo ratings yet

- Chapter 1Document42 pagesChapter 1Mandar Priya PhatakNo ratings yet

- Thesis Bat AlgorithmDocument8 pagesThesis Bat Algorithmogjbvqvcf100% (2)

- PSY3200 U2 AS PsyStatsDocument6 pagesPSY3200 U2 AS PsyStatsPETER KARANJANo ratings yet

- Manual Stata MultilevelDocument371 pagesManual Stata MultilevelJaime CazaNo ratings yet

- FIT3152 Data Analytics. Tutorial 01: Introduction To R. Review of Basic StatisticsDocument4 pagesFIT3152 Data Analytics. Tutorial 01: Introduction To R. Review of Basic Statisticshazel nuttNo ratings yet

- Prais Winsten RegressionDocument33 pagesPrais Winsten Regressionel.cadejoNo ratings yet

- Maximum Likelihood - Modelling Time Varying Volatility When GARCH (1,1) Coefficients Sum To Value Greater One - Cross ValidatedDocument4 pagesMaximum Likelihood - Modelling Time Varying Volatility When GARCH (1,1) Coefficients Sum To Value Greater One - Cross ValidatedJosé-Manuel Martin CoronadoNo ratings yet

- 01 - Introduction To R and RStudioDocument6 pages01 - Introduction To R and RStudiokarpoviguessNo ratings yet

- Regression Tree ThesisDocument4 pagesRegression Tree Thesiskellylindemannmadison100% (2)

- Culpepper 2010Document6 pagesCulpepper 2010Rayhan XhanNo ratings yet

- 7QC ToolsDocument36 pages7QC Toolssweety1188100% (1)

- Stata Demo 3 Econ 396A F2016Document12 pagesStata Demo 3 Econ 396A F2016morry123No ratings yet

- Factor-ChapterDocument26 pagesFactor-ChapterAstrid MarwahNo ratings yet

- Negative Binomial Regression - R Data Analysis ExamplesDocument11 pagesNegative Binomial Regression - R Data Analysis ExamplesFhano HendrianNo ratings yet

- Synthpop: An R Package For Generating Synthetic Versions of Sensitive Microdata For Statistical Disclosure ControlDocument9 pagesSynthpop: An R Package For Generating Synthetic Versions of Sensitive Microdata For Statistical Disclosure Controlmevtorres1977No ratings yet

- Introduction To The R Package PLSPM: Gaston Sanchez, Laura Trinchera, Giorgio RussolilloDocument10 pagesIntroduction To The R Package PLSPM: Gaston Sanchez, Laura Trinchera, Giorgio Russolilloomkar_puri5277No ratings yet

- Data Visualization Using RDocument26 pagesData Visualization Using Rshiva shangariNo ratings yet

- AerDocument6 pagesAerchuck89No ratings yet

- What Is Exploratory Data Analysis?: IntuitionDocument8 pagesWhat Is Exploratory Data Analysis?: IntuitionLakshmi KakarlaNo ratings yet

- Regression and Classification - Supervised Machine Learning - GeeksforGeeksDocument9 pagesRegression and Classification - Supervised Machine Learning - GeeksforGeeksbsudheertecNo ratings yet

- Difference Between Classification and RegressionDocument1 pageDifference Between Classification and RegressionSajid BhattNo ratings yet

- Statistics - SodsDocument45 pagesStatistics - SodsHiren ChauhanNo ratings yet

- Unit IiDocument14 pagesUnit IiDr. R. K. Selvakesavan PSGRKCWNo ratings yet

- SOC260 Demo 8Document4 pagesSOC260 Demo 8kiaufNo ratings yet

- Multivariate Analysis of Mixed Type Data: The Pcamixdata R PackageDocument32 pagesMultivariate Analysis of Mixed Type Data: The Pcamixdata R PackageAhmed GamalNo ratings yet

- Log-Linear Modeling: Concepts, Interpretation, and ApplicationFrom EverandLog-Linear Modeling: Concepts, Interpretation, and ApplicationNo ratings yet

- Cdi 1 Slide 30 To 55Document27 pagesCdi 1 Slide 30 To 55Cristine AvancenaNo ratings yet

- Elementary - Progress Exam-2Document9 pagesElementary - Progress Exam-2Eland ExamsNo ratings yet

- Revision CP 4Document35 pagesRevision CP 4Victor OdipoNo ratings yet

- R AssignmentDocument2 pagesR AssignmentKapardhi kkNo ratings yet

- Plot Gardening - Write Faster, W - Chris FoxDocument147 pagesPlot Gardening - Write Faster, W - Chris FoxAna AlencarNo ratings yet

- Checklist For Equipment Inspection Lifting Tools - TacklesDocument2 pagesChecklist For Equipment Inspection Lifting Tools - TacklesAsaf Ibn RasheedNo ratings yet

- Psat NMSQT Practice Test 2Document25 pagesPsat NMSQT Practice Test 2mahmudNo ratings yet

- Visonic KP-140 PG2 User' S GuideDocument4 pagesVisonic KP-140 PG2 User' S GuideHome_SecurityNo ratings yet

- Receiverbook - Online Receiver Directory - HomeDocument1 pageReceiverbook - Online Receiver Directory - Homekennymckornic5334No ratings yet

- Oumh1203 English For WritDocument14 pagesOumh1203 English For WritPuneswaran UmapathyNo ratings yet

- Analysis of Marketing Communication Tools and SalesDocument8 pagesAnalysis of Marketing Communication Tools and SalesAlexander DeckerNo ratings yet

- Editor - Juan A. Martinez-Velasco - Transient Analysis of Power Systems - A Practical Approach (2020, John Wiley & Sons) - Libgen - LiDocument610 pagesEditor - Juan A. Martinez-Velasco - Transient Analysis of Power Systems - A Practical Approach (2020, John Wiley & Sons) - Libgen - LiDDdivyaNo ratings yet

- Peavey Rockmaster PreampDocument1 pagePeavey Rockmaster PreampFrancisco FerrerNo ratings yet

- SJ Belotti Hughes Pianomortari PDFDocument40 pagesSJ Belotti Hughes Pianomortari PDFakita_1610No ratings yet

- Usman Najam Introduction of Research ScholarDocument10 pagesUsman Najam Introduction of Research ScholarUsmanNo ratings yet

- Amps Flat GainDocument3 pagesAmps Flat GainJaime Misael JalifeNo ratings yet

- Assignment 4 Solution PDFDocument19 pagesAssignment 4 Solution PDFabimalainNo ratings yet

- Car's Disc Brake Picture: Firdaus Putra KuswoyoDocument5 pagesCar's Disc Brake Picture: Firdaus Putra KuswoyoFirdaus Kuswoyo100% (1)

- Effects of Different Charcoal Concentration On The Growth and Yield of Okra PlantDocument2 pagesEffects of Different Charcoal Concentration On The Growth and Yield of Okra PlantWahahahaha suck my dickNo ratings yet

- MUCLecture 2022 51954485Document21 pagesMUCLecture 2022 51954485Mr AliNo ratings yet

- Preasure Exerted by Liquids Class Notes PDF by Sahaj AhujaDocument7 pagesPreasure Exerted by Liquids Class Notes PDF by Sahaj AhujaSahaj AhujaNo ratings yet

- MUltis EP 2Document1 pageMUltis EP 2dnoaisapsNo ratings yet

- Defence Account CodeDocument41 pagesDefence Account Codem kNo ratings yet

- Tunneling Brochure English 04Document7 pagesTunneling Brochure English 04xcvNo ratings yet

- MTCP ETN Server EDocument3 pagesMTCP ETN Server EcardonPTNo ratings yet

- 01 Identifying Challenges of Construction Industry in IndiaDocument15 pages01 Identifying Challenges of Construction Industry in IndiaPranav100% (1)

- Personality DisordersDocument35 pagesPersonality DisordersEsraRamosNo ratings yet

- DT266 SeriesDocument7 pagesDT266 SeriesCOSTELNo ratings yet