Services Rendered by Banks.: Advancing of Loans

Services Rendered by Banks.: Advancing of Loans

You might also like

- Business Development Audit ChecklistDocument2 pagesBusiness Development Audit Checklistandruta197867% (3)

- Banking FacilitiesDocument3 pagesBanking FacilitiesOsama AhmedNo ratings yet

- Banking ServicesDocument5 pagesBanking Servicesbeena antuNo ratings yet

- Unit-2: Banking and Insurance Services: Collection of Cheques, Bills and DraftsDocument45 pagesUnit-2: Banking and Insurance Services: Collection of Cheques, Bills and DraftsRaghu BMNo ratings yet

- Advancing of Loans: Difference Between Bank Overdraft and Cash CreditDocument7 pagesAdvancing of Loans: Difference Between Bank Overdraft and Cash CreditpraharshithaNo ratings yet

- Business Services Class 11 Notes Business Studies - 7114551Document8 pagesBusiness Services Class 11 Notes Business Studies - 7114551TanishqNo ratings yet

- Chapter 4 - Business ServicesDocument12 pagesChapter 4 - Business Servicestayalaryaman751No ratings yet

- CH 4Document10 pagesCH 4RaashiNo ratings yet

- Functions of Commercial BanksDocument19 pagesFunctions of Commercial BanksAravind Kumar G100% (1)

- E BankingDocument65 pagesE Bankingzeeshan shaikh100% (1)

- Financial Services SectorDocument12 pagesFinancial Services SectorDominic RomeroNo ratings yet

- CBO Module 1 Retail Banking Deposit ProductsDocument17 pagesCBO Module 1 Retail Banking Deposit ProductsRajabNo ratings yet

- Commercial BankDocument2 pagesCommercial BankFardin Ahmed MugdhoNo ratings yet

- Banking Awareness, FBNDocument10 pagesBanking Awareness, FBNtoniahokekeNo ratings yet

- General Utility Services of Commercial Banks: Transactions. They Are Called Authorized Dealers. The BankDocument10 pagesGeneral Utility Services of Commercial Banks: Transactions. They Are Called Authorized Dealers. The BankSharan YadavNo ratings yet

- Nature of Business Serv1cesDocument11 pagesNature of Business Serv1cesmadhavanramuduNo ratings yet

- CH 4 Business ServicesDocument13 pagesCH 4 Business ServicesBaklol Babu JiNo ratings yet

- 11 Business Studies Notes Ch04 Business Services 02Document12 pages11 Business Studies Notes Ch04 Business Services 02Subodh SaxenaNo ratings yet

- Unit 4 Business Studies NotesDocument8 pagesUnit 4 Business Studies NotesDhakshithaNo ratings yet

- Bank ServicesDocument2 pagesBank ServicesKürti AnettaNo ratings yet

- Chapter 13 BankingDocument5 pagesChapter 13 BankingdragongskdbsNo ratings yet

- Banking Terms 2021Document48 pagesBanking Terms 2021Sammar AbbasNo ratings yet

- Important Functions of Bank: What Is A Bank?Document3 pagesImportant Functions of Bank: What Is A Bank?Samiksha PawarNo ratings yet

- Role of Commercial Bank-1Document9 pagesRole of Commercial Bank-1TanzeemNo ratings yet

- Unit 2 - Sbaa7001 Banking Products and ServicesDocument38 pagesUnit 2 - Sbaa7001 Banking Products and ServicesGracyNo ratings yet

- 2-Notes On Banking Products & Services-Part 1Document16 pages2-Notes On Banking Products & Services-Part 1Kirti GiyamalaniNo ratings yet

- I) Primary Functions:: A) Accepting DepositsDocument4 pagesI) Primary Functions:: A) Accepting DepositsJoshna SinghNo ratings yet

- Chapter 24 The Role and Function of Financial InstitutionsDocument3 pagesChapter 24 The Role and Function of Financial InstitutionsVỹ San KohNo ratings yet

- Research Paper On Banker As An Agent: Critical Study: Banking and Insurance LawDocument16 pagesResearch Paper On Banker As An Agent: Critical Study: Banking and Insurance LawGyanendra kumarNo ratings yet

- Banking Chapter OneDocument17 pagesBanking Chapter OnefikremariamNo ratings yet

- Lession 3 OperationsDocument13 pagesLession 3 Operationssusma susmaNo ratings yet

- (A.) Commercial Banks - FunctionsDocument3 pages(A.) Commercial Banks - FunctionsEPP-2004 HaneefaNo ratings yet

- Banking NotesDocument84 pagesBanking NotesNitesh MahatoNo ratings yet

- BRO - 4th BBADocument41 pagesBRO - 4th BBANithyananda PatelNo ratings yet

- LPB Unit-1 Introduction To BankingDocument13 pagesLPB Unit-1 Introduction To BankingVeena ReddyNo ratings yet

- Functions of BanksDocument3 pagesFunctions of BanksEbne FahadNo ratings yet

- April 23 2021 12B, C, D, E, F, GChapter14BANKS NotesDocument16 pagesApril 23 2021 12B, C, D, E, F, GChapter14BANKS NotesStephine BochuNo ratings yet

- Chap 1. Banking System in IndiaDocument24 pagesChap 1. Banking System in IndiaShankha MaitiNo ratings yet

- Commercial BankingDocument4 pagesCommercial Bankingsn nNo ratings yet

- Functions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsDocument3 pagesFunctions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsBalaji GajendranNo ratings yet

- Com BankDocument25 pagesCom BankAnonymous y3E7iaNo ratings yet

- Chapter Three Commercial Banking: 1 by SityDocument10 pagesChapter Three Commercial Banking: 1 by SitySeid KassawNo ratings yet

- Products and Services Offer by BankDocument11 pagesProducts and Services Offer by BankRohit JaiswalNo ratings yet

- Functions of Commercial BanksDocument2 pagesFunctions of Commercial BanksAbdul Rasheed ShaikhNo ratings yet

- Instruments of Exchange and PaymentDocument3 pagesInstruments of Exchange and PaymentAnnika liburdNo ratings yet

- Banking Products and ServicesDocument5 pagesBanking Products and ServicesAikya GandhiNo ratings yet

- Banking U5Document4 pagesBanking U5alemayehuNo ratings yet

- Indian BankDocument94 pagesIndian BankManzuhonnur100% (2)

- Financial Analysis at Indian BankDocument93 pagesFinancial Analysis at Indian BankAbhay JainNo ratings yet

- Management of Commercial BankDocument7 pagesManagement of Commercial BankSamridhi RakhejaNo ratings yet

- Functions of Commercial BanksDocument52 pagesFunctions of Commercial BanksPulkit_Saini_789No ratings yet

- XI BS Ch04 Creative PPT With ObjectivesDocument158 pagesXI BS Ch04 Creative PPT With ObjectivesHiya MakhijaNo ratings yet

- Banking Functions: Navjeet Parvez Rakesh Majid NavjotDocument13 pagesBanking Functions: Navjeet Parvez Rakesh Majid Navjotharesh KNo ratings yet

- Amrit Summer Report 000Document68 pagesAmrit Summer Report 000RPSinghNo ratings yet

- Commercial BankingDocument12 pagesCommercial BankingwubeNo ratings yet

- Document (2) 1Document28 pagesDocument (2) 1Bi bi fathima Bi bi fathimaNo ratings yet

- Ethiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry BanksDocument9 pagesEthiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry Banksመስቀል ኃይላችን ነውNo ratings yet

- CH 4 Business ServicesDocument11 pagesCH 4 Business Serviceskeshav sarafNo ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- KULGEETDocument5 pagesKULGEETKulgeet TanyaNo ratings yet

- Mr. A Mr. B: CourtDocument2 pagesMr. A Mr. B: CourtKulgeet TanyaNo ratings yet

- NullDocument9 pagesNullKulgeet TanyaNo ratings yet

- Fund Structure & Legal EnvironmentDocument32 pagesFund Structure & Legal EnvironmentKulgeet TanyaNo ratings yet

- MandateDocument2 pagesMandateKulgeet TanyaNo ratings yet

- Off-Balance Sheet BusinessDocument3 pagesOff-Balance Sheet BusinessKulgeet TanyaNo ratings yet

- Bike Premsons Honda: Banker's LienDocument2 pagesBike Premsons Honda: Banker's LienKulgeet TanyaNo ratings yet

- Different Types of Deposit Products: 1. Savings Bank AccountDocument6 pagesDifferent Types of Deposit Products: 1. Savings Bank AccountKulgeet TanyaNo ratings yet

- Methods of Food PurchasingDocument10 pagesMethods of Food Purchasingrizzwan khan100% (1)

- Data Analyst - AssignmentDocument3 pagesData Analyst - AssignmentChandrakant Babar50% (2)

- Sales Contract No. 001/SC-SHP/09/2021Document2 pagesSales Contract No. 001/SC-SHP/09/2021QrenNo ratings yet

- Kuliah Ke-5 #Cost of CapitalDocument45 pagesKuliah Ke-5 #Cost of CapitalHASNA PUTRINo ratings yet

- What Is Test Scenario - Template With ExamplesDocument3 pagesWhat Is Test Scenario - Template With ExamplesFlorin ConduratNo ratings yet

- Marketing - 5-Segmenntation, Targeting and PositioningDocument46 pagesMarketing - 5-Segmenntation, Targeting and PositioningYogendra ShuklaNo ratings yet

- 3 Org Structures To Consider For Experience Led TransformationDocument15 pages3 Org Structures To Consider For Experience Led TransformationYangjin KwonNo ratings yet

- Concept of Salary Under Income Tax ActDocument29 pagesConcept of Salary Under Income Tax ActMaaz Alam100% (2)

- Cement Industry WCMDocument18 pagesCement Industry WCMAzwad ChowdhuryNo ratings yet

- RW2011-15 Toc 183749110917062932Document6 pagesRW2011-15 Toc 183749110917062932Dwi AgungNo ratings yet

- ZoOm Pitch DeckDocument5 pagesZoOm Pitch DeckHakimuddin TinwalaNo ratings yet

- Account Statement: PrakashDocument1 pageAccount Statement: PrakashRny buriaNo ratings yet

- Property and Equity 2Document101 pagesProperty and Equity 2Bc Violá100% (1)

- PDF TDocument2 pagesPDF TahmdkamyabrjmNo ratings yet

- 31jan2019 - PDs CompiledDocument108 pages31jan2019 - PDs CompiledharigroupphilippinesNo ratings yet

- Cad Cam TheoryDocument12 pagesCad Cam TheoryShashank VermaNo ratings yet

- Financing A Car Loan WorksheetDocument3 pagesFinancing A Car Loan WorksheetDestiney GriffinNo ratings yet

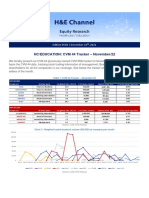

- HC/EDUCATION: CVM 44 Tracker - November/22: Edition #548 - December 16, 2022Document4 pagesHC/EDUCATION: CVM 44 Tracker - November/22: Edition #548 - December 16, 2022CAIO HENRIQUE FIORDELIZNo ratings yet

- Economics Slide C5Document41 pagesEconomics Slide C5Tamara Jacobs100% (1)

- Econ CE GDP MCDocument19 pagesEcon CE GDP MCs sNo ratings yet

- Arnolds v. WillitsDocument1 pageArnolds v. WillitsStephanie Erica Louise RicamonteNo ratings yet

- MBA Case Let It Be MeDocument1 pageMBA Case Let It Be MeMichelle AlvarezNo ratings yet

- Kalbe Farma TBK - Billingual - 30 - Sept - 2023 - ReleasedDocument145 pagesKalbe Farma TBK - Billingual - 30 - Sept - 2023 - ReleasedTimothy GracianovNo ratings yet

- Life Cycle Costing Q&ADocument2 pagesLife Cycle Costing Q&AanjNo ratings yet

- Egyptian International Pharmaceutical Industries Company (EIPICO)Document1 pageEgyptian International Pharmaceutical Industries Company (EIPICO)yasser massryNo ratings yet

- Class Exercises - Accounting Errors - AnswersDocument4 pagesClass Exercises - Accounting Errors - Answerseshakaur100% (2)

- Analysis of Marketing of PerfumeDocument10 pagesAnalysis of Marketing of Perfume337 Nandawat KanishkaNo ratings yet

- HMSI Company Profile 2019 - HinoDocument25 pagesHMSI Company Profile 2019 - HinoahmadmubarokharbarindoNo ratings yet

- Assignment1 - Group 8Document8 pagesAssignment1 - Group 8digamber patilNo ratings yet

Download as pdf or txt

You might also like

- Business Development Audit ChecklistDocument2 pagesBusiness Development Audit Checklistandruta197867% (3)

- Banking FacilitiesDocument3 pagesBanking FacilitiesOsama AhmedNo ratings yet

- Banking ServicesDocument5 pagesBanking Servicesbeena antuNo ratings yet

- Unit-2: Banking and Insurance Services: Collection of Cheques, Bills and DraftsDocument45 pagesUnit-2: Banking and Insurance Services: Collection of Cheques, Bills and DraftsRaghu BMNo ratings yet

- Advancing of Loans: Difference Between Bank Overdraft and Cash CreditDocument7 pagesAdvancing of Loans: Difference Between Bank Overdraft and Cash CreditpraharshithaNo ratings yet

- Business Services Class 11 Notes Business Studies - 7114551Document8 pagesBusiness Services Class 11 Notes Business Studies - 7114551TanishqNo ratings yet

- Chapter 4 - Business ServicesDocument12 pagesChapter 4 - Business Servicestayalaryaman751No ratings yet

- CH 4Document10 pagesCH 4RaashiNo ratings yet

- Functions of Commercial BanksDocument19 pagesFunctions of Commercial BanksAravind Kumar G100% (1)

- E BankingDocument65 pagesE Bankingzeeshan shaikh100% (1)

- Financial Services SectorDocument12 pagesFinancial Services SectorDominic RomeroNo ratings yet

- CBO Module 1 Retail Banking Deposit ProductsDocument17 pagesCBO Module 1 Retail Banking Deposit ProductsRajabNo ratings yet

- Commercial BankDocument2 pagesCommercial BankFardin Ahmed MugdhoNo ratings yet

- Banking Awareness, FBNDocument10 pagesBanking Awareness, FBNtoniahokekeNo ratings yet

- General Utility Services of Commercial Banks: Transactions. They Are Called Authorized Dealers. The BankDocument10 pagesGeneral Utility Services of Commercial Banks: Transactions. They Are Called Authorized Dealers. The BankSharan YadavNo ratings yet

- Nature of Business Serv1cesDocument11 pagesNature of Business Serv1cesmadhavanramuduNo ratings yet

- CH 4 Business ServicesDocument13 pagesCH 4 Business ServicesBaklol Babu JiNo ratings yet

- 11 Business Studies Notes Ch04 Business Services 02Document12 pages11 Business Studies Notes Ch04 Business Services 02Subodh SaxenaNo ratings yet

- Unit 4 Business Studies NotesDocument8 pagesUnit 4 Business Studies NotesDhakshithaNo ratings yet

- Bank ServicesDocument2 pagesBank ServicesKürti AnettaNo ratings yet

- Chapter 13 BankingDocument5 pagesChapter 13 BankingdragongskdbsNo ratings yet

- Banking Terms 2021Document48 pagesBanking Terms 2021Sammar AbbasNo ratings yet

- Important Functions of Bank: What Is A Bank?Document3 pagesImportant Functions of Bank: What Is A Bank?Samiksha PawarNo ratings yet

- Role of Commercial Bank-1Document9 pagesRole of Commercial Bank-1TanzeemNo ratings yet

- Unit 2 - Sbaa7001 Banking Products and ServicesDocument38 pagesUnit 2 - Sbaa7001 Banking Products and ServicesGracyNo ratings yet

- 2-Notes On Banking Products & Services-Part 1Document16 pages2-Notes On Banking Products & Services-Part 1Kirti GiyamalaniNo ratings yet

- I) Primary Functions:: A) Accepting DepositsDocument4 pagesI) Primary Functions:: A) Accepting DepositsJoshna SinghNo ratings yet

- Chapter 24 The Role and Function of Financial InstitutionsDocument3 pagesChapter 24 The Role and Function of Financial InstitutionsVỹ San KohNo ratings yet

- Research Paper On Banker As An Agent: Critical Study: Banking and Insurance LawDocument16 pagesResearch Paper On Banker As An Agent: Critical Study: Banking and Insurance LawGyanendra kumarNo ratings yet

- Banking Chapter OneDocument17 pagesBanking Chapter OnefikremariamNo ratings yet

- Lession 3 OperationsDocument13 pagesLession 3 Operationssusma susmaNo ratings yet

- (A.) Commercial Banks - FunctionsDocument3 pages(A.) Commercial Banks - FunctionsEPP-2004 HaneefaNo ratings yet

- Banking NotesDocument84 pagesBanking NotesNitesh MahatoNo ratings yet

- BRO - 4th BBADocument41 pagesBRO - 4th BBANithyananda PatelNo ratings yet

- LPB Unit-1 Introduction To BankingDocument13 pagesLPB Unit-1 Introduction To BankingVeena ReddyNo ratings yet

- Functions of BanksDocument3 pagesFunctions of BanksEbne FahadNo ratings yet

- April 23 2021 12B, C, D, E, F, GChapter14BANKS NotesDocument16 pagesApril 23 2021 12B, C, D, E, F, GChapter14BANKS NotesStephine BochuNo ratings yet

- Chap 1. Banking System in IndiaDocument24 pagesChap 1. Banking System in IndiaShankha MaitiNo ratings yet

- Commercial BankingDocument4 pagesCommercial Bankingsn nNo ratings yet

- Functions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsDocument3 pagesFunctions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsBalaji GajendranNo ratings yet

- Com BankDocument25 pagesCom BankAnonymous y3E7iaNo ratings yet

- Chapter Three Commercial Banking: 1 by SityDocument10 pagesChapter Three Commercial Banking: 1 by SitySeid KassawNo ratings yet

- Products and Services Offer by BankDocument11 pagesProducts and Services Offer by BankRohit JaiswalNo ratings yet

- Functions of Commercial BanksDocument2 pagesFunctions of Commercial BanksAbdul Rasheed ShaikhNo ratings yet

- Instruments of Exchange and PaymentDocument3 pagesInstruments of Exchange and PaymentAnnika liburdNo ratings yet

- Banking Products and ServicesDocument5 pagesBanking Products and ServicesAikya GandhiNo ratings yet

- Banking U5Document4 pagesBanking U5alemayehuNo ratings yet

- Indian BankDocument94 pagesIndian BankManzuhonnur100% (2)

- Financial Analysis at Indian BankDocument93 pagesFinancial Analysis at Indian BankAbhay JainNo ratings yet

- Management of Commercial BankDocument7 pagesManagement of Commercial BankSamridhi RakhejaNo ratings yet

- Functions of Commercial BanksDocument52 pagesFunctions of Commercial BanksPulkit_Saini_789No ratings yet

- XI BS Ch04 Creative PPT With ObjectivesDocument158 pagesXI BS Ch04 Creative PPT With ObjectivesHiya MakhijaNo ratings yet

- Banking Functions: Navjeet Parvez Rakesh Majid NavjotDocument13 pagesBanking Functions: Navjeet Parvez Rakesh Majid Navjotharesh KNo ratings yet

- Amrit Summer Report 000Document68 pagesAmrit Summer Report 000RPSinghNo ratings yet

- Commercial BankingDocument12 pagesCommercial BankingwubeNo ratings yet

- Document (2) 1Document28 pagesDocument (2) 1Bi bi fathima Bi bi fathimaNo ratings yet

- Ethiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry BanksDocument9 pagesEthiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry Banksመስቀል ኃይላችን ነውNo ratings yet

- CH 4 Business ServicesDocument11 pagesCH 4 Business Serviceskeshav sarafNo ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- KULGEETDocument5 pagesKULGEETKulgeet TanyaNo ratings yet

- Mr. A Mr. B: CourtDocument2 pagesMr. A Mr. B: CourtKulgeet TanyaNo ratings yet

- NullDocument9 pagesNullKulgeet TanyaNo ratings yet

- Fund Structure & Legal EnvironmentDocument32 pagesFund Structure & Legal EnvironmentKulgeet TanyaNo ratings yet

- MandateDocument2 pagesMandateKulgeet TanyaNo ratings yet

- Off-Balance Sheet BusinessDocument3 pagesOff-Balance Sheet BusinessKulgeet TanyaNo ratings yet

- Bike Premsons Honda: Banker's LienDocument2 pagesBike Premsons Honda: Banker's LienKulgeet TanyaNo ratings yet

- Different Types of Deposit Products: 1. Savings Bank AccountDocument6 pagesDifferent Types of Deposit Products: 1. Savings Bank AccountKulgeet TanyaNo ratings yet

- Methods of Food PurchasingDocument10 pagesMethods of Food Purchasingrizzwan khan100% (1)

- Data Analyst - AssignmentDocument3 pagesData Analyst - AssignmentChandrakant Babar50% (2)

- Sales Contract No. 001/SC-SHP/09/2021Document2 pagesSales Contract No. 001/SC-SHP/09/2021QrenNo ratings yet

- Kuliah Ke-5 #Cost of CapitalDocument45 pagesKuliah Ke-5 #Cost of CapitalHASNA PUTRINo ratings yet

- What Is Test Scenario - Template With ExamplesDocument3 pagesWhat Is Test Scenario - Template With ExamplesFlorin ConduratNo ratings yet

- Marketing - 5-Segmenntation, Targeting and PositioningDocument46 pagesMarketing - 5-Segmenntation, Targeting and PositioningYogendra ShuklaNo ratings yet

- 3 Org Structures To Consider For Experience Led TransformationDocument15 pages3 Org Structures To Consider For Experience Led TransformationYangjin KwonNo ratings yet

- Concept of Salary Under Income Tax ActDocument29 pagesConcept of Salary Under Income Tax ActMaaz Alam100% (2)

- Cement Industry WCMDocument18 pagesCement Industry WCMAzwad ChowdhuryNo ratings yet

- RW2011-15 Toc 183749110917062932Document6 pagesRW2011-15 Toc 183749110917062932Dwi AgungNo ratings yet

- ZoOm Pitch DeckDocument5 pagesZoOm Pitch DeckHakimuddin TinwalaNo ratings yet

- Account Statement: PrakashDocument1 pageAccount Statement: PrakashRny buriaNo ratings yet

- Property and Equity 2Document101 pagesProperty and Equity 2Bc Violá100% (1)

- PDF TDocument2 pagesPDF TahmdkamyabrjmNo ratings yet

- 31jan2019 - PDs CompiledDocument108 pages31jan2019 - PDs CompiledharigroupphilippinesNo ratings yet

- Cad Cam TheoryDocument12 pagesCad Cam TheoryShashank VermaNo ratings yet

- Financing A Car Loan WorksheetDocument3 pagesFinancing A Car Loan WorksheetDestiney GriffinNo ratings yet

- HC/EDUCATION: CVM 44 Tracker - November/22: Edition #548 - December 16, 2022Document4 pagesHC/EDUCATION: CVM 44 Tracker - November/22: Edition #548 - December 16, 2022CAIO HENRIQUE FIORDELIZNo ratings yet

- Economics Slide C5Document41 pagesEconomics Slide C5Tamara Jacobs100% (1)

- Econ CE GDP MCDocument19 pagesEcon CE GDP MCs sNo ratings yet

- Arnolds v. WillitsDocument1 pageArnolds v. WillitsStephanie Erica Louise RicamonteNo ratings yet

- MBA Case Let It Be MeDocument1 pageMBA Case Let It Be MeMichelle AlvarezNo ratings yet

- Kalbe Farma TBK - Billingual - 30 - Sept - 2023 - ReleasedDocument145 pagesKalbe Farma TBK - Billingual - 30 - Sept - 2023 - ReleasedTimothy GracianovNo ratings yet

- Life Cycle Costing Q&ADocument2 pagesLife Cycle Costing Q&AanjNo ratings yet

- Egyptian International Pharmaceutical Industries Company (EIPICO)Document1 pageEgyptian International Pharmaceutical Industries Company (EIPICO)yasser massryNo ratings yet

- Class Exercises - Accounting Errors - AnswersDocument4 pagesClass Exercises - Accounting Errors - Answerseshakaur100% (2)

- Analysis of Marketing of PerfumeDocument10 pagesAnalysis of Marketing of Perfume337 Nandawat KanishkaNo ratings yet

- HMSI Company Profile 2019 - HinoDocument25 pagesHMSI Company Profile 2019 - HinoahmadmubarokharbarindoNo ratings yet

- Assignment1 - Group 8Document8 pagesAssignment1 - Group 8digamber patilNo ratings yet