Download as docx, pdf, or txt

You might also like

- AKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaDocument8 pagesAKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaNur Ayu Mariya67% (3)

- Building Wealth Chart #1Document4 pagesBuilding Wealth Chart #1Caleb ReynoldsNo ratings yet

- Bantay KorapsyonDocument18 pagesBantay KorapsyonRheinhart PahilaNo ratings yet

- 00 - HUAWEI - Training IntroductionDocument27 pages00 - HUAWEI - Training IntroductionSav SashaNo ratings yet

- Chapter 4 Partnership Dissolution Without Liquidation ANSWERS To EXERCISE 4-1 To 4-11 PDFDocument19 pagesChapter 4 Partnership Dissolution Without Liquidation ANSWERS To EXERCISE 4-1 To 4-11 PDFJose GuerreroNo ratings yet

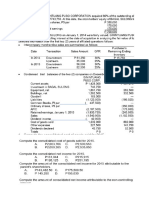

- Investments in Equity Securities Problems (Victoria Corporation) Year 1Document12 pagesInvestments in Equity Securities Problems (Victoria Corporation) Year 1Xyza Faye Regalado100% (2)

- ACCT4110 Advanced Accounting PRACTICE Exam 2 KEY v2Document14 pagesACCT4110 Advanced Accounting PRACTICE Exam 2 KEY v2accounts 3 lifeNo ratings yet

- Ansay, Allyson Charissa T - Activity 4Document14 pagesAnsay, Allyson Charissa T - Activity 4Allyson Charissa AnsayNo ratings yet

- Advanced Accounting Ch3 Cost MethodDocument3 pagesAdvanced Accounting Ch3 Cost MethodFiona TaNo ratings yet

- Economics Higher Level Paper 3: Instructions To CandidatesDocument20 pagesEconomics Higher Level Paper 3: Instructions To Candidatessnadim123No ratings yet

- Online Lecture Material FR IMAGE 03Document28 pagesOnline Lecture Material FR IMAGE 03Dave ClintonNo ratings yet

- In Other Words RE Increased by P250,000 (Income Less Dividends)Document6 pagesIn Other Words RE Increased by P250,000 (Income Less Dividends)Agatha de CastroNo ratings yet

- Quiz - Investment ANSWERDocument3 pagesQuiz - Investment ANSWERJaylord ReyesNo ratings yet

- L7 Consolidation 3 Lecture SolutionsDocument6 pagesL7 Consolidation 3 Lecture SolutionsrohmasspamNo ratings yet

- Accounting Review-Activity 1 Answers 1. B. 2,200,000Document6 pagesAccounting Review-Activity 1 Answers 1. B. 2,200,000Junvy AbordoNo ratings yet

- Unit 9 Retained Earnings: Topic 2 - Appropriation and Quasi-ReorganizationDocument4 pagesUnit 9 Retained Earnings: Topic 2 - Appropriation and Quasi-ReorganizationRey HandumonNo ratings yet

- AFAR-01A (Supplemental Material To Partnership Accounting)Document2 pagesAFAR-01A (Supplemental Material To Partnership Accounting)Maricris AlilinNo ratings yet

- Tutorial 3 Ans PDFDocument13 pagesTutorial 3 Ans PDFSharmiSharlaNo ratings yet

- Problem16 5acctgDocument2 pagesProblem16 5acctgAleah kay BalontongNo ratings yet

- Reo Afst TryDocument4 pagesReo Afst TryAEDRIAN LEE DERECHONo ratings yet

- Chapter 9 Multiple ChoicesDocument5 pagesChapter 9 Multiple Choicesshiroe raabuNo ratings yet

- 2023-Vol-1-Ch-4-Problems-Ans 2Document10 pages2023-Vol-1-Ch-4-Problems-Ans 2Glen ValdezcoNo ratings yet

- Seminar 2 FeedbackDocument5 pagesSeminar 2 FeedbackjekaterinaNo ratings yet

- ACCA Chapter 25,26,27,28,29Document10 pagesACCA Chapter 25,26,27,28,29Esperanza Erens KristiyuantoNo ratings yet

- UntitledDocument2 pagesUntitledNur AsnadirahNo ratings yet

- Illustration 1 & 2Document5 pagesIllustration 1 & 2faith olaNo ratings yet

- Lab 3 - Stock Investment: FATA 2015Document3 pagesLab 3 - Stock Investment: FATA 2015Firda ZhafirahNo ratings yet

- UntitledDocument3 pagesUntitledKim VelascoNo ratings yet

- 4A8 OperationDocument8 pages4A8 OperationCarl Dhaniel Garcia SalenNo ratings yet

- Revision College NotesDocument24 pagesRevision College NotesRiyaNo ratings yet

- Financial Reporting 2 Final Exam 2020Document3 pagesFinancial Reporting 2 Final Exam 2020kateNo ratings yet

- Working PaperDocument1 pageWorking PaperVina Rahma AuliyaNo ratings yet

- Acc 3013 - Fwa Revision AnswersDocument15 pagesAcc 3013 - Fwa Revision Answersfalnuaimi001No ratings yet

- MJ20 FR Sample - Suggested Solutions and Marking Schemes v1.0 PDFDocument9 pagesMJ20 FR Sample - Suggested Solutions and Marking Schemes v1.0 PDFfatehsalehNo ratings yet

- Corporate Finance Solution Chapter 6Document9 pagesCorporate Finance Solution Chapter 6Kunal KumarNo ratings yet

- Shareholder's Equity 2 - PracAccDocument19 pagesShareholder's Equity 2 - PracAccClyn CFNo ratings yet

- 2601 PartnershipsDocument57 pages2601 PartnershipsMerdzNo ratings yet

- ACC2002 Practice 2Document8 pagesACC2002 Practice 2Đan LêNo ratings yet

- SolMan Chapter 4 (Partial)Document9 pagesSolMan Chapter 4 (Partial)zaounxosakubNo ratings yet

- Chapter3aa1sol 2012Document28 pagesChapter3aa1sol 2012JudeNo ratings yet

- MI Worksheet Final LectureDocument3 pagesMI Worksheet Final Lecturethapa_bisNo ratings yet

- ACP312 Intercompany-Sale-Of-Inventory-QuizDocument31 pagesACP312 Intercompany-Sale-Of-Inventory-QuizJocelyn GorospeNo ratings yet

- Ifrs 9 Equity Investments IllustrationDocument7 pagesIfrs 9 Equity Investments IllustrationVatchdemonNo ratings yet

- #75 Busns CombinationDocument3 pages#75 Busns CombinationJon Dumagil InocentesNo ratings yet

- HI 5020 Corporate Accounting: Session 8c Intra-Group TransactionsDocument24 pagesHI 5020 Corporate Accounting: Session 8c Intra-Group TransactionsFeku RamNo ratings yet

- Financial Accounting 3a Assignment 2 2022Document9 pagesFinancial Accounting 3a Assignment 2 2022sartynaftalNo ratings yet

- Problems #1Document20 pagesProblems #1Kaye ManeseNo ratings yet

- Jawaban UTS Genap 2007 AkunDocument8 pagesJawaban UTS Genap 2007 Akunapi-3862199No ratings yet

- Tugas 10Document3 pagesTugas 10Reyhan ArioNo ratings yet

- Afar 2701 PartnershipDocument57 pagesAfar 2701 PartnershipJoshmyrrh Richwel GammadNo ratings yet

- Assignment BAC4102 FDocument5 pagesAssignment BAC4102 FKeemeNo ratings yet

- Far570 Group ProjectDocument4 pagesFar570 Group ProjectN FrzanahNo ratings yet

- Principle and Practice of TaxationDocument5 pagesPrinciple and Practice of TaxationAgyeiNo ratings yet

- Afar 2Document36 pagesAfar 2dbpcastro8No ratings yet

- Solutions - Formation-LumpSum LiquidationDocument14 pagesSolutions - Formation-LumpSum LiquidationLuna SanNo ratings yet

- AACA2 AssignmentsDocument20 pagesAACA2 AssignmentsadieNo ratings yet

- AK18M - Tugas Direct and Indirect Purchase of Obligation Dea LilisDocument4 pagesAK18M - Tugas Direct and Indirect Purchase of Obligation Dea LilisDea Aulia AmanahNo ratings yet

- AP Review NotesDocument2 pagesAP Review NotesCattleyaNo ratings yet

- Gonzales, Ian Rogel L. - Assignment#5Document3 pagesGonzales, Ian Rogel L. - Assignment#5GONZALES, IAN ROGEL L.No ratings yet

- Solution Capital StatementDocument10 pagesSolution Capital StatementhilmanNo ratings yet

- FAC 2602 - 2023 - S1 - Assessment 4 SolutionDocument13 pagesFAC 2602 - 2023 - S1 - Assessment 4 SolutionlennoxhaniNo ratings yet

- Audit CH 9Document6 pagesAudit CH 9Phoebe Dayrit CunananNo ratings yet

- AFAR Preweek Lecture (B42)Document34 pagesAFAR Preweek Lecture (B42)Ciarie Mae Salgado100% (2)

- Fracture TestDocument1 pageFracture TestYuvaraj SathishNo ratings yet

- Property, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Document37 pagesProperty, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Eshetie Mekonene AmareNo ratings yet

- Ratio Analysis of Rafhan FoodsDocument6 pagesRatio Analysis of Rafhan FoodsusmanazizbhattiNo ratings yet

- Calgary Cooperative Funeral Services - Business PlanDocument21 pagesCalgary Cooperative Funeral Services - Business PlanastuteNo ratings yet

- JWT Advertising AgencyDocument6 pagesJWT Advertising AgencysumangalatalurNo ratings yet

- CQA Primer 2019 SampleDocument16 pagesCQA Primer 2019 SampleGee100% (1)

- 9 MPSDocument49 pages9 MPSIrmanda SyahraniNo ratings yet

- Stakeholders-Heathrow T5-Case StudyDocument6 pagesStakeholders-Heathrow T5-Case StudyBanshi DindaNo ratings yet

- Fall Protection Safety AuditDocument1 pageFall Protection Safety AuditVikas YamagarNo ratings yet

- GO (P) No 106-16-Fin DateDocument2 pagesGO (P) No 106-16-Fin Datesunil777tvpmNo ratings yet

- Software Engineering PDFDocument157 pagesSoftware Engineering PDFReshma DevaNo ratings yet

- Group 6 Section B Tech Talk Social Media Strategy PDFDocument22 pagesGroup 6 Section B Tech Talk Social Media Strategy PDFDevanshi Grover100% (1)

- Operation Strategy at Galanz - Piyush KatejaDocument11 pagesOperation Strategy at Galanz - Piyush KatejaPiyush KatejaNo ratings yet

- Buku Log Latihan IndustriDocument26 pagesBuku Log Latihan IndustriajimNo ratings yet

- Managerial Decision Modeling With Spreadsheets: (3rd Edition)Document8 pagesManagerial Decision Modeling With Spreadsheets: (3rd Edition)Niyati ShahNo ratings yet

- Readings - Capital Budgeting - 2Document12 pagesReadings - Capital Budgeting - 2Anish AdhikariNo ratings yet

- Nareg - Make It OutDocument2 pagesNareg - Make It OutLevani JavakhadzeNo ratings yet

- The Revival Strategies of Vespa Scooter in IndiaDocument4 pagesThe Revival Strategies of Vespa Scooter in IndiaJagatheeswari SelviNo ratings yet

- Dissertation Topics For Mba HR StudentsDocument6 pagesDissertation Topics For Mba HR StudentsPapersWritingServiceUK100% (1)

- Corporate Attributes and Creative Accounting of Listed Consumer Firms in NigeriaDocument9 pagesCorporate Attributes and Creative Accounting of Listed Consumer Firms in NigeriaBOHR International Journal of Advances in Management ResearchNo ratings yet

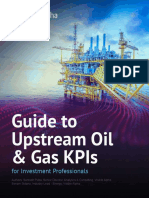

- Visible Alpha Guide To Oil and Gas E&P KPIsDocument29 pagesVisible Alpha Guide To Oil and Gas E&P KPIsdeepikaNo ratings yet

- Synopsis On Virtual Shopping MallDocument56 pagesSynopsis On Virtual Shopping MallSourav KumarNo ratings yet

- UNIT 2 Product Development &product Life CycleDocument18 pagesUNIT 2 Product Development &product Life Cycletherashijain16No ratings yet

- Accounts ProjectDocument12 pagesAccounts Projectsoham dangeNo ratings yet

- Screening Process - Digital Marketing - 9thapril2020Document4 pagesScreening Process - Digital Marketing - 9thapril2020SAURABH SINGHNo ratings yet

- Midterms Exam Tech BsitDocument8 pagesMidterms Exam Tech BsitAC GanadoNo ratings yet