Download as pdf or txt

You might also like

- STANDARD OPERATING PROCEDURE (SOP) Rooftop SolarDocument23 pagesSTANDARD OPERATING PROCEDURE (SOP) Rooftop Solarzatkbgfebnjolcvruv100% (3)

- Energy Storage: Legal and Regulatory Challenges and OpportunitiesFrom EverandEnergy Storage: Legal and Regulatory Challenges and OpportunitiesNo ratings yet

- Full Faith & Credit ActDocument6 pagesFull Faith & Credit ActRoy Tanner100% (3)

- Advantages and Disadvantages of Solar EnergyDocument3 pagesAdvantages and Disadvantages of Solar Energyrubenmariadasan100% (4)

- Exhibitors ListDocument19 pagesExhibitors Listamit goyalNo ratings yet

- Qoaider CSP EnerMENA PresentationDocument24 pagesQoaider CSP EnerMENA PresentationDr alla talal yassinNo ratings yet

- Federal Funding ResourcesDocument4 pagesFederal Funding ResourcesjohnribarNo ratings yet

- HTTP Dsireusaorg Incentives Incentive 2Document2 pagesHTTP Dsireusaorg Incentives Incentive 2Sadara BarrowNo ratings yet

- PTC, ITC, or Cash GrantDocument21 pagesPTC, ITC, or Cash GrantNicolas TroussardNo ratings yet

- State and Federal Policies For Renewable EnergyDocument10 pagesState and Federal Policies For Renewable Energydayawulandari96No ratings yet

- Handbook of Green Building Des6d7b8f7089cb - Anna's Archive 51Document1 pageHandbook of Green Building Des6d7b8f7089cb - Anna's Archive 51gamedesigning87No ratings yet

- Irs CrebsrepcrepitaxsummaryDocument3 pagesIrs CrebsrepcrepitaxsummarymungagungadinNo ratings yet

- Inflation Reduction ActDocument18 pagesInflation Reduction ActEdwin GamboaNo ratings yet

- Advancing The Growth of The U.S. Wind Industry: Federal Incentives, Funding, and Partnership OpportunitiesDocument6 pagesAdvancing The Growth of The U.S. Wind Industry: Federal Incentives, Funding, and Partnership OpportunitiesSUPER INDUSTRIAL ONLINENo ratings yet

- Opportunities in Wind Power Projects in ArgentinaDocument1 pageOpportunities in Wind Power Projects in ArgentinaNicolasEliaschevNo ratings yet

- WND Enegry in IndiaDocument20 pagesWND Enegry in IndiaManohara Reddy PittuNo ratings yet

- Solar Parameter SummaryDocument5 pagesSolar Parameter Summarysrivastava_yugankNo ratings yet

- IRENA RE Latin America Policies 2015 Country ChileDocument9 pagesIRENA RE Latin America Policies 2015 Country ChileBarbara Hansen-DuncanNo ratings yet

- Small Biomass Based Grid Interactive ProjectsDocument3 pagesSmall Biomass Based Grid Interactive Projectsanu141No ratings yet

- Union Budget 2011: Tax Holiday For Power Sector Exended by One YearDocument12 pagesUnion Budget 2011: Tax Holiday For Power Sector Exended by One Yearvivek_sharma@live.inNo ratings yet

- Energy Saving Trust FIT Review Fact SheetDocument9 pagesEnergy Saving Trust FIT Review Fact SheetAdamVaughanNo ratings yet

- The Ins and Outs of Energy Services Agreements - Energy ManagerDocument8 pagesThe Ins and Outs of Energy Services Agreements - Energy ManagerFirst_LastNo ratings yet

- Electricity GenerationDocument20 pagesElectricity GenerationAlaa EhsanNo ratings yet

- Feed-In Tariff (Fit) in Malaysia: WWW - Seda.gov - MyDocument8 pagesFeed-In Tariff (Fit) in Malaysia: WWW - Seda.gov - MyWeiyang TanNo ratings yet

- Power Policy 1994Document15 pagesPower Policy 1994Nauman AkramNo ratings yet

- 145 NotificationDocument21 pages145 NotificationTheGreen BeinNo ratings yet

- SC U 04 2020Document55 pagesSC U 04 2020luxymaheshNo ratings yet

- Are There Any Restrictions Concerning The Foreign Ownership of Electricity Companies or Assets?Document4 pagesAre There Any Restrictions Concerning The Foreign Ownership of Electricity Companies or Assets?Reena MaNo ratings yet

- An Overview of Recent Events For Renewable Energy in Timor-Leste (As of 03 March 2010)Document4 pagesAn Overview of Recent Events For Renewable Energy in Timor-Leste (As of 03 March 2010)scttmcknnnNo ratings yet

- Funding EnergyDocument3 pagesFunding EnergyjohnribarNo ratings yet

- Top Ten' Questions & Answers About Solar Power in OttawaDocument2 pagesTop Ten' Questions & Answers About Solar Power in OttawaRaghu RamNo ratings yet

- Proposal Concerning Utility 2.0 InvestmentsDocument6 pagesProposal Concerning Utility 2.0 InvestmentsNewsdayNo ratings yet

- Frequently Asked Questions: GeneralDocument12 pagesFrequently Asked Questions: GeneralteeyenNo ratings yet

- Codes, Standards and LegislationDocument13 pagesCodes, Standards and LegislationSyed Fawad MarwatNo ratings yet

- The Curious Case of Indias Discoms August 2020Document59 pagesThe Curious Case of Indias Discoms August 2020PraveenNo ratings yet

- Clifford Chance Climate Change Task 1Document1 pageClifford Chance Climate Change Task 1Hannah KamiliyaNo ratings yet

- Faq EnergyDocument2 pagesFaq Energyandrea_e_vedderNo ratings yet

- Regional Greenhouse Gas Initiative Moves Forward - What Does It Mean For Wind Power?Document13 pagesRegional Greenhouse Gas Initiative Moves Forward - What Does It Mean For Wind Power?Northeast Wind Resource Center (NWRC)No ratings yet

- PTI Energy PolicyDocument52 pagesPTI Energy PolicyPTI Official100% (9)

- Renewable Energy: Policy Analysis of Major ConsumersDocument8 pagesRenewable Energy: Policy Analysis of Major ConsumersAwaneesh ShuklaNo ratings yet

- KPMG Union Budget Energy and Natural Resources PoV 2015Document9 pagesKPMG Union Budget Energy and Natural Resources PoV 2015Mukul AzadNo ratings yet

- Comments On RTSDocument8 pagesComments On RTSjay lakhaniNo ratings yet

- Executive Summary: Key PointsDocument9 pagesExecutive Summary: Key PointsBurchell WilsonNo ratings yet

- Damitha Kumarasinghe - Feed-In-Tariff Sri Lankan ExperienceDocument20 pagesDamitha Kumarasinghe - Feed-In-Tariff Sri Lankan ExperienceAsia Clean Energy ForumNo ratings yet

- Cost of Electricity Generation From Hydropower Plants-2Document1 pageCost of Electricity Generation From Hydropower Plants-2Awais AliNo ratings yet

- European Renewable Energy IncentiveDocument7 pagesEuropean Renewable Energy Incentiveapi-241926555No ratings yet

- LL S.R.L. Green Power: Project Buffalo - Business PropositionDocument26 pagesLL S.R.L. Green Power: Project Buffalo - Business Propositionapi-161028199No ratings yet

- Accounting For Electricity Company (IPCC)Document10 pagesAccounting For Electricity Company (IPCC)Rahul Prasad75% (4)

- Electricity Capital Funding v3Document2 pagesElectricity Capital Funding v3api-250660143No ratings yet

- Small Hydro Power Development and PolicyDocument6 pagesSmall Hydro Power Development and PolicywinmyintzawNo ratings yet

- Annual Work Plan 2010 and 5-Year Sector Timeline 2010 - 2014Document28 pagesAnnual Work Plan 2010 and 5-Year Sector Timeline 2010 - 2014Waqas AhmedNo ratings yet

- Guidelines For Development of Hydro Electric ProjectDocument11 pagesGuidelines For Development of Hydro Electric ProjectSushil DhunganaNo ratings yet

- DOE Loan Guarantee Rules Final 4oct 2007 Companies Can ApplyDocument4 pagesDOE Loan Guarantee Rules Final 4oct 2007 Companies Can ApplyKim HedumNo ratings yet

- Perspective On The Proposed Renewable Heat Incentive (RHI) : Summary PointsDocument9 pagesPerspective On The Proposed Renewable Heat Incentive (RHI) : Summary Pointsawhk2006No ratings yet

- Cost of Electricity GenerationDocument2 pagesCost of Electricity GenerationAwais AliNo ratings yet

- Public Consultation: Proposed Work Plan and BudgetDocument37 pagesPublic Consultation: Proposed Work Plan and BudgetBernewsAdminNo ratings yet

- BoozCo Renewable Energy Technologies CrossroadsDocument24 pagesBoozCo Renewable Energy Technologies CrossroadsSikander GirgoukarNo ratings yet

- Energy Talking Points 1Document2 pagesEnergy Talking Points 1Jane PorterNo ratings yet

- Unlocking The Power Sector:: SustainableDocument21 pagesUnlocking The Power Sector:: SustainableThe Sustainable Development Commission (UK, 2000-2011)No ratings yet

- GBIDocument6 pagesGBIAnanth VybhavNo ratings yet

- PWC Indonesia Energy, Utilities & Mining NewsflashDocument16 pagesPWC Indonesia Energy, Utilities & Mining Newsflash'El'KahfiRahmatNo ratings yet

- Government Response: Renewables Obligation ConsultationDocument36 pagesGovernment Response: Renewables Obligation ConsultationBeta AnalyticNo ratings yet

- Renewable energy finance: Sovereign guaranteesFrom EverandRenewable energy finance: Sovereign guaranteesNo ratings yet

- Trump's List - 289 Accomplishments in Just 20 Months, Relentless' Promise-KeepingDocument12 pagesTrump's List - 289 Accomplishments in Just 20 Months, Relentless' Promise-KeepingRoy TannerNo ratings yet

- Gates of HellDocument1 pageGates of HellRoy TannerNo ratings yet

- The Gospel Makes A ComebackDocument1 pageThe Gospel Makes A ComebackRoy TannerNo ratings yet

- America at A Crossroad: TerrorismDocument1 pageAmerica at A Crossroad: TerrorismRoy TannerNo ratings yet

- Trump's List - 289 Accomplishments in Just 20 Months, Relentless' Promise-KeepingDocument12 pagesTrump's List - 289 Accomplishments in Just 20 Months, Relentless' Promise-KeepingRoy TannerNo ratings yet

- 32 Bible Verses About Being Born AgainDocument4 pages32 Bible Verses About Being Born AgainRoy Tanner100% (1)

- Apostasy in The Church and False Doctrines of MenDocument13 pagesApostasy in The Church and False Doctrines of MenRoy TannerNo ratings yet

- 2013 Application For Automatic Extension of Time To File U.S. Individual Income Tax ReturnDocument4 pages2013 Application For Automatic Extension of Time To File U.S. Individual Income Tax ReturnRoy TannerNo ratings yet

- VirgoDocument3 pagesVirgoRoy TannerNo ratings yet

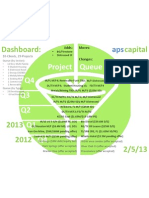

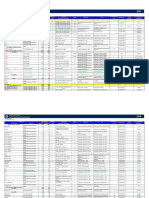

- APSC Project QueueDocument1 pageAPSC Project QueueRoy TannerNo ratings yet

- Cosmic Star of DavidDocument1 pageCosmic Star of DavidRoy Tanner100% (1)

- Siren Songs of StatismDocument1 pageSiren Songs of StatismRoy TannerNo ratings yet

- Entrepreneur & Economy Fast FactsDocument2 pagesEntrepreneur & Economy Fast FactsRoy TannerNo ratings yet

- The Chicago Plan RevisitedDocument71 pagesThe Chicago Plan RevisitedYannis KoutsomitisNo ratings yet

- Adequacy Evaluation of Wind Power Generation Systems: Guided By: TeamDocument7 pagesAdequacy Evaluation of Wind Power Generation Systems: Guided By: TeamAshish AssisiNo ratings yet

- AniketDocument22 pagesAniketanurudhNo ratings yet

- Jawaharlal Nehru National Solar MissionDocument55 pagesJawaharlal Nehru National Solar MissionIshan TiwariNo ratings yet

- String LayoutDocument1 pageString Layoutsyedabubakars12No ratings yet

- Pvpp12 LowDocument108 pagesPvpp12 LowMenthor555No ratings yet

- GRP Project IIDocument24 pagesGRP Project IIJaydeep MulchandaniNo ratings yet

- Ministry of New and Renewable Energy (MNRE)Document12 pagesMinistry of New and Renewable Energy (MNRE)Amol KhadkeNo ratings yet

- Existing Power Plants Mindanao December 2018 PDFDocument3 pagesExisting Power Plants Mindanao December 2018 PDFGM PNo ratings yet

- Heliatek Sets New Organic Photovoltaic World Record Efficiency of 13.2%Document2 pagesHeliatek Sets New Organic Photovoltaic World Record Efficiency of 13.2%reema luizNo ratings yet

- Exploitation of Natural ResourcesDocument3 pagesExploitation of Natural ResourcesMuhammad HabibNo ratings yet

- DiMarzio, G. 2015. The Stillwater Triple Hybrid Power Plant Integrating Geothermal, Solar Photovoltaic and Solar Thermal Power GenerationDocument5 pagesDiMarzio, G. 2015. The Stillwater Triple Hybrid Power Plant Integrating Geothermal, Solar Photovoltaic and Solar Thermal Power GenerationPablitoNo ratings yet

- Cost Effective Analysis of Solar and Wind Power in OmanDocument15 pagesCost Effective Analysis of Solar and Wind Power in OmanMichael GregoryNo ratings yet

- Company Profile PDFDocument3 pagesCompany Profile PDFDivNo ratings yet

- ASC Presentation PDFDocument89 pagesASC Presentation PDFAhmadHussain09No ratings yet

- B. Vocabulary and Grammar: Find The Word Which Doesn't Belong To Each GroupDocument4 pagesB. Vocabulary and Grammar: Find The Word Which Doesn't Belong To Each GroupBretuoba Korankye AnkrahNo ratings yet

- Presentation Innovative Turbine AnakataDocument21 pagesPresentation Innovative Turbine AnakataCristhianFernandoChuraMamaniNo ratings yet

- The Control Center of Gestamp Wind Has Been Accredited by "Red Eléctrica Española"Document2 pagesThe Control Center of Gestamp Wind Has Been Accredited by "Red Eléctrica Española"ACEK RenewablesNo ratings yet

- Solar EnergyDocument4 pagesSolar Energyjenn78No ratings yet

- GESCOM Notification EngDocument2 pagesGESCOM Notification EngshakeebNo ratings yet

- Solar Workshop PowerPoint TemplateDocument22 pagesSolar Workshop PowerPoint TemplateKen ScalesNo ratings yet

- Review Petition Final (V2)Document43 pagesReview Petition Final (V2)Dipanwita Roy100% (1)

- Cavite State University: Capsule For Thesis/Capstone/CapsuleDocument4 pagesCavite State University: Capsule For Thesis/Capstone/CapsuleJohn Mark CantalNo ratings yet

- Design and Control Strategy of Utility Interfaced PV/WTG Hybrid SystemDocument6 pagesDesign and Control Strategy of Utility Interfaced PV/WTG Hybrid SystemDr. Adel A. Elbaset100% (1)

- ASE Lesson PlanDocument37 pagesASE Lesson PlanKrishna MurthyNo ratings yet

- Renewable Energy - Angger Setyo Kusumo - 18050874030 - SP2018Document2 pagesRenewable Energy - Angger Setyo Kusumo - 18050874030 - SP2018Angger Setyo KusumoNo ratings yet

- Idees - Predavanje 10 v2Document143 pagesIdees - Predavanje 10 v2Arnel PNo ratings yet

- Looking For Renewable Energy Master Thesis TopicDocument4 pagesLooking For Renewable Energy Master Thesis TopichussainNo ratings yet