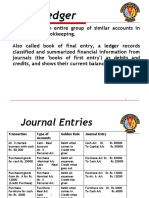

Golden Rule

Golden Rule

You might also like

- Venessa Shilpa FIDocument7 pagesVenessa Shilpa FIamershareef337No ratings yet

- Financial Accounting: I Term - MbaDocument39 pagesFinancial Accounting: I Term - MbaShujath SharieffNo ratings yet

- Basic Terms in Accounts: Assets: Something That You OwnDocument46 pagesBasic Terms in Accounts: Assets: Something That You OwnLeo GladwinNo ratings yet

- 5 FMA Sesskion-5Document4 pages5 FMA Sesskion-5Ashish KumawatNo ratings yet

- Two Column Cash BookDocument24 pagesTwo Column Cash BookDarshans dadNo ratings yet

- Question: Ledger, TB: Dr cash 变多5000Document2 pagesQuestion: Ledger, TB: Dr cash 变多5000S1X 32 許詠棋 KohYongKeeNo ratings yet

- Lesson 1 - Introduction To LedgerDocument18 pagesLesson 1 - Introduction To LedgerNikhita MehraNo ratings yet

- Financial Accounting - Journal EntriesDocument28 pagesFinancial Accounting - Journal EntriesPraneeth KumarNo ratings yet

- Basic Account 1Document10 pagesBasic Account 1COMPUTER WORLDNo ratings yet

- 88ikkjuuikkjj MMJFM FDocument8 pages88ikkjuuikkjj MMJFM FpnareshpnkNo ratings yet

- 3 - Trial Balance To PL Account - ExamplesDocument49 pages3 - Trial Balance To PL Account - ExamplesDivyansh Pandey100% (2)

- Journalizing TransactionsDocument5 pagesJournalizing TransactionsSatvik Bisht100% (1)

- Tally Repor1Document74 pagesTally Repor1Ronak JainNo ratings yet

- 10 Illustration of Ledger 24.10.08Document7 pages10 Illustration of Ledger 24.10.08denish gandhi100% (2)

- Basic Jornal Accounting Pratice 1Document20 pagesBasic Jornal Accounting Pratice 1Lakshya AgrawalNo ratings yet

- 1 BasicConceptDocument9 pages1 BasicConceptVinod RathodNo ratings yet

- Worksheet 1 NMIMS SolutionsDocument7 pagesWorksheet 1 NMIMS SolutionsvipulNo ratings yet

- Example - Class 3Document25 pagesExample - Class 3sakshita palNo ratings yet

- What Are The Golden Rules For AccountingDocument28 pagesWhat Are The Golden Rules For AccountingWong KianTatNo ratings yet

- Lesson 3 - Mechanics of AccountingDocument34 pagesLesson 3 - Mechanics of AccountingYogesh KumarNo ratings yet

- Accounting and Transaction Processing Assignment ADocument6 pagesAccounting and Transaction Processing Assignment AShubha KoiralaNo ratings yet

- Third Day Tally Contents (Journal Entry Part - 1)Document12 pagesThird Day Tally Contents (Journal Entry Part - 1)Kamlesh Kumar100% (1)

- Debit Credit RulesDocument9 pagesDebit Credit RulesMubeen JavedNo ratings yet

- Foa ProjectDocument10 pagesFoa ProjectDrumil KacheriaNo ratings yet

- TallyDocument27 pagesTallyRonak JainNo ratings yet

- Type of Account TallyDocument20 pagesType of Account TallyVERMA NEERAJ100% (2)

- Foa ProjectDocument13 pagesFoa ProjectDrumil KacheriaNo ratings yet

- CCP102Document15 pagesCCP102api-3849444No ratings yet

- Golden and Modern RuleDocument8 pagesGolden and Modern Ruleniraj jainNo ratings yet

- Session 1 BDocument33 pagesSession 1 Babdulw_40No ratings yet

- Accounting Mechanics:: Basic RecordsDocument22 pagesAccounting Mechanics:: Basic RecordsMohit DhawanNo ratings yet

- FINANCIALDocument20 pagesFINANCIALJEBA SCHULZ JNo ratings yet

- Accounts BasicsDocument2 pagesAccounts BasicsRithvik SangilirajNo ratings yet

- Golden Rules of Accounts: Prof. Pallavi Ingale 9850861405Document32 pagesGolden Rules of Accounts: Prof. Pallavi Ingale 9850861405Pallavi Ingale100% (1)

- Question Bank For AccountsDocument12 pagesQuestion Bank For AccountsSwati DubeyNo ratings yet

- Fundamentals of Accounting Model Question PaperDocument3 pagesFundamentals of Accounting Model Question Paperabhishek509.pNo ratings yet

- Bachelor in Business Administration Semester 3: Prepared For: Lecturer's NameDocument3 pagesBachelor in Business Administration Semester 3: Prepared For: Lecturer's NameBrute1989No ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- Tally Prime NotesDocument54 pagesTally Prime Notesroshandhamankar0100% (3)

- Problem 1: Use The Accounting Equation To Show Their Effect On His Assets, Liabilities and CapitalDocument2 pagesProblem 1: Use The Accounting Equation To Show Their Effect On His Assets, Liabilities and CapitalMadeeha KhanNo ratings yet

- 329646710-Venessa-Shilpa-FI Copy 2Document7 pages329646710-Venessa-Shilpa-FI Copy 2pnareshpnkNo ratings yet

- 3 Accounting MechanicsDocument50 pages3 Accounting MechanicsVasu Narang100% (1)

- Journal, Ledger, TB & Final AccountsDocument11 pagesJournal, Ledger, TB & Final AccountsSanjay Dutta100% (1)

- PROBLEMSDocument5 pagesPROBLEMSstudentofficeracademyNo ratings yet

- Test - AccountingDocument7 pagesTest - AccountingSoumyadip DasNo ratings yet

- 179200Document13 pages179200Ankita GuptaNo ratings yet

- Accounting NotesDocument25 pagesAccounting NotesVivienAlagBatalNo ratings yet

- What Is Meant by Debit&Credit?: Human Life in Different StagesDocument30 pagesWhat Is Meant by Debit&Credit?: Human Life in Different StagesRenuka RenuNo ratings yet

- 2 JournalDocument18 pages2 JournalPraveen Yadav100% (1)

- Recording of TransactionDocument20 pagesRecording of TransactionNikita SharmaNo ratings yet

- CCP102Document24 pagesCCP102api-3849444No ratings yet

- BankingDocument11 pagesBankingSg ShaNo ratings yet

- Executive Post Graduate Diploma in Management Subject: Management Accounting & Analysis Question PaperDocument4 pagesExecutive Post Graduate Diploma in Management Subject: Management Accounting & Analysis Question PaperUpasana vNo ratings yet

- Writing and Reading A JournalDocument10 pagesWriting and Reading A JournalGirisha RaoNo ratings yet

- Financial Accounting 1 (By Prof - Rupesh Dahake)Document13 pagesFinancial Accounting 1 (By Prof - Rupesh Dahake)rupeshdahake100% (1)

- Acc106 Group ReportDocument5 pagesAcc106 Group ReportAina AsgaliNo ratings yet

- Chapter - 3 Journal Entries Part 1Document7 pagesChapter - 3 Journal Entries Part 1Abdullah JuttNo ratings yet

- MBA Accounts For ManagerDocument3 pagesMBA Accounts For ManagerGayathri GopiramnathNo ratings yet

- Rules of Debit & CreditDocument16 pagesRules of Debit & CreditVidhya UnniNo ratings yet

Download as docx, pdf, or txt

You might also like

- Venessa Shilpa FIDocument7 pagesVenessa Shilpa FIamershareef337No ratings yet

- Financial Accounting: I Term - MbaDocument39 pagesFinancial Accounting: I Term - MbaShujath SharieffNo ratings yet

- Basic Terms in Accounts: Assets: Something That You OwnDocument46 pagesBasic Terms in Accounts: Assets: Something That You OwnLeo GladwinNo ratings yet

- 5 FMA Sesskion-5Document4 pages5 FMA Sesskion-5Ashish KumawatNo ratings yet

- Two Column Cash BookDocument24 pagesTwo Column Cash BookDarshans dadNo ratings yet

- Question: Ledger, TB: Dr cash 变多5000Document2 pagesQuestion: Ledger, TB: Dr cash 变多5000S1X 32 許詠棋 KohYongKeeNo ratings yet

- Lesson 1 - Introduction To LedgerDocument18 pagesLesson 1 - Introduction To LedgerNikhita MehraNo ratings yet

- Financial Accounting - Journal EntriesDocument28 pagesFinancial Accounting - Journal EntriesPraneeth KumarNo ratings yet

- Basic Account 1Document10 pagesBasic Account 1COMPUTER WORLDNo ratings yet

- 88ikkjuuikkjj MMJFM FDocument8 pages88ikkjuuikkjj MMJFM FpnareshpnkNo ratings yet

- 3 - Trial Balance To PL Account - ExamplesDocument49 pages3 - Trial Balance To PL Account - ExamplesDivyansh Pandey100% (2)

- Journalizing TransactionsDocument5 pagesJournalizing TransactionsSatvik Bisht100% (1)

- Tally Repor1Document74 pagesTally Repor1Ronak JainNo ratings yet

- 10 Illustration of Ledger 24.10.08Document7 pages10 Illustration of Ledger 24.10.08denish gandhi100% (2)

- Basic Jornal Accounting Pratice 1Document20 pagesBasic Jornal Accounting Pratice 1Lakshya AgrawalNo ratings yet

- 1 BasicConceptDocument9 pages1 BasicConceptVinod RathodNo ratings yet

- Worksheet 1 NMIMS SolutionsDocument7 pagesWorksheet 1 NMIMS SolutionsvipulNo ratings yet

- Example - Class 3Document25 pagesExample - Class 3sakshita palNo ratings yet

- What Are The Golden Rules For AccountingDocument28 pagesWhat Are The Golden Rules For AccountingWong KianTatNo ratings yet

- Lesson 3 - Mechanics of AccountingDocument34 pagesLesson 3 - Mechanics of AccountingYogesh KumarNo ratings yet

- Accounting and Transaction Processing Assignment ADocument6 pagesAccounting and Transaction Processing Assignment AShubha KoiralaNo ratings yet

- Third Day Tally Contents (Journal Entry Part - 1)Document12 pagesThird Day Tally Contents (Journal Entry Part - 1)Kamlesh Kumar100% (1)

- Debit Credit RulesDocument9 pagesDebit Credit RulesMubeen JavedNo ratings yet

- Foa ProjectDocument10 pagesFoa ProjectDrumil KacheriaNo ratings yet

- TallyDocument27 pagesTallyRonak JainNo ratings yet

- Type of Account TallyDocument20 pagesType of Account TallyVERMA NEERAJ100% (2)

- Foa ProjectDocument13 pagesFoa ProjectDrumil KacheriaNo ratings yet

- CCP102Document15 pagesCCP102api-3849444No ratings yet

- Golden and Modern RuleDocument8 pagesGolden and Modern Ruleniraj jainNo ratings yet

- Session 1 BDocument33 pagesSession 1 Babdulw_40No ratings yet

- Accounting Mechanics:: Basic RecordsDocument22 pagesAccounting Mechanics:: Basic RecordsMohit DhawanNo ratings yet

- FINANCIALDocument20 pagesFINANCIALJEBA SCHULZ JNo ratings yet

- Accounts BasicsDocument2 pagesAccounts BasicsRithvik SangilirajNo ratings yet

- Golden Rules of Accounts: Prof. Pallavi Ingale 9850861405Document32 pagesGolden Rules of Accounts: Prof. Pallavi Ingale 9850861405Pallavi Ingale100% (1)

- Question Bank For AccountsDocument12 pagesQuestion Bank For AccountsSwati DubeyNo ratings yet

- Fundamentals of Accounting Model Question PaperDocument3 pagesFundamentals of Accounting Model Question Paperabhishek509.pNo ratings yet

- Bachelor in Business Administration Semester 3: Prepared For: Lecturer's NameDocument3 pagesBachelor in Business Administration Semester 3: Prepared For: Lecturer's NameBrute1989No ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- Tally Prime NotesDocument54 pagesTally Prime Notesroshandhamankar0100% (3)

- Problem 1: Use The Accounting Equation To Show Their Effect On His Assets, Liabilities and CapitalDocument2 pagesProblem 1: Use The Accounting Equation To Show Their Effect On His Assets, Liabilities and CapitalMadeeha KhanNo ratings yet

- 329646710-Venessa-Shilpa-FI Copy 2Document7 pages329646710-Venessa-Shilpa-FI Copy 2pnareshpnkNo ratings yet

- 3 Accounting MechanicsDocument50 pages3 Accounting MechanicsVasu Narang100% (1)

- Journal, Ledger, TB & Final AccountsDocument11 pagesJournal, Ledger, TB & Final AccountsSanjay Dutta100% (1)

- PROBLEMSDocument5 pagesPROBLEMSstudentofficeracademyNo ratings yet

- Test - AccountingDocument7 pagesTest - AccountingSoumyadip DasNo ratings yet

- 179200Document13 pages179200Ankita GuptaNo ratings yet

- Accounting NotesDocument25 pagesAccounting NotesVivienAlagBatalNo ratings yet

- What Is Meant by Debit&Credit?: Human Life in Different StagesDocument30 pagesWhat Is Meant by Debit&Credit?: Human Life in Different StagesRenuka RenuNo ratings yet

- 2 JournalDocument18 pages2 JournalPraveen Yadav100% (1)

- Recording of TransactionDocument20 pagesRecording of TransactionNikita SharmaNo ratings yet

- CCP102Document24 pagesCCP102api-3849444No ratings yet

- BankingDocument11 pagesBankingSg ShaNo ratings yet

- Executive Post Graduate Diploma in Management Subject: Management Accounting & Analysis Question PaperDocument4 pagesExecutive Post Graduate Diploma in Management Subject: Management Accounting & Analysis Question PaperUpasana vNo ratings yet

- Writing and Reading A JournalDocument10 pagesWriting and Reading A JournalGirisha RaoNo ratings yet

- Financial Accounting 1 (By Prof - Rupesh Dahake)Document13 pagesFinancial Accounting 1 (By Prof - Rupesh Dahake)rupeshdahake100% (1)

- Acc106 Group ReportDocument5 pagesAcc106 Group ReportAina AsgaliNo ratings yet

- Chapter - 3 Journal Entries Part 1Document7 pagesChapter - 3 Journal Entries Part 1Abdullah JuttNo ratings yet

- MBA Accounts For ManagerDocument3 pagesMBA Accounts For ManagerGayathri GopiramnathNo ratings yet

- Rules of Debit & CreditDocument16 pagesRules of Debit & CreditVidhya UnniNo ratings yet