Download as pdf or txt

You might also like

- Return To Work LetterDocument1 pageReturn To Work LetterDamanManda85% (13)

- Motivational LetterDocument1 pageMotivational Letterramazi941No ratings yet

- 148 On Suspicious Quashed HC DelDocument18 pages148 On Suspicious Quashed HC DelNeena BatlaNo ratings yet

- Augustus Capital JudgmentDocument23 pagesAugustus Capital Judgmentchrispattinson06No ratings yet

- 151-Reopening-Sanction ITAT IMPDocument31 pages151-Reopening-Sanction ITAT IMPNeena BatlaNo ratings yet

- 292b-Mistake-Notice Wrong Name Company SCDocument20 pages292b-Mistake-Notice Wrong Name Company SCNeena BatlaNo ratings yet

- Navneet Dutta Vs ITO Revision of ClaimDocument4 pagesNavneet Dutta Vs ITO Revision of ClaimAnkur ShahNo ratings yet

- TS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDDocument5 pagesTS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDbharath289No ratings yet

- DCIT Vs Toshvin Analytical Private Limited ITAT MumbaiDocument3 pagesDCIT Vs Toshvin Analytical Private Limited ITAT MumbaiCA Prakash Chandra BhandariNo ratings yet

- 2024:BHC-OS:3877-DB: 1/8 Itxa-1491-2019Document8 pages2024:BHC-OS:3877-DB: 1/8 Itxa-1491-2019Shreyas ShrivastavaNo ratings yet

- Alok Bhandari Anr. vs. ACIT ITAT DelhiDocument7 pagesAlok Bhandari Anr. vs. ACIT ITAT DelhivedaNo ratings yet

- 1614060815-5446 Bhupendra JainDocument8 pages1614060815-5446 Bhupendra Jainakhil layogNo ratings yet

- 1614324619-ITA 5044 Arya Process EquipmentDocument6 pages1614324619-ITA 5044 Arya Process Equipmentakhil layogNo ratings yet

- In The High Court of Delhi at New DelhiDocument18 pagesIn The High Court of Delhi at New DelhiSambasivam GanesanNo ratings yet

- Sky Light Hospitality LLP V Assistant Commissioner of Income Tax, New DelhiDocument9 pagesSky Light Hospitality LLP V Assistant Commissioner of Income Tax, New DelhiRaghav NaiduNo ratings yet

- Nitin Parkash Vs DCIT ITAT MumbaiDocument11 pagesNitin Parkash Vs DCIT ITAT MumbaiPuru GuptaNo ratings yet

- Delivery - Westlaw IndiaDocument13 pagesDelivery - Westlaw IndiaDisha LohiyaNo ratings yet

- Per Rajpal Yadav, Judicial MemberDocument5 pagesPer Rajpal Yadav, Judicial MemberSrijan MishraNo ratings yet

- Coon Ol: First DivisionDocument52 pagesCoon Ol: First DivisionMaria Diory Rabajante100% (1)

- 10348632004520708481351refno4550-4553 14 Dcit vs. New Delh Hotels LTDDocument15 pages10348632004520708481351refno4550-4553 14 Dcit vs. New Delh Hotels LTDPrakhar MishraNo ratings yet

- Dated This The 2 Day of November 2016 Present The Hon'Ble MR - Justice Jayant Patel AND The Hon'Ble MR - Justice Aravind KumarDocument32 pagesDated This The 2 Day of November 2016 Present The Hon'Ble MR - Justice Jayant Patel AND The Hon'Ble MR - Justice Aravind KumarKinjal KeyaNo ratings yet

- In The High Court of Delhi at New Delhi % Date of Decision: 10.03.2022 W.P. (C) 6158/2021 and CM APPL. 19532/2021Document7 pagesIn The High Court of Delhi at New Delhi % Date of Decision: 10.03.2022 W.P. (C) 6158/2021 and CM APPL. 19532/2021venugopal murthyNo ratings yet

- Adoption of Stamp Valuation As Sale Consideration Is Not Justified Without Any Evidence - ITAT MumbaiDocument17 pagesAdoption of Stamp Valuation As Sale Consideration Is Not Justified Without Any Evidence - ITAT MumbaiDhanraj SharmaNo ratings yet

- आयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Document8 pagesआयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Saksham ShrivastavNo ratings yet

- Anil Marda 143 2 NoticeDocument32 pagesAnil Marda 143 2 NoticeLNo ratings yet

- Undisclosed Income Discussed by The Delhi High Court Holding Three Former Jharkhand Mukti Morcha MPs Liable To Pay TaxDocument59 pagesUndisclosed Income Discussed by The Delhi High Court Holding Three Former Jharkhand Mukti Morcha MPs Liable To Pay TaxLive LawNo ratings yet

- Revenue WS JDocument13 pagesRevenue WS JSidhaarthNo ratings yet

- In The Income Tax Appellate Tribunal "A" Bench: Bangalore Before Shri N. V. Vasudevan, Vice President and Shri Jason P Boaz, Accountant MemberDocument12 pagesIn The Income Tax Appellate Tribunal "A" Bench: Bangalore Before Shri N. V. Vasudevan, Vice President and Shri Jason P Boaz, Accountant MemberKushwanth Soft SolutionsNo ratings yet

- 2017 39 1501 32212 Judgement 17-Dec-2021Document19 pages2017 39 1501 32212 Judgement 17-Dec-2021Jatinder SinghNo ratings yet

- CIT vs. Dilibagh Rai AroraDocument5 pagesCIT vs. Dilibagh Rai AroraSricharan RNo ratings yet

- Indo Office Solutions (P) Ltd. Versus ACIT, Central Circle-17, New DelhiDocument6 pagesIndo Office Solutions (P) Ltd. Versus ACIT, Central Circle-17, New DelhiAshish GoelNo ratings yet

- Judgment Ito Vs Jawahar Singh CC No 141 3 Dated On 8 February 2010Document16 pagesJudgment Ito Vs Jawahar Singh CC No 141 3 Dated On 8 February 2010Rubal SandhuNo ratings yet

- DCIT v. Punjab Retail - ITAT IndoreDocument17 pagesDCIT v. Punjab Retail - ITAT IndorekalravNo ratings yet

- ETA Star Infopark - WatermarkDocument73 pagesETA Star Infopark - WatermarkRahul KumarNo ratings yet

- 4 Bonifacio Sy Po Vs CTA GR No. 81446Document10 pages4 Bonifacio Sy Po Vs CTA GR No. 81446Jeanne CalalinNo ratings yet

- 4 Bonifacio Sy Po Vs CTA GR No. 81446 PDFDocument10 pages4 Bonifacio Sy Po Vs CTA GR No. 81446 PDFJeanne CalalinNo ratings yet

- Cit (A)Document8 pagesCit (A)Raaja ThalapathyNo ratings yet

- JHC 491832Document11 pagesJHC 491832Kunal NawaleNo ratings yet

- DCIT Vs Force Motors Limited ITAT PuneDocument11 pagesDCIT Vs Force Motors Limited ITAT PuneNIMESH BHATTNo ratings yet

- In The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrDocument47 pagesIn The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrshantXNo ratings yet

- IndexDocument10 pagesIndextanmaystarNo ratings yet

- Tata Motors CaseDocument12 pagesTata Motors CaseRiddhiraj SinghNo ratings yet

- Supreme Court: Basilio E. Duaban For PetitionerDocument4 pagesSupreme Court: Basilio E. Duaban For PetitionermgbautistallaNo ratings yet

- Key Propositions 148 SHRI KAPIL GOELDocument89 pagesKey Propositions 148 SHRI KAPIL GOELRajivShahNo ratings yet

- DIT v. Jyoti Foundation (2013) 357 ITR 388 (Del.)Document5 pagesDIT v. Jyoti Foundation (2013) 357 ITR 388 (Del.)madhusudhan u aNo ratings yet

- Hotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.InDocument2 pagesHotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.Insanjiv kumarNo ratings yet

- Interlocutory Section 54 of IT Act 1961 1715774290Document16 pagesInterlocutory Section 54 of IT Act 1961 1715774290advsakthinathanNo ratings yet

- Adarsh Credit Co-Operative Society LTDDocument7 pagesAdarsh Credit Co-Operative Society LTDdeepakNo ratings yet

- Fitness by Design, Inc., Petitioner, vs. Commissioner of INTERNAL REVENUE, RespondentDocument11 pagesFitness by Design, Inc., Petitioner, vs. Commissioner of INTERNAL REVENUE, RespondentRae ManarNo ratings yet

- DRS Industries - (2021)Document33 pagesDRS Industries - (2021)vedaprakashmNo ratings yet

- Naresh Sunderlal Chug Versus The Income Tax Officer, Ward 8 (1), PuneDocument5 pagesNaresh Sunderlal Chug Versus The Income Tax Officer, Ward 8 (1), PuneAshish GoelNo ratings yet

- Assessee WS JDocument17 pagesAssessee WS JSidhaarthNo ratings yet

- Uma Maheswari - ITAT ChennaiDocument6 pagesUma Maheswari - ITAT ChennaiLakshmivenkataraman T.SNo ratings yet

- Gold Investment TrustDocument8 pagesGold Investment Trusttanuj.agarwalNo ratings yet

- Gurvinder Kaur Bhatia Indore Vs PR Cit 2 Indore On 18 December 2019Document27 pagesGurvinder Kaur Bhatia Indore Vs PR Cit 2 Indore On 18 December 2019praveen chokhaniNo ratings yet

- 2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioDocument7 pages2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioThe Chartered Professional NewsletterNo ratings yet

- Greounds of Appeal To The Commissioner Appeal Against 122Document3 pagesGreounds of Appeal To The Commissioner Appeal Against 122Mian Muhammad Jazib50% (2)

- ITA No.298SRT2023AY.2017-18Document11 pagesITA No.298SRT2023AY.2017-18ys9874145No ratings yet

- Holy Heart Educational Society ITAT RaipurDocument11 pagesHoly Heart Educational Society ITAT RaipurJK JasmatiyaNo ratings yet

- Revfenues MemoDocument6 pagesRevfenues MemoSidhaarthNo ratings yet

- Direct Tax Online: Cited inDocument5 pagesDirect Tax Online: Cited inMukesh RathodNo ratings yet

- Bureaucrats Disputed Bjp Government Ratification of Andrews Ganj Land ScamFrom EverandBureaucrats Disputed Bjp Government Ratification of Andrews Ganj Land ScamNo ratings yet

- 2022 AUSL Omnibus Notes - Civil LawDocument78 pages2022 AUSL Omnibus Notes - Civil LawronaldNo ratings yet

- Election Officer Jobs 2017 All Solved Mcqs Tests Model Papers PDF Book Free Download Election Officers (Bs-17) Course Outline Written Syllabus PaperDocument7 pagesElection Officer Jobs 2017 All Solved Mcqs Tests Model Papers PDF Book Free Download Election Officers (Bs-17) Course Outline Written Syllabus PaperTalha AkhtarNo ratings yet

- Gwennitt County Magistrate Court & MP Somerset LLC UpdatedDocument7 pagesGwennitt County Magistrate Court & MP Somerset LLC Updateddawud beyNo ratings yet

- Document - Military Engineer ServicesDocument14 pagesDocument - Military Engineer ServicesSaChin VermaNo ratings yet

- Civil Appeal (Appli) 24 of 2004Document2 pagesCivil Appeal (Appli) 24 of 2004Day VidNo ratings yet

- History Chapter 1 The Rise of Nationalism in Europe Notes Amp Study MaterialDocument12 pagesHistory Chapter 1 The Rise of Nationalism in Europe Notes Amp Study MaterialAnil KumarNo ratings yet

- Case No. 33 W. Cameron Forbes, J. E. Harding Vs Chuoco Tiaco NotesDocument3 pagesCase No. 33 W. Cameron Forbes, J. E. Harding Vs Chuoco Tiaco NotesLaila Ismael SalisaNo ratings yet

- Who Made Jose Rizal Our Foremost National Hero, and Why?: Group 1Document12 pagesWho Made Jose Rizal Our Foremost National Hero, and Why?: Group 1Richard SanchezNo ratings yet

- EN ISO 648 (2008) (E) CodifiedDocument5 pagesEN ISO 648 (2008) (E) CodifiedKaren HernandezNo ratings yet

- African Centre For Media Excellence (ACME) Annual Lecture On Media and Politics in Africa 2017 - Politics, The Media and Judicial Independence - A Personal FootnoteDocument16 pagesAfrican Centre For Media Excellence (ACME) Annual Lecture On Media and Politics in Africa 2017 - Politics, The Media and Judicial Independence - A Personal FootnoteAfrican Centre for Media ExcellenceNo ratings yet

- General BH Rules Within The PremisesDocument5 pagesGeneral BH Rules Within The Premisesultrakill rampageNo ratings yet

- Labor Law OutlineDocument21 pagesLabor Law OutlinejazzieycpNo ratings yet

- Beo/Licenses & PermissionsDocument2 pagesBeo/Licenses & PermissionsJayant RayNo ratings yet

- BADACDocument8 pagesBADACdesiree joy corpuzNo ratings yet

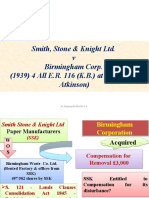

- 10 Smith, Stone & Knight Ltd.Document37 pages10 Smith, Stone & Knight Ltd.gauravNo ratings yet

- Sumaila Bielbiel v. Adamu Dramani & or PDFDocument21 pagesSumaila Bielbiel v. Adamu Dramani & or PDFsbaakpan776No ratings yet

- PP Vs Guilllermo MatantanDocument6 pagesPP Vs Guilllermo MatantanDat Doria PalerNo ratings yet

- Book SM LL.B Tort Law 2023 CH 01Document12 pagesBook SM LL.B Tort Law 2023 CH 01HarshanaaNo ratings yet

- Law Thesis Topics AustraliaDocument6 pagesLaw Thesis Topics Australiacatherinebitkerrochester100% (2)

- Chapter 1 - ObligationsDocument3 pagesChapter 1 - ObligationscartyeolNo ratings yet

- June 12, 1956: March 5Document39 pagesJune 12, 1956: March 5John RyNo ratings yet

- F.M Hammerle RejoinderDocument22 pagesF.M Hammerle RejoinderHarryNo ratings yet

- Constitution and ConstitutionalismDocument26 pagesConstitution and Constitutionalismvnrk585ndzNo ratings yet

- Ben Shapiro NLRB DismissalDocument6 pagesBen Shapiro NLRB DismissalLaw&CrimeNo ratings yet

- Nigeria Is A Founding Member ofDocument3 pagesNigeria Is A Founding Member ofRashid AliNo ratings yet

- MCQs Session 1Document13 pagesMCQs Session 1Harshil MehtaNo ratings yet

- ParsikDocument1 pageParsikkiranNo ratings yet

- GEED 10013: Life and Works of Jose Rizal (Buhay, Mga Gawain at Sinulat Ni Jose Rizal)Document62 pagesGEED 10013: Life and Works of Jose Rizal (Buhay, Mga Gawain at Sinulat Ni Jose Rizal)Maria Fe Noda Casanova100% (1)