03 Lesson 3 - Partnership Dissolution

03 Lesson 3 - Partnership Dissolution

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- 4 - Lecture Notes - Partnership DissolutionDocument18 pages4 - Lecture Notes - Partnership DissolutionNikko Bowie PascualNo ratings yet

- Broidy Amended ComplaintDocument70 pagesBroidy Amended ComplaintLaw&Crime100% (1)

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- 4partnership DissolutionEDITED OnlineDocument15 pages4partnership DissolutionEDITED OnlinePaul BandolaNo ratings yet

- Partnership Formation Activity 2Document4 pagesPartnership Formation Activity 2Shaira Untalan100% (1)

- Partnership Dissolution - Practice ExercisesDocument5 pagesPartnership Dissolution - Practice ExercisesVon Andrei Medina0% (2)

- City of Bingham General Fund Post-Closing Trial Balance As of December 31, 2013 General LedgerDocument8 pagesCity of Bingham General Fund Post-Closing Trial Balance As of December 31, 2013 General LedgerHuma Bashir0% (1)

- Partnership DissolutionDocument21 pagesPartnership DissolutionmartgetaliaNo ratings yet

- Dissolution Is Defined in Article 1825 of The Civil Code of The Philippines As The Change in The RelationDocument18 pagesDissolution Is Defined in Article 1825 of The Civil Code of The Philippines As The Change in The RelationRae SlaughterNo ratings yet

- Chapter 4 DissolutionDocument24 pagesChapter 4 DissolutionJenny BernardinoNo ratings yet

- Partnership Dissolution - PART 1Document17 pagesPartnership Dissolution - PART 1Aby ReedNo ratings yet

- Partnership DissolutionDocument51 pagesPartnership DissolutionChelit LadylieGirl FernandezNo ratings yet

- PartnershipDocument12 pagesPartnershipMila aguasanNo ratings yet

- Accounting 112 C-3Document72 pagesAccounting 112 C-3Mark Erick Acojido RetonelNo ratings yet

- PartnershipDocument14 pagesPartnershipMila aguasanNo ratings yet

- 03 - Partnership DissolutionDocument38 pages03 - Partnership DissolutionDonise Ronadel SantosNo ratings yet

- Dissolution-Changes in OwnershipDocument72 pagesDissolution-Changes in OwnershipmonneNo ratings yet

- Partnership - DissolutionDocument51 pagesPartnership - DissolutionJulius B. OpriasaNo ratings yet

- Partnership Dissolution: Accounting For Special TransactionsDocument58 pagesPartnership Dissolution: Accounting For Special TransactionsjaneNo ratings yet

- 1 Lecture Notes DissolutionDocument17 pages1 Lecture Notes DissolutionMaybelle Espenido0% (2)

- Chapter 4 - Partnership DissolutionDocument15 pagesChapter 4 - Partnership DissolutionXyzra AlfonsoNo ratings yet

- Accounting Treatment of Goodwill at The Time of AdmissionDocument25 pagesAccounting Treatment of Goodwill at The Time of AdmissionMayurRawool100% (2)

- Partnership DissolutionDocument24 pagesPartnership Dissolutionmicaella pasionNo ratings yet

- Partnership Dissolution - DiscussionDocument5 pagesPartnership Dissolution - DiscussionIñego BegdorfNo ratings yet

- 1c Partnership DissolutionDocument9 pages1c Partnership DissolutionMark TaysonNo ratings yet

- Partnership Dissolution DiscussionDocument7 pagesPartnership Dissolution DiscussionDo RaemondNo ratings yet

- Accounting For Partnership DissolutionDocument19 pagesAccounting For Partnership DissolutionMelanie kaye ApostolNo ratings yet

- Acc 30 CorporationDocument8 pagesAcc 30 CorporationGerlie BonleonNo ratings yet

- C ACT100 1 Partnership DissolutionDocument25 pagesC ACT100 1 Partnership DissolutionvmargajavierNo ratings yet

- CMPC 131 3-Partnership-DissltnDocument13 pagesCMPC 131 3-Partnership-DissltnGab IgnacioNo ratings yet

- Dissolution - Changes in OwnershipDocument57 pagesDissolution - Changes in OwnershipJean Rae RemiasNo ratings yet

- PH Dissolution by InvestmentDocument12 pagesPH Dissolution by InvestmentREACTION COPNo ratings yet

- Chapter 2 Dissolution and Liquadation of PartnersipDocument17 pagesChapter 2 Dissolution and Liquadation of PartnersipTekaling NegashNo ratings yet

- Changes in Partnership Ownership Caused byDocument3 pagesChanges in Partnership Ownership Caused byKrizzia MayNo ratings yet

- Reviewer OverallDocument11 pagesReviewer OverallMah2SetNo ratings yet

- Partnership DissolutionDocument17 pagesPartnership DissolutionMich Salvatorē0% (1)

- MinggoyDocument12 pagesMinggoychantrealuna0No ratings yet

- Accounting (Reviewer)Document12 pagesAccounting (Reviewer)Marielle JalandoniNo ratings yet

- Chapter 3 Partnership DissolutionDocument32 pagesChapter 3 Partnership DissolutionmochiNo ratings yet

- DissolutionDocument25 pagesDissolutionallynelbarberNo ratings yet

- Module 3 - Partnership DissolutionDocument54 pagesModule 3 - Partnership DissolutionMaluDyNo ratings yet

- Partnership Dissolution: Prepared By: Cristopherson A. Perez, CPADocument59 pagesPartnership Dissolution: Prepared By: Cristopherson A. Perez, CPAKyla de SilvaNo ratings yet

- AFAR - Partnership DissolutionDocument36 pagesAFAR - Partnership DissolutionReginald ValenciaNo ratings yet

- Detailed Handouts in Partnership DissolutionDocument14 pagesDetailed Handouts in Partnership DissolutionVinz Ray PitargueNo ratings yet

- PARTNERSHIP2Document13 pagesPARTNERSHIP2Anne Marielle Uy0% (2)

- Iv: Accounting For Dissolution (Changes in Membership) of A PartnershipDocument18 pagesIv: Accounting For Dissolution (Changes in Membership) of A PartnershipBerhanu ShancoNo ratings yet

- PARTNERSHIP2Document13 pagesPARTNERSHIP2Anne Marielle UyNo ratings yet

- CMPC131Document15 pagesCMPC131Nhel AlvaroNo ratings yet

- DISSOLUTION - Changes in OwnershipDocument50 pagesDISSOLUTION - Changes in Ownershipmhel cabigonNo ratings yet

- Accounting For Shareholders Equity KINGDocument11 pagesAccounting For Shareholders Equity KINGAlexis KingNo ratings yet

- Partnership & Corporation: 2 SEMESTER 2020-2021Document13 pagesPartnership & Corporation: 2 SEMESTER 2020-2021Erika BucaoNo ratings yet

- Lect.7 Withdrawals of PatnerDocument20 pagesLect.7 Withdrawals of PatnerHany RagabNo ratings yet

- ACCTBA2 ReviewerDocument49 pagesACCTBA2 ReviewerBiean Abao100% (2)

- Partnership DissolutionDocument3 pagesPartnership DissolutionRoselyn Balik100% (1)

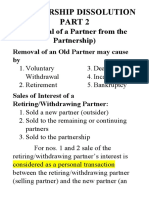

- Chapter 5 - Partnership Dissolution Part 2Document7 pagesChapter 5 - Partnership Dissolution Part 2Xyzra AlfonsoNo ratings yet

- Actpaco ReviewerDocument49 pagesActpaco ReviewerMark Steven Pempengco100% (1)

- Additional Equity TransactionsDocument37 pagesAdditional Equity TransactionsJulius B. OpriasaNo ratings yet

- PED2 Accomplishment Report AR 22 23Document3 pagesPED2 Accomplishment Report AR 22 23ZAIL JEFF ALDEA DALENo ratings yet

- Module 2 - Quiz To Give 03.06.23-1Document1 pageModule 2 - Quiz To Give 03.06.23-1ZAIL JEFF ALDEA DALENo ratings yet

- Nego EvaluateDocument9 pagesNego EvaluateZAIL JEFF ALDEA DALENo ratings yet

- PCOM Manual (Mid)Document50 pagesPCOM Manual (Mid)ZAIL JEFF ALDEA DALENo ratings yet

- UntitledDocument7 pagesUntitledZAIL JEFF ALDEA DALENo ratings yet

- University of St. La Salle Class ListDocument2 pagesUniversity of St. La Salle Class ListZAIL JEFF ALDEA DALENo ratings yet

- Exercises On Partnership Dissolution 03.20.23Document4 pagesExercises On Partnership Dissolution 03.20.23ZAIL JEFF ALDEA DALENo ratings yet

- 02 Lesson 2 - Partnership Operations and Financial ReportingDocument12 pages02 Lesson 2 - Partnership Operations and Financial ReportingZAIL JEFF ALDEA DALENo ratings yet

- Mod 1 FullDocument42 pagesMod 1 FullZAIL JEFF ALDEA DALENo ratings yet

- Module 3 - Quiz 03.22.23 SolutionsDocument2 pagesModule 3 - Quiz 03.22.23 SolutionsZAIL JEFF ALDEA DALENo ratings yet

- Nicor Final Merit and Cover Application2Document11 pagesNicor Final Merit and Cover Application2ZAIL JEFF ALDEA DALENo ratings yet

- The History of My NameDocument1 pageThe History of My NameZAIL JEFF ALDEA DALENo ratings yet

- ACCTG. 101 End - Term ExaminationDocument9 pagesACCTG. 101 End - Term ExaminationZAIL JEFF ALDEA DALENo ratings yet

- Tocap 986Document6 pagesTocap 986ZAIL JEFF ALDEA DALENo ratings yet

- Conversion StoryDocument1 pageConversion StoryZAIL JEFF ALDEA DALENo ratings yet

- Reed QuizDocument2 pagesReed QuizZAIL JEFF ALDEA DALENo ratings yet

- Acctng ReviewerDocument7 pagesAcctng ReviewerZAIL JEFF ALDEA DALENo ratings yet

- Albert EinsteinDocument21 pagesAlbert EinsteinZAIL JEFF ALDEA DALENo ratings yet

- 4.3.1 Lesson. Globalization and MediaDocument25 pages4.3.1 Lesson. Globalization and MediaZAIL JEFF ALDEA DALENo ratings yet

- Notes For Readings in Phil. HistoryDocument6 pagesNotes For Readings in Phil. HistoryZAIL JEFF ALDEA DALENo ratings yet

- Case On GridcoDocument4 pagesCase On Gridcoshahriar62No ratings yet

- Wealth Insight - May 2023Document76 pagesWealth Insight - May 2023Santosh Tiwari100% (1)

- Investor Pitch Deck TemplateDocument17 pagesInvestor Pitch Deck Templateakashprasad0205No ratings yet

- Capital StructureDocument42 pagesCapital Structurevarsha raichalNo ratings yet

- 1 - The Investment SettingDocument48 pages1 - The Investment SettingYash Raj SinghNo ratings yet

- Sip Proposal ReportDocument1 pageSip Proposal ReportRitika PaulNo ratings yet

- Overconfidence and Investment Decisions in Nepalese Stock MarketDocument10 pagesOverconfidence and Investment Decisions in Nepalese Stock MarketMgc RyustailbNo ratings yet

- Bharti Airtel Strategy FinalDocument39 pagesBharti Airtel Strategy FinalniksforloveuNo ratings yet

- Semester V and VIDocument30 pagesSemester V and VIsushantpanigrahiNo ratings yet

- JERNEH-AnnualReport2009 (838KB)Document100 pagesJERNEH-AnnualReport2009 (838KB)Ooi Beng Hooi 黄明辉No ratings yet

- Financial Accounting and Reporting - 399Document37 pagesFinancial Accounting and Reporting - 399Jenny LinNo ratings yet

- China Economy: China's Economic Profile, The Chinese Economy, Economy of ChinaDocument33 pagesChina Economy: China's Economic Profile, The Chinese Economy, Economy of Chinahiral124No ratings yet

- FAR Noel B. Summary of Lectures With PWDDocument4 pagesFAR Noel B. Summary of Lectures With PWDFatima AndresNo ratings yet

- Unlucky Strike Gold and Labor in Zaruma Ecuador 1699 1820Document21 pagesUnlucky Strike Gold and Labor in Zaruma Ecuador 1699 1820albaslm7512No ratings yet

- Global Tactical Asset Allocation (Goldmann Sachs)Document12 pagesGlobal Tactical Asset Allocation (Goldmann Sachs)Marc GrisNo ratings yet

- Axis Mutual Fund Project ReportDocument37 pagesAxis Mutual Fund Project ReportVikas PabaleNo ratings yet

- Risk Management Final AssignmentDocument20 pagesRisk Management Final AssignmentJean-Yves Nguini EffaNo ratings yet

- F3 - Accounting StandardsDocument6 pagesF3 - Accounting Standardsnoor ul anumNo ratings yet

- Mediator's Memorandum LightSquared CaseDocument22 pagesMediator's Memorandum LightSquared CaseDealBookNo ratings yet

- July 15, 2020 - Investor Day Slide PresentationDocument21 pagesJuly 15, 2020 - Investor Day Slide Presentationbillroberts981No ratings yet

- Presented by Anmoldeep Anil Kumar Sanjay Singh Deepak Kumar Gursharan PreetDocument10 pagesPresented by Anmoldeep Anil Kumar Sanjay Singh Deepak Kumar Gursharan PreetRuchi GoenkaNo ratings yet

- Pure GoldDocument45 pagesPure GoldKevin Kim GutigulaoNo ratings yet

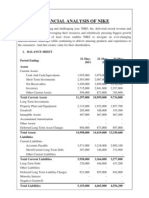

- Financial Analysis of NikeDocument5 pagesFinancial Analysis of NikenimmymathewpkkthlNo ratings yet

- Taxation Law Mock BarDocument8 pagesTaxation Law Mock BarKC ManglapusNo ratings yet

- 07 DCF Steel Dynamics AfterDocument2 pages07 DCF Steel Dynamics AfterJack JacintoNo ratings yet

- Risk Management Surveillance at Ludhiana Stock ExchangeDocument99 pagesRisk Management Surveillance at Ludhiana Stock Exchangepritpal singhNo ratings yet

- AfarDocument12 pagesAfarKris TineNo ratings yet

Download as pdf or txt

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- 4 - Lecture Notes - Partnership DissolutionDocument18 pages4 - Lecture Notes - Partnership DissolutionNikko Bowie PascualNo ratings yet

- Broidy Amended ComplaintDocument70 pagesBroidy Amended ComplaintLaw&Crime100% (1)

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- 4partnership DissolutionEDITED OnlineDocument15 pages4partnership DissolutionEDITED OnlinePaul BandolaNo ratings yet

- Partnership Formation Activity 2Document4 pagesPartnership Formation Activity 2Shaira Untalan100% (1)

- Partnership Dissolution - Practice ExercisesDocument5 pagesPartnership Dissolution - Practice ExercisesVon Andrei Medina0% (2)

- City of Bingham General Fund Post-Closing Trial Balance As of December 31, 2013 General LedgerDocument8 pagesCity of Bingham General Fund Post-Closing Trial Balance As of December 31, 2013 General LedgerHuma Bashir0% (1)

- Partnership DissolutionDocument21 pagesPartnership DissolutionmartgetaliaNo ratings yet

- Dissolution Is Defined in Article 1825 of The Civil Code of The Philippines As The Change in The RelationDocument18 pagesDissolution Is Defined in Article 1825 of The Civil Code of The Philippines As The Change in The RelationRae SlaughterNo ratings yet

- Chapter 4 DissolutionDocument24 pagesChapter 4 DissolutionJenny BernardinoNo ratings yet

- Partnership Dissolution - PART 1Document17 pagesPartnership Dissolution - PART 1Aby ReedNo ratings yet

- Partnership DissolutionDocument51 pagesPartnership DissolutionChelit LadylieGirl FernandezNo ratings yet

- PartnershipDocument12 pagesPartnershipMila aguasanNo ratings yet

- Accounting 112 C-3Document72 pagesAccounting 112 C-3Mark Erick Acojido RetonelNo ratings yet

- PartnershipDocument14 pagesPartnershipMila aguasanNo ratings yet

- 03 - Partnership DissolutionDocument38 pages03 - Partnership DissolutionDonise Ronadel SantosNo ratings yet

- Dissolution-Changes in OwnershipDocument72 pagesDissolution-Changes in OwnershipmonneNo ratings yet

- Partnership - DissolutionDocument51 pagesPartnership - DissolutionJulius B. OpriasaNo ratings yet

- Partnership Dissolution: Accounting For Special TransactionsDocument58 pagesPartnership Dissolution: Accounting For Special TransactionsjaneNo ratings yet

- 1 Lecture Notes DissolutionDocument17 pages1 Lecture Notes DissolutionMaybelle Espenido0% (2)

- Chapter 4 - Partnership DissolutionDocument15 pagesChapter 4 - Partnership DissolutionXyzra AlfonsoNo ratings yet

- Accounting Treatment of Goodwill at The Time of AdmissionDocument25 pagesAccounting Treatment of Goodwill at The Time of AdmissionMayurRawool100% (2)

- Partnership DissolutionDocument24 pagesPartnership Dissolutionmicaella pasionNo ratings yet

- Partnership Dissolution - DiscussionDocument5 pagesPartnership Dissolution - DiscussionIñego BegdorfNo ratings yet

- 1c Partnership DissolutionDocument9 pages1c Partnership DissolutionMark TaysonNo ratings yet

- Partnership Dissolution DiscussionDocument7 pagesPartnership Dissolution DiscussionDo RaemondNo ratings yet

- Accounting For Partnership DissolutionDocument19 pagesAccounting For Partnership DissolutionMelanie kaye ApostolNo ratings yet

- Acc 30 CorporationDocument8 pagesAcc 30 CorporationGerlie BonleonNo ratings yet

- C ACT100 1 Partnership DissolutionDocument25 pagesC ACT100 1 Partnership DissolutionvmargajavierNo ratings yet

- CMPC 131 3-Partnership-DissltnDocument13 pagesCMPC 131 3-Partnership-DissltnGab IgnacioNo ratings yet

- Dissolution - Changes in OwnershipDocument57 pagesDissolution - Changes in OwnershipJean Rae RemiasNo ratings yet

- PH Dissolution by InvestmentDocument12 pagesPH Dissolution by InvestmentREACTION COPNo ratings yet

- Chapter 2 Dissolution and Liquadation of PartnersipDocument17 pagesChapter 2 Dissolution and Liquadation of PartnersipTekaling NegashNo ratings yet

- Changes in Partnership Ownership Caused byDocument3 pagesChanges in Partnership Ownership Caused byKrizzia MayNo ratings yet

- Reviewer OverallDocument11 pagesReviewer OverallMah2SetNo ratings yet

- Partnership DissolutionDocument17 pagesPartnership DissolutionMich Salvatorē0% (1)

- MinggoyDocument12 pagesMinggoychantrealuna0No ratings yet

- Accounting (Reviewer)Document12 pagesAccounting (Reviewer)Marielle JalandoniNo ratings yet

- Chapter 3 Partnership DissolutionDocument32 pagesChapter 3 Partnership DissolutionmochiNo ratings yet

- DissolutionDocument25 pagesDissolutionallynelbarberNo ratings yet

- Module 3 - Partnership DissolutionDocument54 pagesModule 3 - Partnership DissolutionMaluDyNo ratings yet

- Partnership Dissolution: Prepared By: Cristopherson A. Perez, CPADocument59 pagesPartnership Dissolution: Prepared By: Cristopherson A. Perez, CPAKyla de SilvaNo ratings yet

- AFAR - Partnership DissolutionDocument36 pagesAFAR - Partnership DissolutionReginald ValenciaNo ratings yet

- Detailed Handouts in Partnership DissolutionDocument14 pagesDetailed Handouts in Partnership DissolutionVinz Ray PitargueNo ratings yet

- PARTNERSHIP2Document13 pagesPARTNERSHIP2Anne Marielle Uy0% (2)

- Iv: Accounting For Dissolution (Changes in Membership) of A PartnershipDocument18 pagesIv: Accounting For Dissolution (Changes in Membership) of A PartnershipBerhanu ShancoNo ratings yet

- PARTNERSHIP2Document13 pagesPARTNERSHIP2Anne Marielle UyNo ratings yet

- CMPC131Document15 pagesCMPC131Nhel AlvaroNo ratings yet

- DISSOLUTION - Changes in OwnershipDocument50 pagesDISSOLUTION - Changes in Ownershipmhel cabigonNo ratings yet

- Accounting For Shareholders Equity KINGDocument11 pagesAccounting For Shareholders Equity KINGAlexis KingNo ratings yet

- Partnership & Corporation: 2 SEMESTER 2020-2021Document13 pagesPartnership & Corporation: 2 SEMESTER 2020-2021Erika BucaoNo ratings yet

- Lect.7 Withdrawals of PatnerDocument20 pagesLect.7 Withdrawals of PatnerHany RagabNo ratings yet

- ACCTBA2 ReviewerDocument49 pagesACCTBA2 ReviewerBiean Abao100% (2)

- Partnership DissolutionDocument3 pagesPartnership DissolutionRoselyn Balik100% (1)

- Chapter 5 - Partnership Dissolution Part 2Document7 pagesChapter 5 - Partnership Dissolution Part 2Xyzra AlfonsoNo ratings yet

- Actpaco ReviewerDocument49 pagesActpaco ReviewerMark Steven Pempengco100% (1)

- Additional Equity TransactionsDocument37 pagesAdditional Equity TransactionsJulius B. OpriasaNo ratings yet

- PED2 Accomplishment Report AR 22 23Document3 pagesPED2 Accomplishment Report AR 22 23ZAIL JEFF ALDEA DALENo ratings yet

- Module 2 - Quiz To Give 03.06.23-1Document1 pageModule 2 - Quiz To Give 03.06.23-1ZAIL JEFF ALDEA DALENo ratings yet

- Nego EvaluateDocument9 pagesNego EvaluateZAIL JEFF ALDEA DALENo ratings yet

- PCOM Manual (Mid)Document50 pagesPCOM Manual (Mid)ZAIL JEFF ALDEA DALENo ratings yet

- UntitledDocument7 pagesUntitledZAIL JEFF ALDEA DALENo ratings yet

- University of St. La Salle Class ListDocument2 pagesUniversity of St. La Salle Class ListZAIL JEFF ALDEA DALENo ratings yet

- Exercises On Partnership Dissolution 03.20.23Document4 pagesExercises On Partnership Dissolution 03.20.23ZAIL JEFF ALDEA DALENo ratings yet

- 02 Lesson 2 - Partnership Operations and Financial ReportingDocument12 pages02 Lesson 2 - Partnership Operations and Financial ReportingZAIL JEFF ALDEA DALENo ratings yet

- Mod 1 FullDocument42 pagesMod 1 FullZAIL JEFF ALDEA DALENo ratings yet

- Module 3 - Quiz 03.22.23 SolutionsDocument2 pagesModule 3 - Quiz 03.22.23 SolutionsZAIL JEFF ALDEA DALENo ratings yet

- Nicor Final Merit and Cover Application2Document11 pagesNicor Final Merit and Cover Application2ZAIL JEFF ALDEA DALENo ratings yet

- The History of My NameDocument1 pageThe History of My NameZAIL JEFF ALDEA DALENo ratings yet

- ACCTG. 101 End - Term ExaminationDocument9 pagesACCTG. 101 End - Term ExaminationZAIL JEFF ALDEA DALENo ratings yet

- Tocap 986Document6 pagesTocap 986ZAIL JEFF ALDEA DALENo ratings yet

- Conversion StoryDocument1 pageConversion StoryZAIL JEFF ALDEA DALENo ratings yet

- Reed QuizDocument2 pagesReed QuizZAIL JEFF ALDEA DALENo ratings yet

- Acctng ReviewerDocument7 pagesAcctng ReviewerZAIL JEFF ALDEA DALENo ratings yet

- Albert EinsteinDocument21 pagesAlbert EinsteinZAIL JEFF ALDEA DALENo ratings yet

- 4.3.1 Lesson. Globalization and MediaDocument25 pages4.3.1 Lesson. Globalization and MediaZAIL JEFF ALDEA DALENo ratings yet

- Notes For Readings in Phil. HistoryDocument6 pagesNotes For Readings in Phil. HistoryZAIL JEFF ALDEA DALENo ratings yet

- Case On GridcoDocument4 pagesCase On Gridcoshahriar62No ratings yet

- Wealth Insight - May 2023Document76 pagesWealth Insight - May 2023Santosh Tiwari100% (1)

- Investor Pitch Deck TemplateDocument17 pagesInvestor Pitch Deck Templateakashprasad0205No ratings yet

- Capital StructureDocument42 pagesCapital Structurevarsha raichalNo ratings yet

- 1 - The Investment SettingDocument48 pages1 - The Investment SettingYash Raj SinghNo ratings yet

- Sip Proposal ReportDocument1 pageSip Proposal ReportRitika PaulNo ratings yet

- Overconfidence and Investment Decisions in Nepalese Stock MarketDocument10 pagesOverconfidence and Investment Decisions in Nepalese Stock MarketMgc RyustailbNo ratings yet

- Bharti Airtel Strategy FinalDocument39 pagesBharti Airtel Strategy FinalniksforloveuNo ratings yet

- Semester V and VIDocument30 pagesSemester V and VIsushantpanigrahiNo ratings yet

- JERNEH-AnnualReport2009 (838KB)Document100 pagesJERNEH-AnnualReport2009 (838KB)Ooi Beng Hooi 黄明辉No ratings yet

- Financial Accounting and Reporting - 399Document37 pagesFinancial Accounting and Reporting - 399Jenny LinNo ratings yet

- China Economy: China's Economic Profile, The Chinese Economy, Economy of ChinaDocument33 pagesChina Economy: China's Economic Profile, The Chinese Economy, Economy of Chinahiral124No ratings yet

- FAR Noel B. Summary of Lectures With PWDDocument4 pagesFAR Noel B. Summary of Lectures With PWDFatima AndresNo ratings yet

- Unlucky Strike Gold and Labor in Zaruma Ecuador 1699 1820Document21 pagesUnlucky Strike Gold and Labor in Zaruma Ecuador 1699 1820albaslm7512No ratings yet

- Global Tactical Asset Allocation (Goldmann Sachs)Document12 pagesGlobal Tactical Asset Allocation (Goldmann Sachs)Marc GrisNo ratings yet

- Axis Mutual Fund Project ReportDocument37 pagesAxis Mutual Fund Project ReportVikas PabaleNo ratings yet

- Risk Management Final AssignmentDocument20 pagesRisk Management Final AssignmentJean-Yves Nguini EffaNo ratings yet

- F3 - Accounting StandardsDocument6 pagesF3 - Accounting Standardsnoor ul anumNo ratings yet

- Mediator's Memorandum LightSquared CaseDocument22 pagesMediator's Memorandum LightSquared CaseDealBookNo ratings yet

- July 15, 2020 - Investor Day Slide PresentationDocument21 pagesJuly 15, 2020 - Investor Day Slide Presentationbillroberts981No ratings yet

- Presented by Anmoldeep Anil Kumar Sanjay Singh Deepak Kumar Gursharan PreetDocument10 pagesPresented by Anmoldeep Anil Kumar Sanjay Singh Deepak Kumar Gursharan PreetRuchi GoenkaNo ratings yet

- Pure GoldDocument45 pagesPure GoldKevin Kim GutigulaoNo ratings yet

- Financial Analysis of NikeDocument5 pagesFinancial Analysis of NikenimmymathewpkkthlNo ratings yet

- Taxation Law Mock BarDocument8 pagesTaxation Law Mock BarKC ManglapusNo ratings yet

- 07 DCF Steel Dynamics AfterDocument2 pages07 DCF Steel Dynamics AfterJack JacintoNo ratings yet

- Risk Management Surveillance at Ludhiana Stock ExchangeDocument99 pagesRisk Management Surveillance at Ludhiana Stock Exchangepritpal singhNo ratings yet

- AfarDocument12 pagesAfarKris TineNo ratings yet