Download as docx, pdf, or txt

You might also like

- JSSSEH Implementation Guide 20028 - SmithDocument22 pagesJSSSEH Implementation Guide 20028 - Smith135 cashewNo ratings yet

- Columbia Corporation A U S Based Company Acquired A 100 Percent InterestDocument2 pagesColumbia Corporation A U S Based Company Acquired A 100 Percent InterestTaimour Hassan0% (1)

- LiabilitiesDocument4 pagesLiabilitiesarkishaNo ratings yet

- Intention To Acquire Goods in The FutureDocument21 pagesIntention To Acquire Goods in The Futurecynthia reyesNo ratings yet

- Intermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesDocument7 pagesIntermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesdeeznutsNo ratings yet

- Intermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesDocument7 pagesIntermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesdeeznutsNo ratings yet

- Chapter 1 Current LiabilitiesDocument48 pagesChapter 1 Current LiabilitiesNeighvest100% (1)

- LIABILITIESDocument12 pagesLIABILITIESJOHANNANo ratings yet

- Present ObligationDocument6 pagesPresent ObligationArgem Jay PorioNo ratings yet

- Definition Explained:: Liabilities A Liability Is ADocument26 pagesDefinition Explained:: Liabilities A Liability Is ACurtain SoenNo ratings yet

- Ia2 ReviewerDocument7 pagesIa2 ReviewerAiden MagnoNo ratings yet

- Aks 2023 - 2024 - Far 4 - Day 1Document8 pagesAks 2023 - 2024 - Far 4 - Day 1John Carl TuazonNo ratings yet

- Chapter 13 Theory Notes: LO1: Understanding LiabilitiesDocument8 pagesChapter 13 Theory Notes: LO1: Understanding LiabilitiesOmar MetwaliNo ratings yet

- Questions 14,54,81, and 114Document5 pagesQuestions 14,54,81, and 114Damian Sheila MaeNo ratings yet

- Learning Material 1Document7 pagesLearning Material 1salduaerossjacobNo ratings yet

- Module 1-LIABILITIES and PREMIUM LIABILITYDocument10 pagesModule 1-LIABILITIES and PREMIUM LIABILITYKathleen SalesNo ratings yet

- SUMMARY For INTERMEDIATE ACCOUNTING 2 PDFDocument20 pagesSUMMARY For INTERMEDIATE ACCOUNTING 2 PDFArtisan100% (1)

- Chapter 1 Liabilities PDFDocument9 pagesChapter 1 Liabilities PDFKesiah FortunaNo ratings yet

- Liabilities by Valix: Intermediate Accounting 2Document34 pagesLiabilities by Valix: Intermediate Accounting 2Trisha Mae AlburoNo ratings yet

- Current LiabilitiesDocument87 pagesCurrent LiabilitiestheheckwithitNo ratings yet

- Midterm NotesDocument11 pagesMidterm NotesLauNo ratings yet

- Pas 32, Pas 12 & Pas 33Document7 pagesPas 32, Pas 12 & Pas 33Olive Jean TiuNo ratings yet

- LiabilitiesDocument4 pagesLiabilitiesreymonastrera07No ratings yet

- Ms. Sharon A. Bactat Prof. Suerte R. Dy: Sabactat@mmsu - Edu.ph Srdy@mmsu - Edu.phDocument26 pagesMs. Sharon A. Bactat Prof. Suerte R. Dy: Sabactat@mmsu - Edu.ph Srdy@mmsu - Edu.phCrisangel de LeonNo ratings yet

- To Discourage Fraud and Manipulation of Accounts. Dr. Purchases To Record Purchase of Inventory Through VoucherDocument3 pagesTo Discourage Fraud and Manipulation of Accounts. Dr. Purchases To Record Purchase of Inventory Through VoucherkimNo ratings yet

- Intermediate CH 1Document15 pagesIntermediate CH 1Abdi MohamedNo ratings yet

- ReceivablesDocument3 pagesReceivablesashegemedeNo ratings yet

- Intermediate Accounting 2 - CL NCL Lecture NotesDocument2 pagesIntermediate Accounting 2 - CL NCL Lecture NotesRacheel SollezaNo ratings yet

- Chapter 13 Lecture Notes (TA 2020) - Non-Financial and Current LiabilitiesDocument20 pagesChapter 13 Lecture Notes (TA 2020) - Non-Financial and Current LiabilitiesTSEvansNo ratings yet

- L03-Ias 37Document48 pagesL03-Ias 37Mohamed IyaanNo ratings yet

- Week 9 - Analysis of Financing Liabilities & Off-Balance Sheet DebtDocument13 pagesWeek 9 - Analysis of Financing Liabilities & Off-Balance Sheet DebtJarida La UongoNo ratings yet

- GfewgakjbdDocument23 pagesGfewgakjbdJenilyn CalaraNo ratings yet

- College of Business and Accountancy: Obligating EventDocument4 pagesCollege of Business and Accountancy: Obligating EventAnthony DyNo ratings yet

- Module 1 Current LiabilitiesDocument13 pagesModule 1 Current LiabilitiesLea Yvette SaladinoNo ratings yet

- Unit A 1Document12 pagesUnit A 1Karl Lincoln TemporosaNo ratings yet

- Liabilities NotesDocument15 pagesLiabilities NotesFarah PatelNo ratings yet

- Chapter 1 LiabilitiesDocument16 pagesChapter 1 LiabilitiesAlvin Dantes100% (1)

- 1 Introduction To LiabilitiesDocument18 pages1 Introduction To LiabilitiesLhea VillanuevaNo ratings yet

- Current Liabilities - Revised (Warranties)Document14 pagesCurrent Liabilities - Revised (Warranties)Jerome_JadeNo ratings yet

- Ias 37 Provision and Contingencies-2Document9 pagesIas 37 Provision and Contingencies-2Darren PeñaredondoNo ratings yet

- ACTGIA2 - CH01 2 3 4 - Liabilities Etc.Document44 pagesACTGIA2 - CH01 2 3 4 - Liabilities Etc.chingNo ratings yet

- Introduction To LiabilitiesDocument16 pagesIntroduction To LiabilitiesAllene MontemayorNo ratings yet

- ULOa. Liabilities - 0Document8 pagesULOa. Liabilities - 0pam pamNo ratings yet

- Cape Accounting Unit 1 NotesDocument27 pagesCape Accounting Unit 1 NotesDajueNo ratings yet

- Definition and Nature of LiabilitiesDocument6 pagesDefinition and Nature of LiabilitiesRizza Mae BondocNo ratings yet

- Current LiabilitiesDocument14 pagesCurrent LiabilitiesESTRADA, Angelica T.No ratings yet

- Liabilities Technical Knowledge: Lesson 1Document12 pagesLiabilities Technical Knowledge: Lesson 1Cirelle Faye SilvaNo ratings yet

- Section 11Document30 pagesSection 11Abata BageyuNo ratings yet

- Chapter 1 LiabilitiesDocument7 pagesChapter 1 LiabilitiesVirgilio EvangelistaNo ratings yet

- (Liabilities) : Lecture AidDocument20 pages(Liabilities) : Lecture Aidmabel fernandezNo ratings yet

- Learning Resource 1 Lesson 1Document11 pagesLearning Resource 1 Lesson 1Novylyn AldaveNo ratings yet

- Intermediate Accounting ReviewerDocument5 pagesIntermediate Accounting ReviewerBroniNo ratings yet

- Ia 2 - ReviewerDocument3 pagesIa 2 - ReviewerCenelyn PajarillaNo ratings yet

- Ias 32Document24 pagesIas 32fadfadiNo ratings yet

- FAR Financial Liabilities BERNARTE ReviewerDocument5 pagesFAR Financial Liabilities BERNARTE ReviewerMarjorie AugustoNo ratings yet

- Discussion TaDocument23 pagesDiscussion TaRatih Kusuma Dewi IINo ratings yet

- The Balance Sheet, L+EDocument13 pagesThe Balance Sheet, L+EPao VuochneaNo ratings yet

- Module 11 Current Liabilities Provisions and ContingenciesDocument14 pagesModule 11 Current Liabilities Provisions and ContingenciesZyril RamosNo ratings yet

- LESSON 1 Introduction To LiabilityDocument3 pagesLESSON 1 Introduction To LiabilityMONDIDO RONALYN M.No ratings yet

- Current Liabilities and ProvisionsDocument12 pagesCurrent Liabilities and ProvisionsRinkashizu TokimimotakuNo ratings yet

- AttachmentDocument11 pagesAttachmentRegasa GutemaNo ratings yet

- RRLDocument1 pageRRLAngelica MaeNo ratings yet

- Constructive SpeechDocument2 pagesConstructive SpeechAngelica MaeNo ratings yet

- UntitledDocument1 pageUntitledAngelica MaeNo ratings yet

- Milf Stands For? Moro Islamic Liberation Front 8. How Many Elite Cops Were Killed During Mamasapano Clash? 67Document2 pagesMilf Stands For? Moro Islamic Liberation Front 8. How Many Elite Cops Were Killed During Mamasapano Clash? 67Angelica MaeNo ratings yet

- Activity in PHILIPPINE LITERATUREDocument2 pagesActivity in PHILIPPINE LITERATUREAngelica MaeNo ratings yet

- Decision Support SystemDocument12 pagesDecision Support SystemAngelica MaeNo ratings yet

- Managerial Economics Chapter 7-8 ActivitiesDocument4 pagesManagerial Economics Chapter 7-8 ActivitiesAngelica MaeNo ratings yet

- PAS PresentationDocument13 pagesPAS PresentationAngelica MaeNo ratings yet

- Demand SupplyDocument63 pagesDemand SupplyAngelica MaeNo ratings yet

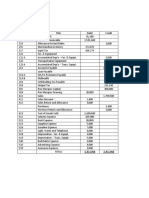

- Trial Balance February 28, 20X1Document3 pagesTrial Balance February 28, 20X1Angelica MaeNo ratings yet

- Chick Literature: Binmaley Catholic School Binmaley, PangasinanDocument5 pagesChick Literature: Binmaley Catholic School Binmaley, PangasinanAngelica MaeNo ratings yet

- Physical Education 1 Handout PrelimDocument4 pagesPhysical Education 1 Handout PrelimAngelica MaeNo ratings yet

- Primary School Net and Gross Attendance Rates, PhilippinesDocument5 pagesPrimary School Net and Gross Attendance Rates, PhilippinesAngelica MaeNo ratings yet

- VenndiagrampracticeanswersDocument2 pagesVenndiagrampracticeanswersAngelica MaeNo ratings yet

- Unpacking The SelfDocument13 pagesUnpacking The SelfAngelica MaeNo ratings yet

- TLA 3mmwDocument3 pagesTLA 3mmwAngelica MaeNo ratings yet

- Applied Economics: Quarter 3 - Module 3Document27 pagesApplied Economics: Quarter 3 - Module 3Johneen DungqueNo ratings yet

- Solution Manual For A First Course in Differential Equations With Modeling Applications 10th EditionDocument23 pagesSolution Manual For A First Course in Differential Equations With Modeling Applications 10th Editiondisbenchcrang9xds100% (45)

- 2023 SDF Budget PlannerDocument44 pages2023 SDF Budget PlannerJoyce D. FernandezNo ratings yet

- SGC ConstitutionDocument11 pagesSGC ConstitutionRaulJunioRamos100% (1)

- Global e MarketingDocument13 pagesGlobal e MarketingSharan BiradarNo ratings yet

- List of Approved Virtual Trade Fairs by Enterprise SingaporeDocument2 pagesList of Approved Virtual Trade Fairs by Enterprise Singaporetantra shivaNo ratings yet

- ANS AlagangWency-2nd-quizDocument13 pagesANS AlagangWency-2nd-quizJazzy MercadoNo ratings yet

- The Rational Unified ProcessDocument34 pagesThe Rational Unified ProcessZona TecnológicaNo ratings yet

- Unique Skills For ResumeDocument5 pagesUnique Skills For Resumeebqlsqekg100% (1)

- Data Architecture-ACNDocument5 pagesData Architecture-ACNimanonNo ratings yet

- Ryan, 2021Document449 pagesRyan, 2021Solav Ezzaaldeen Saeed Dalo100% (2)

- DEP 38.80.30.32-Gen Inspection, Maintenance, Repair and Remanufacture of Hoisting Equipment (Endorsement of ISO 13534)Document7 pagesDEP 38.80.30.32-Gen Inspection, Maintenance, Repair and Remanufacture of Hoisting Equipment (Endorsement of ISO 13534)Sd MahmoodNo ratings yet

- Company Management: Shruti Reddy, Upes SolDocument72 pagesCompany Management: Shruti Reddy, Upes Solvishal bagariaNo ratings yet

- Connected Manufacturing RoadmapDocument41 pagesConnected Manufacturing RoadmapAnnirban BhattacharyaNo ratings yet

- Advocacy On Anti Investment Scams ADZU 2022Document29 pagesAdvocacy On Anti Investment Scams ADZU 2022Ridz TingkahanNo ratings yet

- The Six Steps of Data AnalysisDocument4 pagesThe Six Steps of Data AnalysisGRUPOPOSITIVO POSITIVONo ratings yet

- Developing Sustainable Tourism Product For Sailing Sapa Homestay - Rational ReportDocument73 pagesDeveloping Sustainable Tourism Product For Sailing Sapa Homestay - Rational ReportQTKD 4D-18 Vuong Thuy TrangNo ratings yet

- Report On Tyres Sector by PACRADocument31 pagesReport On Tyres Sector by PACRAKhuram KhanNo ratings yet

- Question Paper - Mock AristoDocument33 pagesQuestion Paper - Mock AristoTONI POOH100% (1)

- Belt Conveyors For Bulk Materials Conveyor: Traducir Esta PáginaDocument4 pagesBelt Conveyors For Bulk Materials Conveyor: Traducir Esta PáginaDIEGO FERNANDO CADENA ARANGONo ratings yet

- Thales Accelerate Not For Resale (NFR) Program For AMER and EMEADocument2 pagesThales Accelerate Not For Resale (NFR) Program For AMER and EMEAFREDDYMENANo ratings yet

- Case Study Champions League FinalDocument14 pagesCase Study Champions League FinalRakeem DavidsonNo ratings yet

- Solved ProblemDocument4 pagesSolved ProblemSophiya NeupaneNo ratings yet

- Ids PDFDocument397 pagesIds PDFMinh Ngô HảiNo ratings yet

- Public Sector Economics Test QuestionsDocument9 pagesPublic Sector Economics Test QuestionsAbdul Hakim MambuayNo ratings yet

- MS Adj 001Document1 pageMS Adj 001Manish ChandNo ratings yet

- Gartner's Hype Cycle For BlockchainDocument3 pagesGartner's Hype Cycle For BlockchainLionelPintoNo ratings yet

- Form 4: Pegram Michael E Caesars Entertainment, IncDocument1 pageForm 4: Pegram Michael E Caesars Entertainment, IncVanessa chagasNo ratings yet