Download as pdf or txt

You might also like

- Deed of Undertaking (For Borrower/s With Documentary Deficiency/ies)Document1 pageDeed of Undertaking (For Borrower/s With Documentary Deficiency/ies)Loren Salanguit100% (2)

- PNB Loan Interest Rate 04 - 08 - 2021Document9 pagesPNB Loan Interest Rate 04 - 08 - 2021Somasundaram MuthiahNo ratings yet

- RLLR SchemeDocument1 pageRLLR SchemeBhushan Singh BadgujjarNo ratings yet

- Bank Loan OffersDocument11 pagesBank Loan OffersAnandNo ratings yet

- ROI OnretaillendingschemesDocument8 pagesROI Onretaillendingschemespassword123resetNo ratings yet

- Rate of InterestDocument9 pagesRate of InterestUdaydeep SinghNo ratings yet

- RBI Format ROI PCDocument6 pagesRBI Format ROI PCSandesh ManeNo ratings yet

- Updated Roi 15.05.2024 To 30.06.2024Document1 pageUpdated Roi 15.05.2024 To 30.06.2024Divya MaheshNo ratings yet

- Green Veh OnepagerDocument2 pagesGreen Veh OnepagerRohith RaoNo ratings yet

- Dena Niwas Housing Loan: (To Be Reset at The End of Every 3 Years)Document24 pagesDena Niwas Housing Loan: (To Be Reset at The End of Every 3 Years)asdNo ratings yet

- RBI ROI FormatDocument11 pagesRBI ROI FormatDevender RajuNo ratings yet

- RBI ROI FormatDocument8 pagesRBI ROI Formatsrinivas.rmbaNo ratings yet

- RBI ROI FormatDocument11 pagesRBI ROI FormatSandeep SandyNo ratings yet

- RBI Format ROI PCDocument8 pagesRBI Format ROI PCom vermaNo ratings yet

- Applicable For Pcc/Ipcc May-2010/Nov-2010Document17 pagesApplicable For Pcc/Ipcc May-2010/Nov-2010Anshul AgarwalNo ratings yet

- RBI Format ROI PC PDFDocument9 pagesRBI Format ROI PC PDFmohana sundaram pNo ratings yet

- Income Tax Card 2023-24 (Finance Act 2023)Document1 pageIncome Tax Card 2023-24 (Finance Act 2023)shahidNo ratings yet

- ROI @ 8.40%Document1 pageROI @ 8.40%hetalkarliNo ratings yet

- Educative Series LAPDocument2 pagesEducative Series LAPRohith RaoNo ratings yet

- NRI News Letter From SBI Thiruvananthapuram Circle : E Turning Indian TaxationDocument7 pagesNRI News Letter From SBI Thiruvananthapuram Circle : E Turning Indian TaxationSherinWorinNo ratings yet

- Msme Working Capital LoansDocument1 pageMsme Working Capital Loansitisthatis65No ratings yet

- Maha Super Housing Loan: Rate of Interest : Starting From 8.00%, Linked With Cibil ScoreDocument2 pagesMaha Super Housing Loan: Rate of Interest : Starting From 8.00%, Linked With Cibil ScoreRohith RaoNo ratings yet

- RBI - ROI FormatDocument9 pagesRBI - ROI Formatranajoy biswasNo ratings yet

- EBLR As On 01.04.2020 Is 7.20 % I.E. RBI Repo Rate (4.40%) + Spread (2.80%)Document6 pagesEBLR As On 01.04.2020 Is 7.20 % I.E. RBI Repo Rate (4.40%) + Spread (2.80%)Atul GuptaNo ratings yet

- ROI OnretaillendingschemesDocument8 pagesROI OnretaillendingschemesSaran ManiNo ratings yet

- 2 Tax RatesDocument15 pages2 Tax RatesragerahulNo ratings yet

- Dexter Consultants: Updated Through Finance Act 2022Document1 pageDexter Consultants: Updated Through Finance Act 2022fahid aslamNo ratings yet

- Msme Loan - Upto 2lakhs: NF-546 NF-998 NF-588 NF-855 NF-803 NF-482 NF-373 NF-368Document4 pagesMsme Loan - Upto 2lakhs: NF-546 NF-998 NF-588 NF-855 NF-803 NF-482 NF-373 NF-368Santosh KumarNo ratings yet

- Rate of Interest and Charges Applicable To Micro & Small Enterprises (Mses) Covered Under Priority SectorDocument2 pagesRate of Interest and Charges Applicable To Micro & Small Enterprises (Mses) Covered Under Priority SectorAjoydeep DasNo ratings yet

- Income Tax CircularDocument6 pagesIncome Tax Circularu19n6735No ratings yet

- Rbi Format Roi PCDocument10 pagesRbi Format Roi PCsriramNo ratings yet

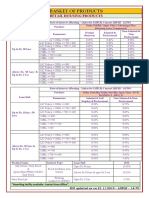

- BASKET OF PRODUCTS As On 21.11.19Document3 pagesBASKET OF PRODUCTS As On 21.11.19Virendra K VermaNo ratings yet

- Administrative Office: ' Mahaveer ', Shree Shahu Market Yard, Kolhapur - 416 008Document3 pagesAdministrative Office: ' Mahaveer ', Shree Shahu Market Yard, Kolhapur - 416 008gmatweakNo ratings yet

- Retail Rate of Interest Updated 15122022Document10 pagesRetail Rate of Interest Updated 15122022srikarNo ratings yet

- Retail Rate of Interest Updated 10012023Document10 pagesRetail Rate of Interest Updated 10012023monty chikNo ratings yet

- P Seg Interest Rate From 15.12.2022Document2 pagesP Seg Interest Rate From 15.12.2022amitNo ratings yet

- ROI OnretaillendingschemesDocument9 pagesROI OnretaillendingschemesFayaz ShaikNo ratings yet

- New Tax Regime Vs Old Calculator by AssetYogiDocument4 pagesNew Tax Regime Vs Old Calculator by AssetYogijohnNo ratings yet

- Tax Rates For Non-Salaried Individuals and AopsDocument4 pagesTax Rates For Non-Salaried Individuals and AopsAdeel QaiserNo ratings yet

- Revision of Service Charges Wef 01042023Document53 pagesRevision of Service Charges Wef 01042023kkrandy01No ratings yet

- Salary Tax Rates (2022 & 2023 Comparison)Document2 pagesSalary Tax Rates (2022 & 2023 Comparison)by kirmaniNo ratings yet

- New Tax Regime Vs Old Calculator - by AssetYogiDocument7 pagesNew Tax Regime Vs Old Calculator - by AssetYogiGajendra HoleNo ratings yet

- About LichflDocument17 pagesAbout LichflHyma KavyaNo ratings yet

- Amendment To Service Provider Agreement 1Document3 pagesAmendment To Service Provider Agreement 1myloan partnerNo ratings yet

- RBI Format ROI PDocument8 pagesRBI Format ROI PSrikanth ReddyNo ratings yet

- The Jammu & Kashmir Bank LTD: AccountDocument5 pagesThe Jammu & Kashmir Bank LTD: AccountĒxçlūsìvē SympãthētìçNo ratings yet

- New Tax Regime Vs Old Calculator by AssetYogiDocument3 pagesNew Tax Regime Vs Old Calculator by AssetYogiSukanta MondalNo ratings yet

- SALIENT FEATURES 2025 ActDocument6 pagesSALIENT FEATURES 2025 ActnaveedNo ratings yet

- 9114 Accts-SERVICE CHARGhjgjgnj)Document5 pages9114 Accts-SERVICE CHARGhjgjgnj)Girish KumarNo ratings yet

- January ExpatDocument5 pagesJanuary ExpatjawadkaNo ratings yet

- Latepayment BFL 1222Document1 pageLatepayment BFL 1222Junaid ShaikNo ratings yet

- Tax Sheet - A.Y 2024-25Document3 pagesTax Sheet - A.Y 2024-25bajajvanshica23No ratings yet

- Retail Rate of Interest Updated 07 09 2023Document9 pagesRetail Rate of Interest Updated 07 09 2023vikaspabuwalNo ratings yet

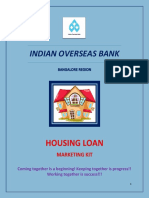

- Housing Loan - Marketing KitDocument15 pagesHousing Loan - Marketing Kitsanty86No ratings yet

- Loan Guideline and DetailDocument1 pageLoan Guideline and DetailIbu SiddiqNo ratings yet

- SOC AssetsDocument2 pagesSOC AssetsptsmithrafoundationNo ratings yet

- Llpa-Matrix Updated 05-17-23Document9 pagesLlpa-Matrix Updated 05-17-23David GNo ratings yet

- Finshots Calculator For Tax RegimeDocument6 pagesFinshots Calculator For Tax RegimeSantosh mudaliarNo ratings yet

- IncomDocument48 pagesIncomMahendra BabuNo ratings yet

- Revision of Interest Rate On Domestic, NRO and NRE Term DepositsDocument2 pagesRevision of Interest Rate On Domestic, NRO and NRE Term DepositsTnaharNo ratings yet

- How to Reverse Recession and Remove Poverty in India: Prove Me Wrong & Win 10 Million Dollar Challenge Within 60 DaysFrom EverandHow to Reverse Recession and Remove Poverty in India: Prove Me Wrong & Win 10 Million Dollar Challenge Within 60 DaysNo ratings yet

- Green Veh OnepagerDocument2 pagesGreen Veh OnepagerRohith RaoNo ratings yet

- Admit Letter For Online CAIIB Electives - June 2023 Candidate DetailsDocument4 pagesAdmit Letter For Online CAIIB Electives - June 2023 Candidate DetailsRohith RaoNo ratings yet

- Maha Super Housing Loan: Rate of Interest : Starting From 8.00%, Linked With Cibil ScoreDocument2 pagesMaha Super Housing Loan: Rate of Interest : Starting From 8.00%, Linked With Cibil ScoreRohith RaoNo ratings yet

- UntitledDocument34 pagesUntitledRohith RaoNo ratings yet

- Educative Series LAPDocument2 pagesEducative Series LAPRohith RaoNo ratings yet

- Dates: For Students To Update Book ChaptersDocument4 pagesDates: For Students To Update Book ChaptersRohith RaoNo ratings yet

- Educative Series Gold LoanDocument2 pagesEducative Series Gold LoanRohith RaoNo ratings yet

- Question #1 of 7: ExplanationDocument74 pagesQuestion #1 of 7: ExplanationRohith RaoNo ratings yet

- मानव संसाधन प्रबंधन ववभाग Human Resources Management Department १५०१ - ५Document2 pagesमानव संसाधन प्रबंधन ववभाग Human Resources Management Department १५०१ - ५Rohith RaoNo ratings yet

- 5e Tox-QuizDocument3 pages5e Tox-QuizRohith RaoNo ratings yet

- BOM-Pre-promotion Digital Training Program - Reading MaterialDocument486 pagesBOM-Pre-promotion Digital Training Program - Reading MaterialRohith RaoNo ratings yet

- Institute of Banking Personnel Selection: 320134 E-Receipt (Candidate'S Copy)Document1 pageInstitute of Banking Personnel Selection: 320134 E-Receipt (Candidate'S Copy)Rohith RaoNo ratings yet

- Admit Letter For Online JAIIB Examination - Jan 2022 Candidate DetailsDocument4 pagesAdmit Letter For Online JAIIB Examination - Jan 2022 Candidate DetailsRohith RaoNo ratings yet

- ApplicationDocument4 pagesApplicationRohith RaoNo ratings yet

- SCM 198934Document65 pagesSCM 198934Rohith RaoNo ratings yet

- AssignmentDocument67 pagesAssignmentRohith RaoNo ratings yet

- Krishna IEEEDocument9 pagesKrishna IEEERohith RaoNo ratings yet

- Basel III Important SectionsDocument22 pagesBasel III Important SectionsGeorge Lekatis100% (1)

- PHD Thesis On Shadow BankingDocument7 pagesPHD Thesis On Shadow Bankingafknekkfs100% (2)

- General Awareness Questions PDFDocument10 pagesGeneral Awareness Questions PDFRamu KNo ratings yet

- Discharge For Death Claim Under Policy No.Document3 pagesDischarge For Death Claim Under Policy No.Jayabalaji RNo ratings yet

- 1144 Working Management of Axis BankDocument60 pages1144 Working Management of Axis BankPriyaNo ratings yet

- Gauhati University Exam Form Payment Receipt - 023959Document2 pagesGauhati University Exam Form Payment Receipt - 023959M Computer & TravelsNo ratings yet

- Banking and Insurance Law NotesDocument164 pagesBanking and Insurance Law NotesFaisal KhanNo ratings yet

- Interim Report - Mahima Sharma - MBADocument6 pagesInterim Report - Mahima Sharma - MBAvijay gaurNo ratings yet

- Fin263 Chapter 7-RemittanceDocument22 pagesFin263 Chapter 7-RemittanceMohamad Khairul100% (1)

- An Analysis of Public Sector Banks PerfoDocument14 pagesAn Analysis of Public Sector Banks PerfoMurali Balaji M CNo ratings yet

- Interest and Commission: Mr. Christian Rae D. Bernales, LPTDocument16 pagesInterest and Commission: Mr. Christian Rae D. Bernales, LPTAlissa MayNo ratings yet

- Sworn Statement of Assets, Liabilities and Net WorthDocument2 pagesSworn Statement of Assets, Liabilities and Net WorthJayson Deocareza Dela Torre100% (1)

- Accounting For Business CombinationsDocument13 pagesAccounting For Business CombinationsDan MorettoNo ratings yet

- Account StatementDocument12 pagesAccount StatementKonanki Venkata SudhakarNo ratings yet

- Black Book Project With CorrectionDocument80 pagesBlack Book Project With CorrectionAbhishek BandalNo ratings yet

- Paytm Money Limited: Combined Margin Statement For The Day: Apr 22 2021Document1 pagePaytm Money Limited: Combined Margin Statement For The Day: Apr 22 2021Lekkalapudi SricharanNo ratings yet

- People of The Phils. v. Gilbert Reyes Wagas, G.R. No. 157943, September 4, 2013Document3 pagesPeople of The Phils. v. Gilbert Reyes Wagas, G.R. No. 157943, September 4, 2013Lexa L. DotyalNo ratings yet

- KGN Pub. Bill No. 16, Majencio Brand SolutionDocument1 pageKGN Pub. Bill No. 16, Majencio Brand Solutioncsingh081No ratings yet

- Ga2 - Far460 - Equity - Note On PpeDocument2 pagesGa2 - Far460 - Equity - Note On PpeAmniNo ratings yet

- RLLR SchemeDocument1 pageRLLR SchemeBhushan Singh BadgujjarNo ratings yet

- Mitesh Prajapati MB20023 (Project Report)Document66 pagesMitesh Prajapati MB20023 (Project Report)Mitesh prajapatiNo ratings yet

- Negotiable Instruments Case Digests For November 8Document3 pagesNegotiable Instruments Case Digests For November 8Megan MateoNo ratings yet

- Customer Satisfaction Towards Retail Lending of UCO Bank in ChandigarhDocument72 pagesCustomer Satisfaction Towards Retail Lending of UCO Bank in Chandigarhshivkmrchauhan0% (1)

- Equity ValuationDocument18 pagesEquity ValuationPhuntru PhiNo ratings yet

- Progress Monitoring Report: Basic Data Available Funds (US$) Total Cost and SourceDocument6 pagesProgress Monitoring Report: Basic Data Available Funds (US$) Total Cost and SourceFREDY RODRINo ratings yet

- Account Statement 231420Document4 pagesAccount Statement 231420Polo OaracilNo ratings yet

- ACTIVITY 5 Interim Reporting PDFDocument2 pagesACTIVITY 5 Interim Reporting PDFEstiloNo ratings yet

- Ibps Po Mains Cracker - 2016Document51 pagesIbps Po Mains Cracker - 2016Vimal PokalNo ratings yet

- Unit2: Treatment of Goodwill in Partnership AccountsDocument27 pagesUnit2: Treatment of Goodwill in Partnership AccountsJavid QuadirNo ratings yet