Download as pdf or txt

You might also like

- BASEL II Concept & ImplicationDocument17 pagesBASEL II Concept & Implicationfar_07No ratings yet

- Final Basel Norms ProjectDocument11 pagesFinal Basel Norms Projectgomathi18@yahoo100% (1)

- Liquidity Position of Nabil BankDocument29 pagesLiquidity Position of Nabil BankYadav Nepal100% (1)

- Investment Banking Interview GuideDocument228 pagesInvestment Banking Interview GuideNeil Grigg100% (2)

- Impact of Basel Iii On Indian Banks: Executive SummaryDocument9 pagesImpact of Basel Iii On Indian Banks: Executive Summarysruthilaya14No ratings yet

- Basel IIIDocument18 pagesBasel IIIPayal SawhneyNo ratings yet

- Basel III Accord - Basel 3 Norms: Contributed byDocument25 pagesBasel III Accord - Basel 3 Norms: Contributed bysamyumuthuNo ratings yet

- Basu Sir PaperDocument7 pagesBasu Sir Paperabhilash diveNo ratings yet

- Basel-III Norms - Highlights: Atul Kumar ThakurDocument9 pagesBasel-III Norms - Highlights: Atul Kumar ThakurJosephin DynaNo ratings yet

- Basel 3Document5 pagesBasel 3Ratan DehuryNo ratings yet

- Financial Sector Reforms Impacting Banking Sector WRT Basel Compliance in HDFC BankDocument29 pagesFinancial Sector Reforms Impacting Banking Sector WRT Basel Compliance in HDFC BankHyndavi VemulaNo ratings yet

- Objective-: Basel Is A City in SwitzerlandDocument8 pagesObjective-: Basel Is A City in Switzerlandpankaj_xaviersNo ratings yet

- Basel Iii: Presented By: Purshottam Singh Rahul Bagla Sandeep S. Sharma Vipul JainDocument10 pagesBasel Iii: Presented By: Purshottam Singh Rahul Bagla Sandeep S. Sharma Vipul JainRahul JainNo ratings yet

- Project Report On Basel IIIDocument8 pagesProject Report On Basel IIICharles DeoraNo ratings yet

- 09 - Chapter 2Document20 pages09 - Chapter 2BEPF 32 Sharma RohitNo ratings yet

- What Is Basel III and Overview of Basel Framework in PakistanDocument4 pagesWhat Is Basel III and Overview of Basel Framework in PakistanSayyam KhanNo ratings yet

- Cost of Implementing Basel IIIDocument4 pagesCost of Implementing Basel IIImsdkumar1990No ratings yet

- Basel 3Document10 pagesBasel 3sampathfriendNo ratings yet

- International Banking Law: Unit-02, PPT - 04Document11 pagesInternational Banking Law: Unit-02, PPT - 04Adarsh MeherNo ratings yet

- Basel II Vs Basel III NormsDocument3 pagesBasel II Vs Basel III NormsNaman Sharma0% (1)

- Basel NormsDocument5 pagesBasel NormsDeepak YadavNo ratings yet

- Basel-IIIDocument3 pagesBasel-IIIJayesh RupaniNo ratings yet

- Cost of Implementing Basel IIIDocument4 pagesCost of Implementing Basel IIIShay WaxenNo ratings yet

- Basel III: Challenges For Bangladesh Banking System: Jafrin Sultana Shamima SharminDocument18 pagesBasel III: Challenges For Bangladesh Banking System: Jafrin Sultana Shamima SharminborzukNo ratings yet

- Leverage Ratios Reserve Capital: Basel IiiDocument5 pagesLeverage Ratios Reserve Capital: Basel IiiroshanNo ratings yet

- A Brief Introduction To Basel Norms: Prepared byDocument10 pagesA Brief Introduction To Basel Norms: Prepared byDHRUMIL DAFTARY MBA 2021-23 (Delhi)No ratings yet

- Basel-III Norms and Indian Financial SystemDocument3 pagesBasel-III Norms and Indian Financial SystemNavneet MayankNo ratings yet

- Speech by N S Vishwanathan RBI ED On Basel 3 ImplementationDocument10 pagesSpeech by N S Vishwanathan RBI ED On Basel 3 ImplementationiyervsrNo ratings yet

- Basel Banking Norms: Their Efficacy, Analysis in The Global Context & Future DirectionDocument13 pagesBasel Banking Norms: Their Efficacy, Analysis in The Global Context & Future DirectionvivekNo ratings yet

- Basel Iii: Implementation and ChallengesDocument4 pagesBasel Iii: Implementation and ChallengessamiamaliveNo ratings yet

- Bassel 3Document7 pagesBassel 3Afzal HossenNo ratings yet

- Sr. Vice-President, Indian Banks' Association, Mumbai: Basel III Orms - S S MurthyDocument7 pagesSr. Vice-President, Indian Banks' Association, Mumbai: Basel III Orms - S S Murthymahendra_kolheNo ratings yet

- Basel Norms For BankingDocument5 pagesBasel Norms For BankingAkshat PrakashNo ratings yet

- Critical Analysis of BASEL III & Deutsche Bank and The Road To Basel III by Group-1Document14 pagesCritical Analysis of BASEL III & Deutsche Bank and The Road To Basel III by Group-1Kathiravan RajendranNo ratings yet

- Ackground For Basel IiiDocument10 pagesAckground For Basel IiiAkash ShuklaNo ratings yet

- FIN-546 Financial Risk Management, 11713633, Roll No. A014, Section Q1E08, Ca 2Document24 pagesFIN-546 Financial Risk Management, 11713633, Roll No. A014, Section Q1E08, Ca 2Sam RehmanNo ratings yet

- Basel Norms, Difference Between Basel Ii and Basel Iii Norms Group 4Document3 pagesBasel Norms, Difference Between Basel Ii and Basel Iii Norms Group 4Rupesh GhimireNo ratings yet

- Basel 3 News July 2011Document33 pagesBasel 3 News July 2011George LekatisNo ratings yet

- Basel Accord and Basel NormsDocument6 pagesBasel Accord and Basel NormsJaspreet SinghNo ratings yet

- ProQuestDocuments 2015-04-22 KDDocument11 pagesProQuestDocuments 2015-04-22 KDKais NandoliaNo ratings yet

- International BankingDocument5 pagesInternational Bankingaditi singhNo ratings yet

- Jahangirnagar University: Institute of Business Administration (IBA-JU)Document5 pagesJahangirnagar University: Institute of Business Administration (IBA-JU)tanishaNo ratings yet

- Banking Law First Internal Assessment: Name: Samarth Dahiya PRN: 19010126043 Course: Bba LLB (Hons) Div: A Semester - VDocument7 pagesBanking Law First Internal Assessment: Name: Samarth Dahiya PRN: 19010126043 Course: Bba LLB (Hons) Div: A Semester - VSamarth DahiyaNo ratings yet

- India and The BASEL-III Reforms Efinitions Basel III:: HQLA (High Quality Liquid Assets)Document5 pagesIndia and The BASEL-III Reforms Efinitions Basel III:: HQLA (High Quality Liquid Assets)Mayank LabhNo ratings yet

- Basel III.: Improving Quality, Consistency and Transparency of CapitalDocument6 pagesBasel III.: Improving Quality, Consistency and Transparency of CapitalKool RishNo ratings yet

- Comparative Discussion Among BASEL I, BASEL II & BASEL IIIDocument4 pagesComparative Discussion Among BASEL I, BASEL II & BASEL IIIRajesh PaulNo ratings yet

- MBFI AasthaaroraDocument4 pagesMBFI AasthaaroraAastha AroraNo ratings yet

- Basel NormsDocument23 pagesBasel NormsPranu PranuNo ratings yet

- Bulletin Finanza: Basel Iii NormsDocument2 pagesBulletin Finanza: Basel Iii Normskaran_w3No ratings yet

- Basel III Comparison Between BII & B III: Mayuri Jatale Sarita Shah Abhijeet HelodeyDocument20 pagesBasel III Comparison Between BII & B III: Mayuri Jatale Sarita Shah Abhijeet HelodeyDiwakar LakhotiyaNo ratings yet

- Basel III Impact Analysis For Indian Banks Siddharth ShuklaDocument11 pagesBasel III Impact Analysis For Indian Banks Siddharth ShuklaDeepak LotiaNo ratings yet

- Risk Compliance News July 2011Document80 pagesRisk Compliance News July 2011George LekatisNo ratings yet

- MPRA Paper 52967Document55 pagesMPRA Paper 52967Arijit DasNo ratings yet

- Module D-Balance Sheet Management PDFDocument14 pagesModule D-Balance Sheet Management PDFvarun_bathulaNo ratings yet

- Basel NormsDocument4 pagesBasel NormsFathima MuhammedNo ratings yet

- Basel NormsDocument14 pagesBasel Normsswatisin93No ratings yet

- Banking Economy Prof. S. Srinivasan (External Contributor)Document2 pagesBanking Economy Prof. S. Srinivasan (External Contributor)Asha DeoNo ratings yet

- Basil 3 AssignmentDocument27 pagesBasil 3 AssignmentSadia Islam MouNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- The Basel II Risk Parameters: Estimation, Validation, Stress Testing - with Applications to Loan Risk ManagementFrom EverandThe Basel II Risk Parameters: Estimation, Validation, Stress Testing - with Applications to Loan Risk ManagementRating: 1 out of 5 stars1/5 (1)

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- E-Resources Module-I in Indian Economy-I by Dr. Rituranjan - 0Document2 pagesE-Resources Module-I in Indian Economy-I by Dr. Rituranjan - 0Lado BahadurNo ratings yet

- Monetary Policy and Operating ProcedureDocument3 pagesMonetary Policy and Operating ProcedureLado BahadurNo ratings yet

- Targets & Instruments of Monetary Policy and Tinbergen ConditionDocument4 pagesTargets & Instruments of Monetary Policy and Tinbergen ConditionLado BahadurNo ratings yet

- Xii. Problems of Monetary Policy MakingDocument4 pagesXii. Problems of Monetary Policy MakingLado BahadurNo ratings yet

- E-Resources Module-VI Paper No.: DSE-xiii Paper Title: Money and Financial Markets Course: B.A. (Hons.) Economics, Sem.-VI Students of S.R.C.CDocument2 pagesE-Resources Module-VI Paper No.: DSE-xiii Paper Title: Money and Financial Markets Course: B.A. (Hons.) Economics, Sem.-VI Students of S.R.C.CLado BahadurNo ratings yet

- Banking Crisis in IndiaDocument3 pagesBanking Crisis in IndiaLado BahadurNo ratings yet

- E-Resources Module-IX Paper No.: DSE-xiii Paper Title: Money and Financial Markets Course: B.A. (Hons.) Economics, Sem.-VI Students of S.R.C.CDocument3 pagesE-Resources Module-IX Paper No.: DSE-xiii Paper Title: Money and Financial Markets Course: B.A. (Hons.) Economics, Sem.-VI Students of S.R.C.CLado BahadurNo ratings yet

- Balance Sheet Management of Banks in Post-Reform IndiaDocument3 pagesBalance Sheet Management of Banks in Post-Reform IndiaLado BahadurNo ratings yet

- Indian Economy II Unit IIIII EcoHVIsemDocument4 pagesIndian Economy II Unit IIIII EcoHVIsemLado BahadurNo ratings yet

- Unit IV Indian Economy II BAHeconomics VIsemDocument2 pagesUnit IV Indian Economy II BAHeconomics VIsemLado BahadurNo ratings yet

- Unit III EcoH VI Semester Indian Economy IIDocument2 pagesUnit III EcoH VI Semester Indian Economy IILado BahadurNo ratings yet

- Samman Mohammadi, Mohammad Monfared Maharlouie, Dan Omid Mansouri. 2012. The Effect of Cash Holdings On Income Smoothing PDFDocument10 pagesSamman Mohammadi, Mohammad Monfared Maharlouie, Dan Omid Mansouri. 2012. The Effect of Cash Holdings On Income Smoothing PDFhebert0595No ratings yet

- Philam Strategic Growth Fund, Inc. (PSGF) : Historical PerformanceDocument1 pagePhilam Strategic Growth Fund, Inc. (PSGF) : Historical Performanceapi-25886697No ratings yet

- Nikhil BankDocument3 pagesNikhil Bankclientlegalfin2022No ratings yet

- Estate Tax SummaryDocument9 pagesEstate Tax SummaryRb BalanayNo ratings yet

- Financial Statement Analysis ofDocument14 pagesFinancial Statement Analysis ofvizakanNo ratings yet

- Ecash: What Is E-Cash?Document6 pagesEcash: What Is E-Cash?Aarchi MaheshwariNo ratings yet

- Mis and CRMDocument2 pagesMis and CRMDivya Carl NazarethNo ratings yet

- Internship Report On Management of Loan and Advances of Dhaka Bank LTDDocument69 pagesInternship Report On Management of Loan and Advances of Dhaka Bank LTDhelal uddinNo ratings yet

- Dipakshi Balance Sheet 2016-17Document25 pagesDipakshi Balance Sheet 2016-17shyam chaudharyNo ratings yet

- Test Bank For Managing Operations Across The Supply Chain 2nd Edition by SwinkDocument36 pagesTest Bank For Managing Operations Across The Supply Chain 2nd Edition by Swinkfeodshippingqors98% (55)

- Mihs Fee Structure 2021.2022Document9 pagesMihs Fee Structure 2021.2022daniel samwelNo ratings yet

- Kerima AliDocument89 pagesKerima AliMohammed ademNo ratings yet

- Bombay HC Sanjay Dhokad - 69C - Discharge of BurdenDocument15 pagesBombay HC Sanjay Dhokad - 69C - Discharge of BurdenSubramanyam SettyNo ratings yet

- Internship Report On The Effect of Strategic Human Resource Management (SHRM) Practices On Organizational Performance - A Study On AB Bank LimitedDocument51 pagesInternship Report On The Effect of Strategic Human Resource Management (SHRM) Practices On Organizational Performance - A Study On AB Bank LimitedMohammad Rakibul IslamNo ratings yet

- Citibank V SabenianoDocument113 pagesCitibank V SabenianoTon RiveraNo ratings yet

- Role of EXIM BankDocument2 pagesRole of EXIM Bankultimatekp144100% (1)

- Post Aceeptance Activities of Contracts 1Document54 pagesPost Aceeptance Activities of Contracts 1Saptarshi PalNo ratings yet

- (123doc) - Script-Should-Anz-Bank-Abandon-The-Physical-Branch-Model-And-Transition-All-Its-Services-OnlineDocument15 pages(123doc) - Script-Should-Anz-Bank-Abandon-The-Physical-Branch-Model-And-Transition-All-Its-Services-OnlineMai AnhNo ratings yet

- PT Bank HSBC Indonesia Annual Report 2020Document357 pagesPT Bank HSBC Indonesia Annual Report 2020Salsabila MaharaniNo ratings yet

- Eco 502 Project PaperDocument16 pagesEco 502 Project Paper0175117278zNo ratings yet

- Jobs Careers JC 21 March 2018..@towardstomorrowDocument4 pagesJobs Careers JC 21 March 2018..@towardstomorrowaravind174No ratings yet

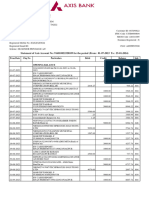

- Statement of Axis Account No:080010100183918 For The Period (From: 19-10-2020 To: 18-10-2021)Document4 pagesStatement of Axis Account No:080010100183918 For The Period (From: 19-10-2020 To: 18-10-2021)Ketan PatelNo ratings yet

- Updates On Open Offer (Company Update)Document80 pagesUpdates On Open Offer (Company Update)Shyam SunderNo ratings yet

- DB Pru PDFDocument20 pagesDB Pru PDFblombardi8No ratings yet

- Thesis 1Document71 pagesThesis 1lulumokeninNo ratings yet

- Financing and Developing PACSDocument3 pagesFinancing and Developing PACSSadaf KushNo ratings yet

- AFM - Lecture 1 2 3 NotesDocument24 pagesAFM - Lecture 1 2 3 NotesArvind Ujjwal MehthaNo ratings yet