Download as pdf or txt

You might also like

- Provide Support To People Living With DementiaDocument9 pagesProvide Support To People Living With DementiaGurpreet Singh WirringNo ratings yet

- Cardiophase™ High Sensitivity C Reactive Protein (HSCRP) : Intended UseDocument14 pagesCardiophase™ High Sensitivity C Reactive Protein (HSCRP) : Intended UseJosé Juan Rodríguez JuárezNo ratings yet

- America's Child-Care Crisis: Rethinking an Essential BusinessFrom EverandAmerica's Child-Care Crisis: Rethinking an Essential BusinessNo ratings yet

- Importance of HousingDocument3 pagesImportance of HousingpriscamthobwaNo ratings yet

- AB - CHCCSM004 AnswersDocument12 pagesAB - CHCCSM004 AnswersShivam Anand Shukla100% (1)

- The Effects of Economic StratificationDocument4 pagesThe Effects of Economic StratificationksmithfranklinNo ratings yet

- Socioeconomic StatusDocument4 pagesSocioeconomic Statusbec.sarl.admiNo ratings yet

- The Family and Economic Development PDFDocument9 pagesThe Family and Economic Development PDFmineasaroeunNo ratings yet

- Putri ADocument2 pagesPutri APutri SG.No ratings yet

- CB End SemDocument13 pagesCB End SemanujNo ratings yet

- Client Relationships and Ethical Boudaries For Social Workers in Child WelfareDocument5 pagesClient Relationships and Ethical Boudaries For Social Workers in Child WelfareGabriela IstrateNo ratings yet

- Socio-Economic SurveyDocument51 pagesSocio-Economic SurveyAlpa ParmarNo ratings yet

- Enterprise - Impact of Affordable Housing On Families and Communities PDFDocument20 pagesEnterprise - Impact of Affordable Housing On Families and Communities PDFCedric ZhouNo ratings yet

- Family and Buying Roles - EditedDocument7 pagesFamily and Buying Roles - Editedoyite danielNo ratings yet

- Socioeconomic StatusDocument5 pagesSocioeconomic StatusGOSHUNo ratings yet

- External Influences Play A Significant Role in Shaping An IndividualDocument1 pageExternal Influences Play A Significant Role in Shaping An IndividualArnold Mark Ian CacanindinNo ratings yet

- What Is The Social EconomyDocument2 pagesWhat Is The Social Economynalli cardonNo ratings yet

- Techniques and Guidelines For Social Work Practice, 7/EDocument71 pagesTechniques and Guidelines For Social Work Practice, 7/EAnanta ChaliseNo ratings yet

- Resident Services Background Paper March 29Document13 pagesResident Services Background Paper March 29Rishab GuptaNo ratings yet

- Document 1Document3 pagesDocument 1aneesNo ratings yet

- Homework and Socioeconomic StatusDocument8 pagesHomework and Socioeconomic Statusvmwwwwmpd100% (1)

- Mmi Caregiving Costs Working CaregiversDocument26 pagesMmi Caregiving Costs Working CaregiversSuman KondojuNo ratings yet

- Poverty and Health Literature ReviewDocument5 pagesPoverty and Health Literature Reviewafmzfvlopbchbe100% (1)

- Home Care LEARNING OUTCOMES After Completing This Chapter, YouDocument18 pagesHome Care LEARNING OUTCOMES After Completing This Chapter, Youtwy113100% (1)

- Marriage 2Document8 pagesMarriage 2EdwinNo ratings yet

- Sociovocational Rehabiliotation/ Socioeconomic RehabilitationDocument32 pagesSociovocational Rehabiliotation/ Socioeconomic RehabilitationSonia guptaNo ratings yet

- The Case Against Procreation: Antinatalism in Modern DiscourseFrom EverandThe Case Against Procreation: Antinatalism in Modern DiscourseNo ratings yet

- Principle of Marketing: Topic: Consumer Behavior, Buying Model and ProcessDocument30 pagesPrinciple of Marketing: Topic: Consumer Behavior, Buying Model and ProcessMadiha HussainNo ratings yet

- Family Impact Analysis ChecklistDocument4 pagesFamily Impact Analysis Checklistapi-283593680No ratings yet

- Educ 111 ActivityDocument23 pagesEduc 111 ActivitySyrile MangudangNo ratings yet

- Zamambo Mkhize AssignmentDocument8 pagesZamambo Mkhize AssignmentZamambo MkhizeNo ratings yet

- International Business Chapter 2Document7 pagesInternational Business Chapter 2DhavalNo ratings yet

- How Social Class Affects Life ChancesDocument3 pagesHow Social Class Affects Life ChancesSarah Sanchez100% (2)

- Beyond Quick Fixes: What Will It Really Take To Improve Child Welfare in America?Document10 pagesBeyond Quick Fixes: What Will It Really Take To Improve Child Welfare in America?Public Consulting GroupNo ratings yet

- HD Pyq SolDocument75 pagesHD Pyq Solshashankvats26No ratings yet

- Healthcare Economic Research Paper TopicsDocument4 pagesHealthcare Economic Research Paper Topicsafmcsvatc100% (1)

- Return On Investment: Cost vs. Benefits: James J. Heckman, University of ChicagoDocument8 pagesReturn On Investment: Cost vs. Benefits: James J. Heckman, University of ChicagoJimmy AlvaradoNo ratings yet

- Project Gs MisDocument25 pagesProject Gs MisKrish AgrawalNo ratings yet

- Effects of Socioeconomic Status On Students AchievementDocument10 pagesEffects of Socioeconomic Status On Students Achievementwarda rashidNo ratings yet

- WhitePaper ImprovingOutcomesOlderYouth FRDocument14 pagesWhitePaper ImprovingOutcomesOlderYouth FRrajrudrapaaNo ratings yet

- Butler WelfareDocument29 pagesButler WelfareAnvitaRamachandranNo ratings yet

- Describe Your Own Community Using Picture/sDocument4 pagesDescribe Your Own Community Using Picture/sKyla TuazonNo ratings yet

- How Social Class Impacts Access To Quality HealthcareDocument3 pagesHow Social Class Impacts Access To Quality HealthcareAutismHelpInNo ratings yet

- Unit 4 Gender StudiesDocument6 pagesUnit 4 Gender StudiesMaanu Shree KNo ratings yet

- Role of Care GiversDocument4 pagesRole of Care GiversJisna AlbyNo ratings yet

- Aging in The Right Place (Excerpt)Document3 pagesAging in The Right Place (Excerpt)Health Professions Press, an imprint of Paul H. Brookes Publishing Co., Inc.No ratings yet

- Chapter 2 Review Related LiteratureDocument4 pagesChapter 2 Review Related LiteratureJanida Basman DalidigNo ratings yet

- NSA Critique #1 WEBINARDocument14 pagesNSA Critique #1 WEBINARKiel Francis TejadaNo ratings yet

- Workplace DiversityDocument8 pagesWorkplace DiversityAssignmentLab.com100% (1)

- Addressing Unemployment Issues in Kenya or Any Country For The MatterDocument8 pagesAddressing Unemployment Issues in Kenya or Any Country For The Matteralexlugalia7No ratings yet

- Economic Determinants of Child HealthDocument6 pagesEconomic Determinants of Child HealthSanifa MedNo ratings yet

- The Effects of Poverty On An IndividualDocument4 pagesThe Effects of Poverty On An IndividualHnin PwintNo ratings yet

- How Will Family Physicians Care For The Patient in The Context of Family and Community?Document13 pagesHow Will Family Physicians Care For The Patient in The Context of Family and Community?andrewwilliampalileo@yahoocomNo ratings yet

- Bridging Gaps: Implementing Public-Private Partnerships to Strengthen Early EducationFrom EverandBridging Gaps: Implementing Public-Private Partnerships to Strengthen Early EducationNo ratings yet

- Direct Sales 1.0selling Process: 1.1 Identify Pontential CostumerDocument17 pagesDirect Sales 1.0selling Process: 1.1 Identify Pontential CostumerNor AtiqahNo ratings yet

- Baby Boomer Retirement SecurityDocument40 pagesBaby Boomer Retirement SecurityWan AlangHazirahNo ratings yet

- Understanding Dependency by David EllwoodDocument29 pagesUnderstanding Dependency by David EllwoodvwkyangNo ratings yet

- While A Strong Economy Can Provide Various Opportunities For FamiliesDocument2 pagesWhile A Strong Economy Can Provide Various Opportunities For FamiliesSUDARCHELVI A/P ALAGANDRAN MoeNo ratings yet

- Lecture 1Document14 pagesLecture 1Aleena ZiaNo ratings yet

- Organizational Environment: Organization and Social EnvironmentDocument16 pagesOrganizational Environment: Organization and Social Environmentpuppypower888No ratings yet

- The Increasing Prices of Basic Necessities Like SugarDocument4 pagesThe Increasing Prices of Basic Necessities Like SugarSUDARCHELVI A/P ALAGANDRAN MoeNo ratings yet

- General Notes: Copy RightDocument1 pageGeneral Notes: Copy Rightchinmoy patraNo ratings yet

- Covid HospitalDocument1 pageCovid Hospitalchinmoy patraNo ratings yet

- Site Visit ReportDocument5 pagesSite Visit Reportchinmoy patraNo ratings yet

- Land Use PlanningDocument4 pagesLand Use Planningchinmoy patraNo ratings yet

- Convention CentreDocument1 pageConvention Centrechinmoy patraNo ratings yet

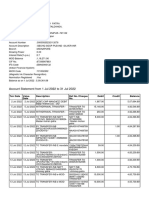

- Account Statement From 21 Jul 2022 To 31 Aug 2022Document3 pagesAccount Statement From 21 Jul 2022 To 31 Aug 2022chinmoy patraNo ratings yet

- Account Statement From 20 Jul 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 20 Jul 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancechinmoy patraNo ratings yet

- Tribal Cultural CentreDocument3 pagesTribal Cultural Centrechinmoy patraNo ratings yet

- Risk Assessment No. 27 PNEUMATIC POWER TOOL Rev 0Document1 pageRisk Assessment No. 27 PNEUMATIC POWER TOOL Rev 0Lalit ChoudharyNo ratings yet

- Saudi Civil Defense Extinguishes Huge Fire at DamDocument3 pagesSaudi Civil Defense Extinguishes Huge Fire at Damamir.slotNo ratings yet

- HRM610 Final SlideDocument19 pagesHRM610 Final SlideArju LubnaNo ratings yet

- I. Vision/Mission of Faith: Transforming Ourselves, Transforming Our WorldDocument16 pagesI. Vision/Mission of Faith: Transforming Ourselves, Transforming Our WorldErica Pasco-LatNo ratings yet

- Persuasive LetterDocument2 pagesPersuasive Letterapi-2379809760% (1)

- Health Insurance, IsIP-222033Document3 pagesHealth Insurance, IsIP-222033AhmedNo ratings yet

- Hand DhejeDocument21 pagesHand Dheje1bookwork1No ratings yet

- MRM2-1000 1200M3X Sigma III Positioner ManualDocument44 pagesMRM2-1000 1200M3X Sigma III Positioner ManualMarcelo BritoNo ratings yet

- Scherer, A. K., 2016. Bioarchaeology and The Skeletons of Pre-Columbian MayaDocument53 pagesScherer, A. K., 2016. Bioarchaeology and The Skeletons of Pre-Columbian MayaĐani NovakovićNo ratings yet

- PSY202 Ch11 Emotion & Health W24Document63 pagesPSY202 Ch11 Emotion & Health W24petersjp82No ratings yet

- 2013 01 Cumene Hydroperoxide Aldrich MSDSDocument7 pages2013 01 Cumene Hydroperoxide Aldrich MSDStpr314No ratings yet

- Mario Madridejos v. NYK Fil Shipmanagement, G.R. No. 204262, 07 June 2017Document3 pagesMario Madridejos v. NYK Fil Shipmanagement, G.R. No. 204262, 07 June 2017Cathy GabroninoNo ratings yet

- Medical Clearance FormDocument2 pagesMedical Clearance FormPhake CodedNo ratings yet

- Diass Fourth Quarter ExamDocument5 pagesDiass Fourth Quarter Examdummyymmudowo100% (1)

- Opinion On InjunctionDocument7 pagesOpinion On InjunctionOregon MikeNo ratings yet

- Challenges/: EpistemeDocument28 pagesChallenges/: EpistemeKádár BiancaNo ratings yet

- Maternal Deprivation HypothesisDocument2 pagesMaternal Deprivation HypothesisChloe100% (3)

- The Politics of Depression: Diverging Trends in Internalizing Symptoms Among US Adolescents by Political BeliefsDocument25 pagesThe Politics of Depression: Diverging Trends in Internalizing Symptoms Among US Adolescents by Political BeliefsJuan PeNo ratings yet

- Punitive, Restorative, and Transformative JusticeDocument4 pagesPunitive, Restorative, and Transformative JusticeMonkey DLuffyyyNo ratings yet

- University of Bath Coursework ExtensionDocument6 pagesUniversity of Bath Coursework Extensionf60pk9dc100% (2)

- Roles and Responsibilities of A Guidance CounselorDocument5 pagesRoles and Responsibilities of A Guidance CounselorDan NavarroNo ratings yet

- SUMMATIVE TEST MAPEH 6 Quarter 1Document4 pagesSUMMATIVE TEST MAPEH 6 Quarter 1M Ivy Estoque100% (2)

- 496 E-Folio - Essential VDocument4 pages496 E-Folio - Essential VldhendersonNo ratings yet

- BB Cost of MBA Report 2021Document31 pagesBB Cost of MBA Report 2021Christian John RojoNo ratings yet

- Comparison Chart: Compare The Benefits of Our PoliciesDocument2 pagesComparison Chart: Compare The Benefits of Our PoliciesMeNo ratings yet

- Prospectus1 2Document77 pagesProspectus1 2Japsifat SinghNo ratings yet

- Mass Media and Pulse Polio Awareness CamDocument7 pagesMass Media and Pulse Polio Awareness CamRajeev RaiNo ratings yet

- Test Description Value(s) Unit Reference RangeDocument5 pagesTest Description Value(s) Unit Reference RangeGalaxys KitchensNo ratings yet