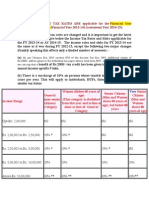

The Slab Codes in The Table View

The Slab Codes in The Table View

You might also like

- Tax Presentation-29.01.2023Document25 pagesTax Presentation-29.01.2023Abhinav Parhi100% (2)

- Narrative Report-Virtual Parent's OrientationnDocument3 pagesNarrative Report-Virtual Parent's OrientationnApril Ramos Dimayuga95% (21)

- Sex, Drugs & Magick: A Journey Beyond LimitsDocument121 pagesSex, Drugs & Magick: A Journey Beyond Limitsvvvulpea80% (5)

- Boq For Box CulvertDocument2 pagesBoq For Box CulvertDaniel Okere100% (1)

- FY 2022-23 (AY 2023-24) - Taxguru - inDocument3 pagesFY 2022-23 (AY 2023-24) - Taxguru - inHarshilNo ratings yet

- Taxguru - In-Income Tax Rates For FY 2020-21 Amp FY 2021-22Document8 pagesTaxguru - In-Income Tax Rates For FY 2020-21 Amp FY 2021-22JiyalalNo ratings yet

- Tax Liability For The Assessment Years 2014-15 and 2015-16Document11 pagesTax Liability For The Assessment Years 2014-15 and 2015-16Accounting & TaxationNo ratings yet

- Income Tax Rates Assessment Year 2011-2012Document10 pagesIncome Tax Rates Assessment Year 2011-2012Pankaj KhannaNo ratings yet

- Guidance Note On Option For Old Vs New Tax Regime - FY22-23 & AY23-24 PDFDocument3 pagesGuidance Note On Option For Old Vs New Tax Regime - FY22-23 & AY23-24 PDFgowtham DevNo ratings yet

- Budget Synopsis 2015-16 PDFDocument12 pagesBudget Synopsis 2015-16 PDFBhagwan PalNo ratings yet

- Normal Tax Rates Applicable To An IndividualDocument12 pagesNormal Tax Rates Applicable To An IndividualAnonymous 9Yv6n5qvSNo ratings yet

- IT RatesDocument6 pagesIT RatesAnjali Krishna SNo ratings yet

- Tax Deduction - DR Sajjad Wani JKASDocument26 pagesTax Deduction - DR Sajjad Wani JKASMohmad Yousuf100% (1)

- Income Tax Slabs & Rates For Assessment Year 2013-14Document37 pagesIncome Tax Slabs & Rates For Assessment Year 2013-14Jigar RavalNo ratings yet

- Income Tax Slab FY 2023-24 and AY 2024-25 - New ADocument3 pagesIncome Tax Slab FY 2023-24 and AY 2024-25 - New ABagath SinghNo ratings yet

- Alternative Tax Regime (This Has Been Dealt in 1.1A of Chapter 1 in YourDocument6 pagesAlternative Tax Regime (This Has Been Dealt in 1.1A of Chapter 1 in YourRhea SharmaNo ratings yet

- Taxation Workbook 2022Document204 pagesTaxation Workbook 2022Navya GulatiNo ratings yet

- E PDF - Know Your Income Tax Rate AY 2021 22 23Document8 pagesE PDF - Know Your Income Tax Rate AY 2021 22 23CHANDAN CHANDUNo ratings yet

- Income Tax Slab FY 2014-15Document3 pagesIncome Tax Slab FY 2014-15zveeraNo ratings yet

- Notes On DTC BillDocument5 pagesNotes On DTC Billshikah sidarNo ratings yet

- Income Tax Calculator Calculate Income Tax For FY 2022-23Document1 pageIncome Tax Calculator Calculate Income Tax For FY 2022-23Vivek LakkakulaNo ratings yet

- How To Calculate Income TaxDocument4 pagesHow To Calculate Income TaxreemaNo ratings yet

- ITR DocumentDocument6 pagesITR DocumentRamesh BabuNo ratings yet

- Module-1 - Introduction & Basic Tax ComputationDocument24 pagesModule-1 - Introduction & Basic Tax Computationshaswat sharmaNo ratings yet

- Individual, HUF, AOP or BOIDocument4 pagesIndividual, HUF, AOP or BOIABC 123No ratings yet

- TDS On SalaryDocument5 pagesTDS On SalaryAato AatoNo ratings yet

- Latest Income Tax Slabs and Rates For FY 2013-14 and AS 2014-15Document6 pagesLatest Income Tax Slabs and Rates For FY 2013-14 and AS 2014-15Michaelben MichaelbenNo ratings yet

- Income Tax: Administrative Set-UpDocument25 pagesIncome Tax: Administrative Set-UpMohit RahejaNo ratings yet

- Individual Txation FY 203 24Document44 pagesIndividual Txation FY 203 24Smarty ShivamNo ratings yet

- Income Tax Slabs & Rates For Assessment Year 2014-15Document4 pagesIncome Tax Slabs & Rates For Assessment Year 2014-15ptk_guly3871No ratings yet

- DeferredDocument11 pagesDeferredShubham MaheshwariNo ratings yet

- Business Environment: Budget 2013-2014 AnalysisDocument11 pagesBusiness Environment: Budget 2013-2014 AnalysisKyle BaileyNo ratings yet

- IT Projection ToolDocument7 pagesIT Projection ToolsaurabhmanitNo ratings yet

- Benefits For Senior Citizens Very Senior Citizens - EnglishDocument8 pagesBenefits For Senior Citizens Very Senior Citizens - EnglishmonishaNo ratings yet

- IT Circular 2011-12Document56 pagesIT Circular 2011-12Narasimha SastryNo ratings yet

- Income Tax On SalaryDocument23 pagesIncome Tax On SalarySarvesh MishraNo ratings yet

- The List of Components Which You Can Use For Salary BreakupDocument8 pagesThe List of Components Which You Can Use For Salary BreakupAnonymous VhqxrXNo ratings yet

- India Budget 2011Document22 pagesIndia Budget 2011ashishgautamNo ratings yet

- Tax Rates As 2015-16Document1 pageTax Rates As 2015-16Jatin PatelNo ratings yet

- Note On Budget Proposals-2020Document4 pagesNote On Budget Proposals-2020Dhananjai SharmaNo ratings yet

- IT Calculator 14 15 Taxguru - inDocument16 pagesIT Calculator 14 15 Taxguru - inanirbanpwd76No ratings yet

- Individual Txation FY 2019 20 With Demo of Return FilingDocument73 pagesIndividual Txation FY 2019 20 With Demo of Return FilingGanesh PNo ratings yet

- Tax Update A.Y. 2015-16Document32 pagesTax Update A.Y. 2015-16Anil PatelNo ratings yet

- Taxation Flow PresentationDocument73 pagesTaxation Flow PresentationMohan ChoudharyNo ratings yet

- Tds SALARY FOR A.Y. 2011-12Document59 pagesTds SALARY FOR A.Y. 2011-12Pragnesh ShahNo ratings yet

- Ammendments in Direct TaxDocument37 pagesAmmendments in Direct TaxVipul KatariyaNo ratings yet

- Scenario 1# You Do Not Have Outstanding Tax LiabilityDocument7 pagesScenario 1# You Do Not Have Outstanding Tax LiabilityBhupendra SharmaNo ratings yet

- Tax Saving FY 2021-22 - FDocument30 pagesTax Saving FY 2021-22 - Fsapreswapnil8388No ratings yet

- Individual Taxation (Ay 2019-20)Document29 pagesIndividual Taxation (Ay 2019-20)Mudit SinghNo ratings yet

- Tax Slabs & Tax Saving Strategies For New Tax Payers 2011-12Document5 pagesTax Slabs & Tax Saving Strategies For New Tax Payers 2011-12channaveer sgNo ratings yet

- How To Calculate Ur Income TaxDocument3 pagesHow To Calculate Ur Income TaxrazeemshipNo ratings yet

- MATH PROJECT TOPIC 2 (Income Tax)Document7 pagesMATH PROJECT TOPIC 2 (Income Tax)avinamakadiaNo ratings yet

- Note On Budget Proposals-2020Document4 pagesNote On Budget Proposals-2020Karthik PenakaNo ratings yet

- 1 3+part+2Document28 pages1 3+part+2jaspreet kaurNo ratings yet

- Income-Tax-Slab 13-14Document2 pagesIncome-Tax-Slab 13-14rani26octNo ratings yet

- Finance Bill, 2012: Provisions Relating To Direct TaxesDocument36 pagesFinance Bill, 2012: Provisions Relating To Direct TaxessangeetsindanNo ratings yet

- Deduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009Document70 pagesDeduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009rhldxmNo ratings yet

- Ryhuqphqwri, QGLD 0Lqlvwu/Ri) LQDQFH 'Hsduwphqwri5Hyhqxh &Hqwudo%Rdugri'Luhfw7D (HVDocument24 pagesRyhuqphqwri, QGLD 0Lqlvwu/Ri) LQDQFH 'Hsduwphqwri5Hyhqxh &Hqwudo%Rdugri'Luhfw7D (HVNiraj JainNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Name: - Date: - Grade and Section: - Score: - Formative AssessmentDocument7 pagesName: - Date: - Grade and Section: - Score: - Formative AssessmentLey F. FajutaganaNo ratings yet

- The Voice On The Skin Self-Mutilation and MerleauDocument13 pagesThe Voice On The Skin Self-Mutilation and MerleauDr FreudNo ratings yet

- The Food Industry in Nigeria Development and QualiDocument6 pagesThe Food Industry in Nigeria Development and Qualimercy luwaNo ratings yet

- Application of Geomatry in BusinessDocument23 pagesApplication of Geomatry in BusinessSoummo ChakmaNo ratings yet

- Perception of Hostel StudentsDocument6 pagesPerception of Hostel StudentsKhairul Hazwan100% (3)

- Venezuelan Food Glossary Ver6Document1 pageVenezuelan Food Glossary Ver6Peter BehringerNo ratings yet

- Fever Tree: Agriculture, Forestry & FisheriesDocument16 pagesFever Tree: Agriculture, Forestry & FisheriesDylanNo ratings yet

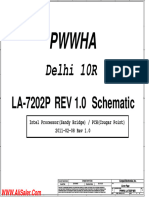

- Toshiba Satellite C660 Compal LA-7202P PWWHA Delphi 10R Rev1.0 SchematicDocument43 pagesToshiba Satellite C660 Compal LA-7202P PWWHA Delphi 10R Rev1.0 Schematicpcs prasannaNo ratings yet

- Equity EssayDocument8 pagesEquity EssayTeeruVarasuNo ratings yet

- Soul Winning TractDocument2 pagesSoul Winning TractPaul Moiloa50% (2)

- Irregular Verbs Nueva Lista DuncanDocument2 pagesIrregular Verbs Nueva Lista DuncanAndrey Vargas MoralesNo ratings yet

- Once Upon The Time in America - Google Search PDFDocument1 pageOnce Upon The Time in America - Google Search PDFDiana KarchavaNo ratings yet

- Unit 5: Ind As 111: Joint ArrangementsDocument26 pagesUnit 5: Ind As 111: Joint ArrangementsDheeraj TurpunatiNo ratings yet

- Argument EssayDocument3 pagesArgument Essayapi-669204574No ratings yet

- GSIS TEMPLATE Fire Insurance Application Form (TRAD)Document3 pagesGSIS TEMPLATE Fire Insurance Application Form (TRAD)Ronan MaquidatoNo ratings yet

- Pengaruh Pemberian Tempe Kacang Hijau Sebagai Polen Pengganti Terhadap Penampilan Larva Lebah Pekerja Apis MelliferaDocument8 pagesPengaruh Pemberian Tempe Kacang Hijau Sebagai Polen Pengganti Terhadap Penampilan Larva Lebah Pekerja Apis MelliferaResti Amelia SusantiNo ratings yet

- Municipal Solid Waste ManagementDocument100 pagesMunicipal Solid Waste ManagementPremkumar T100% (1)

- Kamba Ramayanam IDocument701 pagesKamba Ramayanam IShubham BhatiaNo ratings yet

- Ucl Thesis Citation StyleDocument6 pagesUcl Thesis Citation Stylemaryburgsiouxfalls100% (1)

- Postmodernism and Its Comparative Education ImplicationsDocument18 pagesPostmodernism and Its Comparative Education ImplicationsLetta ZaglaNo ratings yet

- 01.worksheet-1 U1Document1 page01.worksheet-1 U1Jose Manuel AlcantaraNo ratings yet

- Naivas CP & SP Description Cost Price Selling Price %margins C.P S.P %marginsDocument12 pagesNaivas CP & SP Description Cost Price Selling Price %margins C.P S.P %marginsBonnie Maguathi MwauraNo ratings yet

- ShapeFuture Brochure2022 EnglishDocument36 pagesShapeFuture Brochure2022 EnglishJenifer Yajaira Rodríguez ChamorroNo ratings yet

- Course Handout Spreadsheet For ManagersDocument8 pagesCourse Handout Spreadsheet For ManagersSunil ChinnuNo ratings yet

- Pe 3 First QuizDocument1 pagePe 3 First QuizLoremer Delos Santos LiboonNo ratings yet

- Waterfront Boundaries For Grants of Public Crown Lands - MNR - E000074 - 2001Document3 pagesWaterfront Boundaries For Grants of Public Crown Lands - MNR - E000074 - 2001Sen HuNo ratings yet

- Research Question S Timeline Cotton InventionDocument5 pagesResearch Question S Timeline Cotton Inventionapi-480730245No ratings yet

Download as docx, pdf, or txt

You might also like

- Tax Presentation-29.01.2023Document25 pagesTax Presentation-29.01.2023Abhinav Parhi100% (2)

- Narrative Report-Virtual Parent's OrientationnDocument3 pagesNarrative Report-Virtual Parent's OrientationnApril Ramos Dimayuga95% (21)

- Sex, Drugs & Magick: A Journey Beyond LimitsDocument121 pagesSex, Drugs & Magick: A Journey Beyond Limitsvvvulpea80% (5)

- Boq For Box CulvertDocument2 pagesBoq For Box CulvertDaniel Okere100% (1)

- FY 2022-23 (AY 2023-24) - Taxguru - inDocument3 pagesFY 2022-23 (AY 2023-24) - Taxguru - inHarshilNo ratings yet

- Taxguru - In-Income Tax Rates For FY 2020-21 Amp FY 2021-22Document8 pagesTaxguru - In-Income Tax Rates For FY 2020-21 Amp FY 2021-22JiyalalNo ratings yet

- Tax Liability For The Assessment Years 2014-15 and 2015-16Document11 pagesTax Liability For The Assessment Years 2014-15 and 2015-16Accounting & TaxationNo ratings yet

- Income Tax Rates Assessment Year 2011-2012Document10 pagesIncome Tax Rates Assessment Year 2011-2012Pankaj KhannaNo ratings yet

- Guidance Note On Option For Old Vs New Tax Regime - FY22-23 & AY23-24 PDFDocument3 pagesGuidance Note On Option For Old Vs New Tax Regime - FY22-23 & AY23-24 PDFgowtham DevNo ratings yet

- Budget Synopsis 2015-16 PDFDocument12 pagesBudget Synopsis 2015-16 PDFBhagwan PalNo ratings yet

- Normal Tax Rates Applicable To An IndividualDocument12 pagesNormal Tax Rates Applicable To An IndividualAnonymous 9Yv6n5qvSNo ratings yet

- IT RatesDocument6 pagesIT RatesAnjali Krishna SNo ratings yet

- Tax Deduction - DR Sajjad Wani JKASDocument26 pagesTax Deduction - DR Sajjad Wani JKASMohmad Yousuf100% (1)

- Income Tax Slabs & Rates For Assessment Year 2013-14Document37 pagesIncome Tax Slabs & Rates For Assessment Year 2013-14Jigar RavalNo ratings yet

- Income Tax Slab FY 2023-24 and AY 2024-25 - New ADocument3 pagesIncome Tax Slab FY 2023-24 and AY 2024-25 - New ABagath SinghNo ratings yet

- Alternative Tax Regime (This Has Been Dealt in 1.1A of Chapter 1 in YourDocument6 pagesAlternative Tax Regime (This Has Been Dealt in 1.1A of Chapter 1 in YourRhea SharmaNo ratings yet

- Taxation Workbook 2022Document204 pagesTaxation Workbook 2022Navya GulatiNo ratings yet

- E PDF - Know Your Income Tax Rate AY 2021 22 23Document8 pagesE PDF - Know Your Income Tax Rate AY 2021 22 23CHANDAN CHANDUNo ratings yet

- Income Tax Slab FY 2014-15Document3 pagesIncome Tax Slab FY 2014-15zveeraNo ratings yet

- Notes On DTC BillDocument5 pagesNotes On DTC Billshikah sidarNo ratings yet

- Income Tax Calculator Calculate Income Tax For FY 2022-23Document1 pageIncome Tax Calculator Calculate Income Tax For FY 2022-23Vivek LakkakulaNo ratings yet

- How To Calculate Income TaxDocument4 pagesHow To Calculate Income TaxreemaNo ratings yet

- ITR DocumentDocument6 pagesITR DocumentRamesh BabuNo ratings yet

- Module-1 - Introduction & Basic Tax ComputationDocument24 pagesModule-1 - Introduction & Basic Tax Computationshaswat sharmaNo ratings yet

- Individual, HUF, AOP or BOIDocument4 pagesIndividual, HUF, AOP or BOIABC 123No ratings yet

- TDS On SalaryDocument5 pagesTDS On SalaryAato AatoNo ratings yet

- Latest Income Tax Slabs and Rates For FY 2013-14 and AS 2014-15Document6 pagesLatest Income Tax Slabs and Rates For FY 2013-14 and AS 2014-15Michaelben MichaelbenNo ratings yet

- Income Tax: Administrative Set-UpDocument25 pagesIncome Tax: Administrative Set-UpMohit RahejaNo ratings yet

- Individual Txation FY 203 24Document44 pagesIndividual Txation FY 203 24Smarty ShivamNo ratings yet

- Income Tax Slabs & Rates For Assessment Year 2014-15Document4 pagesIncome Tax Slabs & Rates For Assessment Year 2014-15ptk_guly3871No ratings yet

- DeferredDocument11 pagesDeferredShubham MaheshwariNo ratings yet

- Business Environment: Budget 2013-2014 AnalysisDocument11 pagesBusiness Environment: Budget 2013-2014 AnalysisKyle BaileyNo ratings yet

- IT Projection ToolDocument7 pagesIT Projection ToolsaurabhmanitNo ratings yet

- Benefits For Senior Citizens Very Senior Citizens - EnglishDocument8 pagesBenefits For Senior Citizens Very Senior Citizens - EnglishmonishaNo ratings yet

- IT Circular 2011-12Document56 pagesIT Circular 2011-12Narasimha SastryNo ratings yet

- Income Tax On SalaryDocument23 pagesIncome Tax On SalarySarvesh MishraNo ratings yet

- The List of Components Which You Can Use For Salary BreakupDocument8 pagesThe List of Components Which You Can Use For Salary BreakupAnonymous VhqxrXNo ratings yet

- India Budget 2011Document22 pagesIndia Budget 2011ashishgautamNo ratings yet

- Tax Rates As 2015-16Document1 pageTax Rates As 2015-16Jatin PatelNo ratings yet

- Note On Budget Proposals-2020Document4 pagesNote On Budget Proposals-2020Dhananjai SharmaNo ratings yet

- IT Calculator 14 15 Taxguru - inDocument16 pagesIT Calculator 14 15 Taxguru - inanirbanpwd76No ratings yet

- Individual Txation FY 2019 20 With Demo of Return FilingDocument73 pagesIndividual Txation FY 2019 20 With Demo of Return FilingGanesh PNo ratings yet

- Tax Update A.Y. 2015-16Document32 pagesTax Update A.Y. 2015-16Anil PatelNo ratings yet

- Taxation Flow PresentationDocument73 pagesTaxation Flow PresentationMohan ChoudharyNo ratings yet

- Tds SALARY FOR A.Y. 2011-12Document59 pagesTds SALARY FOR A.Y. 2011-12Pragnesh ShahNo ratings yet

- Ammendments in Direct TaxDocument37 pagesAmmendments in Direct TaxVipul KatariyaNo ratings yet

- Scenario 1# You Do Not Have Outstanding Tax LiabilityDocument7 pagesScenario 1# You Do Not Have Outstanding Tax LiabilityBhupendra SharmaNo ratings yet

- Tax Saving FY 2021-22 - FDocument30 pagesTax Saving FY 2021-22 - Fsapreswapnil8388No ratings yet

- Individual Taxation (Ay 2019-20)Document29 pagesIndividual Taxation (Ay 2019-20)Mudit SinghNo ratings yet

- Tax Slabs & Tax Saving Strategies For New Tax Payers 2011-12Document5 pagesTax Slabs & Tax Saving Strategies For New Tax Payers 2011-12channaveer sgNo ratings yet

- How To Calculate Ur Income TaxDocument3 pagesHow To Calculate Ur Income TaxrazeemshipNo ratings yet

- MATH PROJECT TOPIC 2 (Income Tax)Document7 pagesMATH PROJECT TOPIC 2 (Income Tax)avinamakadiaNo ratings yet

- Note On Budget Proposals-2020Document4 pagesNote On Budget Proposals-2020Karthik PenakaNo ratings yet

- 1 3+part+2Document28 pages1 3+part+2jaspreet kaurNo ratings yet

- Income-Tax-Slab 13-14Document2 pagesIncome-Tax-Slab 13-14rani26octNo ratings yet

- Finance Bill, 2012: Provisions Relating To Direct TaxesDocument36 pagesFinance Bill, 2012: Provisions Relating To Direct TaxessangeetsindanNo ratings yet

- Deduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009Document70 pagesDeduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009rhldxmNo ratings yet

- Ryhuqphqwri, QGLD 0Lqlvwu/Ri) LQDQFH 'Hsduwphqwri5Hyhqxh &Hqwudo%Rdugri'Luhfw7D (HVDocument24 pagesRyhuqphqwri, QGLD 0Lqlvwu/Ri) LQDQFH 'Hsduwphqwri5Hyhqxh &Hqwudo%Rdugri'Luhfw7D (HVNiraj JainNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Name: - Date: - Grade and Section: - Score: - Formative AssessmentDocument7 pagesName: - Date: - Grade and Section: - Score: - Formative AssessmentLey F. FajutaganaNo ratings yet

- The Voice On The Skin Self-Mutilation and MerleauDocument13 pagesThe Voice On The Skin Self-Mutilation and MerleauDr FreudNo ratings yet

- The Food Industry in Nigeria Development and QualiDocument6 pagesThe Food Industry in Nigeria Development and Qualimercy luwaNo ratings yet

- Application of Geomatry in BusinessDocument23 pagesApplication of Geomatry in BusinessSoummo ChakmaNo ratings yet

- Perception of Hostel StudentsDocument6 pagesPerception of Hostel StudentsKhairul Hazwan100% (3)

- Venezuelan Food Glossary Ver6Document1 pageVenezuelan Food Glossary Ver6Peter BehringerNo ratings yet

- Fever Tree: Agriculture, Forestry & FisheriesDocument16 pagesFever Tree: Agriculture, Forestry & FisheriesDylanNo ratings yet

- Toshiba Satellite C660 Compal LA-7202P PWWHA Delphi 10R Rev1.0 SchematicDocument43 pagesToshiba Satellite C660 Compal LA-7202P PWWHA Delphi 10R Rev1.0 Schematicpcs prasannaNo ratings yet

- Equity EssayDocument8 pagesEquity EssayTeeruVarasuNo ratings yet

- Soul Winning TractDocument2 pagesSoul Winning TractPaul Moiloa50% (2)

- Irregular Verbs Nueva Lista DuncanDocument2 pagesIrregular Verbs Nueva Lista DuncanAndrey Vargas MoralesNo ratings yet

- Once Upon The Time in America - Google Search PDFDocument1 pageOnce Upon The Time in America - Google Search PDFDiana KarchavaNo ratings yet

- Unit 5: Ind As 111: Joint ArrangementsDocument26 pagesUnit 5: Ind As 111: Joint ArrangementsDheeraj TurpunatiNo ratings yet

- Argument EssayDocument3 pagesArgument Essayapi-669204574No ratings yet

- GSIS TEMPLATE Fire Insurance Application Form (TRAD)Document3 pagesGSIS TEMPLATE Fire Insurance Application Form (TRAD)Ronan MaquidatoNo ratings yet

- Pengaruh Pemberian Tempe Kacang Hijau Sebagai Polen Pengganti Terhadap Penampilan Larva Lebah Pekerja Apis MelliferaDocument8 pagesPengaruh Pemberian Tempe Kacang Hijau Sebagai Polen Pengganti Terhadap Penampilan Larva Lebah Pekerja Apis MelliferaResti Amelia SusantiNo ratings yet

- Municipal Solid Waste ManagementDocument100 pagesMunicipal Solid Waste ManagementPremkumar T100% (1)

- Kamba Ramayanam IDocument701 pagesKamba Ramayanam IShubham BhatiaNo ratings yet

- Ucl Thesis Citation StyleDocument6 pagesUcl Thesis Citation Stylemaryburgsiouxfalls100% (1)

- Postmodernism and Its Comparative Education ImplicationsDocument18 pagesPostmodernism and Its Comparative Education ImplicationsLetta ZaglaNo ratings yet

- 01.worksheet-1 U1Document1 page01.worksheet-1 U1Jose Manuel AlcantaraNo ratings yet

- Naivas CP & SP Description Cost Price Selling Price %margins C.P S.P %marginsDocument12 pagesNaivas CP & SP Description Cost Price Selling Price %margins C.P S.P %marginsBonnie Maguathi MwauraNo ratings yet

- ShapeFuture Brochure2022 EnglishDocument36 pagesShapeFuture Brochure2022 EnglishJenifer Yajaira Rodríguez ChamorroNo ratings yet

- Course Handout Spreadsheet For ManagersDocument8 pagesCourse Handout Spreadsheet For ManagersSunil ChinnuNo ratings yet

- Pe 3 First QuizDocument1 pagePe 3 First QuizLoremer Delos Santos LiboonNo ratings yet

- Waterfront Boundaries For Grants of Public Crown Lands - MNR - E000074 - 2001Document3 pagesWaterfront Boundaries For Grants of Public Crown Lands - MNR - E000074 - 2001Sen HuNo ratings yet

- Research Question S Timeline Cotton InventionDocument5 pagesResearch Question S Timeline Cotton Inventionapi-480730245No ratings yet