UGBS April 2021 Assignment MPhil. MSc. and MBA

UGBS April 2021 Assignment MPhil. MSc. and MBA

You might also like

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Ipsas 1 and Ipsas 2Document6 pagesIpsas 1 and Ipsas 2Esther Akpan0% (1)

- Financial Statement AnalysisDocument6 pagesFinancial Statement AnalysisKimberly AsanteNo ratings yet

- IA 3 Final Assessment PDFDocument5 pagesIA 3 Final Assessment PDFJoy Miraflor Alinood100% (1)

- Sweat Bakery PlanDocument59 pagesSweat Bakery PlanShailaja RaghavendraNo ratings yet

- ACCT 402 AssignmentDocument5 pagesACCT 402 AssignmentDaniel TackieNo ratings yet

- Practice Question 1Document3 pagesPractice Question 1Josh JobsNo ratings yet

- Assignment 6 SolutionsDocument4 pagesAssignment 6 SolutionsjoanNo ratings yet

- Public Sector Accounting May 2021Document27 pagesPublic Sector Accounting May 2021GODSON NKUNUNo ratings yet

- Advanced Financial Accounting and Reporting 14 - NGAS: Straight Problems Problem 1Document6 pagesAdvanced Financial Accounting and Reporting 14 - NGAS: Straight Problems Problem 1Jem ValmonteNo ratings yet

- 2020 1 Accounting in Organisations and Society Assignment-3Document7 pages2020 1 Accounting in Organisations and Society Assignment-3Abs PangaderNo ratings yet

- Chapter 4 Governmental AccountingDocument5 pagesChapter 4 Governmental Accountingmohamad ali osmanNo ratings yet

- Cash ExampleDocument1 pageCash ExampleFRANCIS IAN ALBARACIN IINo ratings yet

- Solution To Practice Question-3Document16 pagesSolution To Practice Question-3Josh JobsNo ratings yet

- Chapter 4 Governmental AccountingDocument8 pagesChapter 4 Governmental Accountingmohamad ali osmanNo ratings yet

- Taxation of Banks Financial InstittutionsDocument7 pagesTaxation of Banks Financial InstittutionsTriila manillaNo ratings yet

- Simple Nonprofit Financial StatementDocument62 pagesSimple Nonprofit Financial StatementThabiso MosokotsoNo ratings yet

- The Institute of Chartered Accountants, Ghana November 2015 Professional Examinations Questions Public Sector Accounting and Finance (2.5)Document22 pagesThe Institute of Chartered Accountants, Ghana November 2015 Professional Examinations Questions Public Sector Accounting and Finance (2.5)Thomas nyade100% (1)

- Camille ManufacturingDocument4 pagesCamille ManufacturingChristina StephensonNo ratings yet

- May 2020 Professional Examiniations Public Sector Accounting and Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeDocument23 pagesMay 2020 Professional Examiniations Public Sector Accounting and Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeThomas nyadeNo ratings yet

- Complete Financial Statements With SCF Direcdt MethodDocument23 pagesComplete Financial Statements With SCF Direcdt MethodJuja FlorentinoNo ratings yet

- Psaf Revision Day 3 May 2023Document8 pagesPsaf Revision Day 3 May 2023Esther AkpanNo ratings yet

- Section B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?Document11 pagesSection B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?18071369 Nguyễn ThànhNo ratings yet

- Crash Landing On You Company Financial StatementsDocument6 pagesCrash Landing On You Company Financial StatementsEmar KimNo ratings yet

- Part F - Additional QuestionsDocument9 pagesPart F - Additional QuestionsDesmond Grasie ZumankyereNo ratings yet

- ACC 303 - Questions On Final AccountsDocument12 pagesACC 303 - Questions On Final AccountsOhene Asare PogastyNo ratings yet

- Corporation TEST PAPERDocument2 pagesCorporation TEST PAPERPrajwal ShettyNo ratings yet

- PSA Q & ADocument5 pagesPSA Q & Aq9dpc6fyd2No ratings yet

- ACCT 2105 Tutorial Exercises - Topic 4 - Income StatementDocument8 pagesACCT 2105 Tutorial Exercises - Topic 4 - Income StatementHoàng Trọng HiếuNo ratings yet

- 2020 Annual Budget Template AplayaDocument14 pages2020 Annual Budget Template Aplayacianomedina11No ratings yet

- Cash Flow Tutorial QnsDocument13 pagesCash Flow Tutorial QnsCristian Renatus100% (1)

- P64571RA Lcci Level 4 Certificate in Financial Accounting ASE20101 RB Sep 2020Document8 pagesP64571RA Lcci Level 4 Certificate in Financial Accounting ASE20101 RB Sep 2020Musthari KhanNo ratings yet

- Question 6 Chic Homes LTD GroupDocument5 pagesQuestion 6 Chic Homes LTD GroupsavagewolfieNo ratings yet

- Application Level Taxation II Nov Dec 2013Document3 pagesApplication Level Taxation II Nov Dec 2013MahediNo ratings yet

- Main 3 - Claveria, Jenny PDFDocument18 pagesMain 3 - Claveria, Jenny PDFSheena marie ClaveriaNo ratings yet

- Acp - Acc417 Case Study 1Document6 pagesAcp - Acc417 Case Study 1Faker MejiaNo ratings yet

- Week 4 P4.21 Modified Question PDFDocument1 pageWeek 4 P4.21 Modified Question PDFalexandraNo ratings yet

- Exercise 10 Statement of Cash Flows - 054935Document3 pagesExercise 10 Statement of Cash Flows - 054935Hoyo VerseNo ratings yet

- Chapter 46 Cash Flow ComprehensiveDocument8 pagesChapter 46 Cash Flow ComprehensiveCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

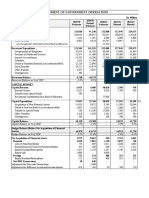

- Statement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Document2 pagesStatement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Yashas SridatNo ratings yet

- Chapter 19 in Class ExercisesDocument14 pagesChapter 19 in Class ExercisesByul ProductionsNo ratings yet

- CF Assignment 1 06102022 091143pmDocument1 pageCF Assignment 1 06102022 091143pmhadsem78No ratings yet

- Assignment Set 12 NOV 2018 1Document20 pagesAssignment Set 12 NOV 2018 1Jessa BeloyNo ratings yet

- ACCT 302 Financial Reporting II Tutorial Set 4-1Document8 pagesACCT 302 Financial Reporting II Tutorial Set 4-1Ohenewaa AppiahNo ratings yet

- Financial Accounting-Assignment-4Document4 pagesFinancial Accounting-Assignment-4Margaux JohannaNo ratings yet

- Final Individual Assignment - 4 Nov 2022Document6 pagesFinal Individual Assignment - 4 Nov 2022Vernice CuffyNo ratings yet

- Problem 3 56 GOVTDocument5 pagesProblem 3 56 GOVTskmasambongcouncilNo ratings yet

- Auswide Bank - Ic 0Document6 pagesAuswide Bank - Ic 0sagarg1998No ratings yet

- The Institute of Chartered Accountants of Nepal: Suggested Answers of Advanced TaxationDocument10 pagesThe Institute of Chartered Accountants of Nepal: Suggested Answers of Advanced TaxationNarendra KumarNo ratings yet

- Final ExaminationsDocument5 pagesFinal ExaminationsBilal Khan BangashNo ratings yet

- Mixed Income Earner ITR PreparationDocument2 pagesMixed Income Earner ITR PreparationTony Rose Arzaga100% (1)

- Business CombinationDocument3 pagesBusiness CombinationNicoleNo ratings yet

- For Revision of Income TaxDocument5 pagesFor Revision of Income TaxMA AttariNo ratings yet

- I1.2-Financial Reporting QPDocument8 pagesI1.2-Financial Reporting QPConstantin NdahimanaNo ratings yet

- Bank AccountingDocument8 pagesBank Accountinggordonomond2022No ratings yet

- 6jamolod Week6Document15 pages6jamolod Week6Jatha JamolodNo ratings yet

- Miriams Kitchen 9.30.21 FS 1Document21 pagesMiriams Kitchen 9.30.21 FS 1Kundai NellyNo ratings yet

- Bacc 2 and Bait 2 Group AssignmentDocument4 pagesBacc 2 and Bait 2 Group AssignmentVannyNo ratings yet

- Assignment 7 SolutionsDocument10 pagesAssignment 7 SolutionsjoanNo ratings yet

- Topic No. 2 - Statement of Cash Flows PDFDocument3 pagesTopic No. 2 - Statement of Cash Flows PDFSARAH ANDREA TORRESNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- REVISION Questions Pricing and ROIDocument3 pagesREVISION Questions Pricing and ROIsaadaltamash920No ratings yet

- Activity 5 - Chapter 22 Investment Property (Cash Surrender Value) Problem 22-2 (IFRS)Document6 pagesActivity 5 - Chapter 22 Investment Property (Cash Surrender Value) Problem 22-2 (IFRS)WeStan LegendsNo ratings yet

- Forum S11 Thread Soal Valuation of Inventories 1-FIFO, LIFO, and AVERAGE - Diaz Hesron Deo Simorangkir - 2602202526Document2 pagesForum S11 Thread Soal Valuation of Inventories 1-FIFO, LIFO, and AVERAGE - Diaz Hesron Deo Simorangkir - 2602202526Diaz Hesron Deo SimorangkirNo ratings yet

- Week 7 Homework Lisa ChandlerDocument13 pagesWeek 7 Homework Lisa ChandlerShopno ChuraNo ratings yet

- ACCT2511 Topic 2 Tutorial Solutions STUDENTDocument8 pagesACCT2511 Topic 2 Tutorial Solutions STUDENTKJSAdNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument9 pages© The Institute of Chartered Accountants of IndiaVishesh JainNo ratings yet

- 40Chpt 12&13FINDocument20 pages40Chpt 12&13FINthe__wude8133No ratings yet

- Business O Level Notes - Chapter 16 PDFDocument4 pagesBusiness O Level Notes - Chapter 16 PDFHeba KhattabNo ratings yet

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Document45 pagesSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNo ratings yet

- 7 Cost of ProductionDocument29 pages7 Cost of ProductionEsha ChaudharyNo ratings yet

- Depreciation MethodsDocument30 pagesDepreciation MethodsJc UyNo ratings yet

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- Income Statement and Statement of Cash FlowsDocument29 pagesIncome Statement and Statement of Cash FlowsNadine Santiago100% (1)

- Body - Internship Report On Ejab GroupDocument42 pagesBody - Internship Report On Ejab GroupAbdullah Muhammad DhruboNo ratings yet

- PFRS 1 - First Time Adoption of PFRSDocument2 pagesPFRS 1 - First Time Adoption of PFRSRicaNo ratings yet

- +2 Accountancy CA - Orukkam 2023-HsscommerceDocument37 pages+2 Accountancy CA - Orukkam 2023-Hsscommercesinanmp0973No ratings yet

- Financial Analysis of Tata Motors: Submitted by Binni.M Semester-2 Mba-Ib ROLL - No-6Document19 pagesFinancial Analysis of Tata Motors: Submitted by Binni.M Semester-2 Mba-Ib ROLL - No-6binnivenus100% (1)

- NP Ex 9-4Document2 pagesNP Ex 9-4anand sennNo ratings yet

- Practical Accounting 2.1Document10 pagesPractical Accounting 2.1Chris Aruh BorsalinaNo ratings yet

- Analysis & Interpretation: Prepared By: Sir Hamza Abdul HaqDocument10 pagesAnalysis & Interpretation: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Managerial Accounting 13th Edition Warren Solutions Manual DownloadDocument71 pagesManagerial Accounting 13th Edition Warren Solutions Manual DownloadRose Speers100% (22)

- 3rd QUARTER EXAMS WEEK 10 FABMDocument6 pages3rd QUARTER EXAMS WEEK 10 FABMLenlyn Fallarcuna Falamig100% (5)

- Audit of Item of FS Notes by CA Kapil GoyalDocument9 pagesAudit of Item of FS Notes by CA Kapil GoyalAbhimanyu Kumar ranaNo ratings yet

- 01.payback Period and NPV Their Different Cash FlowsDocument7 pages01.payback Period and NPV Their Different Cash FlowsAndryNo ratings yet

- 14) Inventories and Biological AssetsDocument10 pages14) Inventories and Biological AssetsDavid JosephNo ratings yet

- Shareholders' Equity: 2. Journal Entry MethodDocument5 pagesShareholders' Equity: 2. Journal Entry MethodSuzette Villalino100% (1)

- Dalmia Cement (Bharat) LTDDocument8 pagesDalmia Cement (Bharat) LTDRemonNo ratings yet

- Financial Accounting & Reporting IIDocument6 pagesFinancial Accounting & Reporting IIKendrick PajarinNo ratings yet

- Spring 2022-FAR-1 - Comprehensive Question On IAS33 IAS8 IAS1 IAS7Document7 pagesSpring 2022-FAR-1 - Comprehensive Question On IAS33 IAS8 IAS1 IAS7Dua FarmoodNo ratings yet

Download as pdf or txt

You might also like

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Ipsas 1 and Ipsas 2Document6 pagesIpsas 1 and Ipsas 2Esther Akpan0% (1)

- Financial Statement AnalysisDocument6 pagesFinancial Statement AnalysisKimberly AsanteNo ratings yet

- IA 3 Final Assessment PDFDocument5 pagesIA 3 Final Assessment PDFJoy Miraflor Alinood100% (1)

- Sweat Bakery PlanDocument59 pagesSweat Bakery PlanShailaja RaghavendraNo ratings yet

- ACCT 402 AssignmentDocument5 pagesACCT 402 AssignmentDaniel TackieNo ratings yet

- Practice Question 1Document3 pagesPractice Question 1Josh JobsNo ratings yet

- Assignment 6 SolutionsDocument4 pagesAssignment 6 SolutionsjoanNo ratings yet

- Public Sector Accounting May 2021Document27 pagesPublic Sector Accounting May 2021GODSON NKUNUNo ratings yet

- Advanced Financial Accounting and Reporting 14 - NGAS: Straight Problems Problem 1Document6 pagesAdvanced Financial Accounting and Reporting 14 - NGAS: Straight Problems Problem 1Jem ValmonteNo ratings yet

- 2020 1 Accounting in Organisations and Society Assignment-3Document7 pages2020 1 Accounting in Organisations and Society Assignment-3Abs PangaderNo ratings yet

- Chapter 4 Governmental AccountingDocument5 pagesChapter 4 Governmental Accountingmohamad ali osmanNo ratings yet

- Cash ExampleDocument1 pageCash ExampleFRANCIS IAN ALBARACIN IINo ratings yet

- Solution To Practice Question-3Document16 pagesSolution To Practice Question-3Josh JobsNo ratings yet

- Chapter 4 Governmental AccountingDocument8 pagesChapter 4 Governmental Accountingmohamad ali osmanNo ratings yet

- Taxation of Banks Financial InstittutionsDocument7 pagesTaxation of Banks Financial InstittutionsTriila manillaNo ratings yet

- Simple Nonprofit Financial StatementDocument62 pagesSimple Nonprofit Financial StatementThabiso MosokotsoNo ratings yet

- The Institute of Chartered Accountants, Ghana November 2015 Professional Examinations Questions Public Sector Accounting and Finance (2.5)Document22 pagesThe Institute of Chartered Accountants, Ghana November 2015 Professional Examinations Questions Public Sector Accounting and Finance (2.5)Thomas nyade100% (1)

- Camille ManufacturingDocument4 pagesCamille ManufacturingChristina StephensonNo ratings yet

- May 2020 Professional Examiniations Public Sector Accounting and Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeDocument23 pagesMay 2020 Professional Examiniations Public Sector Accounting and Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeThomas nyadeNo ratings yet

- Complete Financial Statements With SCF Direcdt MethodDocument23 pagesComplete Financial Statements With SCF Direcdt MethodJuja FlorentinoNo ratings yet

- Psaf Revision Day 3 May 2023Document8 pagesPsaf Revision Day 3 May 2023Esther AkpanNo ratings yet

- Section B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?Document11 pagesSection B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?18071369 Nguyễn ThànhNo ratings yet

- Crash Landing On You Company Financial StatementsDocument6 pagesCrash Landing On You Company Financial StatementsEmar KimNo ratings yet

- Part F - Additional QuestionsDocument9 pagesPart F - Additional QuestionsDesmond Grasie ZumankyereNo ratings yet

- ACC 303 - Questions On Final AccountsDocument12 pagesACC 303 - Questions On Final AccountsOhene Asare PogastyNo ratings yet

- Corporation TEST PAPERDocument2 pagesCorporation TEST PAPERPrajwal ShettyNo ratings yet

- PSA Q & ADocument5 pagesPSA Q & Aq9dpc6fyd2No ratings yet

- ACCT 2105 Tutorial Exercises - Topic 4 - Income StatementDocument8 pagesACCT 2105 Tutorial Exercises - Topic 4 - Income StatementHoàng Trọng HiếuNo ratings yet

- 2020 Annual Budget Template AplayaDocument14 pages2020 Annual Budget Template Aplayacianomedina11No ratings yet

- Cash Flow Tutorial QnsDocument13 pagesCash Flow Tutorial QnsCristian Renatus100% (1)

- P64571RA Lcci Level 4 Certificate in Financial Accounting ASE20101 RB Sep 2020Document8 pagesP64571RA Lcci Level 4 Certificate in Financial Accounting ASE20101 RB Sep 2020Musthari KhanNo ratings yet

- Question 6 Chic Homes LTD GroupDocument5 pagesQuestion 6 Chic Homes LTD GroupsavagewolfieNo ratings yet

- Application Level Taxation II Nov Dec 2013Document3 pagesApplication Level Taxation II Nov Dec 2013MahediNo ratings yet

- Main 3 - Claveria, Jenny PDFDocument18 pagesMain 3 - Claveria, Jenny PDFSheena marie ClaveriaNo ratings yet

- Acp - Acc417 Case Study 1Document6 pagesAcp - Acc417 Case Study 1Faker MejiaNo ratings yet

- Week 4 P4.21 Modified Question PDFDocument1 pageWeek 4 P4.21 Modified Question PDFalexandraNo ratings yet

- Exercise 10 Statement of Cash Flows - 054935Document3 pagesExercise 10 Statement of Cash Flows - 054935Hoyo VerseNo ratings yet

- Chapter 46 Cash Flow ComprehensiveDocument8 pagesChapter 46 Cash Flow ComprehensiveCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

- Statement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Document2 pagesStatement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Yashas SridatNo ratings yet

- Chapter 19 in Class ExercisesDocument14 pagesChapter 19 in Class ExercisesByul ProductionsNo ratings yet

- CF Assignment 1 06102022 091143pmDocument1 pageCF Assignment 1 06102022 091143pmhadsem78No ratings yet

- Assignment Set 12 NOV 2018 1Document20 pagesAssignment Set 12 NOV 2018 1Jessa BeloyNo ratings yet

- ACCT 302 Financial Reporting II Tutorial Set 4-1Document8 pagesACCT 302 Financial Reporting II Tutorial Set 4-1Ohenewaa AppiahNo ratings yet

- Financial Accounting-Assignment-4Document4 pagesFinancial Accounting-Assignment-4Margaux JohannaNo ratings yet

- Final Individual Assignment - 4 Nov 2022Document6 pagesFinal Individual Assignment - 4 Nov 2022Vernice CuffyNo ratings yet

- Problem 3 56 GOVTDocument5 pagesProblem 3 56 GOVTskmasambongcouncilNo ratings yet

- Auswide Bank - Ic 0Document6 pagesAuswide Bank - Ic 0sagarg1998No ratings yet

- The Institute of Chartered Accountants of Nepal: Suggested Answers of Advanced TaxationDocument10 pagesThe Institute of Chartered Accountants of Nepal: Suggested Answers of Advanced TaxationNarendra KumarNo ratings yet

- Final ExaminationsDocument5 pagesFinal ExaminationsBilal Khan BangashNo ratings yet

- Mixed Income Earner ITR PreparationDocument2 pagesMixed Income Earner ITR PreparationTony Rose Arzaga100% (1)

- Business CombinationDocument3 pagesBusiness CombinationNicoleNo ratings yet

- For Revision of Income TaxDocument5 pagesFor Revision of Income TaxMA AttariNo ratings yet

- I1.2-Financial Reporting QPDocument8 pagesI1.2-Financial Reporting QPConstantin NdahimanaNo ratings yet

- Bank AccountingDocument8 pagesBank Accountinggordonomond2022No ratings yet

- 6jamolod Week6Document15 pages6jamolod Week6Jatha JamolodNo ratings yet

- Miriams Kitchen 9.30.21 FS 1Document21 pagesMiriams Kitchen 9.30.21 FS 1Kundai NellyNo ratings yet

- Bacc 2 and Bait 2 Group AssignmentDocument4 pagesBacc 2 and Bait 2 Group AssignmentVannyNo ratings yet

- Assignment 7 SolutionsDocument10 pagesAssignment 7 SolutionsjoanNo ratings yet

- Topic No. 2 - Statement of Cash Flows PDFDocument3 pagesTopic No. 2 - Statement of Cash Flows PDFSARAH ANDREA TORRESNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- REVISION Questions Pricing and ROIDocument3 pagesREVISION Questions Pricing and ROIsaadaltamash920No ratings yet

- Activity 5 - Chapter 22 Investment Property (Cash Surrender Value) Problem 22-2 (IFRS)Document6 pagesActivity 5 - Chapter 22 Investment Property (Cash Surrender Value) Problem 22-2 (IFRS)WeStan LegendsNo ratings yet

- Forum S11 Thread Soal Valuation of Inventories 1-FIFO, LIFO, and AVERAGE - Diaz Hesron Deo Simorangkir - 2602202526Document2 pagesForum S11 Thread Soal Valuation of Inventories 1-FIFO, LIFO, and AVERAGE - Diaz Hesron Deo Simorangkir - 2602202526Diaz Hesron Deo SimorangkirNo ratings yet

- Week 7 Homework Lisa ChandlerDocument13 pagesWeek 7 Homework Lisa ChandlerShopno ChuraNo ratings yet

- ACCT2511 Topic 2 Tutorial Solutions STUDENTDocument8 pagesACCT2511 Topic 2 Tutorial Solutions STUDENTKJSAdNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument9 pages© The Institute of Chartered Accountants of IndiaVishesh JainNo ratings yet

- 40Chpt 12&13FINDocument20 pages40Chpt 12&13FINthe__wude8133No ratings yet

- Business O Level Notes - Chapter 16 PDFDocument4 pagesBusiness O Level Notes - Chapter 16 PDFHeba KhattabNo ratings yet

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Document45 pagesSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNo ratings yet

- 7 Cost of ProductionDocument29 pages7 Cost of ProductionEsha ChaudharyNo ratings yet

- Depreciation MethodsDocument30 pagesDepreciation MethodsJc UyNo ratings yet

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- Income Statement and Statement of Cash FlowsDocument29 pagesIncome Statement and Statement of Cash FlowsNadine Santiago100% (1)

- Body - Internship Report On Ejab GroupDocument42 pagesBody - Internship Report On Ejab GroupAbdullah Muhammad DhruboNo ratings yet

- PFRS 1 - First Time Adoption of PFRSDocument2 pagesPFRS 1 - First Time Adoption of PFRSRicaNo ratings yet

- +2 Accountancy CA - Orukkam 2023-HsscommerceDocument37 pages+2 Accountancy CA - Orukkam 2023-Hsscommercesinanmp0973No ratings yet

- Financial Analysis of Tata Motors: Submitted by Binni.M Semester-2 Mba-Ib ROLL - No-6Document19 pagesFinancial Analysis of Tata Motors: Submitted by Binni.M Semester-2 Mba-Ib ROLL - No-6binnivenus100% (1)

- NP Ex 9-4Document2 pagesNP Ex 9-4anand sennNo ratings yet

- Practical Accounting 2.1Document10 pagesPractical Accounting 2.1Chris Aruh BorsalinaNo ratings yet

- Analysis & Interpretation: Prepared By: Sir Hamza Abdul HaqDocument10 pagesAnalysis & Interpretation: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Managerial Accounting 13th Edition Warren Solutions Manual DownloadDocument71 pagesManagerial Accounting 13th Edition Warren Solutions Manual DownloadRose Speers100% (22)

- 3rd QUARTER EXAMS WEEK 10 FABMDocument6 pages3rd QUARTER EXAMS WEEK 10 FABMLenlyn Fallarcuna Falamig100% (5)

- Audit of Item of FS Notes by CA Kapil GoyalDocument9 pagesAudit of Item of FS Notes by CA Kapil GoyalAbhimanyu Kumar ranaNo ratings yet

- 01.payback Period and NPV Their Different Cash FlowsDocument7 pages01.payback Period and NPV Their Different Cash FlowsAndryNo ratings yet

- 14) Inventories and Biological AssetsDocument10 pages14) Inventories and Biological AssetsDavid JosephNo ratings yet

- Shareholders' Equity: 2. Journal Entry MethodDocument5 pagesShareholders' Equity: 2. Journal Entry MethodSuzette Villalino100% (1)

- Dalmia Cement (Bharat) LTDDocument8 pagesDalmia Cement (Bharat) LTDRemonNo ratings yet

- Financial Accounting & Reporting IIDocument6 pagesFinancial Accounting & Reporting IIKendrick PajarinNo ratings yet

- Spring 2022-FAR-1 - Comprehensive Question On IAS33 IAS8 IAS1 IAS7Document7 pagesSpring 2022-FAR-1 - Comprehensive Question On IAS33 IAS8 IAS1 IAS7Dua FarmoodNo ratings yet