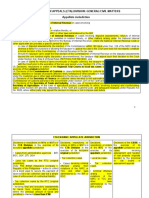

Jurisdiction of The Court of Appeals: Decision by MTC

Jurisdiction of The Court of Appeals: Decision by MTC

You might also like

- Modes of Appeal TableDocument3 pagesModes of Appeal TablemarydalemNo ratings yet

- Management by Objectives at Coca-ColaDocument3 pagesManagement by Objectives at Coca-ColaAlessandra MihaelaNo ratings yet

- Court of Tax Appeals (Cta) Division: General/Civil Matters Appellate JurisdictionDocument7 pagesCourt of Tax Appeals (Cta) Division: General/Civil Matters Appellate JurisdictionClarisse ZaplanNo ratings yet

- Taxation Law ReviewerDocument2 pagesTaxation Law ReviewerGolden LightphNo ratings yet

- Development Bank of The Philippines vs. CADocument2 pagesDevelopment Bank of The Philippines vs. CAJANNNo ratings yet

- TABLE 3: Procedure in Criminal CasesDocument1 pageTABLE 3: Procedure in Criminal CasesJP JimenezNo ratings yet

- Tax Report HandoutDocument4 pagesTax Report HandoutJune FourNo ratings yet

- Quick Rundown of The Protest ProcedureDocument5 pagesQuick Rundown of The Protest ProcedureYasha Min HNo ratings yet

- Constitutionality or An OrdinanceDocument2 pagesConstitutionality or An OrdinanceBINAYAO NAIZA MAENo ratings yet

- Court of Tax AppealsDocument3 pagesCourt of Tax AppealsReniel Belle AgregadoNo ratings yet

- Notes On Jurisdiction and CTA Proceedings by Prof. Eric RecaldeDocument14 pagesNotes On Jurisdiction and CTA Proceedings by Prof. Eric RecaldeDaisyDianeDeGuzmanNo ratings yet

- R.A. 9282, Section 7. Jurisdiction Exclusive Appellate Jurisdiction To Review by AppealDocument8 pagesR.A. 9282, Section 7. Jurisdiction Exclusive Appellate Jurisdiction To Review by AppealPJ SLSRNo ratings yet

- TreeDocument1 pageTreeEricaNo ratings yet

- Rule 40: Appeal From MTC To RTCDocument14 pagesRule 40: Appeal From MTC To RTCKin Pearly FloresNo ratings yet

- City of Manila V Grecia CuerdoDocument3 pagesCity of Manila V Grecia Cuerdoaspiringlawyer1234No ratings yet

- Diagram Appeals OverviewDocument2 pagesDiagram Appeals OverviewRen Concha100% (2)

- Civil Procedure Finals NotesDocument10 pagesCivil Procedure Finals NotesMaria Recheille Banac KinazoNo ratings yet

- Taxation Law - CTADocument7 pagesTaxation Law - CTARia Kriselle Francia PabaleNo ratings yet

- Outline of Procedure in The Court of Tax Appeals (Cta) Appeal To The CTA Division Appeal To The Supreme Court Appeal To The Cta en BancDocument1 pageOutline of Procedure in The Court of Tax Appeals (Cta) Appeal To The CTA Division Appeal To The Supreme Court Appeal To The Cta en BancRaymond RogacionNo ratings yet

- CTA Jurisdiction (Updated)Document2 pagesCTA Jurisdiction (Updated)Andie Player100% (1)

- CTA JurisdictionDocument6 pagesCTA JurisdictionUfbNo ratings yet

- Civil Aspect Collection CasesDocument18 pagesCivil Aspect Collection CasesHNicdaoNo ratings yet

- National Power Corporation vs. Municipal Government of NavotasDocument11 pagesNational Power Corporation vs. Municipal Government of NavotasEvelyn TocgongnaNo ratings yet

- A. Jurisdiction of The Court of Tax Appeals: 1. Civil CasesDocument7 pagesA. Jurisdiction of The Court of Tax Appeals: 1. Civil CasesRovi Anne IgoyNo ratings yet

- ASSOCIATED BANK Vs CADocument3 pagesASSOCIATED BANK Vs CACedric100% (1)

- Tax Reviewer: Law of Basic Taxation in The Philippines Chapter 8: Taxpayer'S RemediesDocument4 pagesTax Reviewer: Law of Basic Taxation in The Philippines Chapter 8: Taxpayer'S RemediesMariko IwakiNo ratings yet

- 4 Commissioner - of - Internal - Revenue - v. - CTA (RESOLUTION)Document6 pages4 Commissioner - of - Internal - Revenue - v. - CTA (RESOLUTION)ervingabralagbonNo ratings yet

- Mediation - Am No 11-1-5-Sc-PhiljaDocument11 pagesMediation - Am No 11-1-5-Sc-PhiljaAlNo ratings yet

- Tax2 TaxremDocument1 pageTax2 TaxremLeica JaymeNo ratings yet

- SMART and PILTEL Vs NTCDocument1 pageSMART and PILTEL Vs NTCShaira Mae CuevillasNo ratings yet

- City of Manila vs. Hon. Caridad Grecia-Cuerdo, RTC Pasay Et AlDocument6 pagesCity of Manila vs. Hon. Caridad Grecia-Cuerdo, RTC Pasay Et AlAP CruzNo ratings yet

- RemediesDocument14 pagesRemediesKent-Kent VillaceranNo ratings yet

- Rem Part IiDocument7 pagesRem Part IiVIctor AlfilerNo ratings yet

- 31 Insular Vs Far EastDocument14 pages31 Insular Vs Far EastFairyssa Bianca SagotNo ratings yet

- Insular Savings Bank v. Far East Bank and Trust CompanyDocument11 pagesInsular Savings Bank v. Far East Bank and Trust CompanyJoshua MaulaNo ratings yet

- Tax 2 NotesDocument3 pagesTax 2 NotesJoyceNo ratings yet

- CIR v. Hedcor Sibulan, Inc.Document2 pagesCIR v. Hedcor Sibulan, Inc.SophiaFrancescaEspinosa100% (1)

- Uniform LayoutDocument7 pagesUniform LayoutJade CoritanaNo ratings yet

- Court of Tax Appeals: by Anna Alyssa J. RobledoDocument52 pagesCourt of Tax Appeals: by Anna Alyssa J. RobledoVal Justin DeatrasNo ratings yet

- Chapter 9: Court Tax Appeals: Tax Reviewer: Law of Basic Taxation in The PhilippinesDocument4 pagesChapter 9: Court Tax Appeals: Tax Reviewer: Law of Basic Taxation in The PhilippinesMino GensonNo ratings yet

- Judicial Action Tax + CasesDocument28 pagesJudicial Action Tax + CasesGillian BrionesNo ratings yet

- Theory and Basis of TaxationDocument3 pagesTheory and Basis of TaxationBai Johara SinsuatNo ratings yet

- Bir Vs KepcoDocument2 pagesBir Vs KepcoJoseph SalidoNo ratings yet

- CLJ4 Chapter 9Document18 pagesCLJ4 Chapter 9Jules Karim A. AragonNo ratings yet

- BM 1755Document3 pagesBM 1755Faith TangoNo ratings yet

- Specpro ReviewerDocument24 pagesSpecpro Reviewerdaryl canozaNo ratings yet

- City of Manila Vs Judge CuerdoDocument21 pagesCity of Manila Vs Judge CuerdoRegina Rae LuzadasNo ratings yet

- Ursal V Court of Tax Appeals: Judicial RemediesDocument4 pagesUrsal V Court of Tax Appeals: Judicial RemediesAileen Love ReyesNo ratings yet

- I. Civil Procedure:: ST NDDocument4 pagesI. Civil Procedure:: ST NDRheaj AureoNo ratings yet

- Rule 42, Section 1-4 - MAGNODocument38 pagesRule 42, Section 1-4 - MAGNOMay RMNo ratings yet

- Commissioner of Internal Revenue vs. Kepco Ilijan Corporation G.R. No.199422, 21 June 2016Document2 pagesCommissioner of Internal Revenue vs. Kepco Ilijan Corporation G.R. No.199422, 21 June 2016Chiic-chiic SalamidaNo ratings yet

- Rule 42, Section 1-4 - MAGNODocument29 pagesRule 42, Section 1-4 - MAGNOMay RMNo ratings yet

- Adr - Emd Exam ReviewerDocument3 pagesAdr - Emd Exam ReviewerElycrisjoe Dela CuestaNo ratings yet

- Finals Personal Study Guide Tax2Document116 pagesFinals Personal Study Guide Tax2TeacherEliNo ratings yet

- Flowchart LGU TaxesDocument1 pageFlowchart LGU TaxesHermay BanarioNo ratings yet

- Admin - V - 3. Smart and Piltel Vs NTC GR No. 151908Document2 pagesAdmin - V - 3. Smart and Piltel Vs NTC GR No. 151908Ervin Franz Mayor CuevillasNo ratings yet

- Insular Savings Bank v. FEBTCDocument2 pagesInsular Savings Bank v. FEBTCHilary MostajoNo ratings yet

- Tax Flowchart Remedies (Tokie)Document9 pagesTax Flowchart Remedies (Tokie)Tokie TokiNo ratings yet

- LC Dismissed The Case W/o TM RTCDocument2 pagesLC Dismissed The Case W/o TM RTCMary Jobeth E. PallasigueNo ratings yet

- REM 1st AssignDocument9 pagesREM 1st AssignTokie TokiNo ratings yet

- California Supreme Court Petition: S173448 – Denied Without OpinionFrom EverandCalifornia Supreme Court Petition: S173448 – Denied Without OpinionRating: 4 out of 5 stars4/5 (1)

- SPL Notes FinalsDocument17 pagesSPL Notes FinalsJoh SuhNo ratings yet

- Special Commercial Laws Case DigestDocument29 pagesSpecial Commercial Laws Case DigestJoh SuhNo ratings yet

- Taxation ReviewerDocument9 pagesTaxation ReviewerJoh SuhNo ratings yet

- Arraignment PleaDocument4 pagesArraignment PleaJoh SuhNo ratings yet

- Anti Online Child PornographyDocument23 pagesAnti Online Child PornographyJoh SuhNo ratings yet

- Comm Rev NotesDocument4 pagesComm Rev NotesJoh SuhNo ratings yet

- Crim Law Lockdown Lecture - Art. 316 319Document7 pagesCrim Law Lockdown Lecture - Art. 316 319Joh SuhNo ratings yet

- Crim Law Lockdown Lecture - Art. 332Document3 pagesCrim Law Lockdown Lecture - Art. 332Joh SuhNo ratings yet

- Corpo Notes 01302023Document4 pagesCorpo Notes 01302023Joh SuhNo ratings yet

- Chapter 6 DEVELOPING STRATEGIC ALTERNATIVESDocument31 pagesChapter 6 DEVELOPING STRATEGIC ALTERNATIVESSheeza AsharNo ratings yet

- Sample 1673514368545Document2 pagesSample 1673514368545Sonm NegiNo ratings yet

- Gen Maths 07Document26 pagesGen Maths 07Sibin G ThomasNo ratings yet

- Dream2Success: About UsDocument3 pagesDream2Success: About UsGionee P2No ratings yet

- Fi32BPP Course NotesDocument384 pagesFi32BPP Course NotesZ XNNo ratings yet

- Market StructuresDocument59 pagesMarket StructuresCharlene Mae GraciasNo ratings yet

- Organizational Management Assignment On Coca ColaDocument11 pagesOrganizational Management Assignment On Coca ColaVix100% (1)

- Ledger TemplateDocument7 pagesLedger TemplateIts SaoirseNo ratings yet

- Complaint For Foreclosure of Real Estate MortgageDocument2 pagesComplaint For Foreclosure of Real Estate MortgageTere Tongson100% (1)

- 5.2 Cupcake ChallengeDocument294 pages5.2 Cupcake ChallengeNhlanhla MpofuNo ratings yet

- Indian Contract Act - IiDocument193 pagesIndian Contract Act - IiPramod ShuklaNo ratings yet

- The Performance Interest in The Law of TrustsDocument34 pagesThe Performance Interest in The Law of TrustsEve AthanasekouNo ratings yet

- CPE Presentation 1Document5 pagesCPE Presentation 1Carlos GarciaNo ratings yet

- Baby Bulls Mega Sectoral AnalysisDocument10 pagesBaby Bulls Mega Sectoral Analysisdaddyyankee995No ratings yet

- Mobile Banking: Mobile Banking Is A Service Provided by A Bank or Other Financial Institution That Allows ItsDocument11 pagesMobile Banking: Mobile Banking Is A Service Provided by A Bank or Other Financial Institution That Allows Itsএক মুঠো স্বপ্নNo ratings yet

- BrexitDocument8 pagesBrexitKomal RaniNo ratings yet

- Testing: Software Engineering Sommerville - Chapter 4,27 and 28Document29 pagesTesting: Software Engineering Sommerville - Chapter 4,27 and 28VCRajanNo ratings yet

- Online Agriculture Support System For Bridging Farmer-Consumer ExpectationsDocument4 pagesOnline Agriculture Support System For Bridging Farmer-Consumer ExpectationsInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- 17, 29 Dalisay Investments vs. SSS DigestDocument7 pages17, 29 Dalisay Investments vs. SSS DigestBay NazarenoNo ratings yet

- Supply Chain Management (3rd Edition) : Managing Economies of Scale in The Supply Chain: Cycle InventoryDocument45 pagesSupply Chain Management (3rd Edition) : Managing Economies of Scale in The Supply Chain: Cycle InventoryVinoadh Kumar KrishnanNo ratings yet

- Securityproductsmarketing AcasestudyDocument8 pagesSecurityproductsmarketing AcasestudyMuhammad Rehan NasirNo ratings yet

- Agro Tech Foods and The Branded Pulses SegmentDocument13 pagesAgro Tech Foods and The Branded Pulses SegmentManuel HijarNo ratings yet

- Crane Hire and Contract Lift-090626 PDFDocument6 pagesCrane Hire and Contract Lift-090626 PDFANIBAL MARQUEZNo ratings yet

- Presentation On MR Azim PremjiDocument13 pagesPresentation On MR Azim PremjiAnkur BhatiNo ratings yet

- Building On StrengthDocument292 pagesBuilding On StrengthSouradeep SanyalNo ratings yet

- Pune Institute of Business Management: BATCH 2019 - 2021Document24 pagesPune Institute of Business Management: BATCH 2019 - 2021Pragati ChaudharyNo ratings yet

- Student Profile BookDocument67 pagesStudent Profile BookGautam SharmaNo ratings yet

- Garment Manufacturing ProcessDocument54 pagesGarment Manufacturing Processroselyn ayensa100% (1)

- IPC PL 14 04 Issue 4Document27 pagesIPC PL 14 04 Issue 4saladinNo ratings yet

Download as docx, pdf, or txt

You might also like

- Modes of Appeal TableDocument3 pagesModes of Appeal TablemarydalemNo ratings yet

- Management by Objectives at Coca-ColaDocument3 pagesManagement by Objectives at Coca-ColaAlessandra MihaelaNo ratings yet

- Court of Tax Appeals (Cta) Division: General/Civil Matters Appellate JurisdictionDocument7 pagesCourt of Tax Appeals (Cta) Division: General/Civil Matters Appellate JurisdictionClarisse ZaplanNo ratings yet

- Taxation Law ReviewerDocument2 pagesTaxation Law ReviewerGolden LightphNo ratings yet

- Development Bank of The Philippines vs. CADocument2 pagesDevelopment Bank of The Philippines vs. CAJANNNo ratings yet

- TABLE 3: Procedure in Criminal CasesDocument1 pageTABLE 3: Procedure in Criminal CasesJP JimenezNo ratings yet

- Tax Report HandoutDocument4 pagesTax Report HandoutJune FourNo ratings yet

- Quick Rundown of The Protest ProcedureDocument5 pagesQuick Rundown of The Protest ProcedureYasha Min HNo ratings yet

- Constitutionality or An OrdinanceDocument2 pagesConstitutionality or An OrdinanceBINAYAO NAIZA MAENo ratings yet

- Court of Tax AppealsDocument3 pagesCourt of Tax AppealsReniel Belle AgregadoNo ratings yet

- Notes On Jurisdiction and CTA Proceedings by Prof. Eric RecaldeDocument14 pagesNotes On Jurisdiction and CTA Proceedings by Prof. Eric RecaldeDaisyDianeDeGuzmanNo ratings yet

- R.A. 9282, Section 7. Jurisdiction Exclusive Appellate Jurisdiction To Review by AppealDocument8 pagesR.A. 9282, Section 7. Jurisdiction Exclusive Appellate Jurisdiction To Review by AppealPJ SLSRNo ratings yet

- TreeDocument1 pageTreeEricaNo ratings yet

- Rule 40: Appeal From MTC To RTCDocument14 pagesRule 40: Appeal From MTC To RTCKin Pearly FloresNo ratings yet

- City of Manila V Grecia CuerdoDocument3 pagesCity of Manila V Grecia Cuerdoaspiringlawyer1234No ratings yet

- Diagram Appeals OverviewDocument2 pagesDiagram Appeals OverviewRen Concha100% (2)

- Civil Procedure Finals NotesDocument10 pagesCivil Procedure Finals NotesMaria Recheille Banac KinazoNo ratings yet

- Taxation Law - CTADocument7 pagesTaxation Law - CTARia Kriselle Francia PabaleNo ratings yet

- Outline of Procedure in The Court of Tax Appeals (Cta) Appeal To The CTA Division Appeal To The Supreme Court Appeal To The Cta en BancDocument1 pageOutline of Procedure in The Court of Tax Appeals (Cta) Appeal To The CTA Division Appeal To The Supreme Court Appeal To The Cta en BancRaymond RogacionNo ratings yet

- CTA Jurisdiction (Updated)Document2 pagesCTA Jurisdiction (Updated)Andie Player100% (1)

- CTA JurisdictionDocument6 pagesCTA JurisdictionUfbNo ratings yet

- Civil Aspect Collection CasesDocument18 pagesCivil Aspect Collection CasesHNicdaoNo ratings yet

- National Power Corporation vs. Municipal Government of NavotasDocument11 pagesNational Power Corporation vs. Municipal Government of NavotasEvelyn TocgongnaNo ratings yet

- A. Jurisdiction of The Court of Tax Appeals: 1. Civil CasesDocument7 pagesA. Jurisdiction of The Court of Tax Appeals: 1. Civil CasesRovi Anne IgoyNo ratings yet

- ASSOCIATED BANK Vs CADocument3 pagesASSOCIATED BANK Vs CACedric100% (1)

- Tax Reviewer: Law of Basic Taxation in The Philippines Chapter 8: Taxpayer'S RemediesDocument4 pagesTax Reviewer: Law of Basic Taxation in The Philippines Chapter 8: Taxpayer'S RemediesMariko IwakiNo ratings yet

- 4 Commissioner - of - Internal - Revenue - v. - CTA (RESOLUTION)Document6 pages4 Commissioner - of - Internal - Revenue - v. - CTA (RESOLUTION)ervingabralagbonNo ratings yet

- Mediation - Am No 11-1-5-Sc-PhiljaDocument11 pagesMediation - Am No 11-1-5-Sc-PhiljaAlNo ratings yet

- Tax2 TaxremDocument1 pageTax2 TaxremLeica JaymeNo ratings yet

- SMART and PILTEL Vs NTCDocument1 pageSMART and PILTEL Vs NTCShaira Mae CuevillasNo ratings yet

- City of Manila vs. Hon. Caridad Grecia-Cuerdo, RTC Pasay Et AlDocument6 pagesCity of Manila vs. Hon. Caridad Grecia-Cuerdo, RTC Pasay Et AlAP CruzNo ratings yet

- RemediesDocument14 pagesRemediesKent-Kent VillaceranNo ratings yet

- Rem Part IiDocument7 pagesRem Part IiVIctor AlfilerNo ratings yet

- 31 Insular Vs Far EastDocument14 pages31 Insular Vs Far EastFairyssa Bianca SagotNo ratings yet

- Insular Savings Bank v. Far East Bank and Trust CompanyDocument11 pagesInsular Savings Bank v. Far East Bank and Trust CompanyJoshua MaulaNo ratings yet

- Tax 2 NotesDocument3 pagesTax 2 NotesJoyceNo ratings yet

- CIR v. Hedcor Sibulan, Inc.Document2 pagesCIR v. Hedcor Sibulan, Inc.SophiaFrancescaEspinosa100% (1)

- Uniform LayoutDocument7 pagesUniform LayoutJade CoritanaNo ratings yet

- Court of Tax Appeals: by Anna Alyssa J. RobledoDocument52 pagesCourt of Tax Appeals: by Anna Alyssa J. RobledoVal Justin DeatrasNo ratings yet

- Chapter 9: Court Tax Appeals: Tax Reviewer: Law of Basic Taxation in The PhilippinesDocument4 pagesChapter 9: Court Tax Appeals: Tax Reviewer: Law of Basic Taxation in The PhilippinesMino GensonNo ratings yet

- Judicial Action Tax + CasesDocument28 pagesJudicial Action Tax + CasesGillian BrionesNo ratings yet

- Theory and Basis of TaxationDocument3 pagesTheory and Basis of TaxationBai Johara SinsuatNo ratings yet

- Bir Vs KepcoDocument2 pagesBir Vs KepcoJoseph SalidoNo ratings yet

- CLJ4 Chapter 9Document18 pagesCLJ4 Chapter 9Jules Karim A. AragonNo ratings yet

- BM 1755Document3 pagesBM 1755Faith TangoNo ratings yet

- Specpro ReviewerDocument24 pagesSpecpro Reviewerdaryl canozaNo ratings yet

- City of Manila Vs Judge CuerdoDocument21 pagesCity of Manila Vs Judge CuerdoRegina Rae LuzadasNo ratings yet

- Ursal V Court of Tax Appeals: Judicial RemediesDocument4 pagesUrsal V Court of Tax Appeals: Judicial RemediesAileen Love ReyesNo ratings yet

- I. Civil Procedure:: ST NDDocument4 pagesI. Civil Procedure:: ST NDRheaj AureoNo ratings yet

- Rule 42, Section 1-4 - MAGNODocument38 pagesRule 42, Section 1-4 - MAGNOMay RMNo ratings yet

- Commissioner of Internal Revenue vs. Kepco Ilijan Corporation G.R. No.199422, 21 June 2016Document2 pagesCommissioner of Internal Revenue vs. Kepco Ilijan Corporation G.R. No.199422, 21 June 2016Chiic-chiic SalamidaNo ratings yet

- Rule 42, Section 1-4 - MAGNODocument29 pagesRule 42, Section 1-4 - MAGNOMay RMNo ratings yet

- Adr - Emd Exam ReviewerDocument3 pagesAdr - Emd Exam ReviewerElycrisjoe Dela CuestaNo ratings yet

- Finals Personal Study Guide Tax2Document116 pagesFinals Personal Study Guide Tax2TeacherEliNo ratings yet

- Flowchart LGU TaxesDocument1 pageFlowchart LGU TaxesHermay BanarioNo ratings yet

- Admin - V - 3. Smart and Piltel Vs NTC GR No. 151908Document2 pagesAdmin - V - 3. Smart and Piltel Vs NTC GR No. 151908Ervin Franz Mayor CuevillasNo ratings yet

- Insular Savings Bank v. FEBTCDocument2 pagesInsular Savings Bank v. FEBTCHilary MostajoNo ratings yet

- Tax Flowchart Remedies (Tokie)Document9 pagesTax Flowchart Remedies (Tokie)Tokie TokiNo ratings yet

- LC Dismissed The Case W/o TM RTCDocument2 pagesLC Dismissed The Case W/o TM RTCMary Jobeth E. PallasigueNo ratings yet

- REM 1st AssignDocument9 pagesREM 1st AssignTokie TokiNo ratings yet

- California Supreme Court Petition: S173448 – Denied Without OpinionFrom EverandCalifornia Supreme Court Petition: S173448 – Denied Without OpinionRating: 4 out of 5 stars4/5 (1)

- SPL Notes FinalsDocument17 pagesSPL Notes FinalsJoh SuhNo ratings yet

- Special Commercial Laws Case DigestDocument29 pagesSpecial Commercial Laws Case DigestJoh SuhNo ratings yet

- Taxation ReviewerDocument9 pagesTaxation ReviewerJoh SuhNo ratings yet

- Arraignment PleaDocument4 pagesArraignment PleaJoh SuhNo ratings yet

- Anti Online Child PornographyDocument23 pagesAnti Online Child PornographyJoh SuhNo ratings yet

- Comm Rev NotesDocument4 pagesComm Rev NotesJoh SuhNo ratings yet

- Crim Law Lockdown Lecture - Art. 316 319Document7 pagesCrim Law Lockdown Lecture - Art. 316 319Joh SuhNo ratings yet

- Crim Law Lockdown Lecture - Art. 332Document3 pagesCrim Law Lockdown Lecture - Art. 332Joh SuhNo ratings yet

- Corpo Notes 01302023Document4 pagesCorpo Notes 01302023Joh SuhNo ratings yet

- Chapter 6 DEVELOPING STRATEGIC ALTERNATIVESDocument31 pagesChapter 6 DEVELOPING STRATEGIC ALTERNATIVESSheeza AsharNo ratings yet

- Sample 1673514368545Document2 pagesSample 1673514368545Sonm NegiNo ratings yet

- Gen Maths 07Document26 pagesGen Maths 07Sibin G ThomasNo ratings yet

- Dream2Success: About UsDocument3 pagesDream2Success: About UsGionee P2No ratings yet

- Fi32BPP Course NotesDocument384 pagesFi32BPP Course NotesZ XNNo ratings yet

- Market StructuresDocument59 pagesMarket StructuresCharlene Mae GraciasNo ratings yet

- Organizational Management Assignment On Coca ColaDocument11 pagesOrganizational Management Assignment On Coca ColaVix100% (1)

- Ledger TemplateDocument7 pagesLedger TemplateIts SaoirseNo ratings yet

- Complaint For Foreclosure of Real Estate MortgageDocument2 pagesComplaint For Foreclosure of Real Estate MortgageTere Tongson100% (1)

- 5.2 Cupcake ChallengeDocument294 pages5.2 Cupcake ChallengeNhlanhla MpofuNo ratings yet

- Indian Contract Act - IiDocument193 pagesIndian Contract Act - IiPramod ShuklaNo ratings yet

- The Performance Interest in The Law of TrustsDocument34 pagesThe Performance Interest in The Law of TrustsEve AthanasekouNo ratings yet

- CPE Presentation 1Document5 pagesCPE Presentation 1Carlos GarciaNo ratings yet

- Baby Bulls Mega Sectoral AnalysisDocument10 pagesBaby Bulls Mega Sectoral Analysisdaddyyankee995No ratings yet

- Mobile Banking: Mobile Banking Is A Service Provided by A Bank or Other Financial Institution That Allows ItsDocument11 pagesMobile Banking: Mobile Banking Is A Service Provided by A Bank or Other Financial Institution That Allows Itsএক মুঠো স্বপ্নNo ratings yet

- BrexitDocument8 pagesBrexitKomal RaniNo ratings yet

- Testing: Software Engineering Sommerville - Chapter 4,27 and 28Document29 pagesTesting: Software Engineering Sommerville - Chapter 4,27 and 28VCRajanNo ratings yet

- Online Agriculture Support System For Bridging Farmer-Consumer ExpectationsDocument4 pagesOnline Agriculture Support System For Bridging Farmer-Consumer ExpectationsInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- 17, 29 Dalisay Investments vs. SSS DigestDocument7 pages17, 29 Dalisay Investments vs. SSS DigestBay NazarenoNo ratings yet

- Supply Chain Management (3rd Edition) : Managing Economies of Scale in The Supply Chain: Cycle InventoryDocument45 pagesSupply Chain Management (3rd Edition) : Managing Economies of Scale in The Supply Chain: Cycle InventoryVinoadh Kumar KrishnanNo ratings yet

- Securityproductsmarketing AcasestudyDocument8 pagesSecurityproductsmarketing AcasestudyMuhammad Rehan NasirNo ratings yet

- Agro Tech Foods and The Branded Pulses SegmentDocument13 pagesAgro Tech Foods and The Branded Pulses SegmentManuel HijarNo ratings yet

- Crane Hire and Contract Lift-090626 PDFDocument6 pagesCrane Hire and Contract Lift-090626 PDFANIBAL MARQUEZNo ratings yet

- Presentation On MR Azim PremjiDocument13 pagesPresentation On MR Azim PremjiAnkur BhatiNo ratings yet

- Building On StrengthDocument292 pagesBuilding On StrengthSouradeep SanyalNo ratings yet

- Pune Institute of Business Management: BATCH 2019 - 2021Document24 pagesPune Institute of Business Management: BATCH 2019 - 2021Pragati ChaudharyNo ratings yet

- Student Profile BookDocument67 pagesStudent Profile BookGautam SharmaNo ratings yet

- Garment Manufacturing ProcessDocument54 pagesGarment Manufacturing Processroselyn ayensa100% (1)

- IPC PL 14 04 Issue 4Document27 pagesIPC PL 14 04 Issue 4saladinNo ratings yet