RBI

RBI

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5824)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- March 2008 CAIA Level II Sample Questions: Chartered Alternative Investment AnalystDocument35 pagesMarch 2008 CAIA Level II Sample Questions: Chartered Alternative Investment AnalystAnubhav Srivastava100% (1)

- UST WC Finance With AnswersDocument11 pagesUST WC Finance With AnswersPauline Kisha Castro100% (1)

- Chap - 4 ProblemsDocument2 pagesChap - 4 Problemspartha_biswas_uiuNo ratings yet

- (Sffis: The 8tel. 735 9807 AccountancyDocument18 pages(Sffis: The 8tel. 735 9807 AccountancyCharry RamosNo ratings yet

- Distance Education: Instructional ModuleDocument11 pagesDistance Education: Instructional ModuleRD Suarez83% (6)

- Balance Sheet Net PP&EDocument13 pagesBalance Sheet Net PP&Esalimanderz813No ratings yet

- Subsequent Measurement:: Differ in Inventory ValueDocument4 pagesSubsequent Measurement:: Differ in Inventory ValueCharina Jane PascualNo ratings yet

- Chan-A Comparison of Government Accounting and Business AccountingDocument13 pagesChan-A Comparison of Government Accounting and Business AccountingAndy LincolnNo ratings yet

- REPUBLIC ACT No 10846 (Sec.8-13)Document3 pagesREPUBLIC ACT No 10846 (Sec.8-13)School FilesNo ratings yet

- Financial Management 2 Test 2Document3 pagesFinancial Management 2 Test 2William MushongaNo ratings yet

- Gianluca Fusai Resume October 2016Document10 pagesGianluca Fusai Resume October 2016dioguinhoNo ratings yet

- Foreign Exchange Business PlanDocument8 pagesForeign Exchange Business PlanbillrocksNo ratings yet

- Fno Profit & Loss Report From 01 Apr 2021 ToDocument8 pagesFno Profit & Loss Report From 01 Apr 2021 ToSourabh AhujaNo ratings yet

- SIX Swiss Exchange Swiss Leader Index (SLI) FactsheetDocument4 pagesSIX Swiss Exchange Swiss Leader Index (SLI) FactsheetjennabushNo ratings yet

- MGMT 41150 - Chapter 15 - The Black-Scholes-Merton ModelDocument49 pagesMGMT 41150 - Chapter 15 - The Black-Scholes-Merton ModelLaxus DreyerNo ratings yet

- Glosar NabavkiDocument20 pagesGlosar NabavkiSandra GlišićNo ratings yet

- Affiance Capital PDFDocument6 pagesAffiance Capital PDFTrice KabundiNo ratings yet

- Disagreement of BPJS: by Mafruhatun Nadhifah & Mayang Mustika Dewi TariganDocument7 pagesDisagreement of BPJS: by Mafruhatun Nadhifah & Mayang Mustika Dewi TariganMayang Mustika Dewi TariganNo ratings yet

- Taxation Law 2007 Bar Question and AnswerDocument12 pagesTaxation Law 2007 Bar Question and AnswerHenry M. Macatuno Jr.No ratings yet

- TCS 10 Year Financial Statement FinalDocument14 pagesTCS 10 Year Financial Statement Finalgaurav sahuNo ratings yet

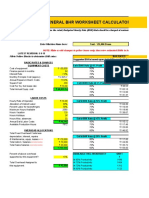

- General BHR Worksheet CalculatorDocument2 pagesGeneral BHR Worksheet CalculatorEmba MadrasNo ratings yet

- Ratio Analysis of Hero Honda 2007-2008: Prepared byDocument25 pagesRatio Analysis of Hero Honda 2007-2008: Prepared byAkanksha RajanNo ratings yet

- Giaa 0919Document146 pagesGiaa 0919Zaa ZahrohNo ratings yet

- Online Banking - WikipediaDocument39 pagesOnline Banking - WikipediaAjay RathodNo ratings yet

- Pid 58667064 - IpDocument6 pagesPid 58667064 - IpTrent RobertsenNo ratings yet

- A Comparative Study On Investment Policy of Nepalese Commercial BankDocument5 pagesA Comparative Study On Investment Policy of Nepalese Commercial Bankdevi ghimireNo ratings yet

- Wells Fargo StatementDocument4 pagesWells Fargo Statementandy0% (1)

- Theory Questions (1-7)Document2 pagesTheory Questions (1-7)sharmadisha0703No ratings yet

- Isurance CarDocument506 pagesIsurance CarLatif SugandiNo ratings yet

- Final Summer Training ReportDocument76 pagesFinal Summer Training Reportjavedaliamu100% (1)

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5824)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- March 2008 CAIA Level II Sample Questions: Chartered Alternative Investment AnalystDocument35 pagesMarch 2008 CAIA Level II Sample Questions: Chartered Alternative Investment AnalystAnubhav Srivastava100% (1)

- UST WC Finance With AnswersDocument11 pagesUST WC Finance With AnswersPauline Kisha Castro100% (1)

- Chap - 4 ProblemsDocument2 pagesChap - 4 Problemspartha_biswas_uiuNo ratings yet

- (Sffis: The 8tel. 735 9807 AccountancyDocument18 pages(Sffis: The 8tel. 735 9807 AccountancyCharry RamosNo ratings yet

- Distance Education: Instructional ModuleDocument11 pagesDistance Education: Instructional ModuleRD Suarez83% (6)

- Balance Sheet Net PP&EDocument13 pagesBalance Sheet Net PP&Esalimanderz813No ratings yet

- Subsequent Measurement:: Differ in Inventory ValueDocument4 pagesSubsequent Measurement:: Differ in Inventory ValueCharina Jane PascualNo ratings yet

- Chan-A Comparison of Government Accounting and Business AccountingDocument13 pagesChan-A Comparison of Government Accounting and Business AccountingAndy LincolnNo ratings yet

- REPUBLIC ACT No 10846 (Sec.8-13)Document3 pagesREPUBLIC ACT No 10846 (Sec.8-13)School FilesNo ratings yet

- Financial Management 2 Test 2Document3 pagesFinancial Management 2 Test 2William MushongaNo ratings yet

- Gianluca Fusai Resume October 2016Document10 pagesGianluca Fusai Resume October 2016dioguinhoNo ratings yet

- Foreign Exchange Business PlanDocument8 pagesForeign Exchange Business PlanbillrocksNo ratings yet

- Fno Profit & Loss Report From 01 Apr 2021 ToDocument8 pagesFno Profit & Loss Report From 01 Apr 2021 ToSourabh AhujaNo ratings yet

- SIX Swiss Exchange Swiss Leader Index (SLI) FactsheetDocument4 pagesSIX Swiss Exchange Swiss Leader Index (SLI) FactsheetjennabushNo ratings yet

- MGMT 41150 - Chapter 15 - The Black-Scholes-Merton ModelDocument49 pagesMGMT 41150 - Chapter 15 - The Black-Scholes-Merton ModelLaxus DreyerNo ratings yet

- Glosar NabavkiDocument20 pagesGlosar NabavkiSandra GlišićNo ratings yet

- Affiance Capital PDFDocument6 pagesAffiance Capital PDFTrice KabundiNo ratings yet

- Disagreement of BPJS: by Mafruhatun Nadhifah & Mayang Mustika Dewi TariganDocument7 pagesDisagreement of BPJS: by Mafruhatun Nadhifah & Mayang Mustika Dewi TariganMayang Mustika Dewi TariganNo ratings yet

- Taxation Law 2007 Bar Question and AnswerDocument12 pagesTaxation Law 2007 Bar Question and AnswerHenry M. Macatuno Jr.No ratings yet

- TCS 10 Year Financial Statement FinalDocument14 pagesTCS 10 Year Financial Statement Finalgaurav sahuNo ratings yet

- General BHR Worksheet CalculatorDocument2 pagesGeneral BHR Worksheet CalculatorEmba MadrasNo ratings yet

- Ratio Analysis of Hero Honda 2007-2008: Prepared byDocument25 pagesRatio Analysis of Hero Honda 2007-2008: Prepared byAkanksha RajanNo ratings yet

- Giaa 0919Document146 pagesGiaa 0919Zaa ZahrohNo ratings yet

- Online Banking - WikipediaDocument39 pagesOnline Banking - WikipediaAjay RathodNo ratings yet

- Pid 58667064 - IpDocument6 pagesPid 58667064 - IpTrent RobertsenNo ratings yet

- A Comparative Study On Investment Policy of Nepalese Commercial BankDocument5 pagesA Comparative Study On Investment Policy of Nepalese Commercial Bankdevi ghimireNo ratings yet

- Wells Fargo StatementDocument4 pagesWells Fargo Statementandy0% (1)

- Theory Questions (1-7)Document2 pagesTheory Questions (1-7)sharmadisha0703No ratings yet

- Isurance CarDocument506 pagesIsurance CarLatif SugandiNo ratings yet

- Final Summer Training ReportDocument76 pagesFinal Summer Training Reportjavedaliamu100% (1)