Download as pdf or txt

You might also like

- Recording Transactions Under PERPETUAL INVENTORY SYSTEMDocument6 pagesRecording Transactions Under PERPETUAL INVENTORY SYSTEMJalieca Lumbria Gadong0% (1)

- ADM-SHS-StatProb-Q3-M10-Illustrating A Normal Random Variable and Its CharacteristicsDocument27 pagesADM-SHS-StatProb-Q3-M10-Illustrating A Normal Random Variable and Its CharacteristicsSitti Halima Amilbahar AdgesNo ratings yet

- 2 CHAPTER Lesson 2 1 AssetsDocument6 pages2 CHAPTER Lesson 2 1 AssetsRegine BaterisnaNo ratings yet

- AcctgDocument28 pagesAcctgcarla i100% (2)

- Fundamentals of Accountancy, Business and Management 1 (FABM 1)Document12 pagesFundamentals of Accountancy, Business and Management 1 (FABM 1)trek boiNo ratings yet

- Merchandising Accounting Cycle: Periodic: Subject-Descriptive Title Subject - CodeDocument22 pagesMerchandising Accounting Cycle: Periodic: Subject-Descriptive Title Subject - CodeRose LaureanoNo ratings yet

- Accounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloDocument41 pagesAccounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloRoxe XNo ratings yet

- JOURNALIZINGDocument2 pagesJOURNALIZINGArneld SantiagoNo ratings yet

- Lecture Notes - Chapter 7Document17 pagesLecture Notes - Chapter 7Nova Grace LatinaNo ratings yet

- Chapter 1 Introduction To AccountingDocument51 pagesChapter 1 Introduction To AccountingHeisei De LunaNo ratings yet

- Pages 178Document7 pagesPages 178Krestyl Ann GabaldaNo ratings yet

- Exercise 3 Leah GarciaDocument12 pagesExercise 3 Leah GarciaMa Sophia Mikaela EreceNo ratings yet

- 2nd ActivityDocument2 pages2nd ActivityResaa100% (1)

- Accounting Cycle and Book of AccountsDocument23 pagesAccounting Cycle and Book of AccountsChaaaNo ratings yet

- Fundamentals of Accounting Practice Test 1: I. DirectionDocument4 pagesFundamentals of Accounting Practice Test 1: I. DirectionNorie EcijaNo ratings yet

- ABM 3 Quarterly ExamDocument2 pagesABM 3 Quarterly ExamLenyBarrogaNo ratings yet

- 7FABM 1 Module Accounting EquationDocument6 pages7FABM 1 Module Accounting EquationKristhine DarvinNo ratings yet

- This Study Resource Was Shared ViaDocument8 pagesThis Study Resource Was Shared Viadave iganoNo ratings yet

- Answer This To Be Checked On Tuesday, September 21, 2021Document2 pagesAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNo ratings yet

- Midterm - Chapter 4Document78 pagesMidterm - Chapter 4JoshrylNo ratings yet

- Dental Clinic AnswerDocument16 pagesDental Clinic AnswerMaria Licuanan100% (1)

- FABM ActivityDocument3 pagesFABM ActivityRey VillaNo ratings yet

- Accounting For Merchandising BusinessDocument88 pagesAccounting For Merchandising BusinessRonnell Vic Cañeda YuNo ratings yet

- 4.3. Obligations of Borrowers: Questions To PonderDocument6 pages4.3. Obligations of Borrowers: Questions To PonderTin CabosNo ratings yet

- Chapter 10 Special JournalsDocument5 pagesChapter 10 Special JournalsPaw VerdilloNo ratings yet

- Accounting 101Document17 pagesAccounting 101Jenne Santiago BabantoNo ratings yet

- Fabm 1 ExamDocument2 pagesFabm 1 ExamJasfer Niño100% (1)

- Lesson 5 Analyzing Business Transactions PDFDocument25 pagesLesson 5 Analyzing Business Transactions PDFZybel RosalesNo ratings yet

- Chapter 09Document12 pagesChapter 09Dan ChuaNo ratings yet

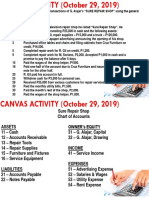

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 pagesCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- Unit II Lesson 5 and 6 ADJUSTING ENTRIES and FSDocument25 pagesUnit II Lesson 5 and 6 ADJUSTING ENTRIES and FSAlezandra SantelicesNo ratings yet

- Practical Accounting 1Document90 pagesPractical Accounting 1Honie Rose MondayNo ratings yet

- Integrated Accounting Learning Module Attachment (Do Not Copy)Document15 pagesIntegrated Accounting Learning Module Attachment (Do Not Copy)Jasper PelicanoNo ratings yet

- Accounting Cycle of A Service Business-ExerciseDocument50 pagesAccounting Cycle of A Service Business-ExerciseHannah GarciaNo ratings yet

- 01 Quiz 1Document2 pages01 Quiz 1Laisan SantosNo ratings yet

- Analysis of Financial Statements Mix RatioDocument30 pagesAnalysis of Financial Statements Mix RatioBianca Angela Camayra QuiaNo ratings yet

- Steps in The Accounting Cycle of A Service Business (Posting and Preparing Trial Balance)Document15 pagesSteps in The Accounting Cycle of A Service Business (Posting and Preparing Trial Balance)Zybel RosalesNo ratings yet

- PeriodicDocument23 pagesPeriodicalmorsNo ratings yet

- Adjusting EntriesDocument6 pagesAdjusting EntriesJanna PleteNo ratings yet

- Laurente Cleaning Services LedgerDocument3 pagesLaurente Cleaning Services LedgerAriel Palay100% (1)

- Journalizing ProcessDocument32 pagesJournalizing ProcessMarquez, Lynn Andrea L.No ratings yet

- Aef BsaDocument3 pagesAef BsaAdrian Ivashkov100% (1)

- Quiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeDocument6 pagesQuiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeJOHN MITCHELL GALLARDONo ratings yet

- Inancial CCTG: Adjusting The AccountsDocument28 pagesInancial CCTG: Adjusting The AccountsLj BesaNo ratings yet

- Financial Statement ExamDocument2 pagesFinancial Statement ExamTam TamNo ratings yet

- Accounting For Merchandising Business: Learning OutcomesDocument15 pagesAccounting For Merchandising Business: Learning OutcomesJuan Dela Cruz100% (1)

- ABM PM 2nd QTR SLM Week12Document9 pagesABM PM 2nd QTR SLM Week12ganda dyosaNo ratings yet

- Chapter 2 ActivityDocument10 pagesChapter 2 ActivityBELARMINO LOUIE A.No ratings yet

- Sample Compilation of RRLDocument4 pagesSample Compilation of RRLTyrelle CastilloNo ratings yet

- Financial Accounting and ReportingDocument1 pageFinancial Accounting and ReportingPaula BautistaNo ratings yet

- ACTIVITY 1 MabalaDocument5 pagesACTIVITY 1 MabalaJulie mabuyoNo ratings yet

- ACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsDocument1 pageACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsMiguel Lulab100% (1)

- I. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1Document3 pagesI. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1HLeigh Nietes-GabutanNo ratings yet

- Practice Problem 11.0: Name Date Course/Year ScoreDocument5 pagesPractice Problem 11.0: Name Date Course/Year ScoreCatherine GonzalesNo ratings yet

- Cash FlowDocument2 pagesCash FlowJasmine ActaNo ratings yet

- CH 03Document7 pagesCH 03Bind Prozt100% (1)

- Quiz SolutionDocument3 pagesQuiz SolutionKim Patrick VictoriaNo ratings yet

- FABM 2 Module 1Document16 pagesFABM 2 Module 1Rene Castillo JrNo ratings yet

- Senior 12 FABM2 Q1 - M7Document20 pagesSenior 12 FABM2 Q1 - M7Sitti Halima Amilbahar AdgesNo ratings yet

- FABM2 Module 1. Statement of Financial PositionDocument10 pagesFABM2 Module 1. Statement of Financial PositionSITTIE RAYMAH ABDULLAHNo ratings yet

- Fundamentals of ABM1 - Q4 - LAS7 DRAFTDocument15 pagesFundamentals of ABM1 - Q4 - LAS7 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- Fundamentals of ABM1 - Q4 - LAS2 DRAFTDocument10 pagesFundamentals of ABM1 - Q4 - LAS2 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- Fundamentals of ABM1 - Q4 - LAS1 DRAFTDocument17 pagesFundamentals of ABM1 - Q4 - LAS1 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- Senior 12 FABM2 Q1 - M8Document22 pagesSenior 12 FABM2 Q1 - M8Sitti Halima Amilbahar AdgesNo ratings yet

- ArabicNumberChart 1Document1 pageArabicNumberChart 1Sitti Halima Amilbahar AdgesNo ratings yet

- Senior 12 FABM2 Q1 - M7Document20 pagesSenior 12 FABM2 Q1 - M7Sitti Halima Amilbahar AdgesNo ratings yet

- Senior 12 FABM2 Q1 - M6Document25 pagesSenior 12 FABM2 Q1 - M6Sitti Halima Amilbahar AdgesNo ratings yet

- Poetry and Creative NonfictionDocument1 pagePoetry and Creative NonfictionSitti Halima Amilbahar AdgesNo ratings yet

- Code of Ethics of Professional TeachersDocument18 pagesCode of Ethics of Professional TeachersSitti Halima Amilbahar AdgesNo ratings yet

- Learning ResourcesDocument13 pagesLearning ResourcesSitti Halima Amilbahar AdgesNo ratings yet

- Creative Nonfiction Midterm ExaminationDocument2 pagesCreative Nonfiction Midterm ExaminationSitti Halima Amilbahar AdgesNo ratings yet

- UntitledDocument5 pagesUntitledSitti Halima Amilbahar AdgesNo ratings yet

- ADM-SHS-StatProb-Q3-M3-Finding Possible Values of A Random VariableDocument27 pagesADM-SHS-StatProb-Q3-M3-Finding Possible Values of A Random VariableSitti Halima Amilbahar AdgesNo ratings yet

- ADM SHS StatProb Q3 M8 Interpreting Mean and Variance of A Discrete Random Variable - Version 2nndlDocument27 pagesADM SHS StatProb Q3 M8 Interpreting Mean and Variance of A Discrete Random Variable - Version 2nndlSitti Halima Amilbahar AdgesNo ratings yet

- ADM-SHS-StatProb-Q3-M5-Computing Probability Corresponding To A Given Random VariableDocument27 pagesADM-SHS-StatProb-Q3-M5-Computing Probability Corresponding To A Given Random VariableSitti Halima Amilbahar AdgesNo ratings yet

- Cost Volume Profit AnalysisDocument4 pagesCost Volume Profit AnalysisSitti Halima Amilbahar AdgesNo ratings yet

- ADM SHS StatProb Q3 M1 Illustrates Random Variables Discrete and Continuous - Version 1.final 1Document27 pagesADM SHS StatProb Q3 M1 Illustrates Random Variables Discrete and Continuous - Version 1.final 1Sitti Halima Amilbahar AdgesNo ratings yet

- ADM-SHS-StatProb-Q3-M12-Converting A Normal Random Variable To A Standard Normal Variable and Vice-VersaDocument27 pagesADM-SHS-StatProb-Q3-M12-Converting A Normal Random Variable To A Standard Normal Variable and Vice-VersaSitti Halima Amilbahar AdgesNo ratings yet