Download as pdf or txt

You might also like

- Kenmare Architects LTD Kal Was Incorporated and Commenced Operations OnDocument1 pageKenmare Architects LTD Kal Was Incorporated and Commenced Operations OnMiroslav GegoskiNo ratings yet

- Use The Following Information For Items 1 To 5:: Chapter 5 - Problem 1: True or FalseDocument33 pagesUse The Following Information For Items 1 To 5:: Chapter 5 - Problem 1: True or FalseAlarich Catayoc80% (5)

- Corporate Financial Distress, Restructuring, and Bankruptcy: Analyze Leveraged Finance, Distressed Debt, and BankruptcyFrom EverandCorporate Financial Distress, Restructuring, and Bankruptcy: Analyze Leveraged Finance, Distressed Debt, and BankruptcyNo ratings yet

- WEL TB PAY002 Account Activation Form PDFDocument1 pageWEL TB PAY002 Account Activation Form PDFAnonymous Z6ve7AqWKNo ratings yet

- FA (1st) May2019 2Document3 pagesFA (1st) May2019 2Darsh KumarNo ratings yet

- Accounting For Managers Model Question Paper-2: First Semester MBA Degree ExaminationDocument5 pagesAccounting For Managers Model Question Paper-2: First Semester MBA Degree ExaminationRohan Chaugule0% (1)

- Basic Accounting: Instructions To CandidatesDocument2 pagesBasic Accounting: Instructions To CandidatesCheena PanjolaNo ratings yet

- Financial Accounting: Instructions To CandidatesDocument3 pagesFinancial Accounting: Instructions To CandidatesKudlappa AiholliNo ratings yet

- CA Bcom PH 3rd Sem 2016Document7 pagesCA Bcom PH 3rd Sem 2016Gursirat KaurNo ratings yet

- Bba 208Document3 pagesBba 208armaanNo ratings yet

- TB 6Document2 pagesTB 6Louiza Kyla AridaNo ratings yet

- Adobe Scan Aug 19, 2022Document11 pagesAdobe Scan Aug 19, 2022Purushottam YadhuvanshiNo ratings yet

- 3054 Faca-V L 8Document8 pages3054 Faca-V L 8ab6154951No ratings yet

- FA (1st) May2018Document3 pagesFA (1st) May2018JahangirNo ratings yet

- Income Tax-I: Write Short NotesDocument3 pagesIncome Tax-I: Write Short NotesHappy PaulNo ratings yet

- FA (1st) Dec2017Document3 pagesFA (1st) Dec2017dkdjfNo ratings yet

- Accounting Refresher Course 1 Advance Financial Accounting and Reporting Corporate LiquidationDocument1 pageAccounting Refresher Course 1 Advance Financial Accounting and Reporting Corporate LiquidationNyra BeldoroNo ratings yet

- CLASS XI ACCOUNTANCY 8.financial Statement of Sole Proprietorship and Accounts From Incomplete Records (COMPETENCY - BASED TEST ITEMS) MARKS WISEDocument18 pagesCLASS XI ACCOUNTANCY 8.financial Statement of Sole Proprietorship and Accounts From Incomplete Records (COMPETENCY - BASED TEST ITEMS) MARKS WISEgowtham.ttfaNo ratings yet

- Quiz 2 - Corp Liqui and Installment SalesDocument8 pagesQuiz 2 - Corp Liqui and Installment SalesKenneth Christian WilburNo ratings yet

- Corporate Account IIDocument7 pagesCorporate Account IIalphadark72No ratings yet

- MID-TERM Adv - Actg. 1 (No Answer)Document10 pagesMID-TERM Adv - Actg. 1 (No Answer)Jose Benzon100% (1)

- IPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDocument6 pagesIPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDrShailesh Singh ThakurNo ratings yet

- Accounting For Special Transactions Midterm Examination: Use The Following Information For The Next Two QuestionsDocument13 pagesAccounting For Special Transactions Midterm Examination: Use The Following Information For The Next Two QuestionsAndrew wigginNo ratings yet

- 6.accounting For DebenturesDocument22 pages6.accounting For Debenturestripatjotkaur757No ratings yet

- Class Xii Accountancy 6.accounting For Debentures Competency - Based Test ItemsDocument33 pagesClass Xii Accountancy 6.accounting For Debentures Competency - Based Test ItemsjashanjeetNo ratings yet

- Accountancy Worksheets 4Document15 pagesAccountancy Worksheets 4devanshubhattacharya018No ratings yet

- QP CODE: 22100973: Reg No: NameDocument6 pagesQP CODE: 22100973: Reg No: NameSajithaNo ratings yet

- Ca-Ii May 2022Document6 pagesCa-Ii May 2022Gayathri V GNo ratings yet

- IInd Sem Final Exam Corporate Accounting June-2023Document2 pagesIInd Sem Final Exam Corporate Accounting June-2023tomarsimran55No ratings yet

- Unit 3 Amalgamation and Absorption For ClassDocument4 pagesUnit 3 Amalgamation and Absorption For ClassanshNo ratings yet

- 03-Partnership Liquidation Quiz2Document6 pages03-Partnership Liquidation Quiz2JiddahNo ratings yet

- Adv Acc QN Bank Compiler PDF With Imp Questions - n22Document500 pagesAdv Acc QN Bank Compiler PDF With Imp Questions - n22harshita23hrNo ratings yet

- PDF Midterm Exam Ast With Answers CompressDocument15 pagesPDF Midterm Exam Ast With Answers CompressSarah Del RosarioNo ratings yet

- 3562 Question PaperDocument3 pages3562 Question PaperKimberly MataruseNo ratings yet

- 588c69bdc763b - Sample Paper Accountancy - 230102 - 185610Document7 pages588c69bdc763b - Sample Paper Accountancy - 230102 - 185610sanchitchaudhary431No ratings yet

- Finals 2019Document4 pagesFinals 2019GargiNo ratings yet

- Admission of A Partner PDFDocument8 pagesAdmission of A Partner PDFSpandan DasNo ratings yet

- Capital Reduction 2Document6 pagesCapital Reduction 2SANJIB SHARMANo ratings yet

- SPECTRANS Chapter-17-Corporate-Liquidations-And-ReorganizationsDocument17 pagesSPECTRANS Chapter-17-Corporate-Liquidations-And-ReorganizationsLiberty NovaNo ratings yet

- 14 Corporate Accounting - April May 2021 (Repeaters 2013-14 and Onwards)Document8 pages14 Corporate Accounting - April May 2021 (Repeaters 2013-14 and Onwards)premium info2222No ratings yet

- Partner Ship - IIDocument6 pagesPartner Ship - IIM JEEVARATHNAM NAIDUNo ratings yet

- ElementsBookKeepingAccountancy SQPDocument7 pagesElementsBookKeepingAccountancy SQPKanya PrakashNo ratings yet

- PT 06 (Partnership) (5 Dec)Document8 pagesPT 06 (Partnership) (5 Dec)Rajesh Kumar100% (2)

- Corporate Accounting Ii 2020Document4 pagesCorporate Accounting Ii 2020joe josephNo ratings yet

- Financial Accounting NotesDocument7 pagesFinancial Accounting NotessrishaaNo ratings yet

- The Accounting Process: Name: Date: Professor: Section: Score: QuizDocument6 pagesThe Accounting Process: Name: Date: Professor: Section: Score: QuizAllyna Jane Enriquez100% (1)

- y 78 Ei 4 JkwagshbkjdDocument5 pagesy 78 Ei 4 JkwagshbkjdJenilyn CalaraNo ratings yet

- Ratio AnalysisDocument24 pagesRatio AnalysisBISHAL ROYNo ratings yet

- Afar 02: Corporate Liquidation: I. True or False - Theory of AccountsDocument5 pagesAfar 02: Corporate Liquidation: I. True or False - Theory of AccountsRoxell CaibogNo ratings yet

- 943 Question PaperDocument3 pages943 Question PaperPacific TigerNo ratings yet

- Corporate Liquidation Quiz 5docxDocument5 pagesCorporate Liquidation Quiz 5docxAngelica Duarte33% (6)

- Paper - 1: Advanced Accounting: Answer All QuestionsDocument22 pagesPaper - 1: Advanced Accounting: Answer All Questionsmakarand8july78100% (1)

- Adv Acc - Buy Back and LiquidationDocument15 pagesAdv Acc - Buy Back and Liquidationrshyams165No ratings yet

- B.B.A., Sem.-III CC-202 Fundamentals of Financial Management-2017Document4 pagesB.B.A., Sem.-III CC-202 Fundamentals of Financial Management-2017Harshit MistryNo ratings yet

- Management Accounting: Instructions To CandidatesDocument3 pagesManagement Accounting: Instructions To CandidatessumanNo ratings yet

- Test-Bank-Advanced-Accounting-3 By-Jeter-10-ChapterDocument20 pagesTest-Bank-Advanced-Accounting-3 By-Jeter-10-Chapterjhean dabatosNo ratings yet

- Final Exam Advance Accounting WADocument5 pagesFinal Exam Advance Accounting WAShawn OrganoNo ratings yet

- Cbse Class 11 Accountancy Sample Paper Set 1 QuestionsDocument6 pagesCbse Class 11 Accountancy Sample Paper Set 1 QuestionsNishtha 3153No ratings yet

- Chapter 17 Corporate Liquidations and ReorganizationsDocument16 pagesChapter 17 Corporate Liquidations and ReorganizationsMarvin ClementeNo ratings yet

- The Handbook of Credit Risk Management: Originating, Assessing, and Managing Credit ExposuresFrom EverandThe Handbook of Credit Risk Management: Originating, Assessing, and Managing Credit ExposuresNo ratings yet

- Depreciation Reports in British Columbia: The Strata Lots Owners Guide to Selecting Your Provider and Understanding Your ReportFrom EverandDepreciation Reports in British Columbia: The Strata Lots Owners Guide to Selecting Your Provider and Understanding Your ReportNo ratings yet

- Entrepreneurship Development: Instructions To CandidatesDocument2 pagesEntrepreneurship Development: Instructions To CandidatesDeepanshu SainiNo ratings yet

- UntitledDocument2 pagesUntitledDeepanshu SainiNo ratings yet

- UntitledDocument2 pagesUntitledDeepanshu SainiNo ratings yet

- UntitledDocument2 pagesUntitledDeepanshu SainiNo ratings yet

- Mahusay - Bsa211 - Module 2 Self ExercisesDocument6 pagesMahusay - Bsa211 - Module 2 Self ExercisesJeth Mahusay100% (1)

- Understanding The 3 Financial Statements 1653805473Document11 pagesUnderstanding The 3 Financial Statements 1653805473RaikhanNo ratings yet

- US Small Business Administration Disaster Loan Information For August StormDocument2 pagesUS Small Business Administration Disaster Loan Information For August StormKaren WallNo ratings yet

- Eight Reasons Concerned Seniors Purchase Final Expense PlansDocument2 pagesEight Reasons Concerned Seniors Purchase Final Expense PlansNatali FialloNo ratings yet

- Chapter 5 Advanced AccountingDocument19 pagesChapter 5 Advanced AccountingMarife De Leon VillalonNo ratings yet

- Timeline of The Lehman Brothers CollapseDocument3 pagesTimeline of The Lehman Brothers CollapseJonas MondalaNo ratings yet

- Sop For Client Purchase of PropertyDocument3 pagesSop For Client Purchase of PropertyMary FuntoNo ratings yet

- OLAYANJU - FinTech Regulatory Framework PDFDocument28 pagesOLAYANJU - FinTech Regulatory Framework PDFAjiboye Tooni100% (1)

- Canadian IBA Wire and AFT Instructions - CAD4171Document2 pagesCanadian IBA Wire and AFT Instructions - CAD4171Roshan MadusankaNo ratings yet

- Guerrero CH14 - ProblemsDocument14 pagesGuerrero CH14 - ProblemsClaireNo ratings yet

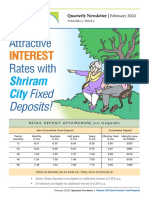

- Attractive Rates With: InterestDocument4 pagesAttractive Rates With: Interestdharam singhNo ratings yet

- Insurance Note Taking GuideDocument2 pagesInsurance Note Taking Guideapi-2523918430% (1)

- Accounting - Basics - Deloitte. 1Document56 pagesAccounting - Basics - Deloitte. 1Shubh100% (1)

- Stevens Textiles S 2010 Financial Statements Are Shown BelowDocument1 pageStevens Textiles S 2010 Financial Statements Are Shown BelowAmit PandeyNo ratings yet

- Checklist Advancepayment UpdatedDocument4 pagesChecklist Advancepayment UpdatedAlyyssa Julfa ArcenoNo ratings yet

- Important Instructions For Filling Ach Mandate Form: HdfcbankltdDocument1 pageImportant Instructions For Filling Ach Mandate Form: HdfcbankltdFUTURE NEXTTIMENo ratings yet

- SEC v. Goldman Sachs & Co - Summary of ComplaintDocument2 pagesSEC v. Goldman Sachs & Co - Summary of ComplaintGeorge ConkNo ratings yet

- C5 - Discounting and Accumulating PDFDocument33 pagesC5 - Discounting and Accumulating PDFhairil haqeemNo ratings yet

- Assignment - DBB2203 - BBA 4 - Set 1 and 2 - Aug-Sep - 2022Document3 pagesAssignment - DBB2203 - BBA 4 - Set 1 and 2 - Aug-Sep - 2022aishuNo ratings yet

- Chapter 1 Quickbooks Online Test Drive NovellaDocument52 pagesChapter 1 Quickbooks Online Test Drive NovellaBest IT ProductsNo ratings yet

- Percuma Punya SoftwareDocument80 pagesPercuma Punya SoftwareSitus Teknik SipilNo ratings yet

- Operating Assets: Property, Plant, and Equipment, Natural Resources & IntangiblesDocument37 pagesOperating Assets: Property, Plant, and Equipment, Natural Resources & Intangiblesakram oukNo ratings yet

- AFAR First Preboard May 2023 BatchDocument14 pagesAFAR First Preboard May 2023 BatchRhea Mae CarantoNo ratings yet

- Ratio Analysis (Divya Jadi Booti)Document85 pagesRatio Analysis (Divya Jadi Booti)Michael AdhikariNo ratings yet

- SIMPLE DEFERRED ANNUITY (For DEMO)Document86 pagesSIMPLE DEFERRED ANNUITY (For DEMO)JuanitoNo ratings yet

- Rosoft Office PowerPoint PresentationDocument13 pagesRosoft Office PowerPoint PresentationNancy VermaNo ratings yet

- Mett International Pty LTD Financial Forecast 3 Year SummaryDocument134 pagesMett International Pty LTD Financial Forecast 3 Year SummaryJamilexNo ratings yet

- Latihan Jurnal Khusus Praktika Akuntansi Per. DagangDocument14 pagesLatihan Jurnal Khusus Praktika Akuntansi Per. DagangAzka Yasfa UgaNo ratings yet